Chapter 5

Accounting for Merchandising

Operations

QUESTIONS

1. Merchandising companies report Merchandise Inventory on the balance sheet,

2. Additional accounts of a merchandising company likely include Merchandise

3. A company can have a net loss if its expenses (absent cost of goods sold) are

4. A cash discount can be offered to encourage customers to promptly pay. This

5. For a perpetual inventory system, inventory shrinkage is determined by taking a

6. Cash discounts are granted in return for early payment and reduce the amount

paid below the negotiated price. Cash discounts are recorded in the accounting

7. Sales discount is a term used by a seller to describe a cash discount granted to a

8. A manager is concerned about the quantity of its purchase returns because the

9. The sender (maker) of a debit memorandum records a debit in an account of the

recipient; and the recipient records a credit in an account maintained for the sender.

5-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

10. The single-step income statement format presents cost of goods sold and expenses

in one list, totals the list, and subtracts the total from net sales in one step. The

11. Apple calls its inventory account “Inventories.” A detailed calculation of

cost of goods sold is not presented by Apple.

12. Google titles its cost of sales accounts as “Cost of revenues” Google

13. Samsung titles its cost of goods sold account “Cost of sales.”

15. A buyer should attempt to negotiate the shipping terms FOB destination. In

QUICK STUDIES

Quick Study 5-1 (10 minutes)

1. G. 6. H.

Quick Study 5-2 (5 minutes)

Answer: d

5-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Quick Study 5-3 (15 minutes)

Computation of net income:

Krug Service Co.

Revenues………………………………………….. $14,000

Kleiner Merchandising Co.

Sales………………………………………………… $ 9,500

*Computation of cost of goods sold: _

Beginning inventory $ 5,000

Quick Study 5-4 (15 minutes)

Nov. 5 Merchandise Inventory ………………………………. 6,000

Nov. 7 Accounts Payable ……………………………………… 250

Nov. 15 Accounts Payable …………………………………….. 5,750

5-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Quick Study 5-5 (10 minutes)

a)

Aug. 1 Merchandise Inventory……………………………….. 60,000

b)

Aug. 11 Accounts Payable………………………………………. 60,000

Quick Study 5-6 (10 minutes)

a)

Sept. 15 Merchandise Inventory……………………………….. 35,000

b)

Sept. 28 Accounts Payable………………………………………. 35,000

5-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Quick Study 5-7 (10 minutes)

Apr. 1 Accounts Receivable ……………………………… 3,000

Sales ……………………………………………… 3,000

To record credit sale.

11 Cash ……………………………………………………… 2,352

Sales Discounts* ……………………………………. 48

Quick Study 5-8 (10 minutes)

July 31 Cost of Goods Sold …………………………….. 1,900

5-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Quick Study 5-9 (10 minutes)

July 31 Sales …………………………………………………….. 160,200

Income Summary……………………………. 160,200

To close temporary accounts with credit balances.

July 31 Income Summary …………………………………… 165,900

Quick Study 5-10 (10 minutes)

Quick Study 5-11 (10 minutes)

Explanation of acid-test ratio: The acid-test ratio is used to evaluate (reflect on)

5-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Quick Study 5-12 (10 minutes)

Similarities: Both the acid-test ratio and current ratio are used to assess

liquidity. Both ratios are computed with current liabilities as the denominator.

Differences: The current ratio includes all current assets in the numerator.

The acid-test ratio includes current assets less inventories and prepaids in its

numerator (leaving cash & equivalents, current receivables, and short-term

investments).

Comparison and Description: Compared with the current ratio, the acid-test

ratio is a more stringent test of a company’s ability to meet its current

obligations. The acid-test ratio is more stringent as it does not assume a

company relies on prepaids and inventory to pay current liabilities. This is

because prepaids and inventory assets are not generally available to satisfy

current obligations.

Quick Study 5-13 (10 minutes)

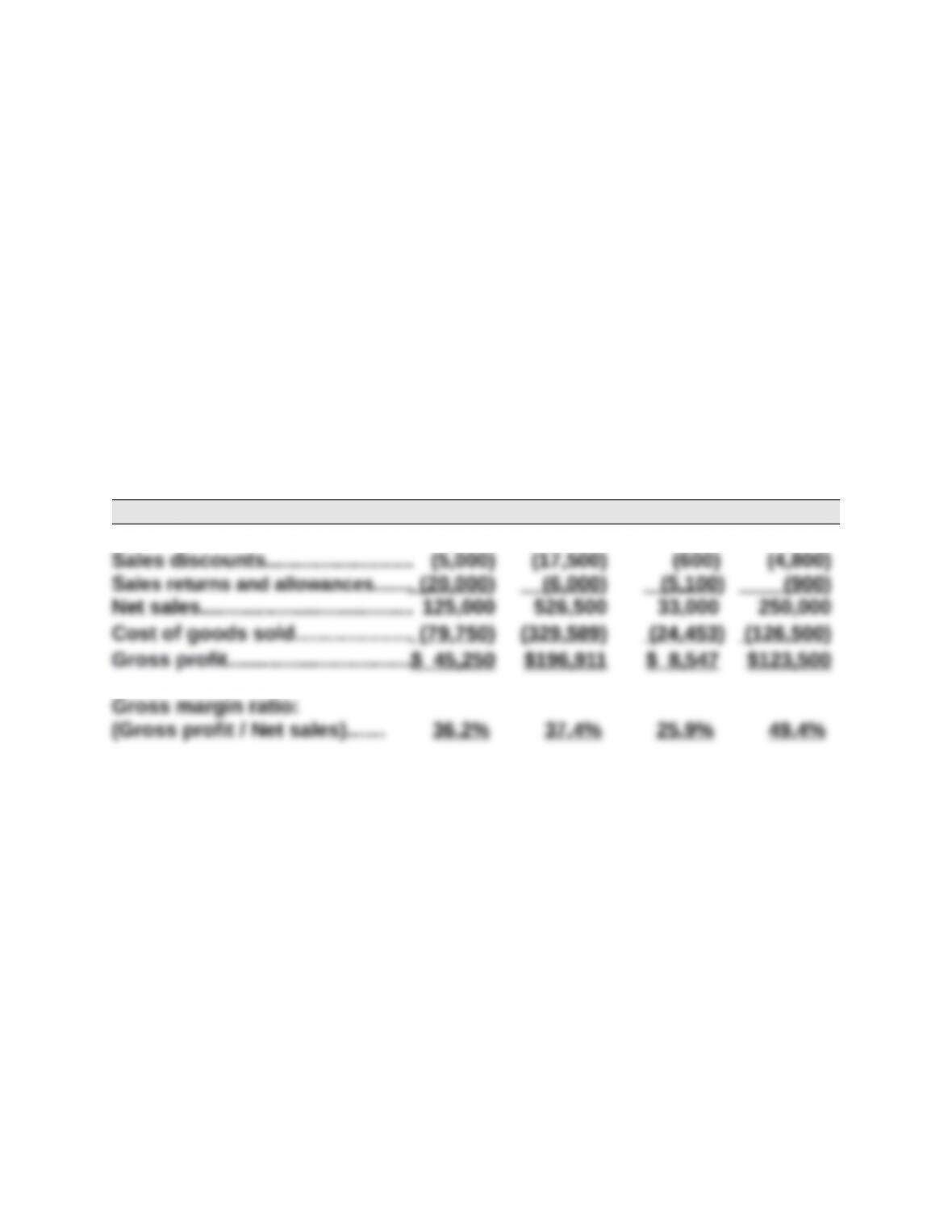

(a) (b) (c) (d)

Sales…………………………………….$150,000 $550,000 $38,700 $255,700

Interpretation of gross margin ratio for case a: The ratio of 36.2% implies

that for each dollar in net sales the company earns 36.2 cents in gross

profit. The company must still deduct other expenses that it incurs in

running the business when computing net income.

5-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Quick Study 5-14 (20 minutes)

1. Multiple-step income statement

adidas Group

Income Statement (€ millions)

For Year Ended December 31, 2013

Net sales………………………………………………………….. €14,492

Cost of sales…………………………………………………….. 7,352

Gross profit………………………………………………………. 7,140

2. Single-step income statement

adidas Group

Income Statement (€ millions)

For Year Ended December 31, 2013

Revenues

Net sales……………………………………………………….. €14,492

Expenses

Cost of sales…………………………………………………. €7,352

5-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Quick Study 5-15A (5 minutes)

a. Periodic inventory system

Quick Study 5-16A (10 minutes)

Nov. 5 Purchases…………………………………………………. 6,000

7 Accounts Payable………………………………………. 250

15 Accounts Payable………………………………………. 5,750

Quick Study 5-17A (10 minutes)

Apr. 1 Accounts Receivable …………………………………. 3,000

4 Sales Returns and Allowances …………………… 600

11 Cash …………………………………………………………. 2,352

Sales Discounts* ……………………………………….. 48

5-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Quick Study 5-18 (10 minutes)

a. Both U.S. GAAP and IFRS include broad and similar guidance for the

accounting of merchandise purchases and sales.

5-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.