Problem 4-2B (Continued)

Part 3

POWER DEMOLITION COMPANY

Income Statement

For Year Ended April 30, 2015

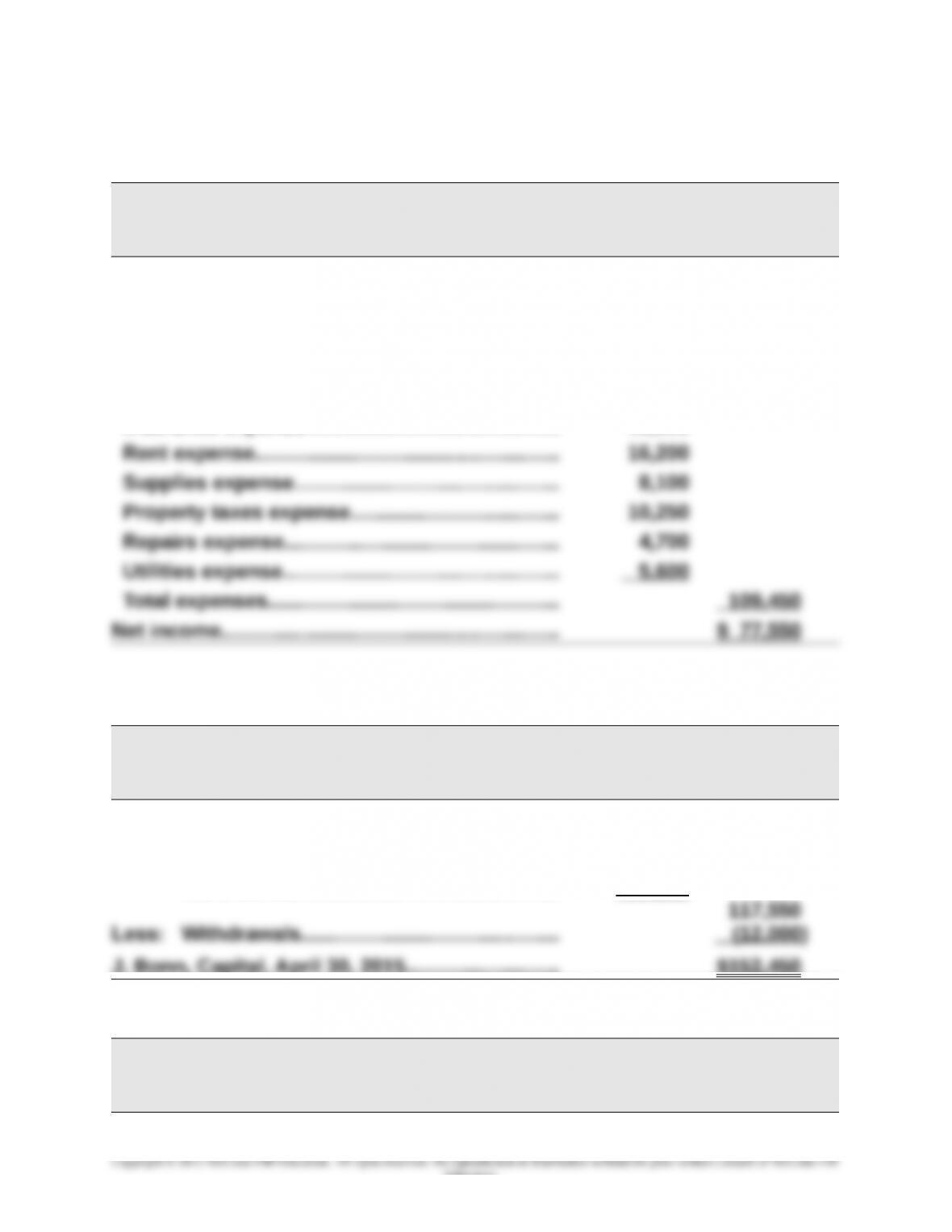

Demolition fees earned………………………….……… $187,000

Expenses

Depreciation expense–Equipment................... $ 7,000

Wages expense…………………………………………… 43,400

Interest expense…………………………………………. 3,600

Insurance expense……………………………………… 10,600

POWER DEMOLITION COMPANY

Statement of Owner’s Equity

For Year Ended April 30, 2015

J. Bonn, Capital, April 30, 2014…….……………….. $ 46,900

Add: Investments by owner……………………….. $40,000

Net income………………………………………… 77 ,550

J. Bonn, Capital, April 30, 2015…….……………….. $152 ,450

Problem 4-2B (Continued)

POWER DEMOLITION COMPANY

Balance Sheet

April 30, 2015

4-1

Education.

Assets

Current assets

Cash…………………………………………………………… $ 7,000

Supplies…………………………………………………….. 7,900

Prepaid insurance………………….…………………… 2 ,000

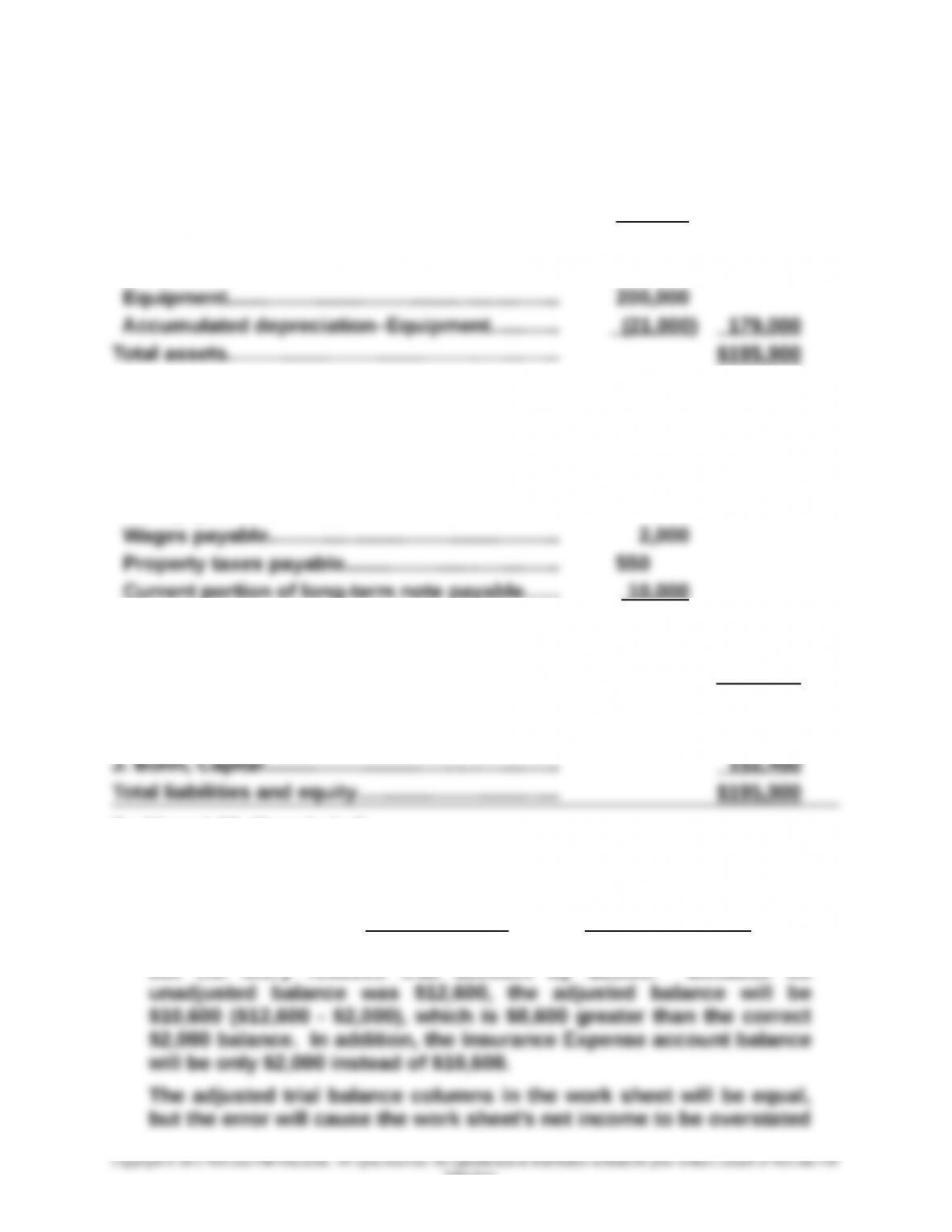

Total current assets………..………………………….. $ 16,900

Plant assets

Liabilities

Current liabilities

Accounts payable………………………………….……. $ 7,600

Interest payable…………………………….……………. 300

Rent payable………………………………..…………….. 3,000

Total current liabilities…………..……………………. $ 23,450

Long-term liabilities

Long-term note payable (less current portion) 20 ,000

Total liabilities…………………………………………..….. 43,450

Equity

Problem 4-2B (Concluded)

Part 4

(a) This error enters the wrong amount in the correct accounts. The

ending balance of the Prepaid Insurance account should be $2,000,

but the entry reduces that account by $2,000. Because its

4-2

Education.

by $8,600 because of the understatement of the expense. In

addition, the balance sheet columns will include the overstated

balance for the Prepaid Insurance account.

This error is not likely to be detected as a result of completing the

the unexpired insurance and total equity by $8,600.

(b) This error inserts a debit in the balance sheet columns instead of the

income statement columns. In the unlikely event that this error is

In all likelihood, the error will be discovered in the process of

drafting the balance sheet because the accountant will realize that

repairs expense is not an asset. If it is detected and corrected, the

Problem 4-3B (15 minutes)

1. Z 6. F 11. A 16. E

Problem 4-4B (75 minutes)

Part 1

ANARA CO.

4-3

Education.

Income Statement

For Year Ended December 31, 2015

Revenues

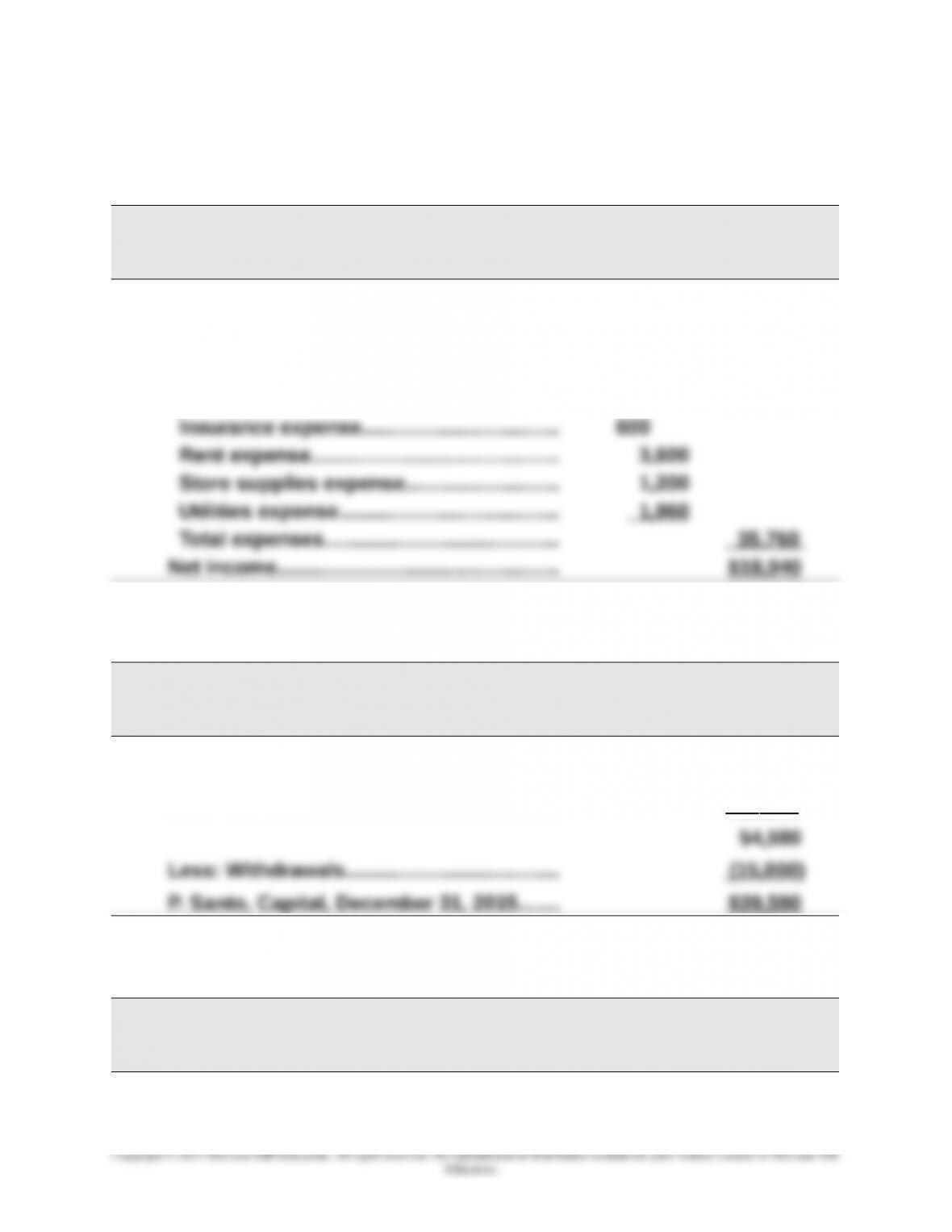

Professional fees earned…………………………….. $59,600

Total revenues……………………………………………. $66,420

Expenses

Depreciation expense—Building..……………….. 2,000

Depreciation expense—Equipment…..…………. 1,000

Wages expense…………………………………………… 18,500

Postage expense…………………………..……………. 410

Property taxes expense………………….…………… 4,825

Repairs expense…………………………………..…….. 679

ANARA CO.

Statement of Owner’s Equity

For Year Ended December 31, 2015

P. Anara, Capital, December 31, 2014….…………. $ 52,800

Add: Investments by owner..……………………….. $40,000

Net income…………………………..……………… 28 ,890 68 ,890

4-4

Education.

Problem 4-4B (Continued)

ANARA CO.

Balance Sheet

December 31, 2015

Assets

Current assets

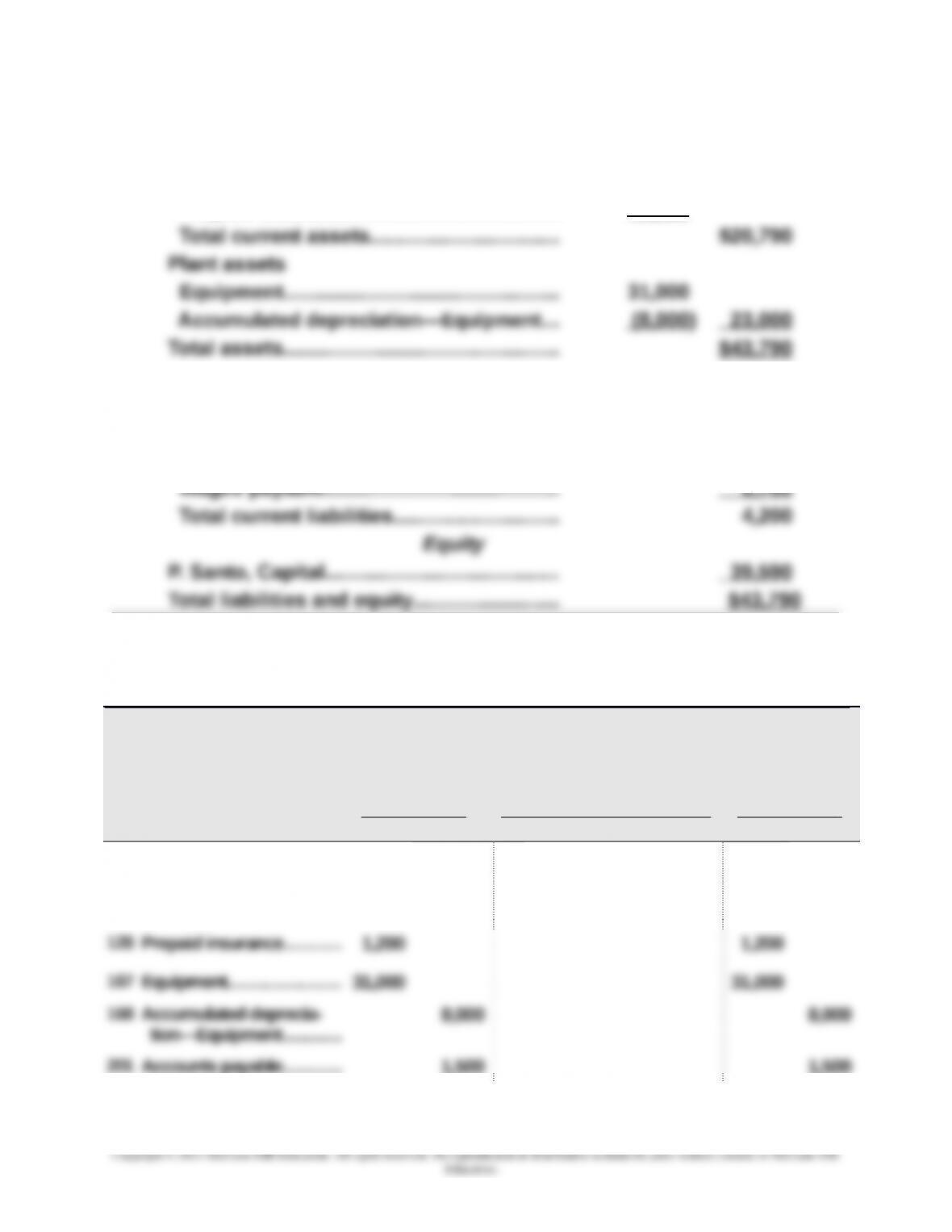

Cash $ 7,400

$ 24,200

Plant assets

Equipment $24,000

Accumulated depreciation—Equipment (4 ,000)

Total assets

$164 ,700

Liabilities

Current liabilities

Accounts payable $ 3,500

Interest payable 1,750

Total current liabilities

$ 19,410

Long-term liabilities

Long-term notes payable ($40,000-$8,400)

31 ,600

Total liabilities

4-5

51,010

Equity

4-6

Problem 4-4B (Continued)

Part 2

Closing entries (all dated December 31, 2015)

Instructor note: Entries are shown without an account reference column because no posting is required.

(1) Professional Fees Earned……………..……….. 59,600

Income Summary.…………………………… 66,420

To close the revenue accounts.

(2) Income Summary…………………………………… 37,530

Depreciation Expense—Building.…….. 2,000

Depreciation Expense—Equipment.... 1,000

Postage Expense…………………………….. 410

Property Taxes Expense………………….. 4,825

Repairs Expense.……………………………. 679

Telephone Expense………………..……….. 521

Utilities Expense……………………………... 1,920

P. Anara, Withdrawals……………………… 8,000

To close the withdrawals account.

Part 3

a. Return on assets = $28,890/[($160,000 + $164,700)/2] = 17.8% (or 0.178)

b. Debt ratio = $51,010/$164,700 = 0.31

4-7

Problem 4-5B (90 minutes)

Part 1

SANTO COMPANY

Income Statement

For Year Ended December 31, 2015

Repair fees earned…………..………………….. $54,700

Expenses

Depreciation expense—Equipment........ $ 2,000

Wages expense………………………………….. 26,400

SANTO COMPANY

Statement of Owner’s Equity

For Year Ended December 31, 2015

P. Santo, Capital, December 31, 2014....... $35,650

Add: Net income………………………….……… 18 ,940

Problem 4-5B (Continued)

SANTO COMPANY

Balance Sheet

December 31, 2015

Assets

4-8

Current assets

Cash………………………………………………..… $14,450

Store supplies………………………………….... 5,140

Prepaid insurance……………………………… 1 ,200

Liabilities

Current liabilities

Accounts payable………………………………. $ 1,500

Problem 4-5B (Continued)

Parts 2 and 3

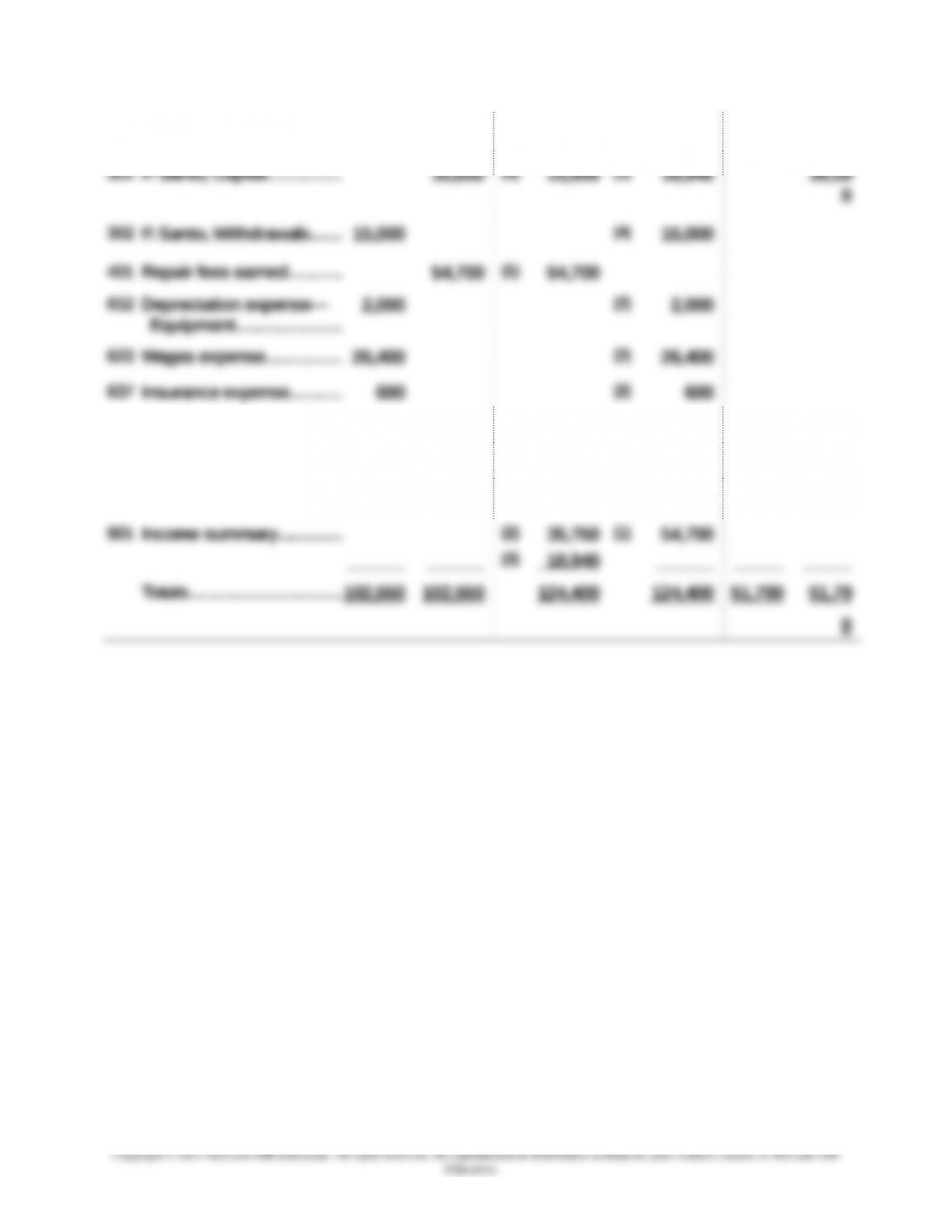

SANTO COMPANY

Work Sheet

For Year Ended December 31, 2015

Adjusted

Trial Balance

Closing Entry Information

Post–Closing

Trial Balance

No. Account Title Dr. Cr. Dr. Cr. Dr. Cr.

101 Cash………………………….. 14,450 14,450

125 Store supplies….….......... 5,140 5,140

4-9

210 Wages payable..…..……... 2,700 2,700

640 Rent expense....…........... 3,600 (2) 3,600

651 Store supplies expense... 1,200 (2) 1,200

690 Utilities expense.….......... 1,960 (2) 1,960

Problem 4-5B (Concluded)

Part 3

Closing entries (all dated December 31, 2015)

Instructor note: Entries are shown without an account reference column because no posting is required.

(2) Income Summary…………..………………………… 35,760

Depreciation Expense, Equipment…..…. 2,000

Wages Expense…………………………………. 26,400

Insurance Expense…………..……………….. 600

Rent Expense…………………..……………….. 3,600

To close the Income Summary account.

(4) P. Santo, Capital………….…………………………… 15,000

P. Santo, Withdrawals…………………..……. 15,000

To close the withdrawals account.

Part 4

(a) If none of the $600 insurance expense had expired, the income

Financial Statement Changes

The income statement would reflect the following:

Net income would be increased by $600 + $2,700 = $3,300. (a) & (b)

The balance sheet would reflect the following:

4-11

4-12