Chapter 04 – Completing the Accounting Cycle

CHAPTER 4

COMPLETING THE ACCOUNTING CYCLE

Related Assignment Materials

Student Learning Objectives Questions

Quick

Studies* Exercises* Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Explain why temporary

accounts are closed each period.

2, 3, 4, 5 4-5 4-5 4-1 4-1, 4-4

C2. Identify steps in the accounting

cycle.

8 4-8 4-11 4-1 4-3, 4-8

C3. Explain and prepare a classified

balance sheet.

9, 10, 11, 14,

15

4-9 4-12 4-2, 4-3,

4-4, 4-5

4-7

Analytical objectives:

A1. Compute the current ratio and

describe what it reveals about a

company’s financial condition.

4-11 4-14, 4-15 4-4 4-2, 4-5,

4-7, 4-9

Procedural objectives:

P1. Prepare a work sheet and

explain its usefulness.

6, 7 4-1, 4-2,

4-3, 4-4,

4-7, 4-8

4-1, 4-2, 4-3,

4-4, 4-6, 4-7

4-2 4-6

P2. Describe and prepare closing

entries.

1, 3, 4, 5, 6,

16, 17

4-6, 4-10 4-6, 4-7, 4-8,

4-9, 4-10,

4-13

4-1, 4-2,

4-4, 4-5

4-1, 4-4,

4-6, 4-7

P3. Explain and prepare a

post-closing trial balance.

4 4-7 4-9, 4-10 4-1, 4-5 4-6

P4A. Prepare reversing entries and

explain their purpose.

12, 13 4-11 4-16, 4-17 4-6

*See additional information on next page that pertains to these quick studies, exercises and problems.

4-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 04 – Completing the Accounting Cycle

Additional Information on Related Assignment Material

The Serial Problem for Success Systems continues in this chapter. Problems 4-2A and 4-4A can be

completed using Excel. Problem 4-4A, 4-5A and the Serial Problem can be completed with Sage 50

Software and QuickBooks.

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode.

Synopsis of Chapter Revision

The Naked Hippie: NEW opener with new entrepreneurial assignment

New multi-color-coded 5-step layout for work sheet preparation and use

Updated current ratio section using Limited Brands

4-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 04 – Completing the Accounting Cycle

Chapter Outline Notes

I. Work Sheet as a Tool

A. The work sheet is an internal document that serves as a useful tool

for organizing accounting information. It is not a required report.

B. Benefits include: aids the preparation of financial statements,

reduces possibility of errors, links accounts and adjustments to

their impacts in financial statements, assists in planning and

organizing an audit of financial statements, helps in preparing

interim (monthly and quarterly) financial statements, and shows

the effect of proposed or “what if” transactions.

C. Steps to prepare a work sheet:

1. Enter the unadjusted trial balance in the first two columns.

2. Enter the adjustments in the third and fourth columns. Total

columns to verify debit adjustments equal credit adjustments.

3. Prepare the Adjusted Trial Balance. This is done by

combining the unadjusted trial balance and adjustment

columns. Total Adjusted Trial Balance columns to verify

debits equal credits.

4. Sort the adjusted trial balance amounts to the appropriate

financial statement columns.

5. Total statement columns, compute net income or loss and

balance the columns by adding net income or loss.

D. Work Sheet Applications and Analysis—it does not substitute for

financial statements. The financial statement columns yield pro

forma financial statements because they show the statements as if

the proposed transactions occurred.

II. Closing Process—The closing process is an important step at end of

the accounting period after financial statements have been completed.

Prepares accounts for recording transactions and events for the next

period.

A Steps in closing process:

1. Identify accounts for closing.

2. Record and post closing entries.

3. Prepare a post-closing trial balance.

B. Purpose of closing process:

1. To reset revenues, expenses, and withdrawals account

balances to zero at the end of every period to prepare these

accounts for proper measurement in the next period.

2. To update the capital account with the effect of the period’s

net income (revenue minus expenses) and owner withdrawals.

C. Temporary and Permanent Accounts

1. Temporary (or nominal) accounts accumulate data related to

one accounting period. (They are the income statement

accounts, withdrawals accounts, and Income Summary.)

4-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 04 – Completing the Accounting Cycle

Chapter Outline Notes

2. Permanent (or real) accounts report on activities related to

one or more future accounting periods. They are all balance

sheet accounts that are not closed.

D. Recording Closing Entries—the purpose is to transfer the

end-of-period balances in revenue, expense, and withdrawals

accounts to the permanent capital account.

1. Use a new temporary account called Income Summary. The

four closing entries are:

a. Close credit balances in revenue (and gain) accounts by

debiting the accounts and crediting Income Summary.

This transfers revenue balances to the credit side Income

Summary.

b. Close debit balances in expense (and loss) accounts by

crediting the accounts and debiting Income Summary.

This transfers the expense balances to the debit side of

Income Summary.

c. Close the Income Summary account to the owner’s capital

account.

Note: The Income Summary account, prior to closing, will

have a credit balance equal to net income or a debit balance

equal to net loss. Therefore this entry will credit capital for the

amount of net income (or debit capital for a net loss).

d. Close withdrawals account by crediting the account and

debiting the owner’s capital account.

2. After all closing entries are posted, all temporary accounts

have a zero balance and capital is up to date.

E. Post-Closing Trial Balance—a list of permanent accounts and their

balances taken from the ledger.

1. Prepared after closing entries are journalized and posted.

2. Verifies that total debits equal total credits for permanent

accounts and all temporary accounts have zero ending

balances.

4-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 04 – Completing the Accounting Cycle

Chapter Outline Notes

F. The Accounting Cycle–steps can vary if a worksheet is used (see

Visual #4-1)

The ten steps repeated each accounting cycle are as follows:

1. Analyze transactions

2. Journalize

3. Post

4. Prepare unadjusted trial balance

5. Adjust

6. Prepare an adjusted trial balance

7. Prepare statements

8. Close

9. Prepare a post-closing trial balance.

10. Reverse (optional)

III. Classified Balance Sheet—organizes assets and liabilities into

important subgroups and provides more information for decision

makers.

A. Classification Structure

1. One of the more important classifications is the separation

between current and noncurrent assets and liabilities.

2. Current items are expected to come due (both collected and

owed) within the longer of one year or the company’s

operating cycle.

3. An operating cycle is the time span from when cash is used to

acquire goods and services until cash is received from the sale

of those goods and services.

B. Classification Categories

1. Current assets—cash or other resources that are expected to be

sold, collected, or used within one year or the operating cycle,

whichever is longer. Examples: cash, short-term investments,

accounts receivable, short-term notes receivable, merchandise

inventory, and prepaid expenses.

2. Long-term investments—assets held for more than one year,

that are not used in business operations. Examples: stocks,

bonds, promissory notes, and land held for future expansion.

3. Plant assets—tangible, long-lived assets that are used to

produce or sell goods and services. Examples: equipment,

buildings, land.

4. Intangible assets—long-term resources that benefit business

operation. They lack physical form. Their value comes from

the privileges or rights that are granted to or held by the

owner. Examples: goodwill, patents, trademarks, franchises,

copyrights.

4-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 04 – Completing the Accounting Cycle

5. Current liabilities—obligations due to be paid or settled within

the longer of one year or the operating cycle. Examples:

accounts payable, notes payable, wages payable, taxes

payable, interest payable, unearned revenues, current portions

of long-term liabilities.

6. Long-term liabilities—obligations that are not due to be paid

within one year or the operating cycle of the business.

Examples: notes payable, mortgage payable, bonds payable.

7. Equity—owner’s claim on assets. For a proprietorship it is

reported in this section as the owner’s capital account. In a

corporation, equity is divided into two main subsections:

capital stock and retained earnings.

IV. Global View—Compares U.S.GAAP to IFRS

A. Both systems have similar definitions of assets that involve the

same three basic criteria.

B. Both systems define initial asset value as historical cost for nearly

all assets.

C. After acquisition both systems value at historical cost or fair value

but GAAP and IFRS differ slightly in how they define fair value.

D. Both systems have similar definitions of liabilities that involve the

same three basic criteria and similar valuation at acquisition.

Later chapter discuss specific difference in valuation after

acquisition.

V. Decision Analysis—Current Ratio

A. Assesses a company’s ability to pay its debts in the near future.

B. Calculation: total current assets divided by total current liabilities.

VI. Appendix 4A—Reversing Entries

A. Accounting with reversing entries (an optional step)

1. Linked to asset and liability account balances that arose from

the accrual of revenues and expenses.

2. Purpose is to simplify recordkeeping.

3. They are prepared after closing entries and dated the first day

of the new period.

4. Procedure is to transfer accrued asset and liability account

balances to related revenue and expense accounts creating an

abnormal balance in these accounts.

5. The full subsequent cash receipts (and payments) are recorded

as increases in revenue (and expense) accounts creating a net

balance equal to the amount earned or incurred in that period.

B. Accounting without reversing entries

1. To construct proper entries when the cash receipt/payment

occurs in the new accounting period, the related accrual or

deferral adjustment must be recalled and considered.

2. With or without reversing entries use, it will yield the same

result.

4-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 04 – Completing the Accounting Cycle

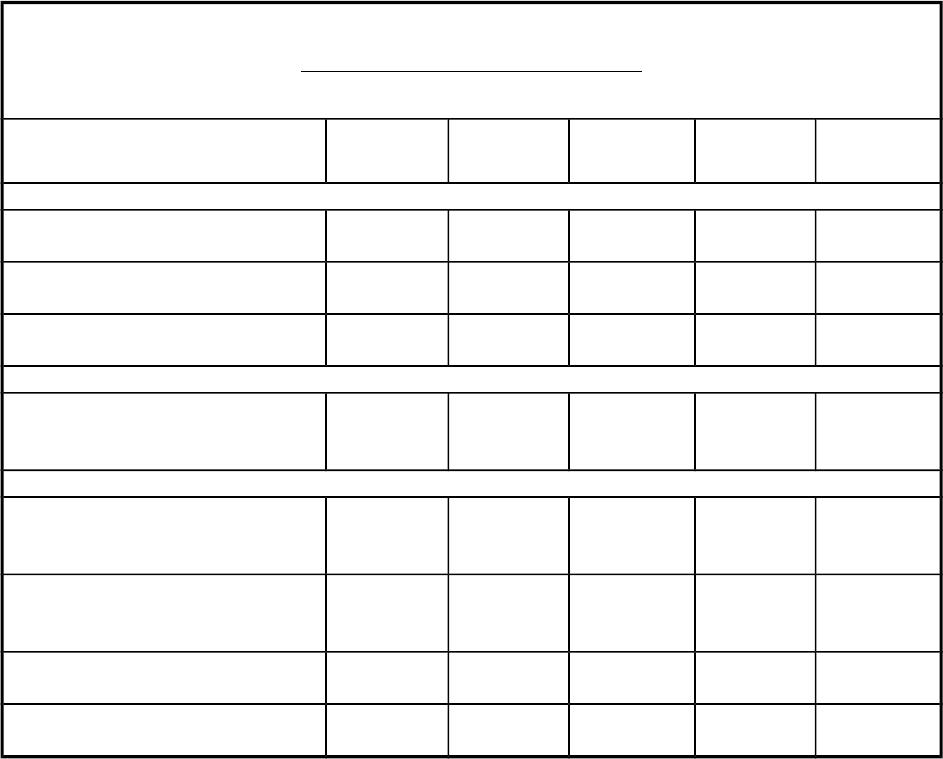

VISUAL #4-1

THE ACCOUNTING CYCLE

STEPS PURPOSE TIMING

1. Analyze

transactions

To determine accounts to be debited

and credited

During the period

2. Journalize To record the daily transactions During the period

3. Post To transfer the amounts from journal

entries to the individual accounts

affected by the recorded transaction

During the period

4. Prepare

unadjusted trial

balance

To summarize unadjusted ledger

accounts and amount.

End of period

5. Journalizing and

posting of

adjusting entries

To bring the ledger accounts to

adjusted balances

End of year

6. Prepare adjusted

trial balance

To summarize adjusted ledger

accounts and amounts

End of year

7. Preparing the

statements

To report financial information End of period*

8. Journalizing and

posting of

closing entries

To bring all temporary accounts to

zero and the capital account

up-to-date

End of year

9. Post-closing

trial balance

To prove the accuracy of the

adjusting and closing procedures

End of year

10. Reversing

entries

(optional)

To provide for recording in new fiscal

period without consideration of

accruals from previous periods

adjustments.

Beginning of new

year

*If statements are to be prepared for interim period (less than a year), a worksheet

is generally used to project adjusted numbers for statements.

Steps 4 and 6 can be done on a worksheet.

4-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 04 – Completing the Accounting Cycle

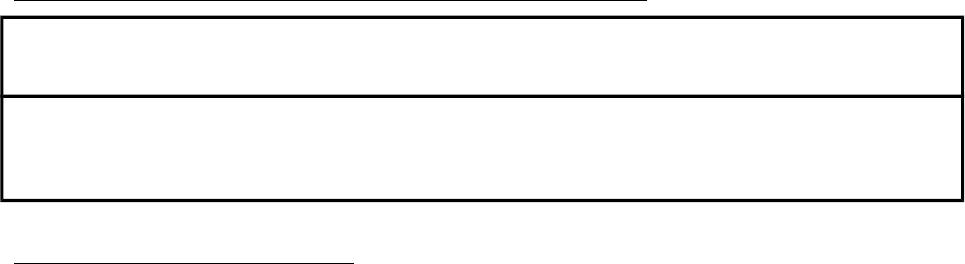

VISUAL #4-2

MUSIC WORLD

BALANCE SHEET

DECEMBER 31, 20XX

Assets

Current Assets

Cash $30,360

Short-Term Investments 2,000

Notes Receivable 8,000

Accounts Receivable 35,300

Merchandise Inventory 60,400

Prepaid Insurance 6,600

Supplies 1,696

Total Current Assets $144,356

Investments

Land Held for Future Use 13,950

Property, Plant, and Equipment

Land $ 4,500

Building $20,650

Less Accumulated Depreciation 8,640 12,010

Office Equipment $ 8,600

Less Accumulated Depreciation 5,000 3,600

Total Property, Plant, and Equipment 20,110

Intangible Assets

Trademark 500

Total Assets $178,916

Liabilities

Current Liabilities

Notes Payable $15,000

Accounts Payable 25,683

Salaries Payable 2,000

Mortgage Payable 10,200

Total Current Liabilities $52,883

Long-Term Liabilities

Mortgage Payable 27,600

Total Liabilities $ 80,483

Owner’s Equity

Joy Melody, Capital 98,433

Total Liabilities and Owner’s Equity $178,916

4-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 04 – Completing the Accounting Cycle

Alternate Demo Problem Four

The trial balance of Large Company, Inc. at the end of its annual accounting

period is as follows:

LARGE COMPANY, INC.

Trial Balance

December 31, 2013

Cash………………………………………………………….….. $ 4,000

Prepaid Insurance…………………………………….……. 1,600

Supplies ……………………………………………………….. 2,100

Equipment …………..…………..………........................ 20,000

Accumulated Depreciation—Equipment.............. $ 2,000

C. Large, Capital ……………………………………………. 19,000

C. Large, Withdrawals…………………………………….. 2,000

Revenue………………………………………………………… 33,000

Salaries Expense……..…………............................... 18,300

Rent Expense ……………..…………..…...................... 6,000 ______

Totals….……..……………..…………............................. $54,000 $54,000

Additional information:

1. Expired insurance, $600.

2. Unused supplies, per inventory, $800.

3. Estimated depreciation, $1,000.

4. Earned but unpaid salaries, $700

Required

1. Prepare adjusting entries.

2. Prepare closing entries.

3. Prepare a post-closing trial balance.

4-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 04 – Completing the Accounting Cycle

Solution: Alternate Demo Problem Four

1. Insurance Expense……………………………………. 600

Prepaid Insurance…………………………....…. 600

Supplies Expense…………………………………….. 1,300

Supplies……………………………………………... 1,300

Depreciation Expense Equip….….................... 1,000

Accumulated Depreciation Equip............. 1,000

Salaries Expense…………………………………….... 700

Salaries Payable…………………………………. 700

2. Revenue……………………………………....…....….... 33,000

Income Summary……….….….….................. 33,000

Income Summary……….….…............................ 27,900

Salaries Expense….….…............................ 19,000

Rent Expense…..….….….…..….................... 6,000

Insurance Expense….…..…........................ 600

Supplies Expense….…..….…...................... 1,300

Depreciation Expense............................... 1,000

Income Summary……….….…............................ 5,100

C. Large, Capital…………………………………. 5,100

C. Large, Capital………………………………....….... 2,000

C. Large, Withdrawal…………………………… 2,000

Solution continued next page

4-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 04 – Completing the Accounting Cycle

3. LARGE COMPANY, INC.

Post-Closing Trial Balance

December 31, 2013

Dr. Cr.

Cash…………………………………………...…....…..… $4,000

Prepaid Insurance…..….…..….….…................... 1,000

Supplies………………………………………...…....….. 800

Equipment…..….…..….….…............................... 20,000

Accumulated Depreciation, Equipment.......... $ 3,000

Salaries Payable……………………………….....…... 700

C. Large, Capital….…..….….….…..….….….......... ______ 22,100

Totals……………………………………………………….. $25,800 $25,800

4-11

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.