Quick Study 3-18 (10 minutes)

a. Under IFRS, financial statements normally present assets from least

liquid to most liquid.

Quick Study 3-19 (10 minutes)

Quick Study 3-20A (5 minutes)

EXERCISES

Exercise 3-1 (20 minutes)

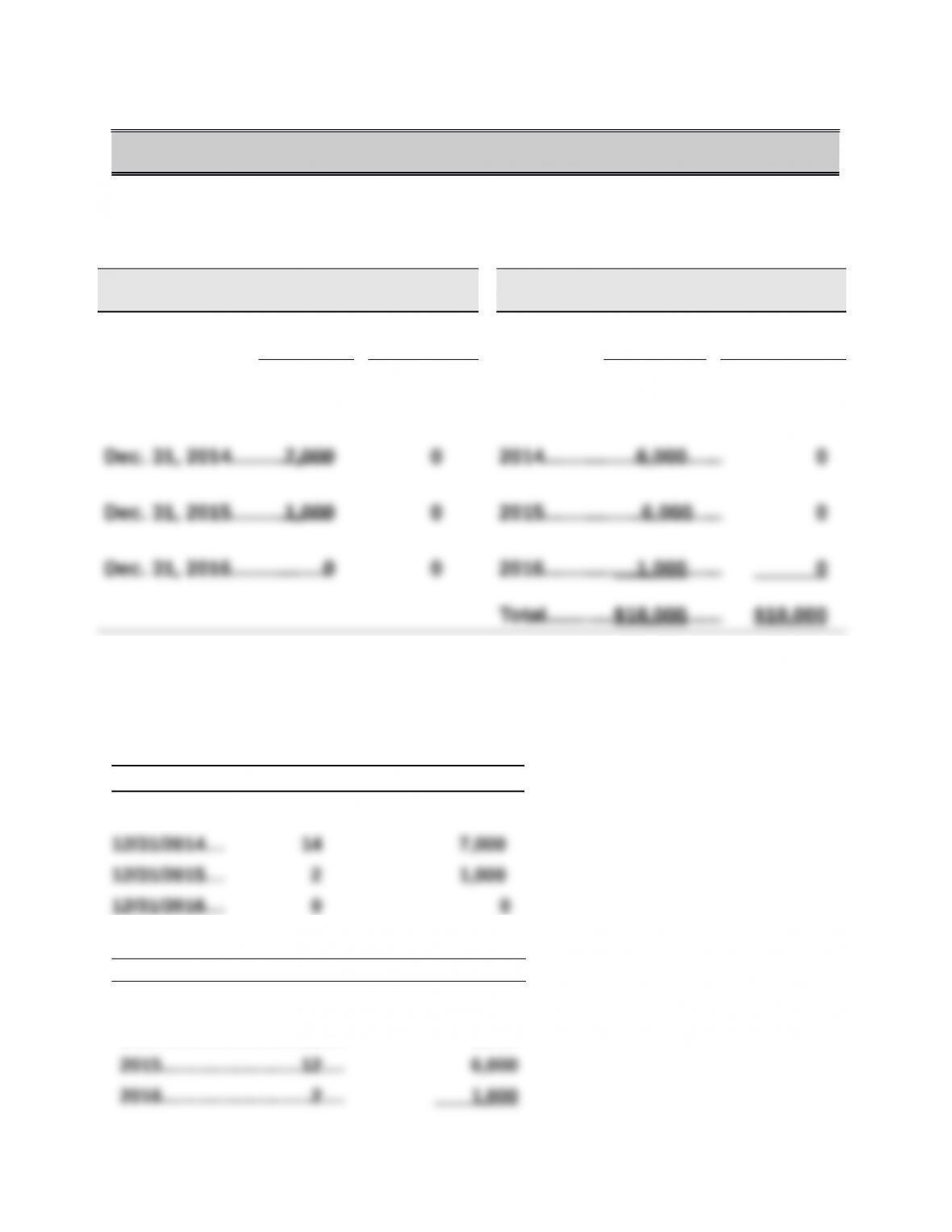

Balance Sheet Insurance Asset using Insurance Expense using

Accrual

Basis*

Cash

Basis

Accrual

Basis**

Cash

Basis

Dec. 31, 2013……..………$13,000 $0 2013…………………..….....$ 5,000 $18,000

Explanations:

*Accrual asset balance equals months left in the policy x $500 per month (monthly

cost is computed as $18,000 / 36 months).

Months Left Balance

12/31/2013... 26 $13,000

**Accrual insurance expense equals months covered in the year x $500 per month.

Months Covered Expense

2013…….……………..….…....10 $ 5,000

2014…….……………..….…....12 6,000

Exercise 3-2 (10 minutes)

Exercise 3-3 (15 minutes)

a. Adjusting entry:

2015

Dec. 31 Wages Expense………………………………….……..…………..

1,250

Wages Payable…………………………………………..….. 1,250

To record accrued wages for one day.

(5 workers x $250)

b. Payday entry:

2016

Exercise 3-4 (15 minutes)

a. Supplies expense for current year: $2,550

Proof:

(a) (b) (c) (d)

Supplies available – prior year-end......... $ 400 $1,200 $ 1,260 $2,288

Supplies purchased in current year........ 2,800 6,500 8,490 3,000

Exercise 3-5 (25 minutes)

a.

Apr. 30 Legal Fees Expense………………………………..…… 3,500

Legal Fees Payable.……………………………… 3,500

To record accrued legal fees.

May 12 Legal Fees Payable……………………………...……… 3,500

May 20 Interest Payable…………………………………………… 3,000

Interest Expense*………………………………………… 6,000

Cash…………………………………………..………... 9,000

To record payment of accrued and current

interest. *($9,000 monthly interest x 20/30)

c.

Apr. 30 Salaries Expense…………………………………………. 4,000

Exercise 3-6 (25 minutes)

($6,000 – $1,100).

c. Office Supplies Expense…….………........................…....... 3,880

Office Supplies**………………..……….......................…..... 3,880

To record office supplies used ($700 + $3,480 – $300).

e. Insurance Expense…………………………………………………… 5,800

Prepaid Insurance………………………………………..…….... 5,800

To record insurance coverage that expired.

Notes:

Prepaid Insurance*Office Supplies**

? Used ? Used

End. Bal. 1,100 End. Bal. 300

Exercise 3-7 (30 minutes)

a. Unearned Fee Revenue…………………………………………….. 5,000

Fee Revenue………………………………………………..…..….. 5,000

To record earned portion of fee received in advance

($15,000 x 1/3).

d. Office Supplies Expense…..………..…....…........................ 5,000

Office Supplies*……………………………………..……..…..…. 5,000

To record office supplies used ($240 + $5,200 – $440).

g. Interest Expense……………………………………………….……. 2,500

Interest Payable…………………………………….…..……….. 2,500

To record interest incurred but not yet paid.

Notes:

Prepaid Insurance†Office Supplies*

Exercise 3-8 (25 minutes)

Dec. 31 Accounts Receivable………………………………………. 2,100

Fees Earned…………………………………..………… 2,100

To record earned but unbilled fees (30% x $7,000).

To record depreciation on office furniture.

31 Salaries Expense……………………………..…………….. 2,250

Salaries Payable………………………..…………….. 2,250

To record accrued salaries.

31 Insurance Expense…………………………..…..…………. 1,400

Prepaid Insurance……………….…………..………. 1,400

To record expired prepaid insurance.

To record incurred and unpaid utility costs.

Exercise 3-9 (20 minutes)

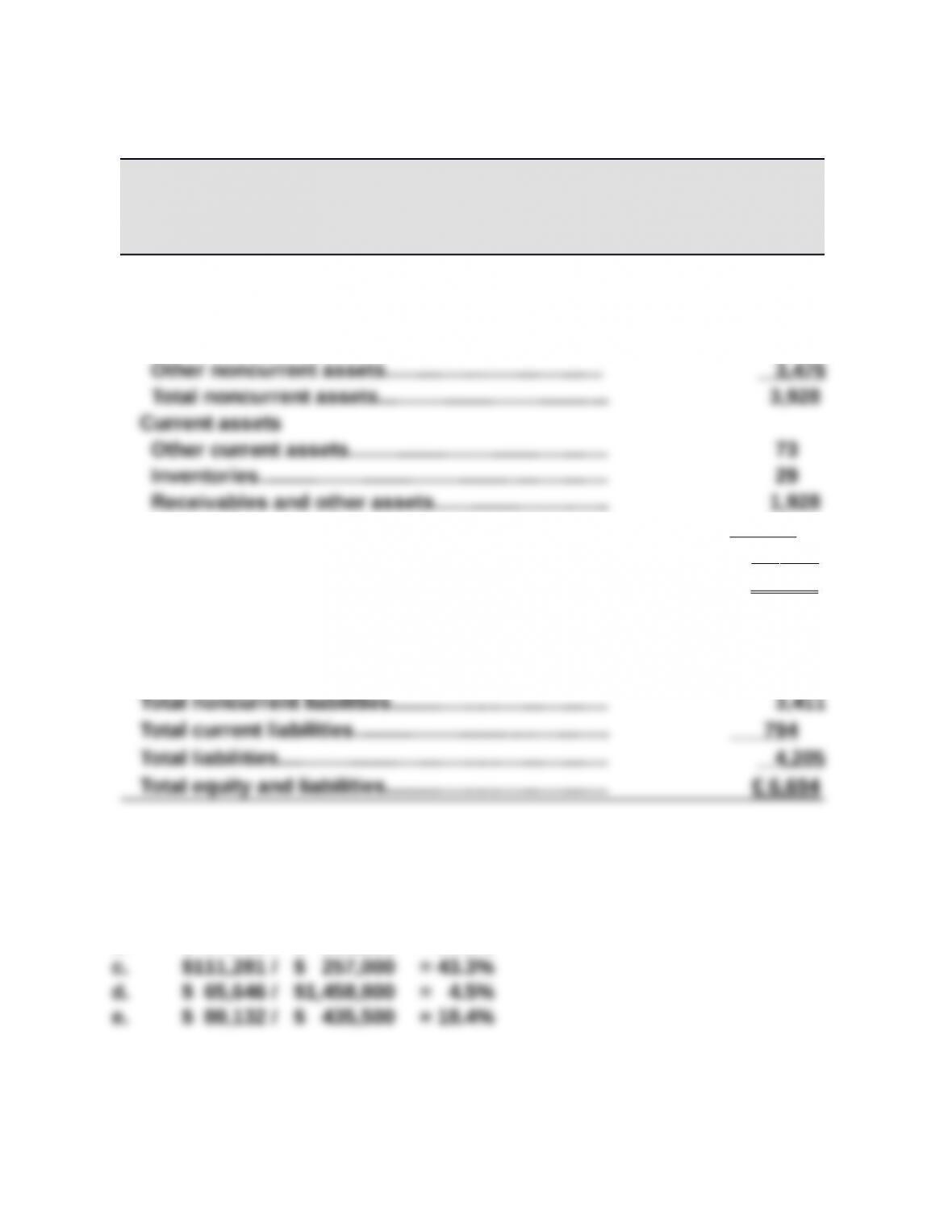

adidas AG

Balance Sheet

December 31, 2013

(Euros in millions)

Assets

Noncurrent assets

Intangible assets………………………………..………..… € 148

Tangible and other assets………………………………. 304

Cash and cash equivalents…………………………….. 736

Total current assets…………………………..…………… 2 ,766

Total assets……………………………………………………... € 6 ,694

Equity

Total equity……………………………………………..………. € 2,489

Liabilities

Exercise 3-10 (10 minutes)

a. $ 4,361 / $ 44,500 = 9.8%

b. $ 97,706 / $ 398,800 = 24.5%

Analysis and Interpretation: Company c has the highest profitability