Problem 25-2B (Continued)

Part 4

PROJECT A

Present Value of Net Cash Flows

Present Present

Value of Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-4……………………………………………… $99,900 3.3121 $330,879

PROJECT B

Present Value of Net Cash Flows

Present Present

Value of Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-3……………………………………………… $105,900 2.5771 $272,915

Part 5

Recommendation to management is to pursue Project A. This is because

although both projects have a positive net present value, Project A has a

Problem 25-3B (60 minutes)

Part 1

RESULTS USING STRAIGHT-LINE DEPRECIATION

(a)

Income

Before

Deprec.

(b)

Straight-Li

ne Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

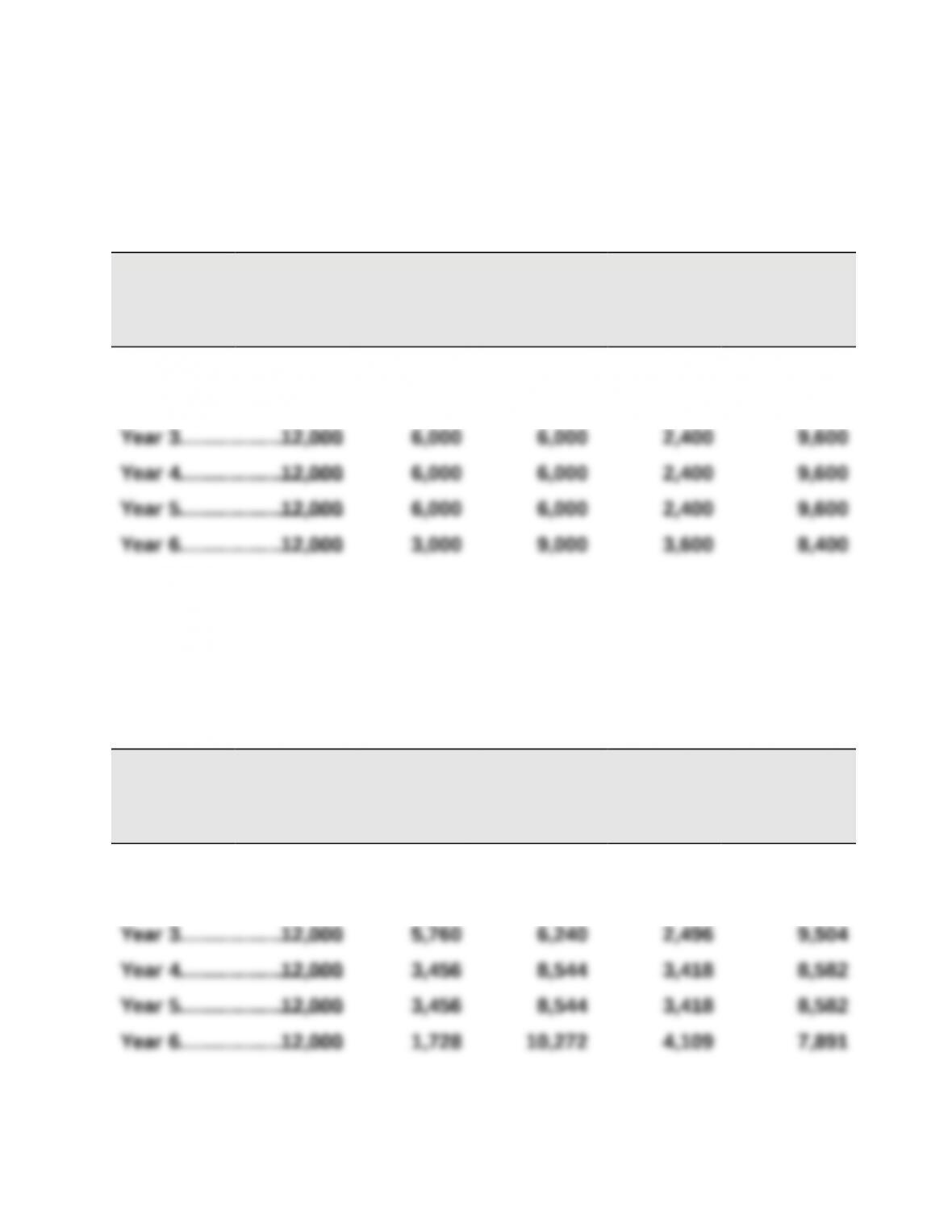

Year 1……………………….$12,000 $3,000 $ 9,000 $3,600 $8,400

Year 2……………………….12,000 6,000 6,000 2,400 9,600

Part 2

RESULTS USING MACRS DEPRECIATION

(a)

Income

Before

Deprec.

(b)

MACRS

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1……………………….$12,000 $6,000 $ 6,000 $2,400 $ 9,600

Year 2……………………….12,000 9,600 2,400 960 11,040

Problem 25-3B (Continued)

Part 3

NET PRESENT VALUE OF ASSET USING STRAIGHT-LINE DEPRECIATION

Present Present

Net Cash Value of Value of Net

Flows 1 at 10% Cash Flows

Year 1…………………………………………………. $ 8,400 0.9091 $ 7,636

Year 2…………………………………………………. 9,600 0.8264 7,933

Part 4

NET PRESENT VALUE OF ASSET USING MACRS DEPRECIATION

Present Present

Net Cash Value of Value of Net

Flows 1 at 10% Cash Flows

Year 1…………………………………………………. $ 9,600 0.9091 $ 8,727

Year 2…………………………………………………. 11,040 0.8264 9,123

Part 5

Analysis: The net present value using MACRS depreciation is greater than the

net present value using straight-line depreciation because the cash flows are

larger in the earlier years of the asset’s life under MACRS depreciation. They

are larger because the depreciation deductions are larger, resulting in less

income taxes paid in the earlier years.

Problem 25-4B (45 minutes)

WINDMIRE COMPANY

COMPARATIVE INCOME STATEMENTS

(1) (2) (3)

Normal New

Volume Business Combined

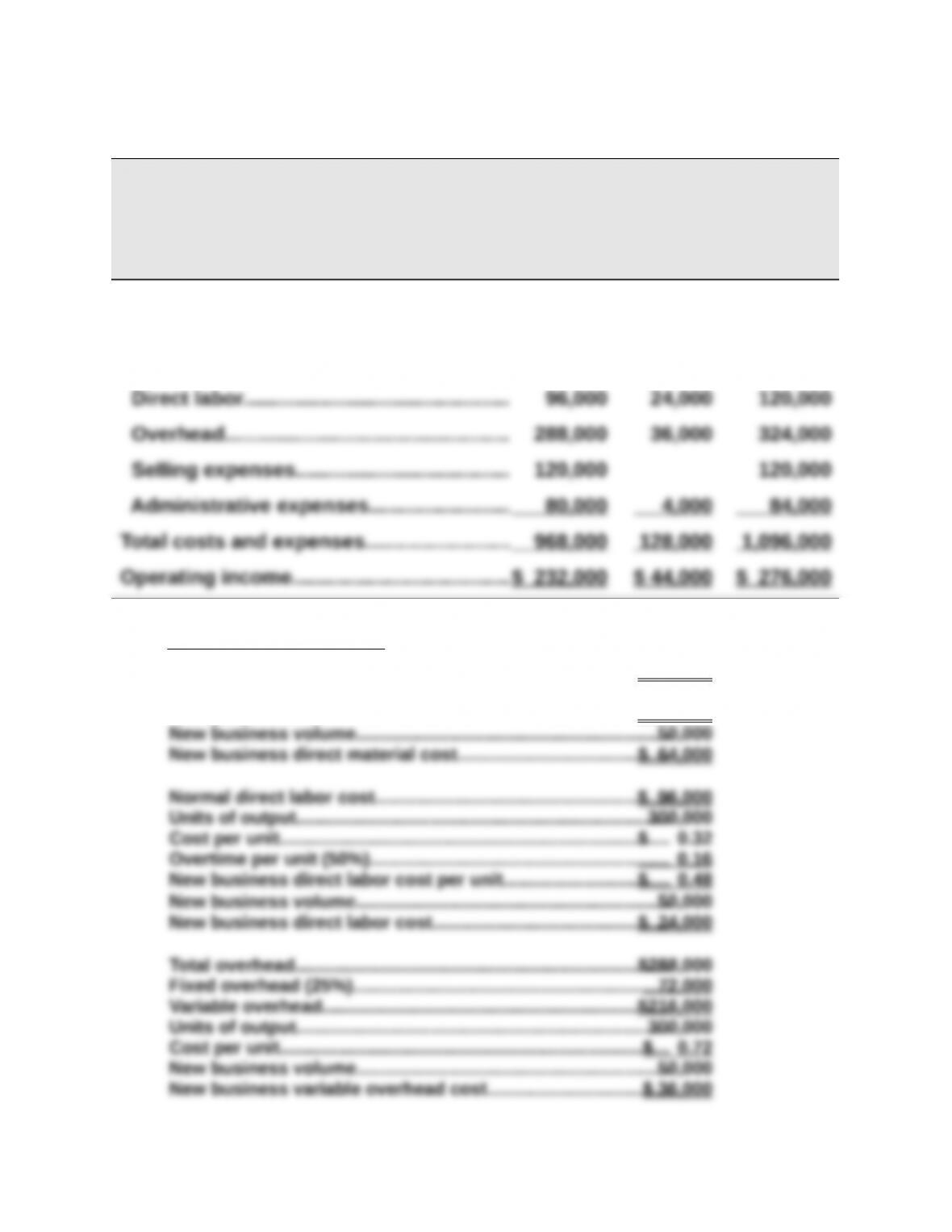

Sales………………………………………………….$1,200,000 $172,000 $1,372,000

Costs and expenses

Direct materials………………………………… 384,000 64,000 448,000

Supporting computations

Normal direct material cost………………………………………………$384,000

Units of output…………………………………………………………………300,000

Cost per unit……………………………………………………………………$ 1.28

Problem 25-5B (55 minutes)

Part 1

Product R Product T

Selling price per unit……………………………………………. $ 60 $ 80

Part 2

Sales Mix Recommendation To the extent allowed by production and

market constraints, the company should produce as much of Product R as

Contribution Margin at Recommended Sales Mix

Contribution margin = 440 units x $40 per unit = $17,600 per month

0.4 hrs. per unit

Problem 25-5B (Continued)

Part 3

Sales Mix Recommendation with Second Shift If the second shift is added,

the maximum possible output of R will double:

However, this level of output exceeds the company’s market constraint of

Units of Product R………………………………………………….. = 550 units per month

The output of Product T with 132 production hours is

Contribution Margin at This Sales Mix

Units Contr./unit Total

From R……………………………………………………….. 550 $40 $22,000

From T……………………………………………………….. 132 35 4,620

Less extra shift costs………………………………….. (3,250)

Total contribution margin…………………………….. $23,370

Management decision This amount of $23,370 exceeds the contribution

margin of $17,600 generated by one shift alone (see part 2). Therefore,

management should add the second shift.

352 hrs. per mo.

0.4 hrs. per unit

132 hrs. per mo.

1.0 hrs. per unit

Problem 25-5B (Continued)

Part 4

Sales Mix Recommendation By incurring additional marketing cost, the

company can relax the market constraint for sales of Product R up to the

point where 675 units can be sold. This means the company can produce

675 units of Product R, and commit the remainder of its productive

capacity to Product T. These computations are:

Units of Product R………………………………………………….. = 675 units per month

The output of Product T with 82 production hours is

Contribution Margin with This Sales Mix

Units Contr./unit Total

From R……………………………………………………….. 675 $40 $27,000

Management decision This amount of $22,120 is less than the contribution

margin of $23,370 generated under the existing market constraint (see part

3). Therefore, management should not undertake this marketing strategy.

1.0 hr. per unit

Problem 25-6B (60 minutes)

Part 1

ESME COMPANY

Analysis of Expenses under Elimination of Department Z

Total Eliminated Continuing

Expenses Expenses Expenses

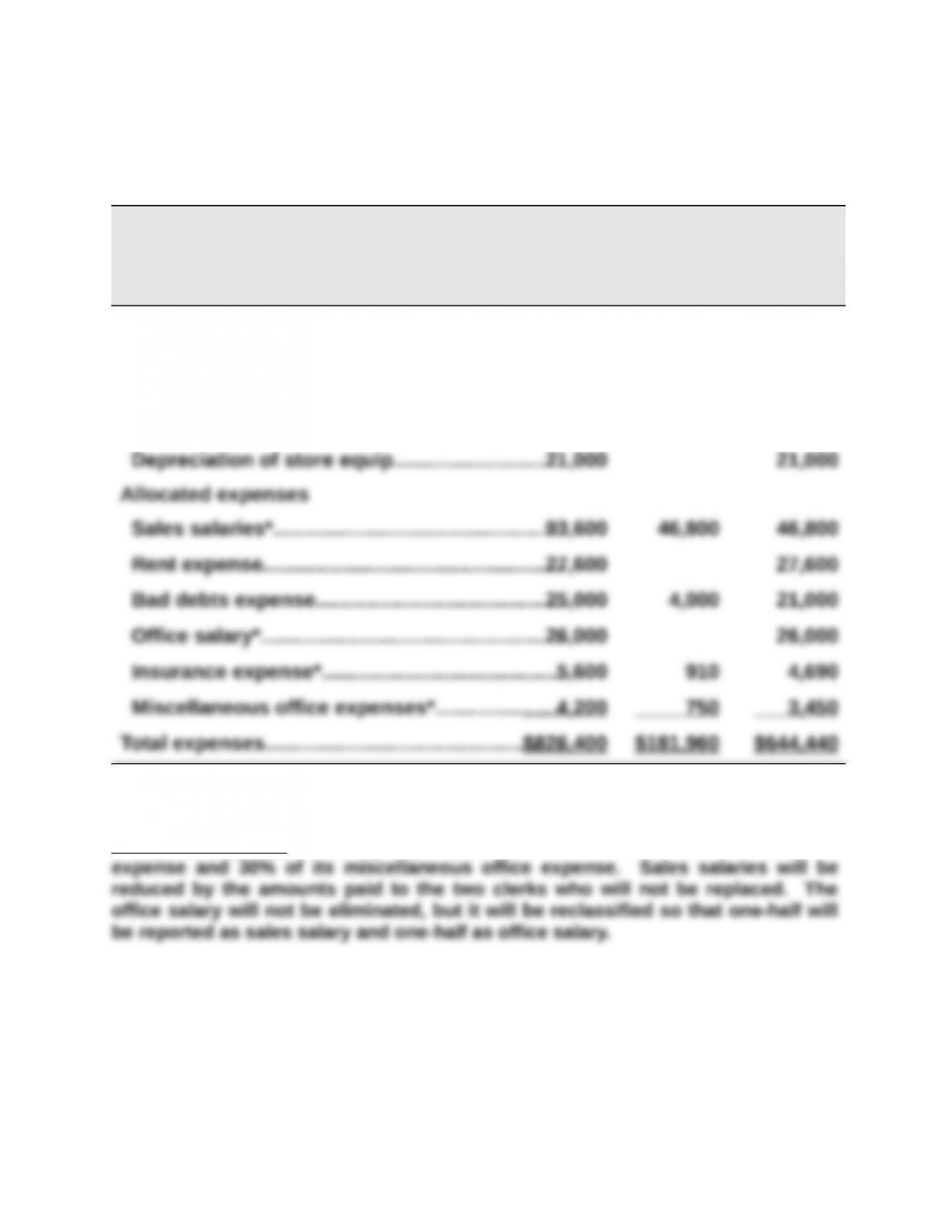

Cost of goods sold……………………………………….$586,400 $125,100 $461,300

Direct expenses

Advertising………………………………………………..30,000 3,000 27,000

Store supplies used……………………………………7,000 1,400 5,600

Computation Notes Closing Department Z will eliminate 65% of its insurance

Problem 25-6B (Continued)

Part 2

ESME COMPANY

Forecasted Annual Income Statement

Under Plan to Eliminate Department Z

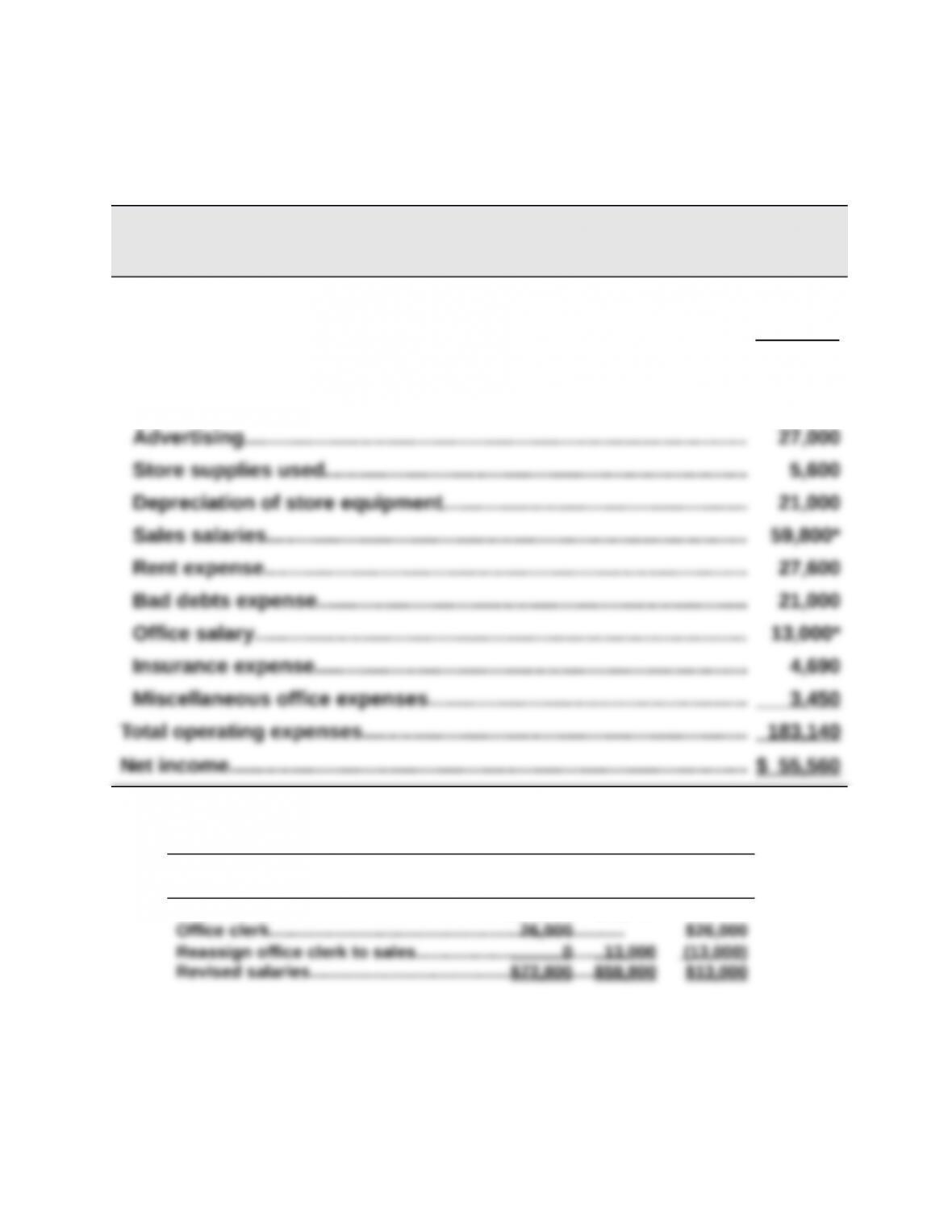

Sales………………………………………………………………………………………. $700,000

Cost of goods sold………………………………………………………………….. 461,300

Gross profit from sales……………………………………………………………. 238,700

Operating expenses

* Office salary reassignment

Total Sales Office

Salaries Salaries Salary

Sales clerks………………………………………………………………..$46,800 $46,800

Problem 25-6B (Continued)

Part 3

ESME COMPANY

Reconciliation of Combined Income with Forecasted Income

Combined net income ……………………………………………………………….$ 48,600

ANALYSIS

Department Z’s avoidable expenses of $181,960 are $6,960 greater than its