Exercise 25-26 (20 minutes)

ALTERNATIVE A: INCREASE OR (DECREASE) IN NET INCOME

Cost to buy new machine………………………………………………………………..$(115,000)

ALTERNATIVE B: INCREASE OR (DECREASE) IN NET INCOME

Cost to buy new machine………………………………………………………………..$(125,000)

The company should replace the machine with alternative machine B. This

will increase net income by $32,000.

Exercise 25-27 (15 minutes)

1. Recovery time computation

2. The advantage of break-even time is that it considers the time value of

3. When (1) the interest rate is very low, 1% for example, and (2) the

PROBLEM SET A

Problem 25-1A (50 minutes)

Part 1

Annual straight-line depreciation = = $115,000

Part 2

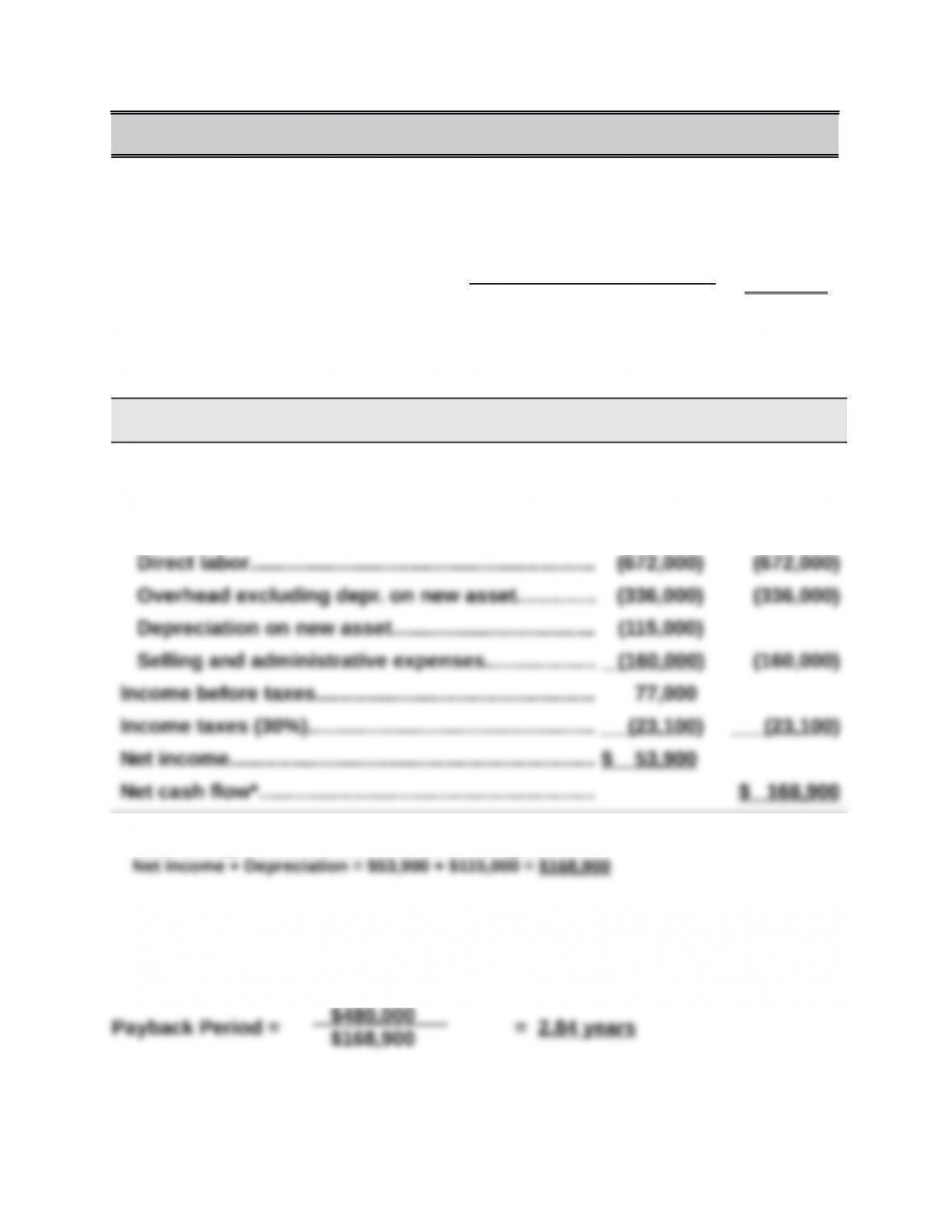

Net Net Cash

Income Flow

Expected annual sales of new product………………$1,840,000 $1,840,000

Expected costs of new product

Direct materials…………………………………………….. (480,000) (480,000)

* Alternatively, annual net cash flow can be computed as

Part 3

$480,000 – $20,000

4 years

Problem 25-1A (Continued)

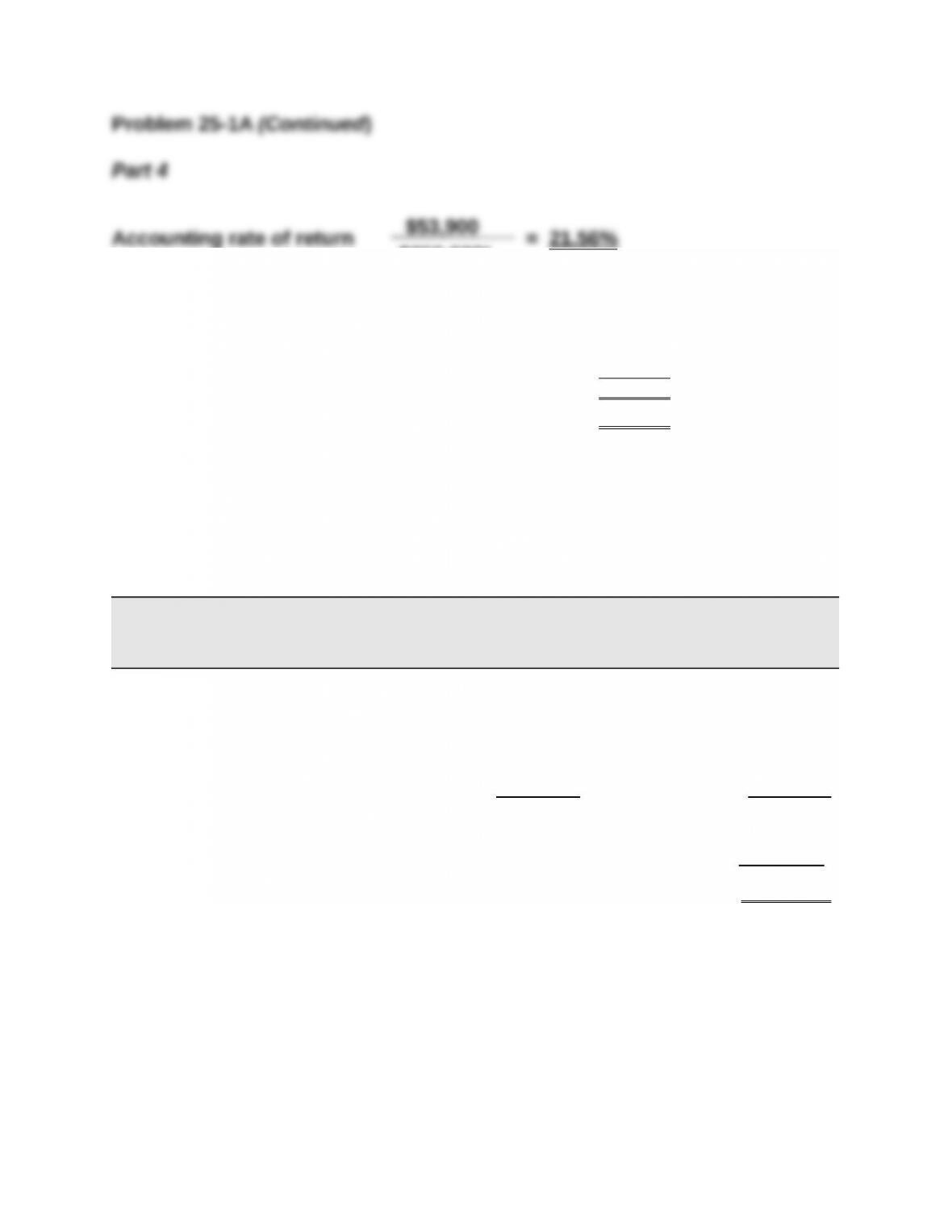

Part 4

Accounting rate of return = = 21.56%

* Average investment

Asset cost…………………………………………………………………………..$480,000

Final year’s book value………………………………………………………. 20,000

Sum……………………………………………………………………………………$500,000

Average (Sum /2)………………………………………………………………..$250,000

Part 5

Present Value of Net Cash Flows

Present Present

Net Cash Value of Value of Net

Flows 1 at 7% Cash Flows

Year 1…………………………………………………$168,900 0.9346 $ 157,854

Year 2…………………………………………………168,900 0.8734 147,517

Year 3…………………………………………………168,900 0.8163 137,873

Year 4*……………………………………………….. 188,900 0.7629 144,112

Totals…………………………………………………$695,600 587,356

Amount invested………………………………… (480,000)

Net present value……………………………….. $ 107,356

* Year 4’s cash flow includes the $20,000 salvage value.

$250,000*

Problem 25-2A (55 minutes)

Part 1

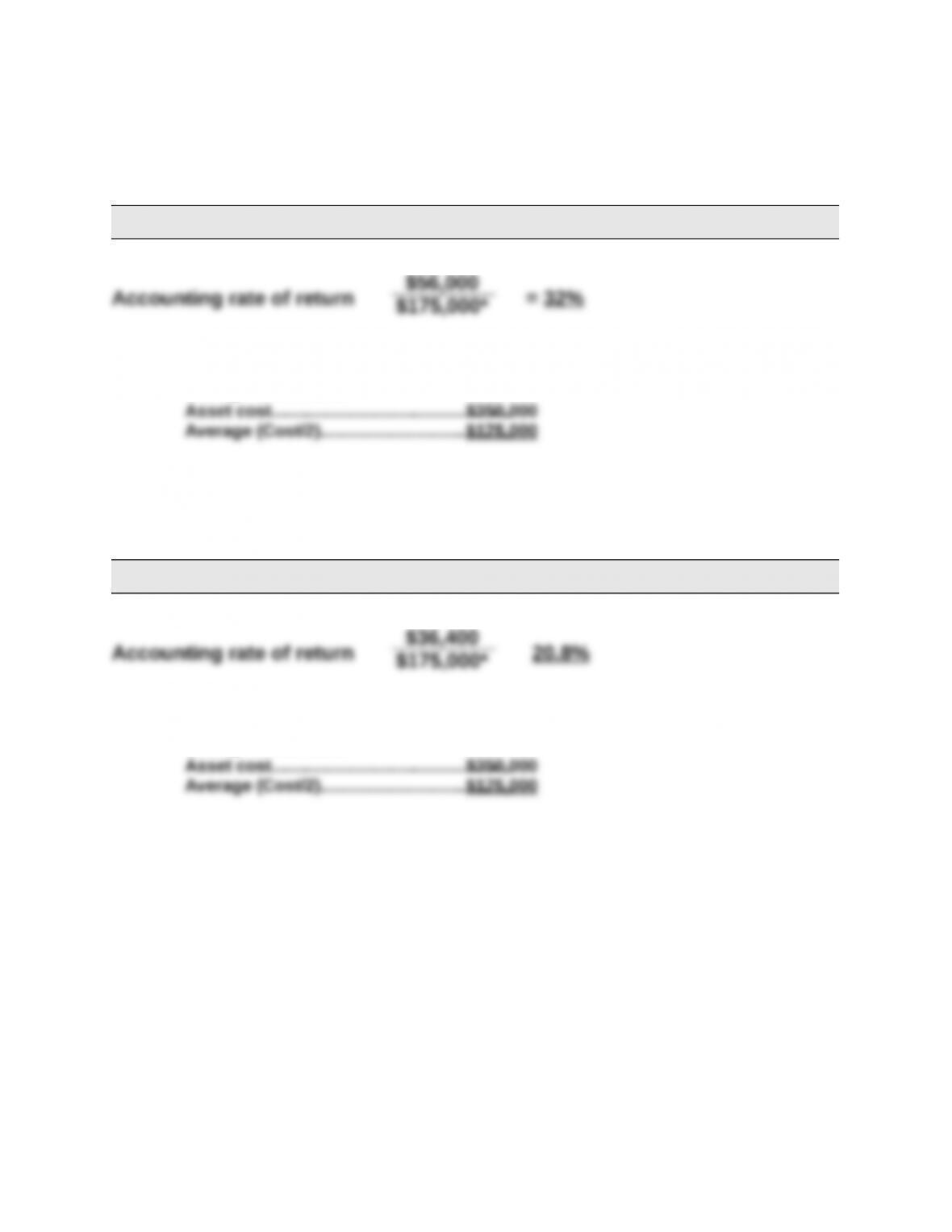

PROJECT Y

Net income…………………………………………………………………………… $ 56,000

PROJECT Z

Net income…………………………………………………………………………… $ 36,400

Part 2

PROJECT Y

PROJECT Z

4 years

3 years

$350,000

$143,500

$350,000

Problem 25-2A (Continued)

Part 3

PROJECT Y

*Average investment

PROJECT Z

*Average investment

Asset cost……………………………………………$350,000

Average (Cost/2)…………………………………..$175,000

$56,000

$175,000*

$36,400

$175,000*

Problem 25-2A (Continued)

Part 4

PROJECT Y

Present Value of Net Cash Flows

Present Present

Value of Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-4…………………………………………….. $143,500 3.3121 $475,286

PROJECT Z

Present Value of Net Cash Flows

Present Present

Value of Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-3…………………………………………….. $153,067 2.5771 $394,469

Part 5

Recommendation to management is to pursue Project Y. This is because

Project Y has a positive net present value, which means that we expect it to

Problem 25-3A (60 minutes)

Part 1

RESULTS USING STRAIGHT-LINE DEPRECIATION

(a)

Income

Before

Deprec.

(b)

Straight-Li

ne Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

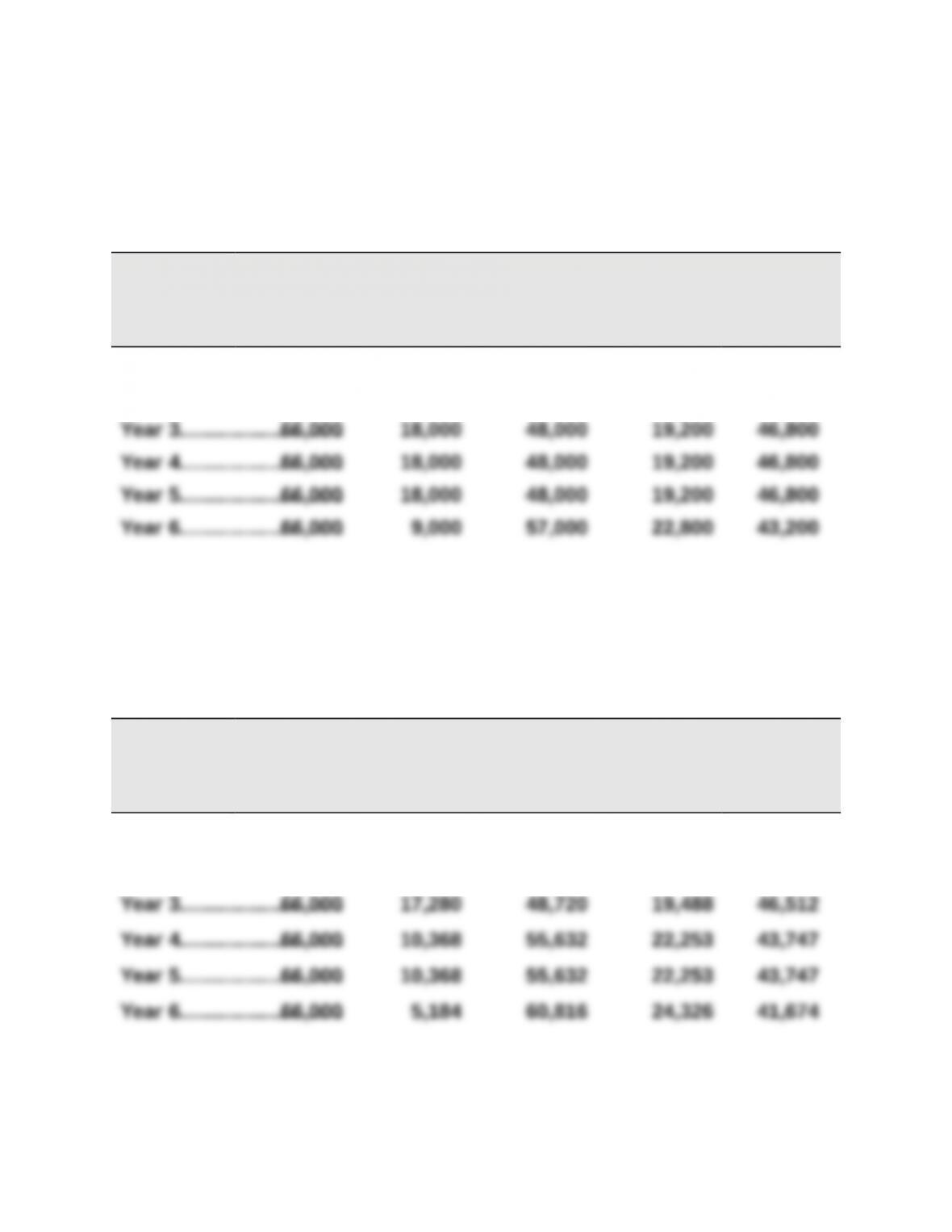

Year 1……………………….$66,000 $ 9,000 $57,000 $22,800 $43,200

Year 2……………………….66,000 18,000 48,000 19,200 46,800

Part 2

RESULTS USING MACRS DEPRECIATION

(a)

Income

Before

Deprec.

(b)

MACRS

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1……………………….$66,000 $18,000 $48,000 $19,200 $46,800

Year 2……………………….66,000 28,800 37,200 14,880 51,120

Problem 25-3A (Continued)

Part 3

NET PRESENT VALUE OF ASSET USING STRAIGHT-LINE DEPRECIATION

Present

Present Value of

Net Cash

Flows

Value of

1 at 10%

Net Cash

Flows

Year 1………………………………………………… $ 43,200 0.9091 $ 39,273

Year 2………………………………………………… 46,800 0.8264 38,676

Problem 25-4A (45 minutes)

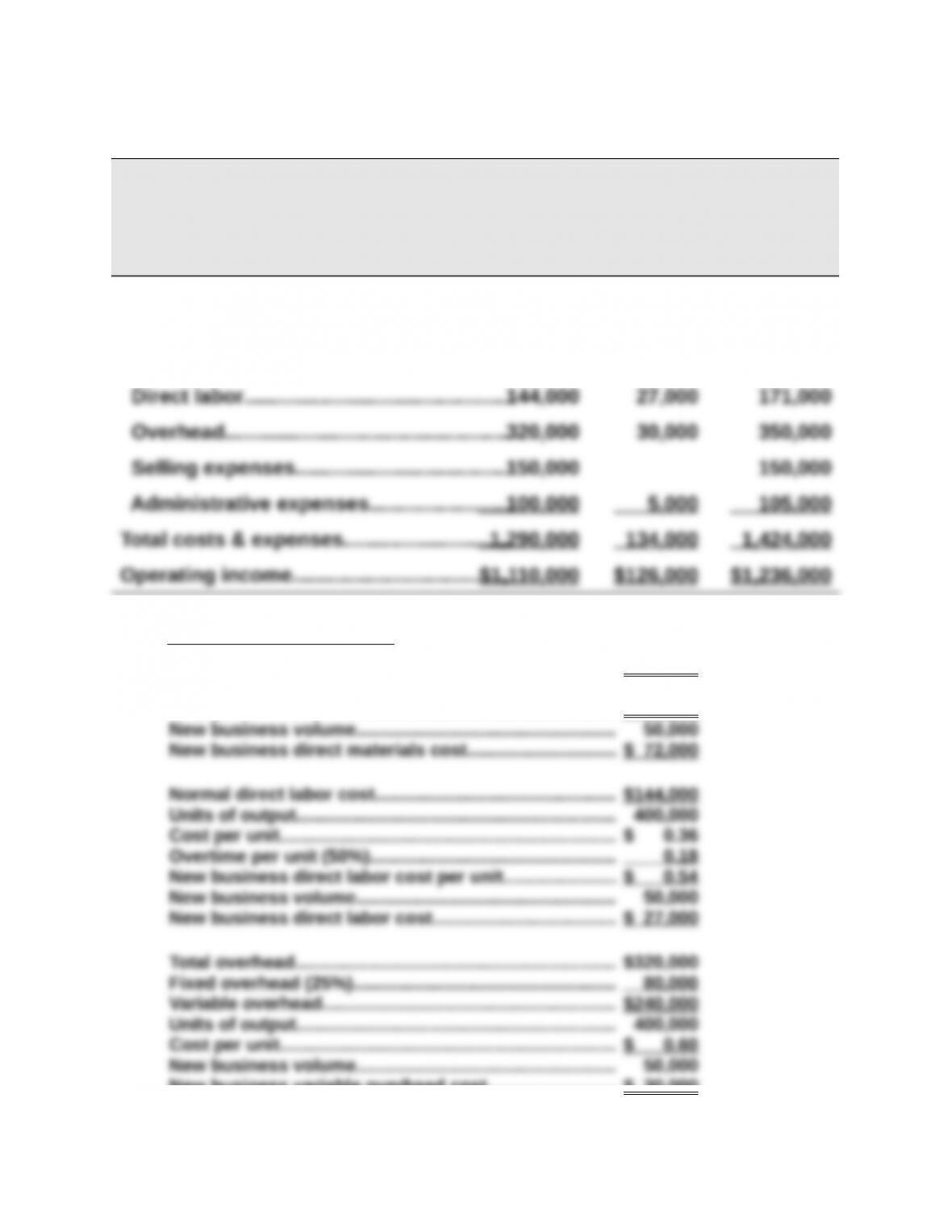

JONES PRODUCTS

COMPARATIVE INCOME STATEMENTS

(1) (2) (3)

Normal New

Volume Business Combined

Sales………………………………………………….$2,400,000 $260,000 $2,660,000

Costs and expenses

Direct materials…………………………………576,000 72,000 648,000

Supporting computations

Normal direct materials cost………………………………….. $576,000

Units of output………………………………………………………. 400,000

Cost per unit…………………………………………………………. $ 1.44

New business variable overhead cost…………………….. $ 30,000

Problem 25-5A (55 minutes)

Part 1

Product G Product B

Selling price per unit……………………………………………. $120 $160

Part 2

Sales Mix Recommendation. To the extent allowed by production and

Contribution Margin at Recommended Sales Mix

Contribution margin = 440 units x $80 per unit = $35,200 per month

0.4 hrs. per unit