Exercise 25-13 (20 minutes)

Using Excel, Project X1 (X2) has an internal rate of return of 20.34% (12.99%).

Project X1 Project X2

A B C D

1 Initial investment -80000 -120000

2Annual cash flows,

end of period

Both of these IRR’s are above the company’s required rate of return of 4%,

thus both projects should be accepted.

Exercise 25-14 (35 minutes)

1.

PROJECT C1

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of Net

Cash Flows

Year 1………………………………………………………….$ 12,000 0.8929 $ 10,715

Exercise 25-14 (continued)

PROJECT C2

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of Net

Cash Flows

Year 1………………………………………………………….$ 96,000 0.8929 $ 85,718

PROJECT C3

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of

Net Cash

Flows

Year 1………………………………………………………….$180,000 0.8929 $160,722

Analysis and Interpretation: Both Project C2 and C3 yield a positive net present value. Accordingly, both

C2 and C3 are acceptable investments. Project C1 has a negative net present value, so it should be

rejected.

2. INTERNAL RATE OF RETURN VS. NET PRESENT VALUE FOR C2

Project C2 will have an internal rate of return higher than 12%.

Exercise 25-15A (20 minutes)

Using Excel, Project A (B) has an internal rate of return of 26.96 (35.00%).

Project A Project B

A B C D

1 Initial investment -160000 -105000

2Annual cash flows,

end of period

Exercise 25-16 (10 minutes)

1. Sunk cost

Exercise 25-17 (25 minutes)

Normal Additional Combined

Volume Volume* Total

Sales…………………………………………. $2,250,000 $180,000 $2,430,000

Costs and expenses

Direct materials………………………… 300,000 30,0001330,000

The company should accept the offer as it increases income by $3,000.

* ADDITIONAL VOLUME COMPUTATIONS

Additional sales revenue = 15,000 units @ $12 = $180,000

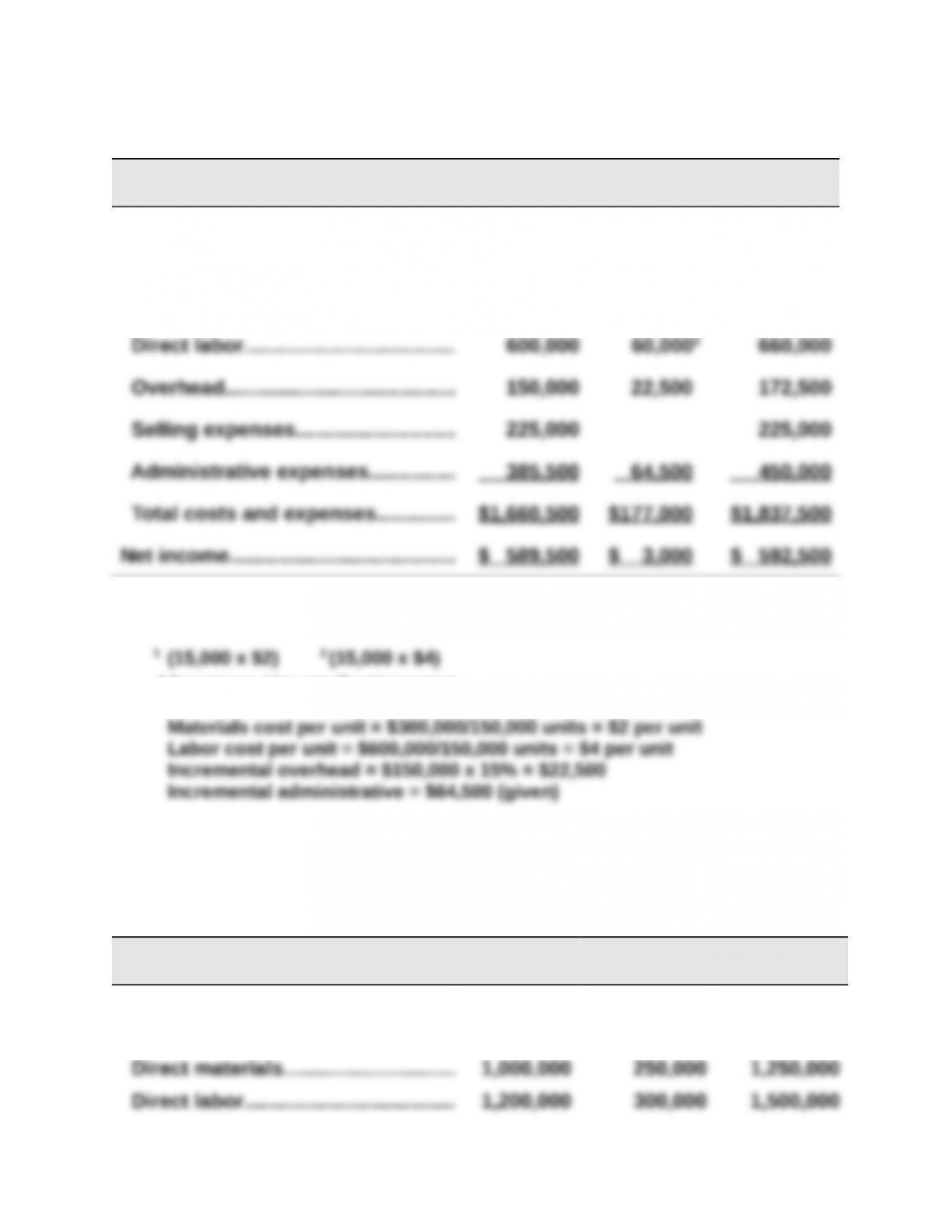

Exercise 25-18 (20 minutes)

Part 1

Normal Additional Combined

Volume Volume Total

Sales…………………………………………. $8,000,000 $1,500,000 $9,500,000

Costs and expenses

Variable overhead…………………….. 800,000 200,000 1,000,000

Calculations:

Normal volume sales: 80,000 units x $100 per unit = $8,000,000

Additional revenue from new order: 20,000 units x $75 per unit = $1,500,000

Based on this analysis, Goshford should accept the new business.

Part 2

Other factors that Goshford should consider before deciding whether to

accept the new business are:

Will regular customers demand a reduction in their selling price if they

hear of the sale to the new customer?

Exercise 25-19 (20 minutes)

Make Buy

Variable costs (65,000 @ $1.95)……………………. $126,750 —-

RECOMMENDATION : Note that the allocated fixed costs of $62,000 are not

relevant to this managerial decision because they will continue whether the

Note: We should recognize that this decision depends on the alternative uses for the

Exercise 25-20 (20 minutes)

Make Buy

Variable costs (40,000 @ $1.95)……………………. $78,000 —-

RECOMMENDATION : Note that the allocated fixed costs of $58,500 are not

relevant to this managerial decision because they will continue whether the

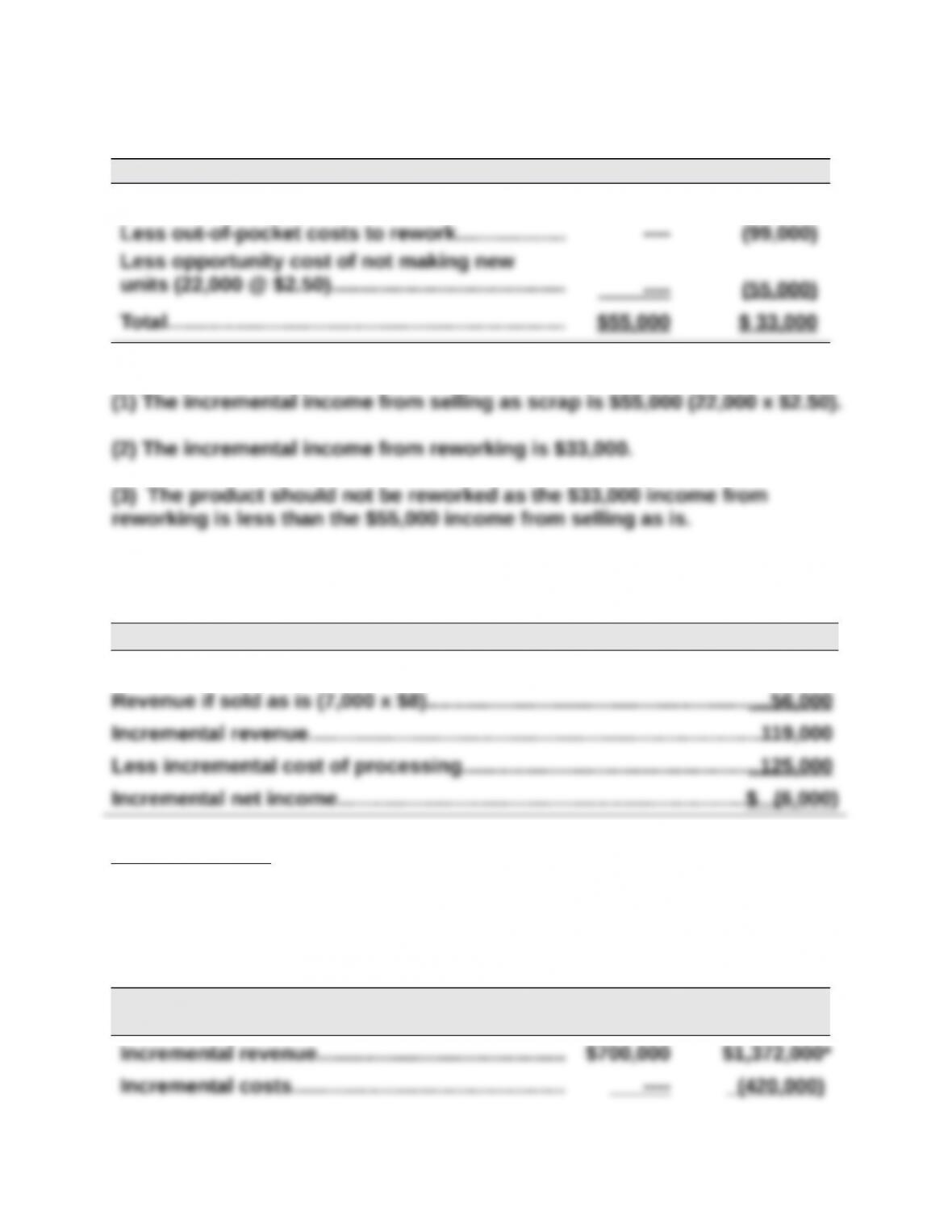

Exercise 25-21 (15 minutes)

Scrap Rework

Sale of scrapped/reworked units………………….. $55,000 $187,000

Exercise 25-22 (15 minutes)

INCREMENTAL REVENUE AND COST OF ADDITIONAL PROCESSING

Revenue if processed further (7,000 x $25)……………………………………….$175,000

RECOMMENDATION : Varto should not process these units further, as they will

be $6,000 worse off if they do so. (Note that the $22 per unit manufacturing

cost is not relevant because it is a sunk cost.)

Exercise 25-23 (25 minutes)

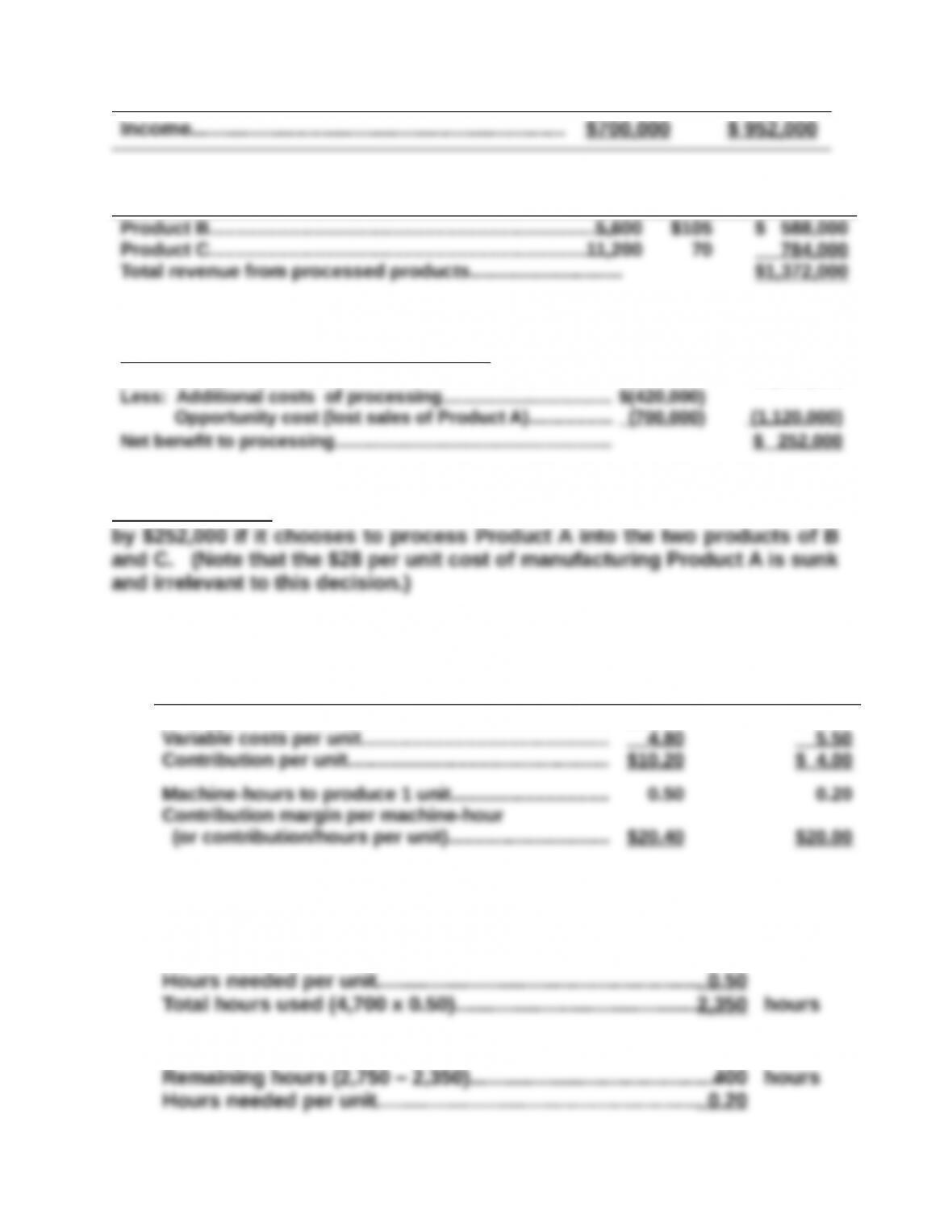

Sell as is

Process

further

*Revenue from processed products

Units Price Total

ALTERNATE SOLUTION FORMAT

Net income (loss) from processed products

Revenue if processed further…………………………………………. $1,372,000

RECOMMENDATION : This analysis shows that the company will be better off

Exercise 25-24 (30 minutes)

Preliminary computations

Contribution margin per hour Product TLX Product MTV

Selling price per unit…………………………………………. $15.00 $ 9.50

Exercise 25-24 (continued)

1. FOR PRODUCT TLX

Maximum sales……………………………………………………………..4,700 units

FOR PRODUCT MTV

SALES MIX RECOMMENDATION : These results suggest the company

should manufacture as many units of Product TLX as it can produce

2. CONTRIBUTION MARGIN FROM THE RECOMMENDED SALES MIX

Un

its

Contribution

per Unit Total

Exercise 25-25 (30 minutes)

Instructor note: In all cases, the total unavoidable expenses of $107,800 remain the same

because they cannot be avoided by eliminating departments.

1. DEPARTMENTS WITH EXPECTED NET LOSSES ELIMINATED

Total M N O P T

Sales………………………………………………$119,000 $63,000 $ 0 $56,000 $ 0 $ 0

Expenses

Avoidable……………………………………..32,200 9,800 0 22,400 0 0