Chapter 25 – Capital Budgeting and Managerial Decisions

EXERCISES

Exercise 25-1 (20 minutes)

Annual Net Cumulative

Cash Flows Cash Flows

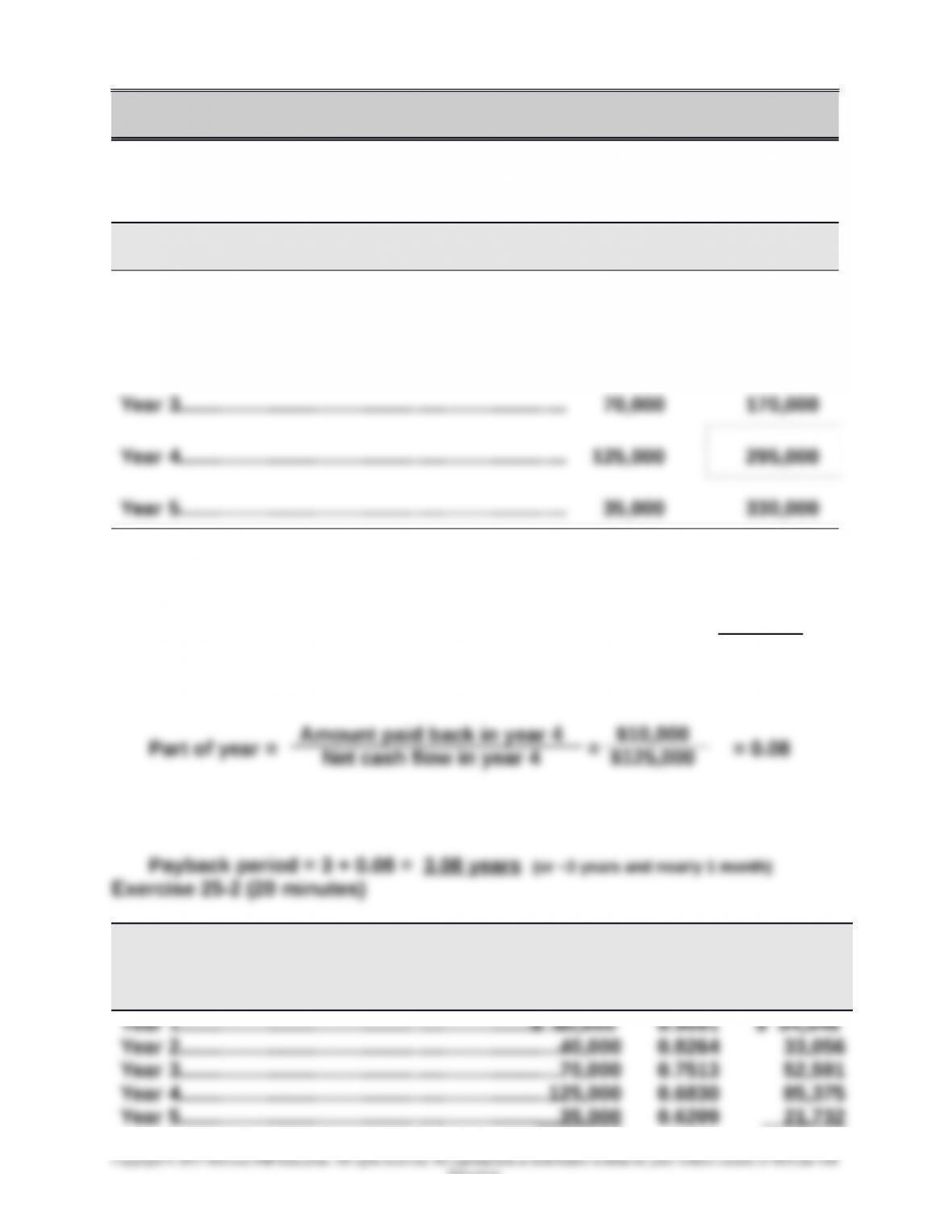

Year 1…………………………………………………………... $ 60,000 $ 60,000

Year 2…………………………………………………………... 40,000 100,000

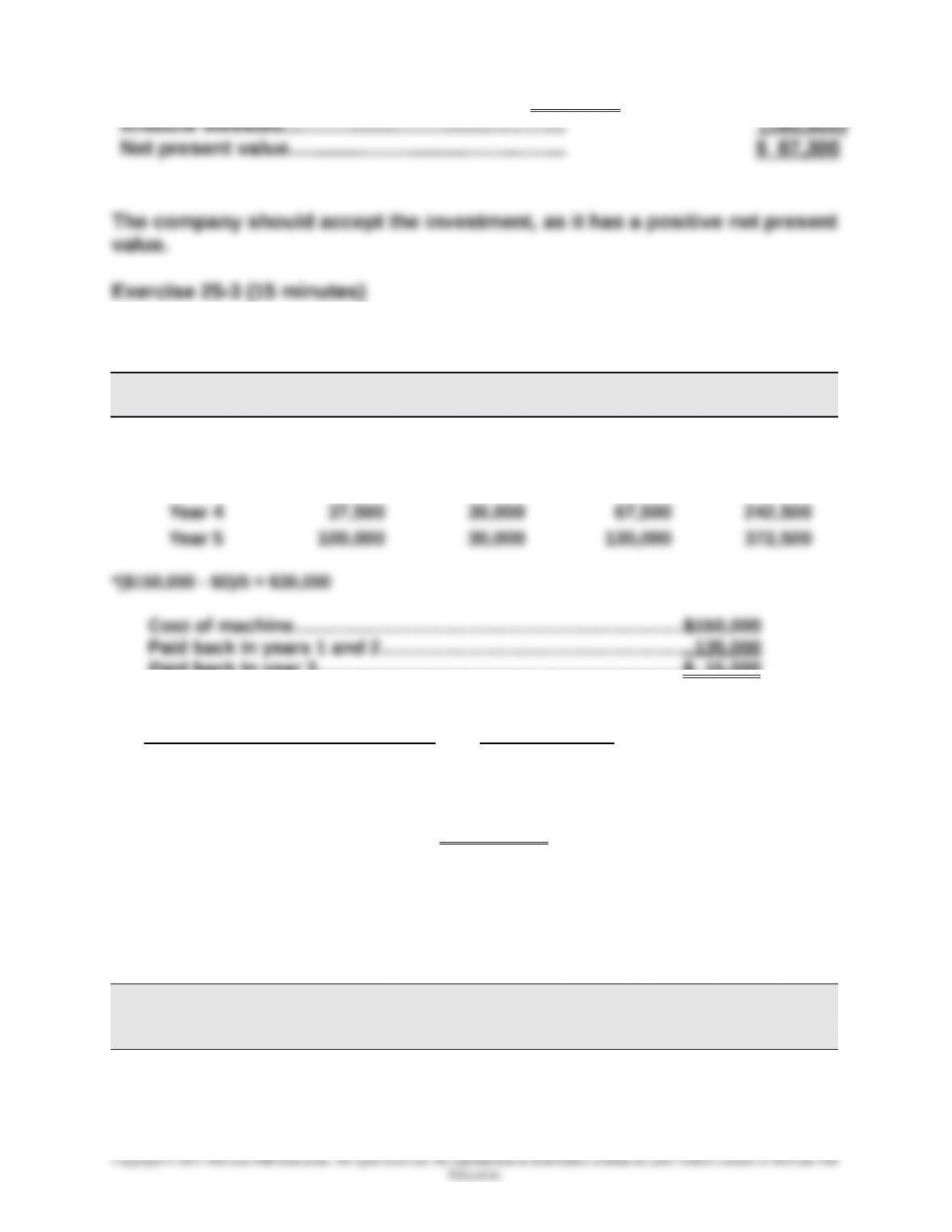

Cost of investment………………………………………………………….….……$180,000

Paid back in years 1-3……………………………………………………………... 170,000

Paid back in year 4…………………………………………………………………..$ 10,000

Net Cash

Flows

Present

Value of

1 at 10%

Present

Value of Net

Cash Flows

25-1481

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

Totals…………………………………………………….….….$330,000 247,300

ANNUAL CASH FLOWS

Net

Income Depreciation*

Net Cash

Flow

Cumulative

Cash Flow

Year 1 $ 10,000 $30,000 $ 40,000 $ 40,000

Year 2 25,000 30,000 55,000 95,000

Year 3 50,000 30,000 80,000 175,000

Paid back in year 3………………..………..……….………..………..…..…….$ 15,000

= = 0.188

Payback period = 2 + 0.188 = 2.188 years

Exercise 25-4 (30 minutes)

COMPUTATION OF ANNUAL DEPRECIATION EXPENSE

Double-declining balance rate = (100% / 5) x 2 = 40%

Annual Depr.

Beginning (40% of Accum. Depr. Ending

Year Book Value Book Value) at Year-End Book Value

1 $150,000 $60,000 $ 60,000 $90,000

2 90,000 36,000 96,000 54,000

25-1482

$15,000

$80,000

Amount paid back in year 3

Net cash flows in year 3

3 54,000 21,600 117,600 32,400

4 32,400 12,960 130,560 19,440

5 19,440 19,440 150,000 0

ANNUAL CASH FLOWS

Net

Income Depreciation

Net Cash

Flow

Cumulative

Cash Flow

Year 1 $ 10,000 $60,000 $ 70,000 $ 70,000

Year 2 25,000 36,000 61,000 131,000

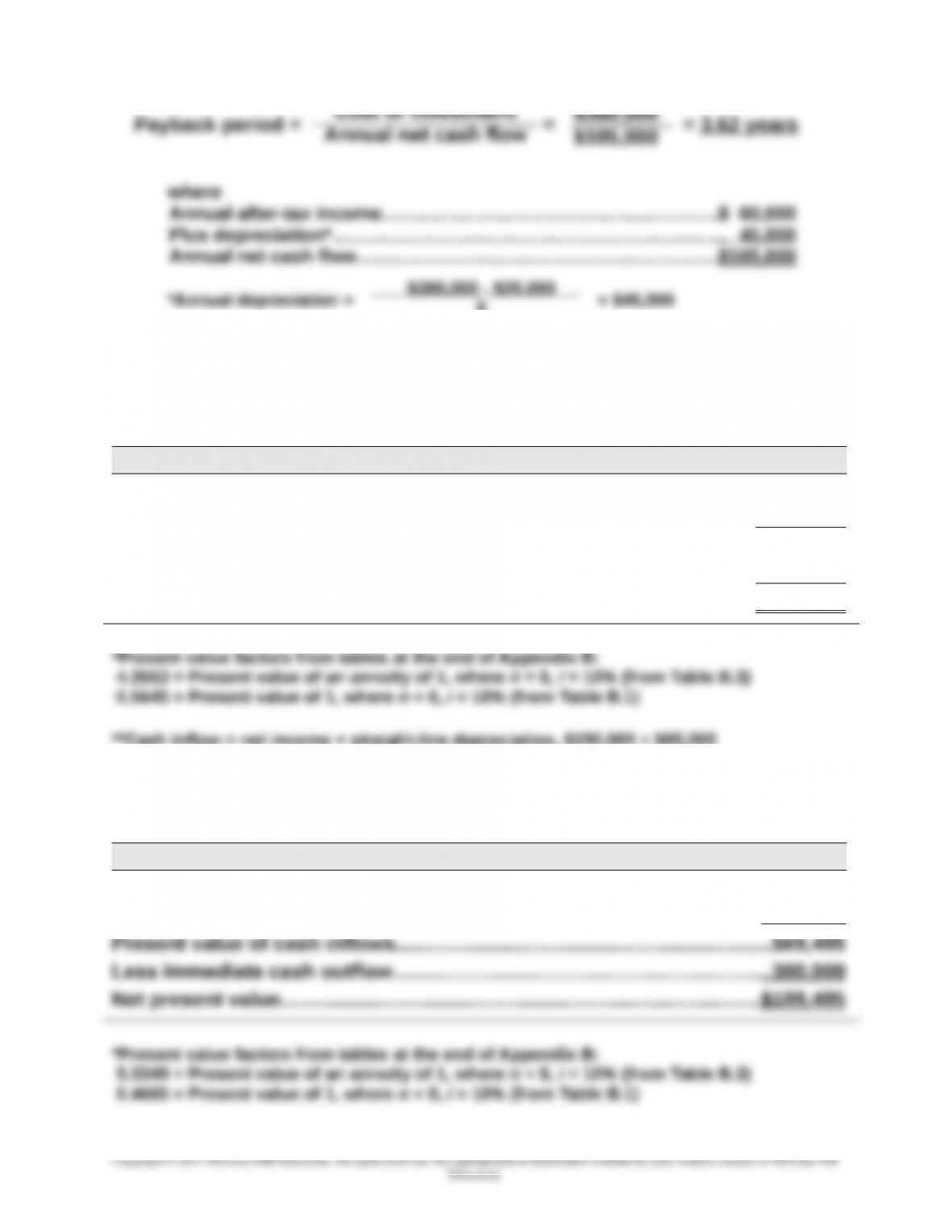

= = 0.265

a.

Payback period = = = 2.21 years

where

Annual after-tax income…………….……….………..………..……………....$150,000

b.

25-1483

Education.

$19,000

$71,600

Amount paid back in year 3

Net cash flows in year 3

Cost of investment

Annual net cash flow

$520,000

$235,000

6

Chapter 25 – Capital Budgeting and Managerial Decisions

Exercise 25-6 (20 minutes)

a.

Net present value of investment*

Present value of six $235,000** cash inflows ($235,000 x 4.3553)..........

$1,023,496

Present value of $10,000 at end of six years ($10,000 x 0.5645)............. 5,645

Present value of cash inflows……………………………………………….…….……. 1,029,411

Less immediate cash outflow…………………………………….…….…….…….….. 520,000

Net present value…………………………………………………..….…….…….…….…..$ 509,141

**Cash inflow = net income + straight-line depreciation, $150,000 + $85,000

Exercise 25-6 (continued)

b.

Net present value of investment*

Present value of eight $105,000** cash inflows ($105,000 x 5.3349)……..$560,165

Present value of $20,000 at end of eight years ($20,000 x 0.4665)..…..... 9,330

25-1484

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

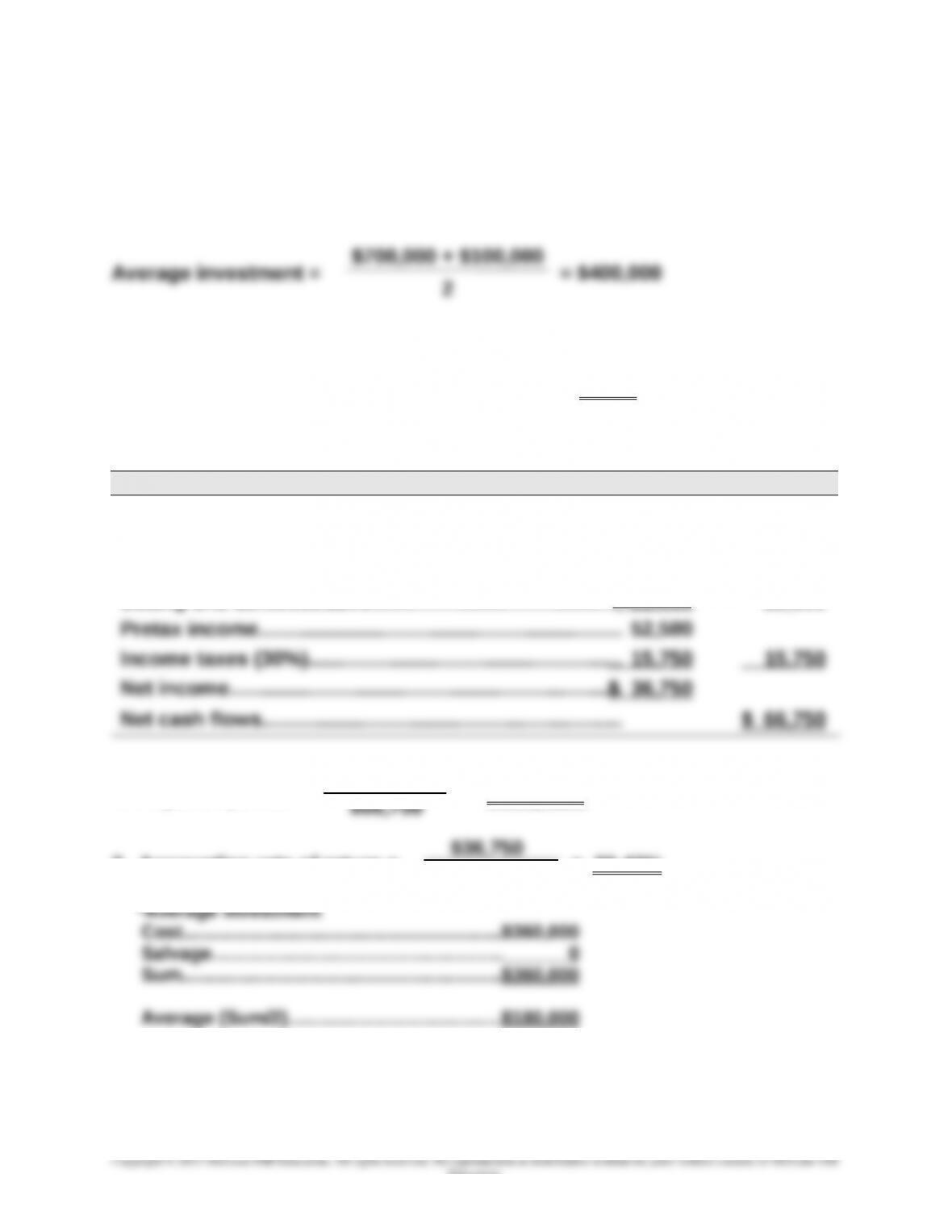

$380,000

Cost of investment

8

Chapter 25 – Capital Budgeting and Managerial Decisions

**Cash inflow = net income + straight-line depreciation, $60,000 + $45,000

Exercise 25-7 (15 minutes)

Accounting rate of return = $52,000 / $400,000 = 13.0%

Exercise 25-8 (20 minutes)

COMPUTING NET CASH FLOWS FROM NET INCOME

Net income Cash flows

Sales……………………………………………………………………..$225,000 $225,000

Materials, labor & overhead………………….….…….……...120,000 120,000

Depreciation………………………………..….…….…….…….…. 30,000

Selling and administrative……………………………………… 22,500 22,500

1. Payback period = = 5.39 years

2. Accounting rate of return = = 20.42%

25-1485

Education.

$360,000

$180,000*

Chapter 25 – Capital Budgeting and Managerial Decisions

Exercise 25-9 (15 minutes)

Annual

Net Cash

Flows

Present

Value of

Annuity

at 8%

Present

Value of

Net Cash

Flows

Years 1 through 6……………………..…….…….……...$ 66,750 4.6229 $ 308,579

25-1486

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

Exercise 25-10 (20 minutes)

PROJECT A

Net Cash

Flows

Present

Value of

1 at 10%

Present

Value of Net

Cash Flows

Year 1……………………………………………………………$ 40,000 0.9091 $ 36,364

Year 2……………………………………………………………56,000 0.8264 46,278

Year 3……………………………………………………………80,295 0.7513 60,326

Year 4……………………………………………………………90,400 0.6830 61,743

PROJECT B

Net Cash

Flows

Present

Value of

1 at 10%

Present

Value of Net

Cash Flows

Year 1…………………………………………………………… $ 32,000 0.9091 $ 29,091

Year 2……………………………………………………………50,000 0.8264 41,320

Year 3……………………………………………………………66,000 0.7513 49,586

Both projects have positive net present values. However, if the company

can choose only one project, it should select project B, since it has a

higher profitability index.

Exercise 25-11 (25 minutes)

a.

Present

Present

Value of Net

25-1487

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

Project X1 Net Cash

Flows

Value of

1 at 4%

Cash Flows

Year 1……………………………………………………………$ 25,000 0.9615 $ 24,038

Year 2……………………………………………………………35,500 0.9246 32,823

Project X2 Net Cash

Flows

Present

Value of

1 at 4%

Present

Value of Net

Cash Flows

Year 1……………………………………………………………$ 60,000 0.9615 $ 57,690

Year 2……………………………………………………………50,000 0.9246 46,230

b.

Profitability index, Project X1 = $110,646 / $80,000 = 1.38

a.

Project X1 Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of

Net Cash

Flows

Year 1……………………………………………………………$ 25,000 0.8929 $ 22,323

Year 2……………………………………………………………35,500 0.7972 28,301

25-1488

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

Project X2 Net Cash

Flows

Present

Value of

1 at 4%

Present

Value of Net

Cash Flows

Year 1……………………………………………………………$ 60,000 0.8929 $ 53,574

Year 2……………………………………………………………50,000 0.7972 39,860

Year 3…………………………………………………………… 40,000 0.7118 28,472

b.

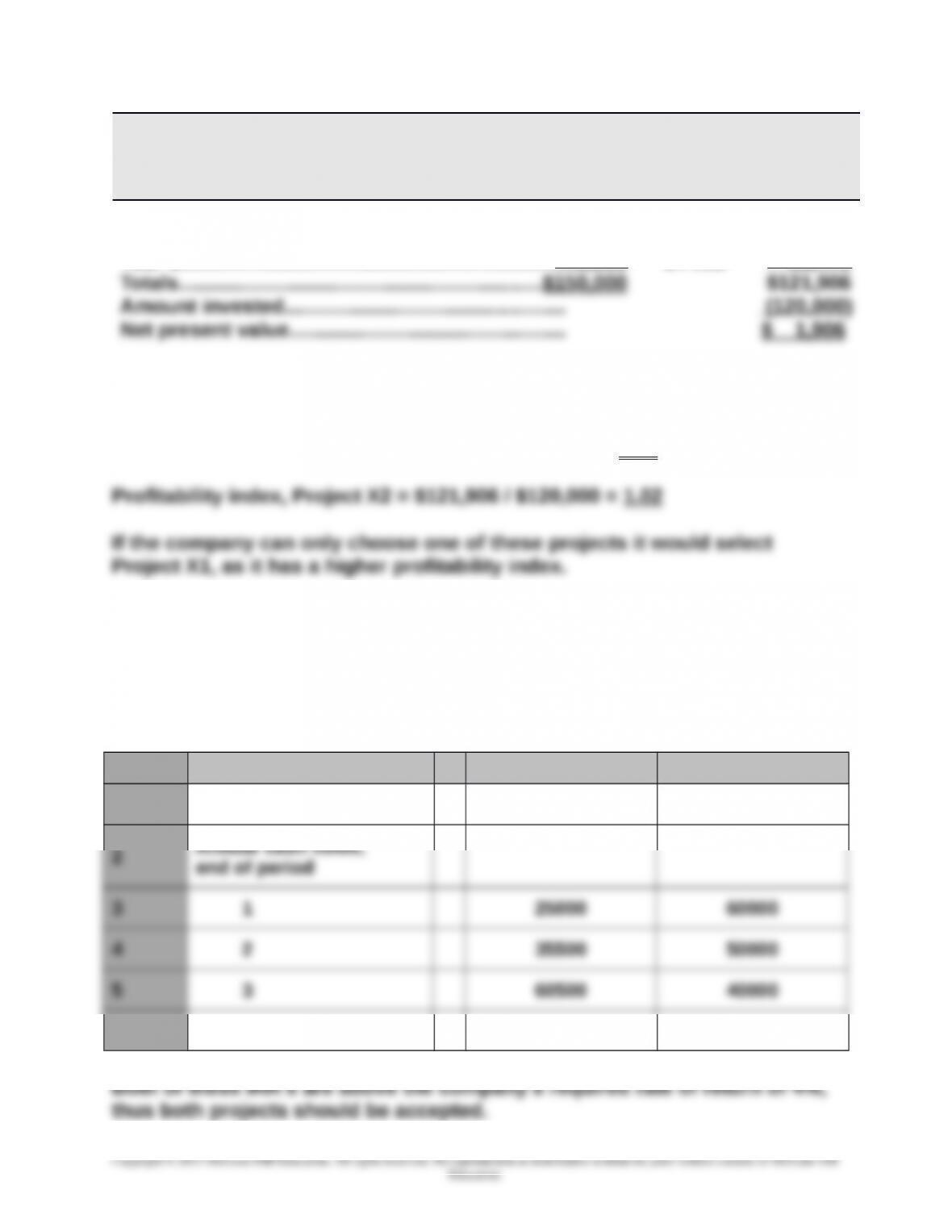

Profitability index, Project X1 = $93,688 / $80,000 = 1.17

Exercise 25-13 (20 minutes)

Using Excel, Project X1 (X2) has an internal rate of return of 20.34% (12.99%).

Project X1 Project X2

A B C D

1 Initial investment -80000 -120000

8 Formula for IRR =IRR(C1:C5) =IRR(D1:D5)

25-1489

Chapter 25 – Capital Budgeting and Managerial Decisions

Exercise 25-14 (35 minutes)

1.

PROJECT C1

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of Net

Cash Flows

Year 1……………………………………………………………$ 12,000 0.8929 $ 10,715

Year 2……………………………………………………………108,000 0.7972 86,098

25-1490