Quick Study 25-27 (15 minutes)

1. Payback period of investment = €80,000,000 / €16,000,000 = 5 years

EXERCISES

Exercise 25-1 (20 minutes)

Annual Net Cumulative

Cash Flows Cash Flows

Year 1…………………………………………………………. $ 60,000 $ 60,000

Cost of investment…………………………………………………………………$180,000

Exercise 25-2 (20 minutes)

Net Cash

Flows

Present

Value of

1 at 10%

Present

Value of Net

Cash Flows

Year 1………………………………………………………….$ 60,000 0.9091 $ 54,546

Year 2………………………………………………………….40,000 0.8264 33,056

The company should accept the investment, as it has a positive net present

value.

Exercise 25-3 (15 minutes)

ANNUAL CASH FLOWS

Net

Income Depreciation*

Net Cash

Flow

Cumulative

Cash Flow

Year 1 $ 10,000 $30,000 $ 40,000 $ 40,000

Year 2 25,000 30,000 55,000 95,000

Exercise 25-4 (30 minutes)

COMPUTATION OF ANNUAL DEPRECIATION EXPENSE

Double-declining balance rate = (100% / 5) x 2 = 40%

Annual Depr.

Beginning (40% of Accum. Depr. Ending

Year Book Value Book Value) at Year-End Book Value

1 $150,000 $60,000 $ 60,000 $90,000

ANNUAL CASH FLOWS

Net

Income Depreciation

Net Cash

Flow

Cumulative

Cash Flow

Year 1 $ 10,000 $60,000 $ 70,000 $ 70,000

Exercise 25-5 (20 minutes)

a.

b.

Exercise 25-6 (20 minutes)

a.

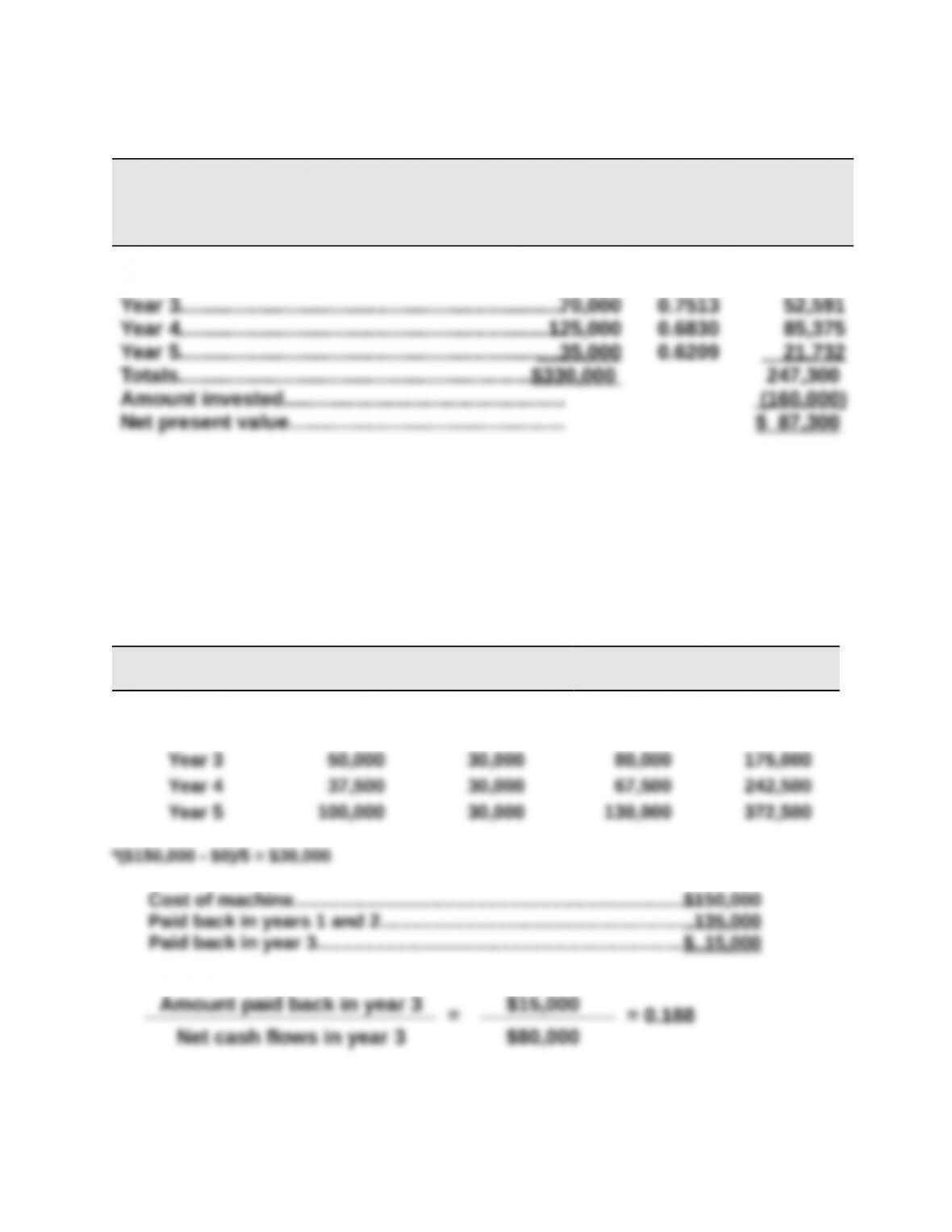

Net present value of investment*

Present value of six $235,000** cash inflows ($235,000 x 4.3553)..........

$1,023,496

*Present value factors from tables at the end of Appendix B:

6

**Cash inflow = net income + straight-line depreciation, $150,000 + $85,000

Exercise 25-6 (continued)

b.

Net present value of investment*

Present value of eight $105,000** cash inflows ($105,000 x 5.3349)……..$560,165

*Present value factors from tables at the end of Appendix B:

Exercise 25-7 (15 minutes)

Accounting rate of return = $52,000 / $400,000 = 13.0%

$700,000 + $100,000

Exercise 25-8 (20 minutes)

COMPUTING NET CASH FLOWS FROM NET INCOME

Net income Cash flows

Sales……………………………………………………………………$225,000 $225,000

Materials, labor & overhead…………………………………..120,000 120,000

*Average investment

Exercise 25-9 (15 minutes)

Annual

Net Cash

Flows

Present

Value of

Annuity

at 8%

Present

Value of

Net Cash

Flows

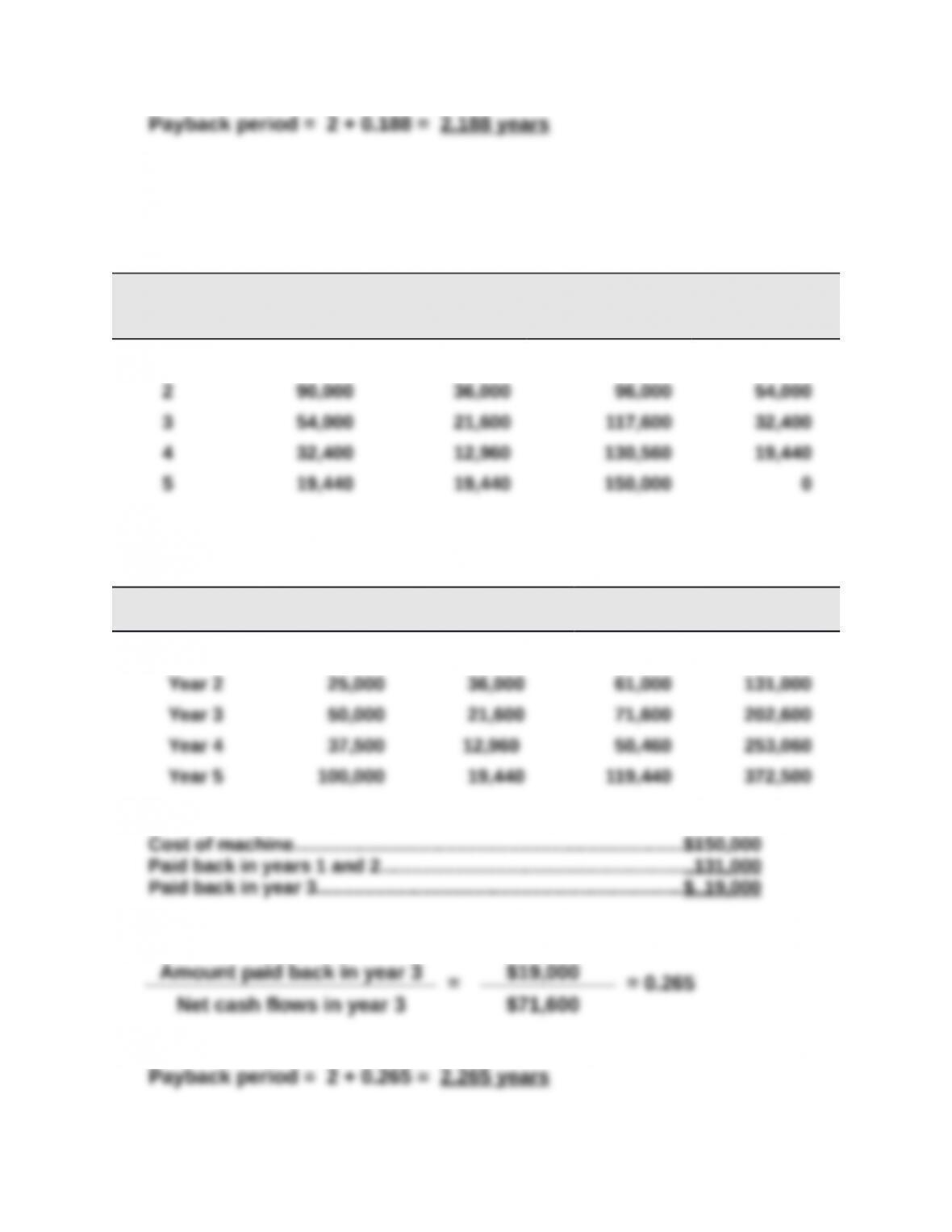

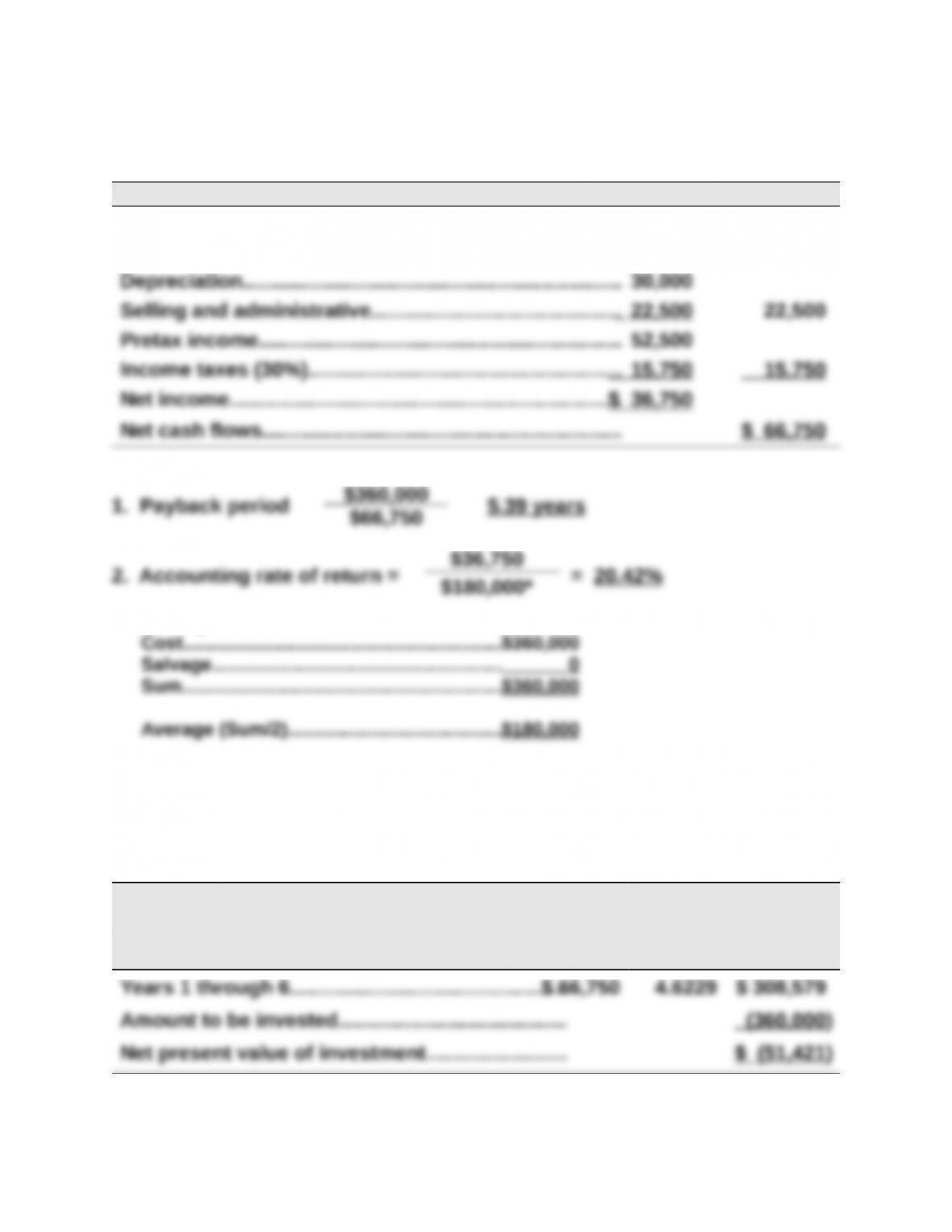

Years 1 through 6…………………………………………$ 66,750 4.6229 $ 308,579

Amount to be invested………………………………… (360,000)

Net present value of investment…………………… $ (51,421)

$180,000*

Based on this net present value analysis, the investment is not acceptable.

Exercise 25-10 (20 minutes)

PROJECT A

Net Cash

Flows

Present

Value of

1 at 10%

Present

Value of Net

Cash Flows

Year 1………………………………………………………….$ 40,000 0.9091 $ 36,364

Year 2………………………………………………………….56,000 0.8264 46,278

PROJECT B

Net Cash

Flows

Present

Value of

1 at 10%

Present

Value of Net

Cash Flows

Year 1…………………………………………………………. $ 32,000 0.9091 $ 29,091

Year 2………………………………………………………….50,000 0.8264 41,320

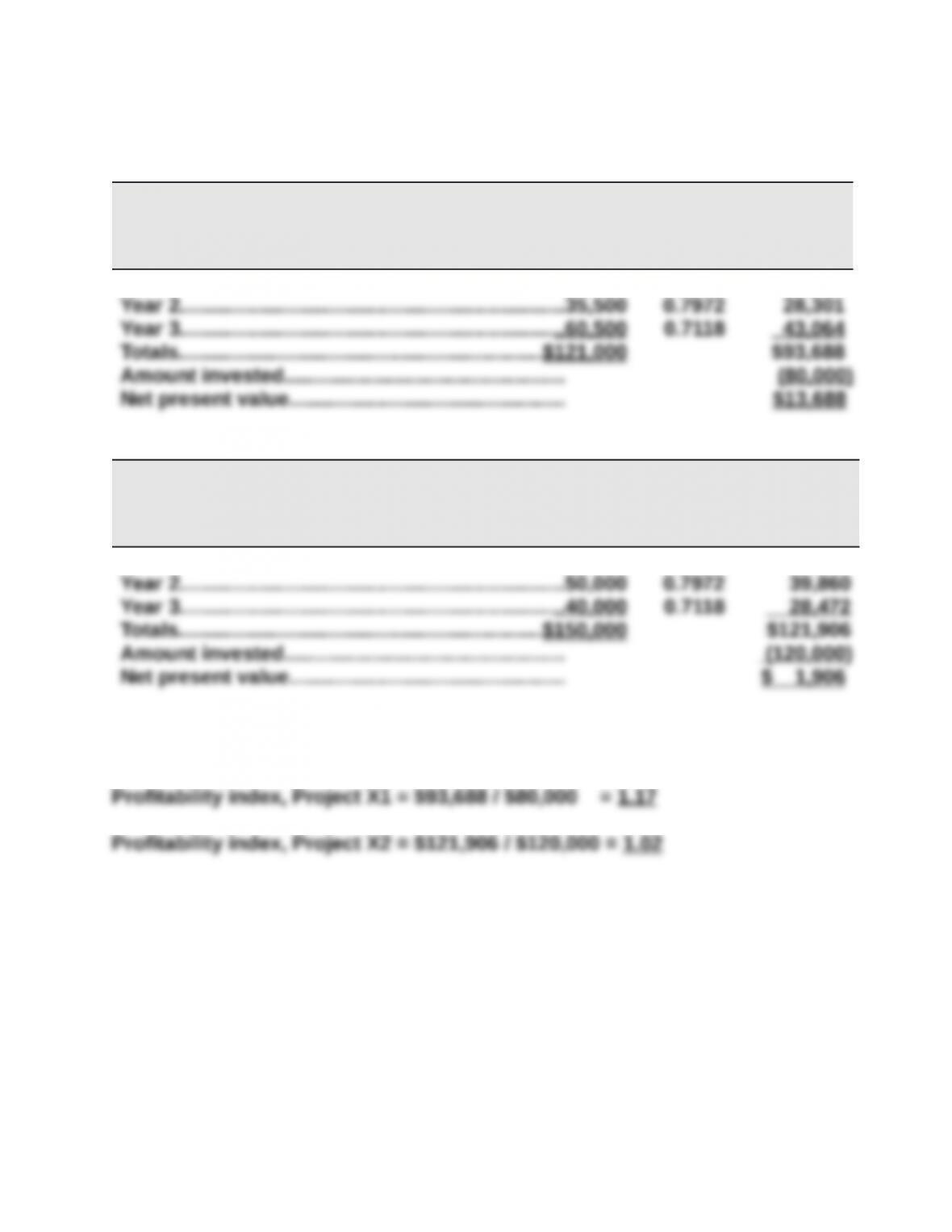

Both projects have positive net present values. However, if the company

Exercise 25-11 (25 minutes)

a.

Project X1 Net Cash

Flows

Present

Value of

1 at 4%

Present

Value of Net

Cash Flows

Year 1………………………………………………………….$ 25,000 0.9615 $ 24,038

Project X2 Net Cash

Flows

Present

Value of

1 at 4%

Present

Value of Net

Cash Flows

Year 1………………………………………………………….$ 60,000 0.9615 $ 57,690

b.

Exercise 25-12 (25 minutes)

a.

Project X1 Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of

Net Cash

Flows

Year 1………………………………………………………….$ 25,000 0.8929 $ 22,323

Project X2 Net Cash

Flows

Present

Value of

1 at 4%

Present

Value of Net

Cash Flows

Year 1………………………………………………………….$ 60,000 0.8929 $ 53,574

b.

If the company can only choose one of these projects it would select

Project X1, as it has a higher profitability index.