Chapter 25 – Capital Budgeting and Managerial Decisions

Chapter 25

Capital Budgeting and Managerial

Decisions

QUESTIONS

1. Capital budgeting decisions require careful analysis because they are generally

the most difficult and risky decisions that management faces.

2. Capital budgeting is the process of planning the acquisition or sale of plant

assets.

3. Capital budgeting decisions are risky because: (1) the outcomes are uncertain,

4. The payback period ignores both the present value of cash flows and all cash

flows after the payback period.

5. A shorter payback period is desirable because management prefers to reduce

the risk that the investment might not be profitable over the long run. As a result

6. If net income is earned evenly throughout each year and straight-line

7. When the present value of expected net cash flows, discounted at 10%, exceeds

the amount invested it indicates that the expected rate of return on the

8. Receiving $100 one year from today is worth less than $100 today because a

25-1481

9. The internal rate of return is the rate that produces a net present value of zero. If

10. Accelerated depreciation produces larger tax deductions and lower tax

payments in the early years of an asset’s life compared with straight-line

11. An out-of-pocket cost requires a current outlay of cash. An opportunity cost is

12. Sunk costs are irrelevant because they remain the same whether the product is

sold in its present condition or processed further.

13. There are virtually no incremental costs associated with shipping the additional

iPod. The company’s employees would not receive any additional compensation

14. Management could use one of the following common methods to evaluate the

15. The company might be willing to sell the units internationally if (a) the company

has excess capacity, (b) the incremental costs of manufacturing and selling the

units are less than $5,000 each, which it appears to be at $4,000 variable cost per

unit (c) the international sales won’t reduce domestic sales, and (d) the

international buyer is unwilling to pay more than $5,000.

QUICK STUDIES

Quick Study 25-1 (5 minutes)

Payback period of investment = $27,000 / $9,000 = 3.0 years

Quick Study 25-2 (5 minutes)

Net present value of investment

Present value of four $9,000 cash inflows ($9,000 x 3.1699*)….…..…..….$28,529

Less immediate cash outflow…………………………………………..…..…..…..…. 27,000

25-1482

Chapter 25 – Capital Budgeting and Managerial Decisions

Net present value…………………………………………………..…..…..…..…..…..…..$ 1,529

*Present value factor from Table B.3:

3.1699 = Present value of an annuity of 1, where n = 4, i = 10%

Quick Study 25-3 (5 minutes)

than the hurdle rate of 10%, the company should make the investment.

Quick Study 25-4 (10 minutes)

1. If all else is equal, Investment A would be preferred over Investment B

because of A’s shorter payback period.

2. However, if the investments are different, then there are at least four

reasons why Investment B might be preferred over Investment A:

i. The present value of cash flows from Investment B might greatly

exceed the present value of cash flows from Investment A.

25-1483

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

Quick Study 25-7 (5 minutes)

Accounting rate of return = $1,950 / [($45,000 + $6,000)/2] = 7.65%

Quick Study 25-8 (15 minutes)

Net present value of investment*

Present value of three $14,950 cash inflows ($14,950 x 2.2832)…………..$34,134

Present value of $6,000 at end of three years ($6,000 x 0.6575)……..…... 3,945

Present value of cash inflows……………………………………………….…..…..…. 38,079

Quick Study 25-9 (15 minutes)

Net present value of investment*

Present value of seven $10,000 cash inflows ($10,000 x 4.8684)....…..…$48,684

Present value of $6,000 at end of seven years ($6,000 x 0.5132)…......... 3,079

Present value of cash inflows……………………………………………….…..…..…. 51,763

Quick Study 25-10 (10 minutes)

Project A: Profitability index = $1,100,000 / $400,000 = 2.75

25-1484

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

Project B: Profitability index = $6,000,000 / $4,000,000 = 1.50

Higher values of the profitability index indicate a better project, so on the

basis of this measure the company should select Project A.

Quick Study 25-11 (15 minutes)

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of Net

Cash Flows

Year 1……………………………………………………………$100,000 0.8929 $ 89,290

Year 2……………………………………………………………90,000 0.7972 71,748

Year 3…………………………………………………………… 75,000 0.7118 53,385

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of Net

Cash Flows

Year 1……………………………………………………………$100,000 0.8929 $ 89,290

Year 2……………………………………………………………90,000 0.7972 71,748

Year 3…………………………………………………………… 95,000 0.7118 67,621

Quick Study 25-13 (10 minutes)

Present value factor = Amount invested = $47,947 = 2.2832 (rounded)

Net cash flows $21,000

25-1485

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

Quick Study 25-14 (10 minutes)

Net present value of investment

Present value of three $21,000 cash inflows ($21,000 x 2.5771*)....…..…$54,119

Less immediate cash outflow…………………………………………..…..…..…..…. 47,947

Net present value…………………………………………………..…..…..…..…..…..…..$ 6,172

*Present value factor from Table B.3:

2.5771 = Present value of an annuity of 1, where n = 3, i = 8%

Quick Study 25-15 (5 minutes)

Quick Study 25-16 (15 minutes)

INCREMENTAL INCOME FROM NEW BUSINESS

Sales (750 units @ $250)…………………………………………………..…..…..…..…$ 187,500

The company should accept the offer for new business as it increases

income by $25,000.

Quick Study 25-17 (15 minutes)

Incremental cost analysis

Costs of purchasing

Cost to purchase Product B………………………………………………………..…....$5.00

Revenue loss from reduced price ($13.50 – $12.00)………………………..….. 1.50

25-1486

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

Analysis: Kando Co. should continue to manufacture and sell Product A.

Quick Study 25-18 (10 minutes)

(Per unit) Make Buy

Direct materials………………………….…..…..…..…... $2.25 —-

25-1487

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

Quick Study 25-19 (15 minutes)

Quick Study 25-20 (15 minutes)

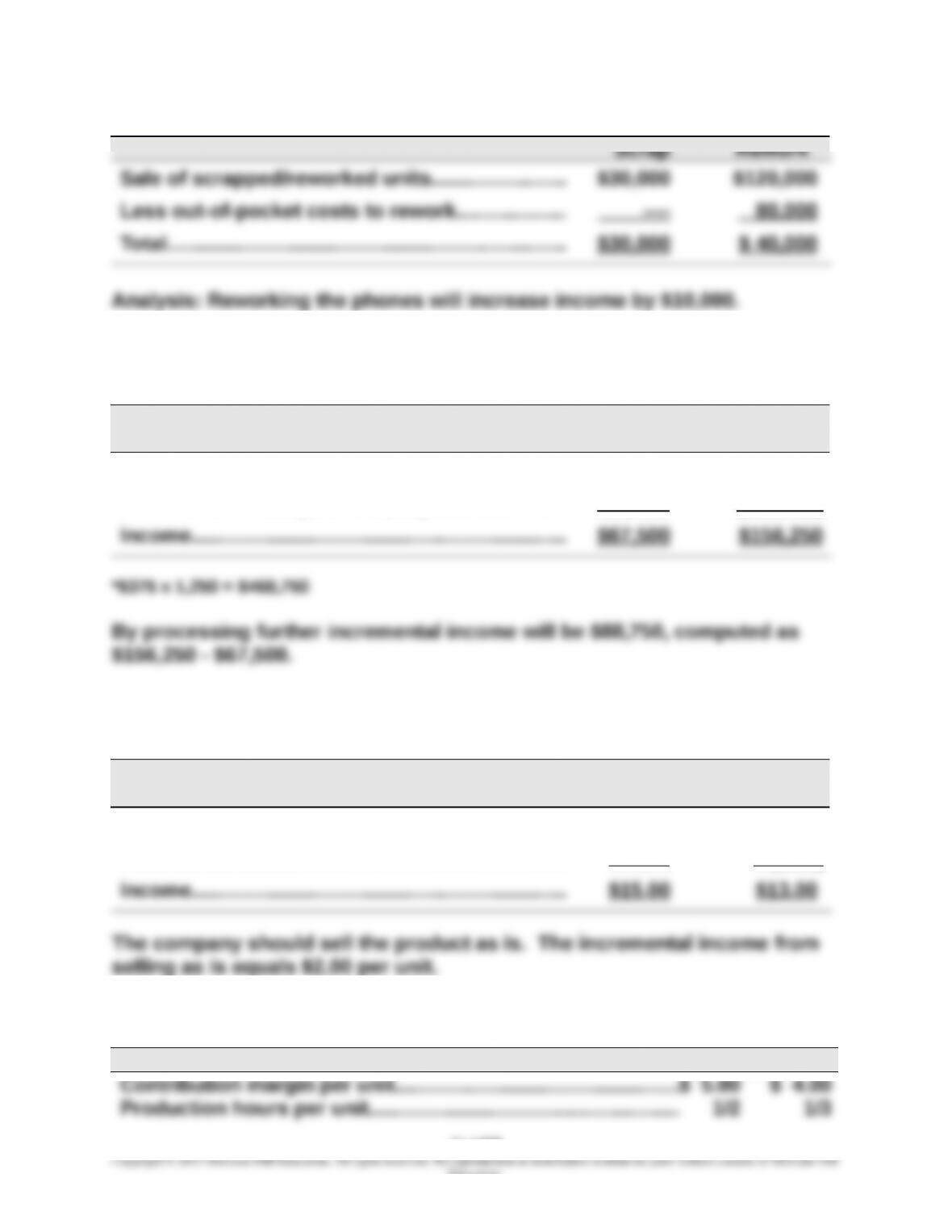

Sell as is

Process

further

Incremental revenue………………………..…..…..….. $67,500 $468,750*

Incremental costs ($250 x 1,250)………..…..…..… —- (312,500)

Quick Study 25-21 (5 minutes)

(Per unit) Sell as is

Process

further

Incremental revenue………………………..…..…..….. $15.00 $21.00

Incremental costs…………………………………………. —- (8.00)

Quick Study 25-22 (15 minutes)

X Y

25-1488

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

Contribution margin per production hour..…..…..…..…..…....$10.00 $12.00

Sales mix analysis: Since Excel Memory can sell all it can produce of both

products, it should allocate all of its production capacity to Product Y. This

is because Y yields a $12 contribution margin per production hour (versus

$10 for X).

Quick Study 25-23 (15 minutes)

Avoidable Unavoidable

Expenses Expenses

Cost of goods sold……………………………………….. $56,000 —-

Direct expenses……………………………………………. 9,250 $1,250

The division should not be eliminated because its sales of $72,000 are

greater than its avoidable expenses of $71,720.

Quick Study 25-24 (5 minutes)

Avoidable

Expenses

Variable costs……………………………………..…..…... $145,000

Direct fixed costs……………………….…..…..…..…... 30,000

Indirect expenses (40% avoidable)..…...…..……. 20,000

Quick Study 25-25 (10 minutes)

25-1489

Education.

Chapter 25 – Capital Budgeting and Managerial Decisions

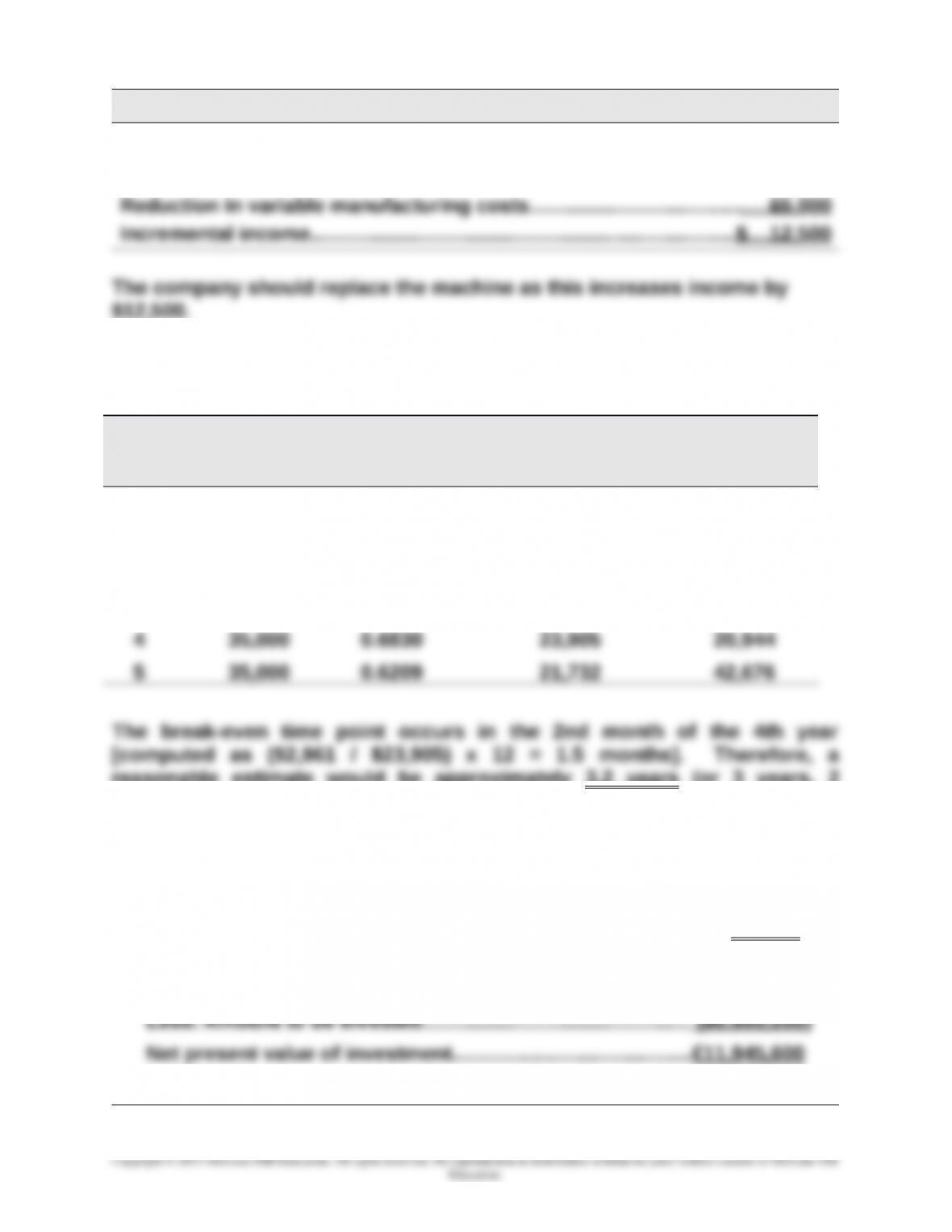

INCREMENTAL INCOME FROM REPLACING MACHINE

Cost to buy new machine…………………………………………………………….…...$(112,500)

Cash received to trade in old machine……………………….…..………..…..….. 60,000

Quick Study 25-26 (15 minutes)

Year Cash flows

Present value

of 1 at 10%

Present value of

cash flows

Cumulative

present value of

cash flows

0 $(90,000) 1.0000 $(90,000) $(90,000)

1 35,000 0.9091 31,819 (58,181)

2 35,000 0.8264 28,924 (29,257)

3 35,000 0.7513 26,296 (2,961)

reasonable estimate would be approximately 3.2 years (or 3 years, 2

months) for break-even time.

Quick Study 25-27 (15 minutes)

1. Payback period of investment = €80,000,000 / €16,000,000 = 5 years

2. Present value of cash inflows (€16,000,000 x 5.7466) €91,945,600

25-1490