Chapter 24 – Performance Measurement and Responsibility Accounting

Problem 24-5AB (60 minutes)

Part 1

Allocations of joint costs on the basis of sales values

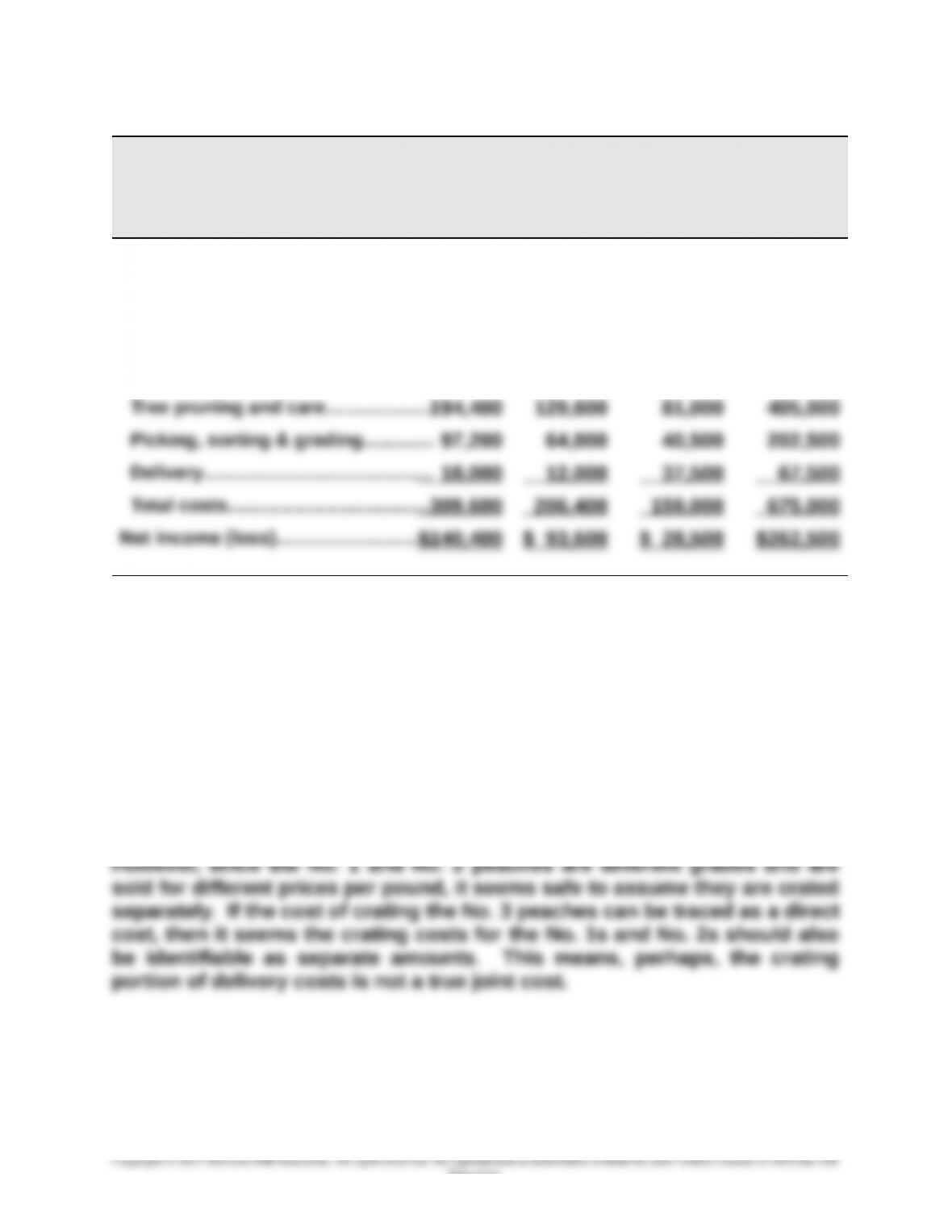

Tree pruning and care: $405,000

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1……………………….…$450,000 48.0% $194,400

Picking, sorting, and grading: $202,500

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1……………………….…$450,000 48.0% $ 97,200

Grade

Value

of Total

Cost

No. 1……………………….…$450,000 60.0% $18,000

No. 2……………………….…300,000 40.0 12,000

**The No. 3 Grade delivery costs are given in the problem description.

Problem 24-5AB (Continued)

24-1425

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Part 2

GEORGIA ORCHARDS

Income Statement

For Year Ended December 31, 2015

No. 1 No. 2 No. 3 Combined

Sales (by grade)

No. 1: 300,000 lbs. @ $1.50............

$450,000

No. 2: 300,000 lbs. @ $1.00............ $300,000

No. 3: 750,000 lbs. @ $0.25............ $187,500

Total sales….…………………….….….… $937,500

Costs

Part 3

Delivery costs include both crating and hauling costs. Georgia is able to

identify the portion of the cost directly related to the No. 3 peaches,

presumably because the No. 3s are going to a different destination than the

No. 1 and No. 2 peaches. If the No. 1s and No. 2s are going to the same

place, then the hauling portion of the delivery cost may truly be a joint cost,

at least for the No. 1 and No. 2 peaches.

24-1426

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

PROBLEM SET B

Problem 24-1B (50 minutes)

Part 1

a.

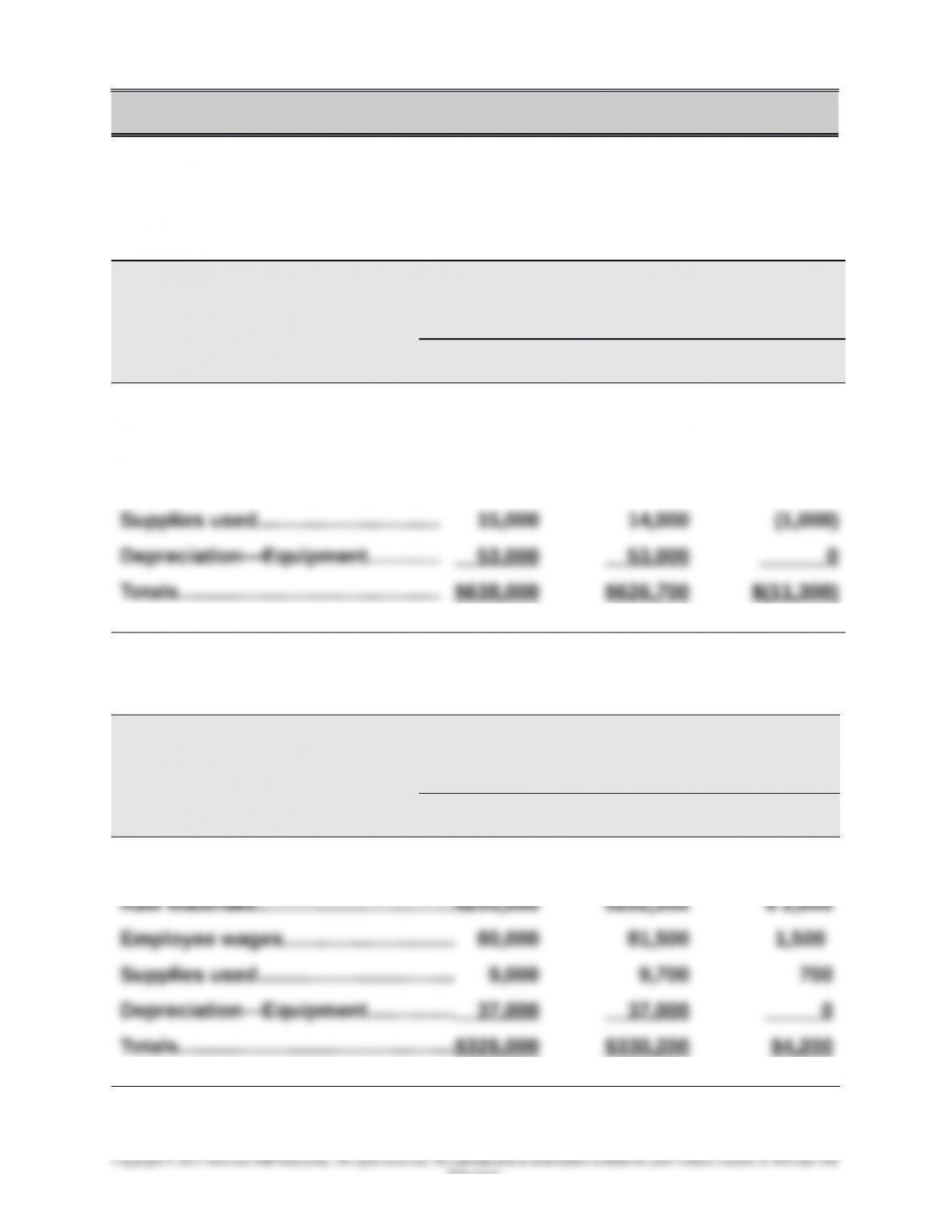

Responsibility Accounting Performance Report

Dept. Manager, Refrigerator Department

For the Month of April

Budgeted Actual Over (Under)

Amount Amount Budget

Controllable Costs

Raw materials….………..…………..... $400,000 $385,000 $(15,000)

Employee wages…………………….… 170,000 174,700 4,700

b.

Responsibility Accounting Performance Report

Dept. Manager, Dishwasher Department

For the Month of April

Budgeted Actual Over (Under)

Amount Amount Budget

Controllable Costs

24-1427

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Problem 24-1B (Continued)

c.

Controllable Costs

Dept. manager salaries…....... $ 104,000 $ 101,500 $ (2,500)

Utilities……………………………… 48,000 55,200 7,200

Building rent….……..…………... 80,000 82,300 2,300

Other office salaries…….…….. 40,000 35,200 (4,800)

Part 2

The refrigerator department manager did a good job of controlling costs

and meeting the budget, spending $11,300 below budget. However, the

dishwasher department did not do such a good job, spending $4,200 above

the budgeted amount. The plant manager’s controllable costs would have

been under budget by $300 if the Dishwasher department manager’s actual

costs had been equal to budgeted costs.

Problem 24-2B (60 minutes)

Part 1

24-1428

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Department Square

Footage

Rate Total

Style’s Dept…..……..…… 2,000 $23.25 $46,500

Part 2

Market rates are used to allocate occupancy costs for the building rent.

Lighting and cleaning costs are allocated to the departments on all three

floors at the average rate per square foot. Costs assigned to each class are:

Occupancy Costs

Total

Costs

Value-Based

Costs

Usage-Based

Costs

Building rent….……..…………... $400,000 $400,000

Value-based costs are allocated in two steps

(i) Compute market value of each floor

Floor

Square

Footage

Value per

Sq. Ft. Total

First floor……………………………7,500 $40 $300,000

Second floor….……..…….........7,500 20 150,000

(ii) Allocate the $400,000 to each floor based on its percent of market value

Floor

Market

Value

% of

Total

Allocated

Cost

Cost per

Sq. Ft.

First floor……………………………$300,000 60% $240,000 $32.00

24-1429

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

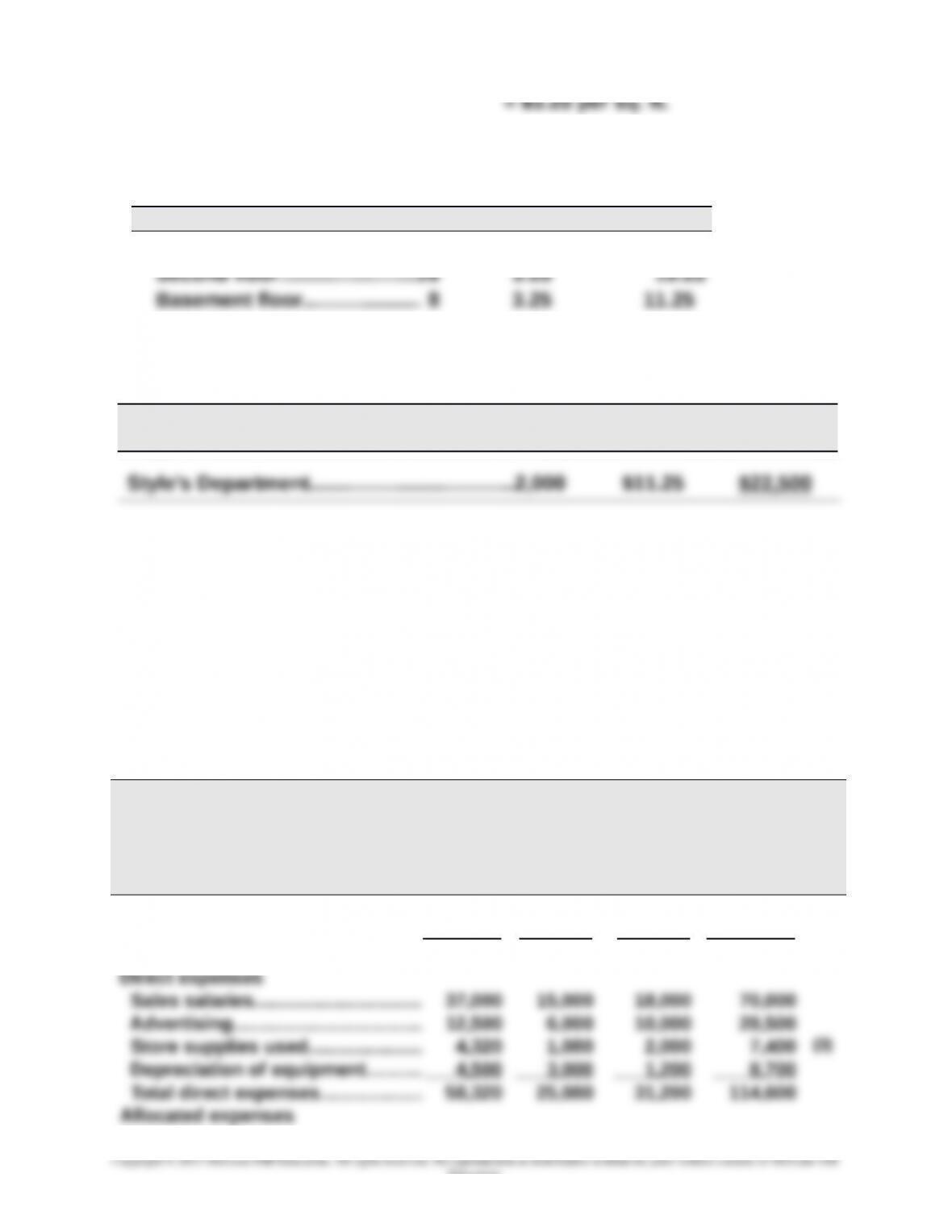

Total allocation rates for the departments on all three floors are

Floor Value Usage Total

First floor………….……………..$32 $3.25 $35.25

These rates are applied to allocate occupancy costs to Style’s department:

Department

Square

Footage Rate Total

Part 3

A basement manager would prefer the allocation based on market value. This

is a reasonable and logical approach to allocation of occupancy costs. With a

flat rate method, all square footage has equal value. This is not logical for this

type of occupancy. Less cost would be allocated to the basement

departments if the market value method were used.

Problem 24-3B (70 minutes)

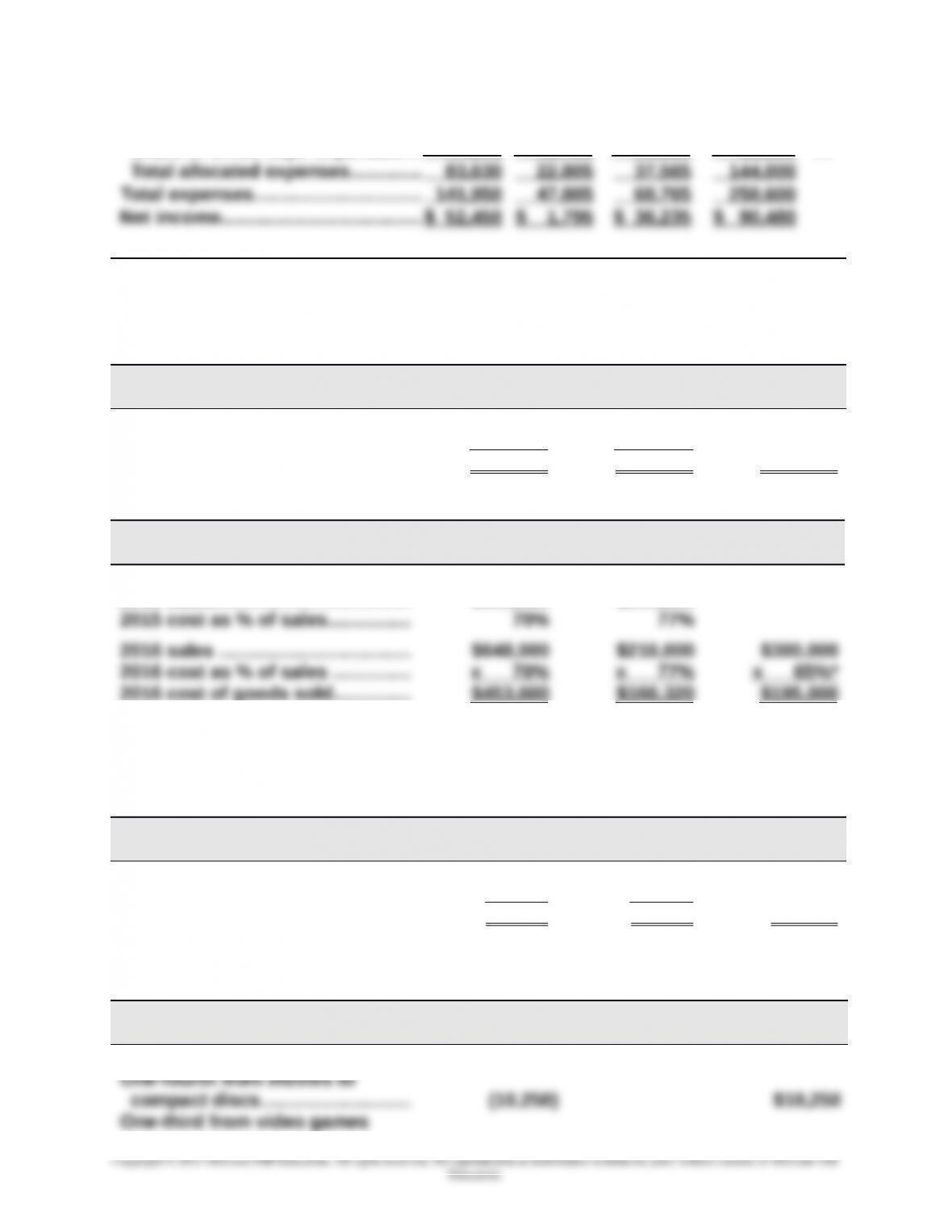

BONANZA ENTERTAINMENT

Forecasted Departmental Income Statements

For Year Ended December 31, 2016

Movies

Video

Games

Compact

Discs Combined

Sales…..……………………………….….... $648,000 $216,000 $300,000 $1,164,000 (1)

Cost of goods sold……..….….......... 453,600 166,320 195,000 814,920 (2)

Gross profit………..………………..….... 194,400 49,680 105,000 349,080

24-1430

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Rent expense……….………………..… 30,750 6,000 13,250 50,000 (4)

Utilities expense…………………….… 5,535 1,080 2,385 9,000 (4)

Share of office dept. expenses.... 47,345 15,725 21,930 85,000 (5)

Supporting Computations—coded (1) through (5) in statement above

Note 1 (Sales)

Movies

Video

Games

Compact

Discs

2015 sales…………………….….…..…. $600,000 $200,000

Growth rate (8% increase)........... x 108% x 108%

2016 sales…………………….….…..…. $648,000 $216,000 $300,000

Note 2 (Cost of Goods Sold)

Movies

Video

Games

Compact

Discs

2015 cost of goods sold…………... $420,000 $154,000

2015 sales…………………….….…..…. $600,000 $200,000

* The 65% cost of goods sold percent is computed as 100% minus the predicted 35% gross margin.

Problem 24-3B (Continued)

Note 3 (Store Supplies Used)

Movies

Video

Games

Compact

Discs

2015 store supplies used ……...... $ 4,000 $ 1,000

Growth rate (8% increase)........... x 108% x 108%

2016 store supplies …..…............. $ 4,320 $ 1,080 $ 2,000

Note 4 (Rent and Utilities)

Movies

Video

Games

Compact

Discs

2015 rent …….…………..….….…..….. $41,000 $ 9,000

24-1431

2016 rent …….…………..….….…..….. $30,750 $ 6,000 $13,250

Percent of total ………..………….….. 61.5% 12.0% 26.5%

2016 allocation of $9,000

total utilities ………….…………..….. $ 5,535 $1,080 $ 2,385

2016 sales ……………………….…..…. $648,000 $216,000 $300,000

Percent of total sales* …..…......... 55.7% 18.5%†25.8%

2016 allocation of $85,000

* Rounded to the nearest 0.1% * If students round to something other than one-tenth of a percent,

their numbers will slightly vary.

†Adjusted to eliminate rounding difference.

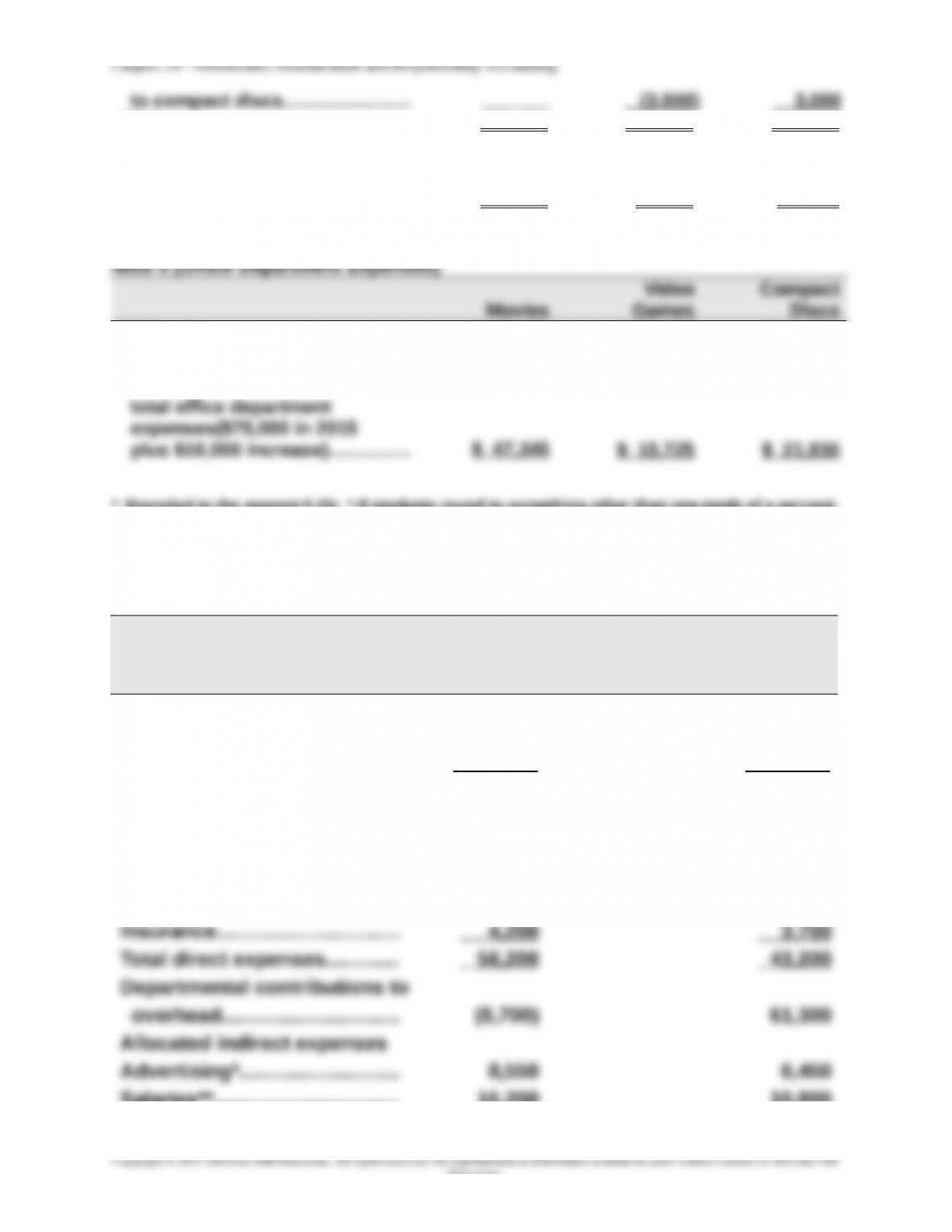

Problem 24-4B (45 minutes)

Part 1

SADAR COMPANY

Departmental Contribution Statements

Videos Music

Sales…………………..…..………… $370,500 $279,500

Cost of goods sold……..……… 320,000 175,000

Gross profit……………….………. 50,500 104,500

Direct expenses

Salaries……………………………... 35,000 25,000

Maintenance……………………....

Utilities………………………………

12,000

5,000

10,000

4,500

Salaries**………………………..…. 16,200 10,800

24-1432

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Office****…………………………....

Total indirect expenses……….

2,000

26,750

1,200

18,450

Operating income……….……… $ (32,450) $ 42,850

*Advertising allocation: Sales % Amount Allocated

Videos $370,500 57% $15,000 $ 8,550

Music 279,500 43% 15,000 6,450

Total $650,000 100% $15,000

** Salaries allocation: Employees % Amount Allocated

Problem 22-4B (Concluded)

Part 2

The videos department has both a negative contribution to overhead and a

negative departmental net income. It is not even covering its own direct

costs, and is therefore not contributing anything to overhead. Before

deciding whether to eliminate the video department, Sadar should consider

24-1433