Chapter 24 – Performance Measurement and Responsibility Accounting

Exercise 24-21 (20 minutes)

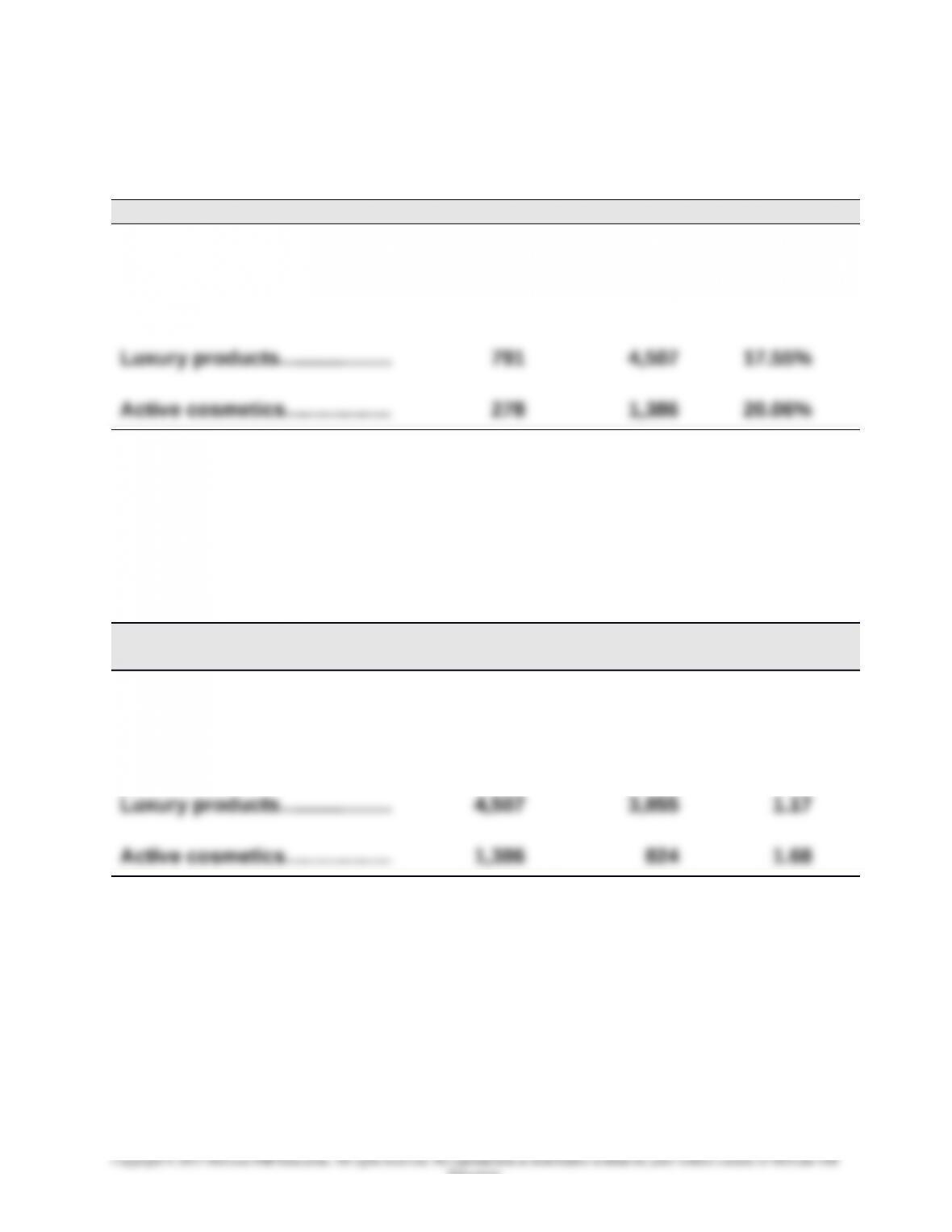

(1) Profit margin = Income/Sales

Investment center Income* Sales* Profit margin

Professional products..…..... € 552 €2,717 20.32%

Consumer products………….. 1,765 9,530 18.52%

*In € millions

The professional products department has the highest profit margin.

(2) Investment turnover = Sales/Average invested assets

Investment center

Sales*

Avg. assets* Investment

turnover

Professional products..…..... €2,717 €2,570 1.06

Consumer products………….. 9,530 5,745 1.66

*In € millions. Avg. assets = Beginning assets plus ending assets, divided by two.

Note: Profit margin and investment turnover amounts are rounded to two decimal places.

The Active cosmetics department has the highest investment turnover.

PROBLEM SET A

Problem 24-1A (50 minutes)

Part 1

a.

24-1425

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

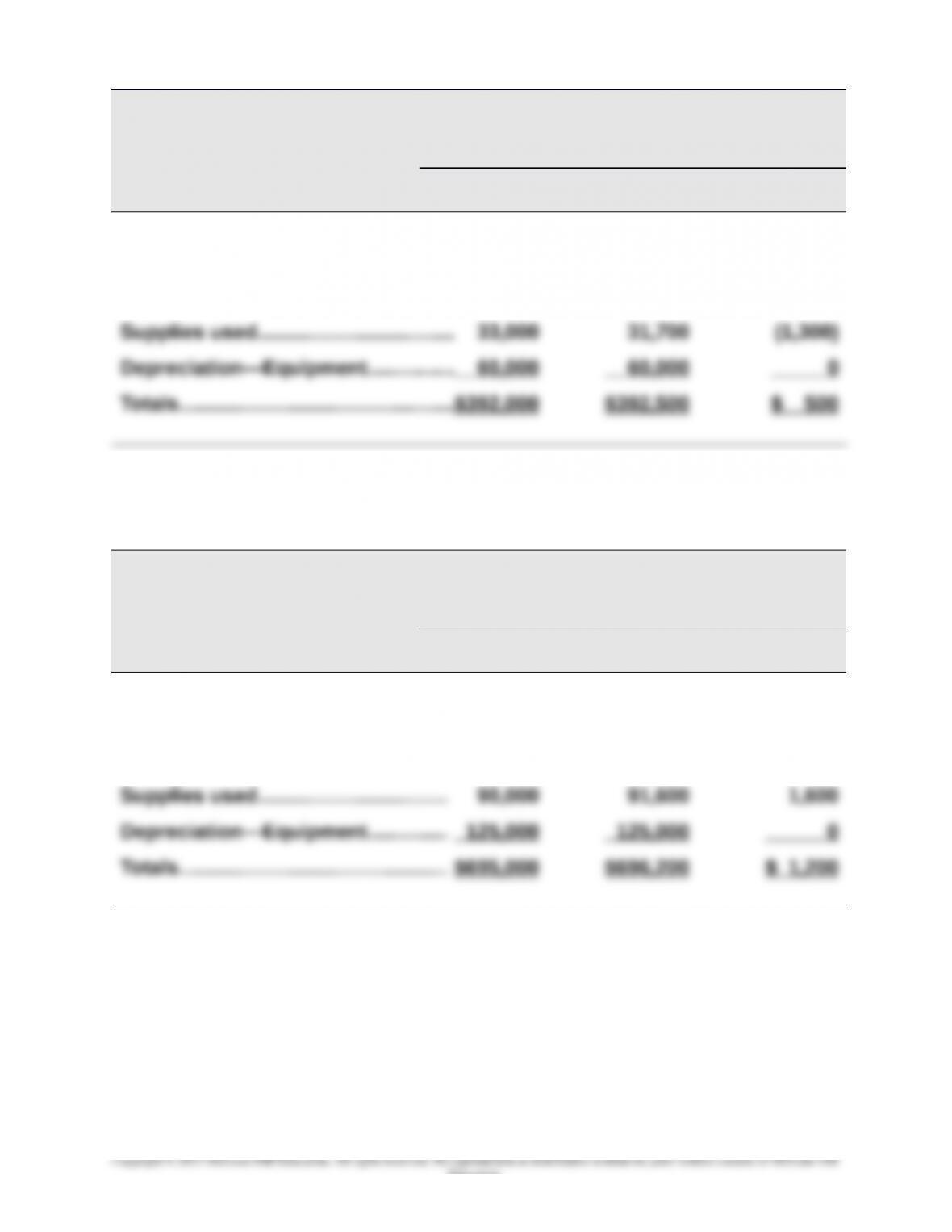

Responsibility Accounting Performance Report

Dept. Manager, Camper Department

For the Year

Budgeted Actual Over (Under)

Amount Amount Budget

Controllable Costs

Raw materials……………………………..$195,000 $194,200 $ (800)

Employee wages………………………… 104,000 106,600 2,600

b.

Responsibility Accounting Performance Report

Dept. Manager, Trailer Department

For the Year

Budgeted Actual Over (Under)

Amount Amount Budget

Controllable Costs

Raw materials………………………..….. $275,000 $273,200 $(1,800)

Employee wages……………..………… 205,000 206,400 1,400

24-1426

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Problem 24-1A (Continued)

c.

Responsibility Accounting Performance Report

Plant Manager, Indiana Plant

For the Year

Budgeted Actual Over (Under)

Amount Amount Budget

Controllable Costs

Dept. manager salaries….…..........$ 95,000 $ 97,500 $ 2,500

Utilities…………………………………….. 9,000 8,300 (700)

Building rent….………………………... 15,000 14,000 (1,000)

Other office salaries…..…………….. 32,500 30,100 (2,400)

Other office costs…………………….. 25,000 23,000 (2,000)

Part 2

The plant manager did a better job of controlling costs and meeting the

budget. She came in under budget for the plant even though she paid the

department managers more than budgeted and had to absorb the amounts

over budget in their departments. This is because she spent less than the

budget amount on utilities, building rent, other office salaries, and other

office costs. Each of the department managers came in over budget.

Problem 24-2A (60 minutes)

Part 1

24-1427

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Department Square Footage Rate Total

Linder’s Dept…............. 1,000 $8.25 $ 8,250

Part 2

Market rates are used to allocate occupancy costs for depreciation,

interest, and taxes. Heating, lighting, and maintenance costs are allocated

to the departments on both floors at the average rate per square foot.

These costs are separately assigned to each class as follows:

Total

Costs

Value-Based

Costs

Usage-Based

Costs

Depreciation—Building………………..$18,000 $18,000

Interest—Building mortgage..…...... 27,000 27,000

Taxes—Building and land………….... 9,000 9,000

24-1428

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Problem 24-2A (Continued)

Value-based costs are allocated to departments in two steps

(i) Compute market value of each floor

Floor

Square

Footage

Value per

Sq. Ft. Total

First floor………………………..….4,000 $30 $120,000

(ii) Allocate $54,000 to each floor based on its percent of market value

Floor

Market

Value

% of

Total

Allocated

Cost

Cost per

Sq. Ft.

First floor………………………..….$120,000 60% $32,400 $8.10

Usage-based costs allocation rate = $12,000 / 8,000 sq. ft.

= $1.50 per sq. ft.

We can then compute total allocation rates for the floors

Floor Value Usage Total

First floor…………………………… $8.10 $1.50 $9.60

Second floor….……………........ 5.40 1.50 $6.90

These rates are applied to allocate occupancy costs to departments

Department

Square

Footage Rate Total

Linder’s Department….……………….. 1,000 $9.60 $ 9,600

Chiro’s Department…………………….. 1,800 6.90 $12,420

Part 3

A second-floor manager would prefer allocation based on market value. This is a

reasonable and logical approach to allocation of occupancy costs. The current

method implies all square footage has equal value. This is not logical for this

type of occupancy. It also means the second-floor space would be allocated a

larger portion of costs under the current method, but less using an allocation

based on market value.

Problem 24-3A (70 minutes)

24-1429

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Williams Company

Forecasted Departmental Income Statements

For Year Ended December 31, 2016

Clock Mirror Paintings Combined

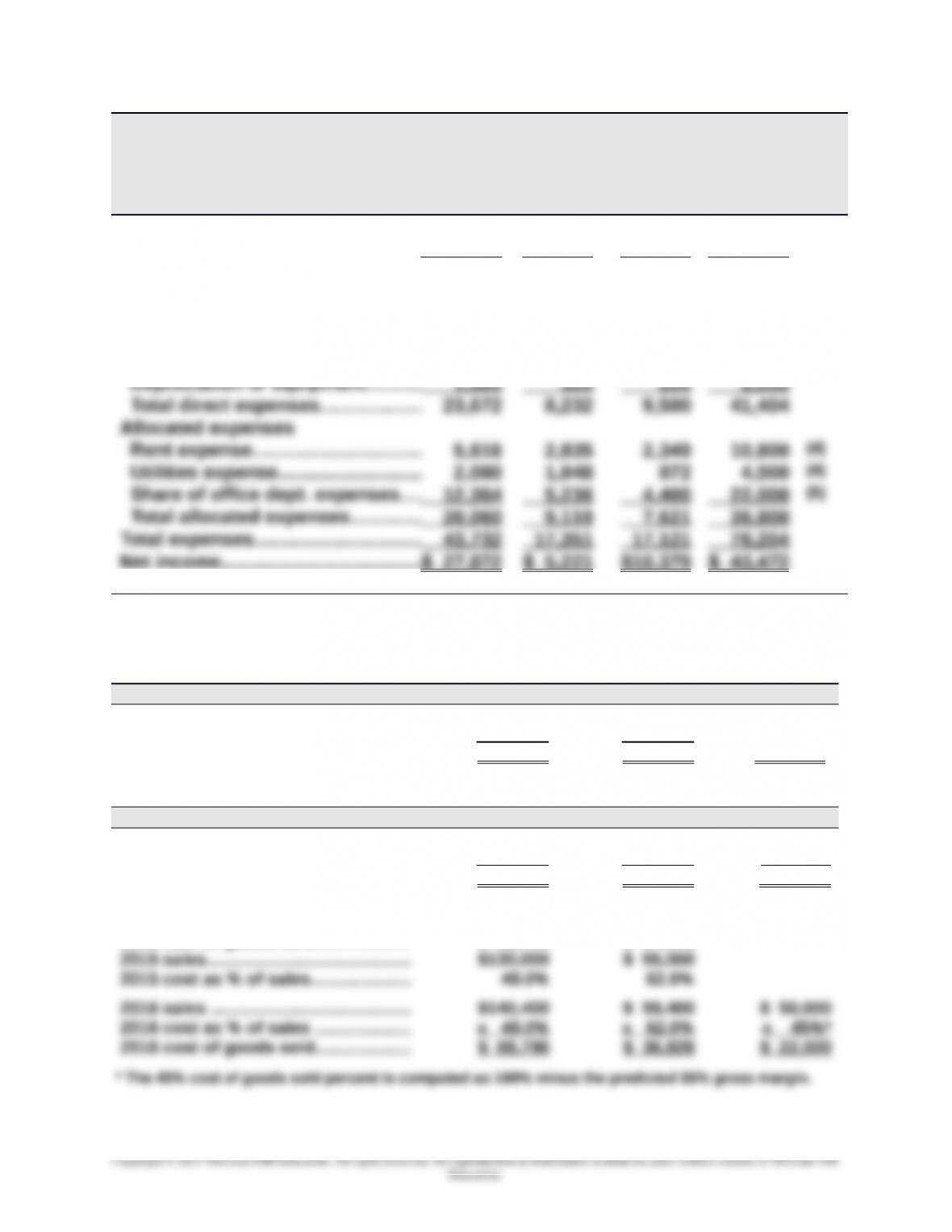

Sales…..………………………………..…...$140,400 $59,400 $50,000 $249,800 (1)

Cost of goods sold……..….….......... 68,796 36,828 22,500 128,124 (2)

Gross profit………..………………..….... 71,604 22,572 27,500 121,676

Direct expenses

Sales salaries………………………….. 20,000 7,000 8,000 35,000

Advertising………..………………..…… 1,200 500 800 2,500

Store supplies used…………………. 972 432 500 1,904 (3)

Supporting Computations—coded (1) through (5) in statement above

Note 1 (Sales)

Clock Mirror Paintings

2015 sales…………………..................... $130,000 $ 55,000

Growth rate (8% increase)................ x 108% x 108%

2016 sales…………………..................... $140,400 $ 59,400 $ 50,000

Note 2 (Cost of Goods Sold)

Clock Mirror Paintings

2015 cost of goods sold................... $ 63,700 $ 34,100 $ 50,000

Growth rate (8% increase)................ x 108% x 108% x 45%*

2016 cost of goods sold................... $ 68,796 $ 36,828 $ 22,500

ALTERNATIVELY

2015 cost of goods sold................... $ 63,700 $ 34,100

24-1430

Chapter 24 – Performance Measurement and Responsibility Accounting

Problem 24-3A (Continued)

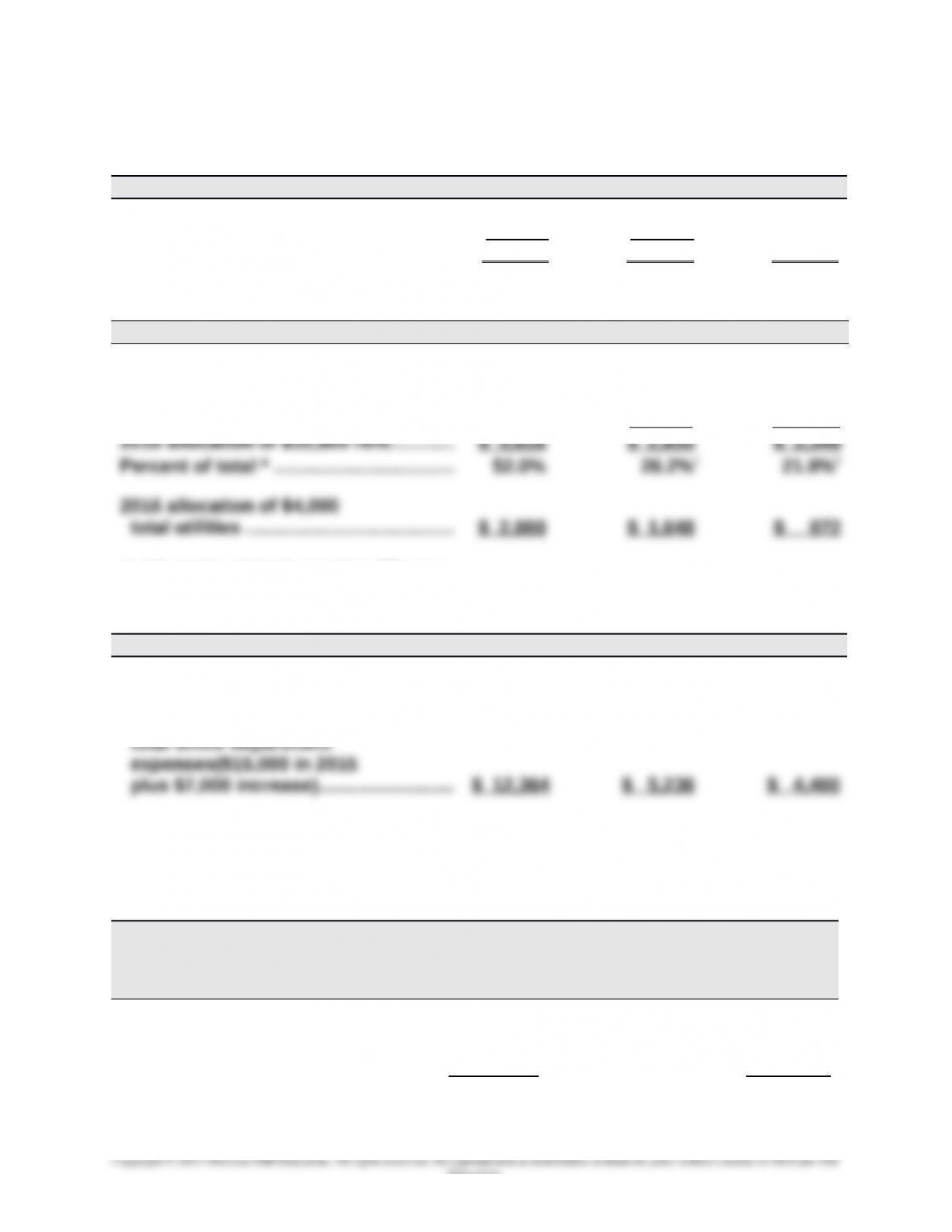

Note 3 (Store Supplies Used)

Clock Mirror Paintings

2015 store supplies used …….............. $ 900 $ 400

Growth rate (8% increase)…………….…. x 108% x 108%

2016 store supplies ……….……..….…..… $ 972 $ 432 $ 500

Note 4 (Rent and Utilities)

Clock Mirror Paintings

2015 rent …….………………………………….. $ 7,020 $ 3,780

One-fifth from clock to paintings……… (1,404) $ 1,404

One-fourth from mirror to

paintings……..…………………………………. ______ (945) 945

†Adjusted to eliminate rounding difference.

Note 5 (Office Department Expenses)

Clock Mirror Paintings

2015 sales …………..…..….…..….…..….…. $140,400 $ 59,400 $ 50,000

Percent of total sales *………..…………… 56.2% 23.8% 20.0%

2016 allocation of $22,000

* Instructor note: If students round to something other than one-tenth of a percent, their

numbers will slightly vary.

Problem 22-4A (45 minutes)

Part 1

VORTEX COMPANY

Departmental Contribution Statements

Dept. A Dept. B

Sales…………………..…………….. $800,000 $450,000

Cost of goods sold……..……… 497,000 291,000

Gross profit……………….………. 303,000 159,000

24-1431

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Direct expenses

Total direct expenses.………… 197,000 129,000

Departmental contributions to

overhead………………………....

Allocated indirect expenses

106,000 30,000

Salaries*……….…………………… 23,040 12,960

*Salaries allocation: Sales % Amount Allocated

Department A $ 800,000 64% $36,000 $23,040

Department B 450,000 36% 36,000 12,960

Total $1,250,000 100% $36,000

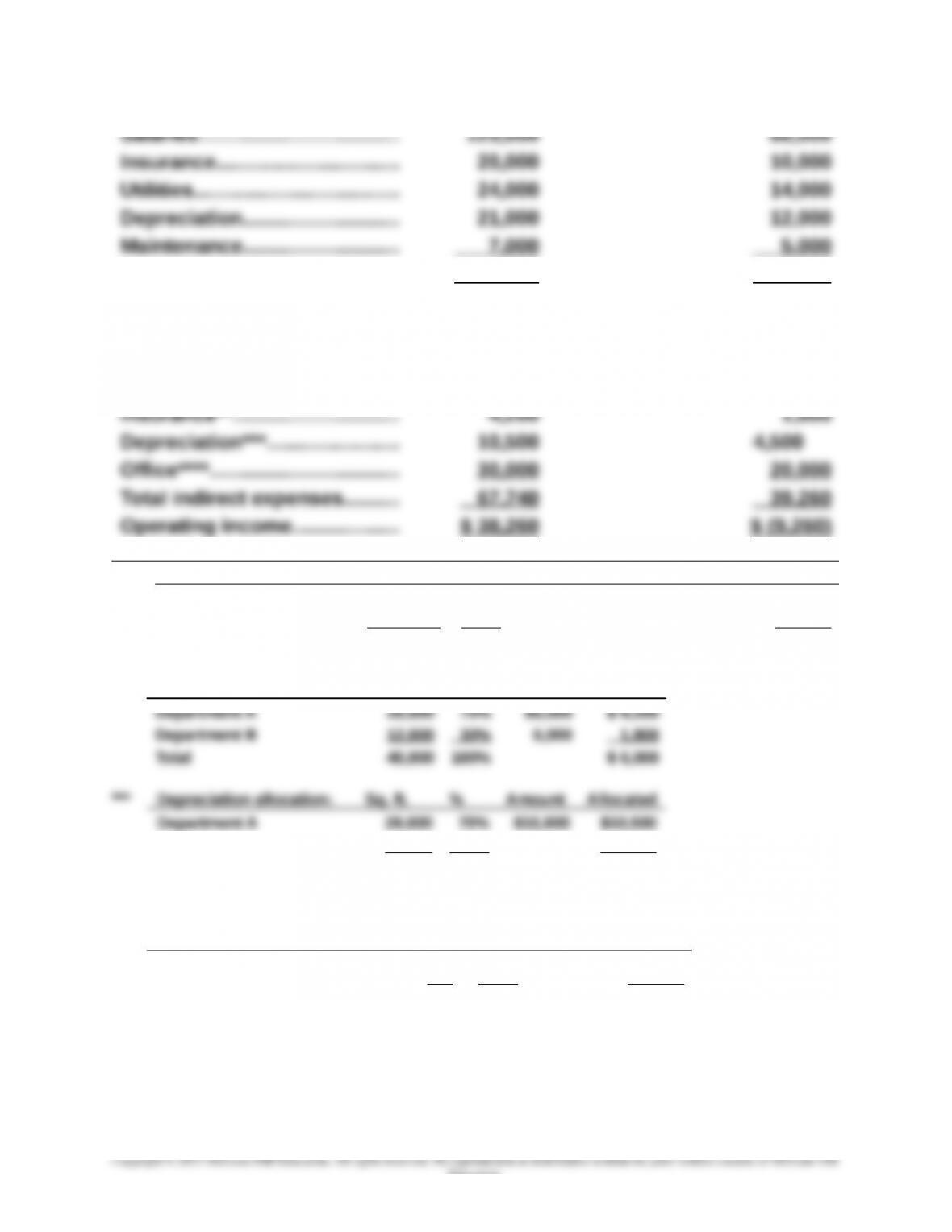

** Insurance allocation: Sq. ft. % Amount Allocated

Department B 12,000 30% 15,000 4,500

Total 40,000 100% $15,000

Problem 22-4A (Concluded)

**** Office expense allocation: Employees % Amount Allocated

Department A 75 60% $50,000 $30,000

Department B 50 40% 50,000 20,000

Total 125 100% $50,000

Part 2

Although Department B has a negative departmental income, it is

24-1432

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

contributing $30,000 to overhead. If none of the indirect expenses can be

reduced by eliminating Department B, then eliminating it would not be a

good idea. Overall company income will be reduced by $30,000. It is

24-1433