Chapter 24 – Performance Measurement and Responsibility Accounting

Exercise 24-8 (15 minutes)

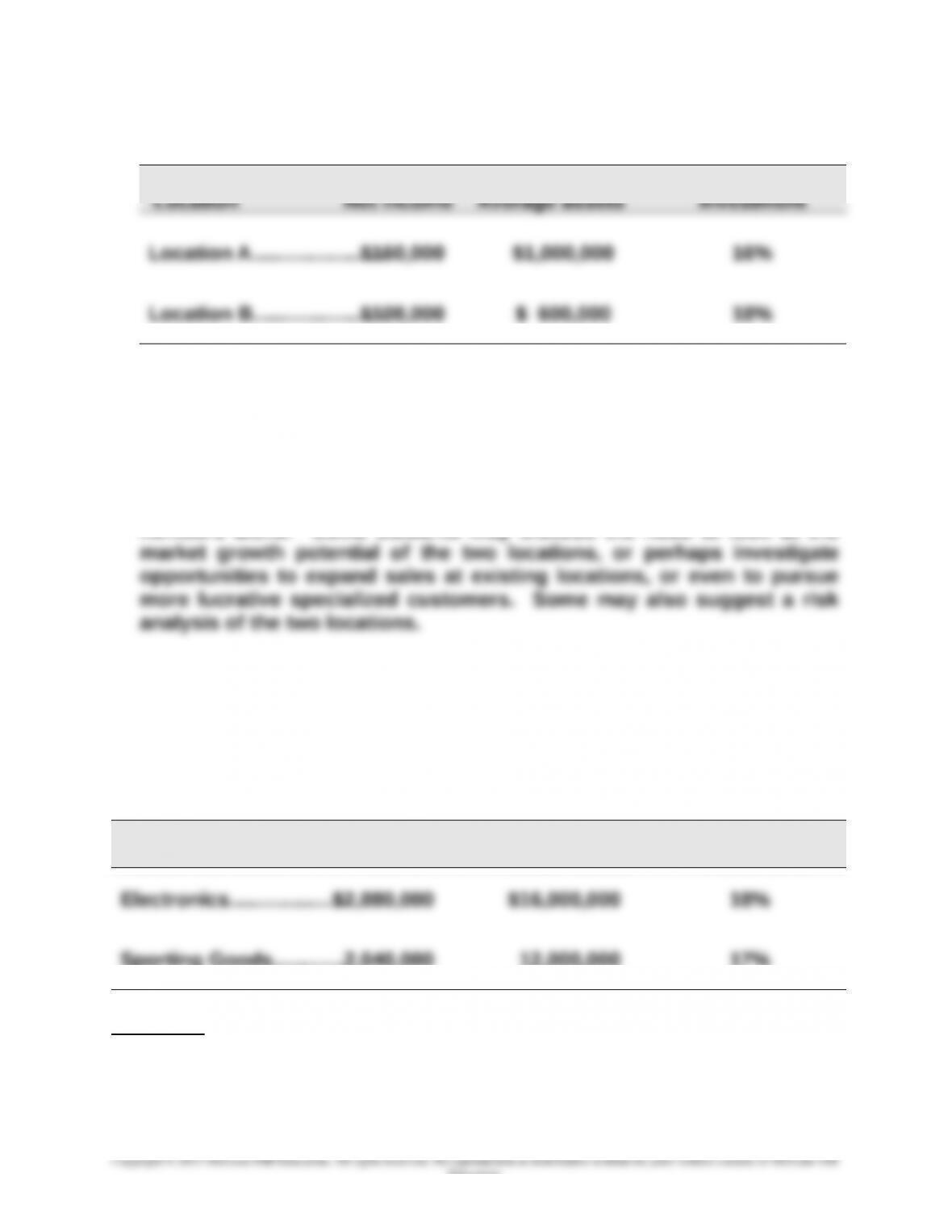

1.

Return on

2. The recommendation is to pursue Location B because its return on

investment (assets) is 18%, compared to 16% at Location A. Moreover,

given the normal return of 18% for this chain, only Location B meets this

hurdle.

This exercise should caution students to think beyond financial

numbers alone. Some students may discuss the need to look at the

Exercise 24-9 (20 minutes)

(1)

Investment center Income Average assets

Return on

investment

Sporting Goods............2,040,000 12,000,000 17%

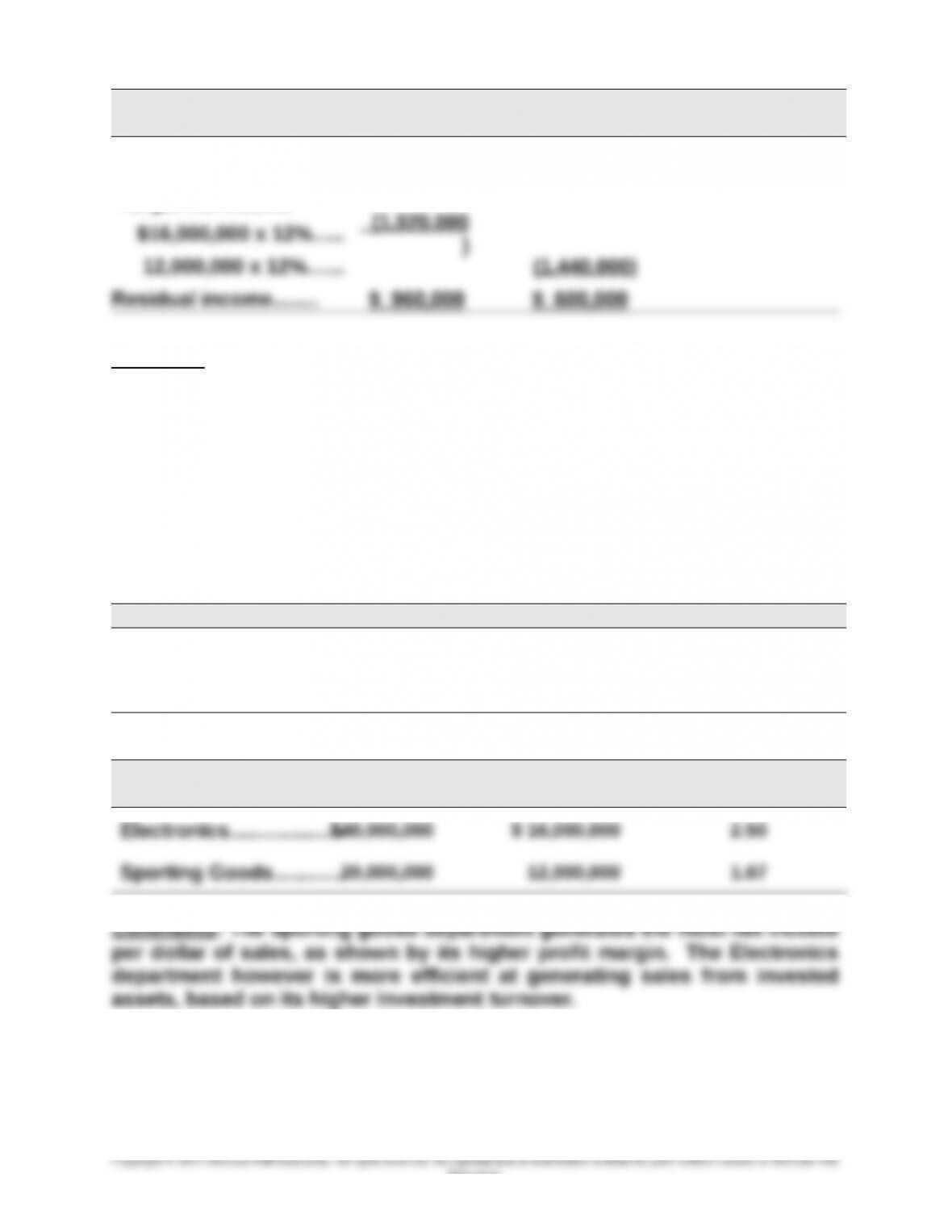

Comment: The electronics division is the superior investment center on the

basis of the investment center return on investment (assets).

Exercise 24-9 (continued)

(2)

24-1425

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Investment Center Electronics

Sporting

Goods

Net income……………….. $2,880,000 $2,040,000

Target net income

(1,920,000

Comment: The electronics department is the superior investment center on

the basis of investment center residual income.

(3) The electronics department should accept the new opportunity, since it

will generate residual income of 3% (15% – 12%) of the investment’s

invested assets.

Exercise 24-10 (15 minutes)

Investment Center Income Sales Profit margin

Electronics………………..$2,880,000 $40,000,000 7.20%

Sporting Goods............2,040,000 20,000,000 10.20%

Investment Center Sales Average assets

Investment

turnover

24-1426

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

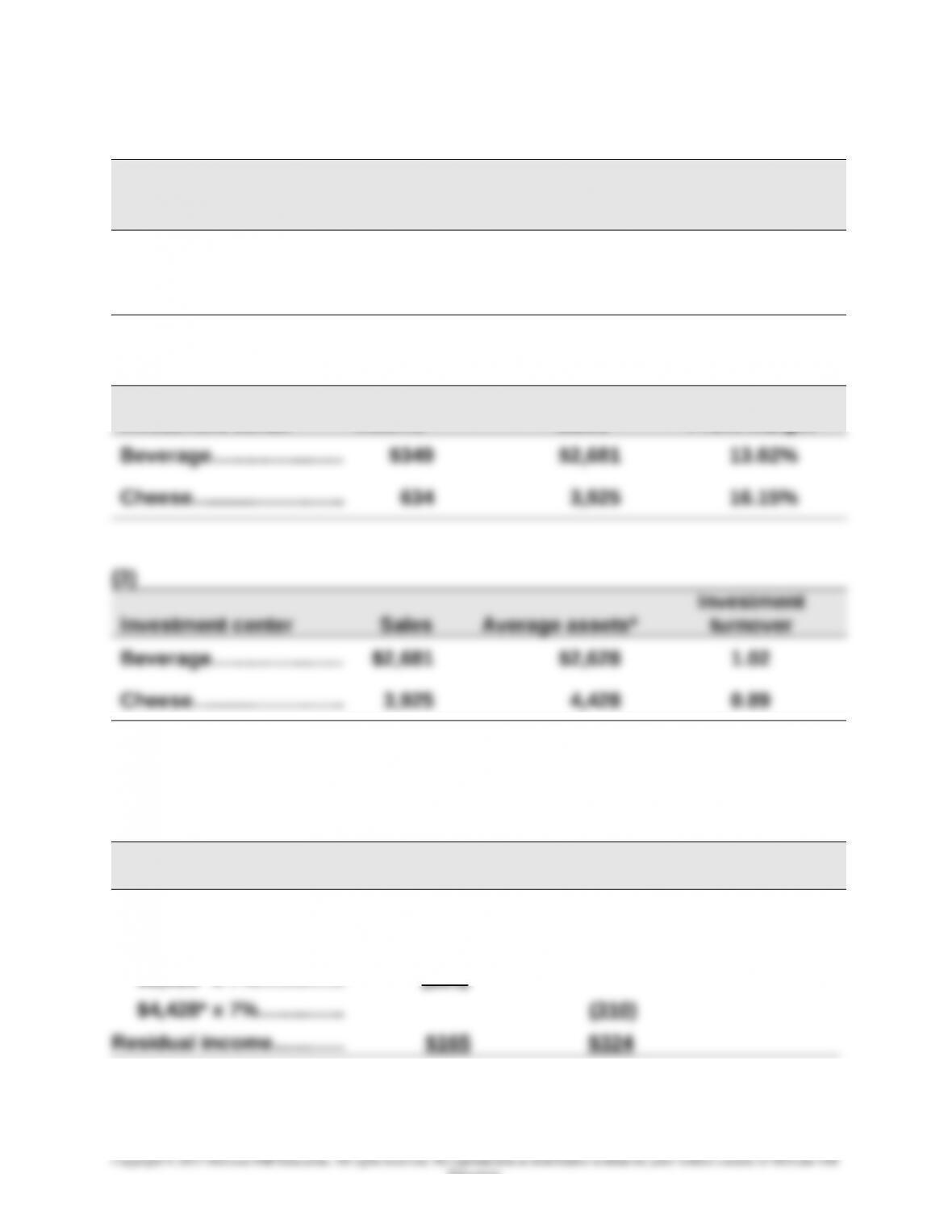

Exercise 24-11 (20 minutes)

(1)

Investment center

Operating

income Average assets*

Return on

investment

Beverage….…………....... $349 $2,628 13.28%

Cheese……………………... 634 4,428 14.32%

(2)

Investment center

Operating

income Sales Profit margin

*Beginning plus ending invested assets, divided by 2. Rounded to the nearest dollar.

Exercise 24-12 (10 minutes)

($ millions) Beverage Cheese

Operating income……... $349 $634

Target net income

$2,628* x 7%……………

(184)

*Average invested assets. Computed as beginning plus ending invested assets, divided by two,

and rounded to nearest dollar.

Exercise 24-13 (15 minutes)

24-1427

Education.

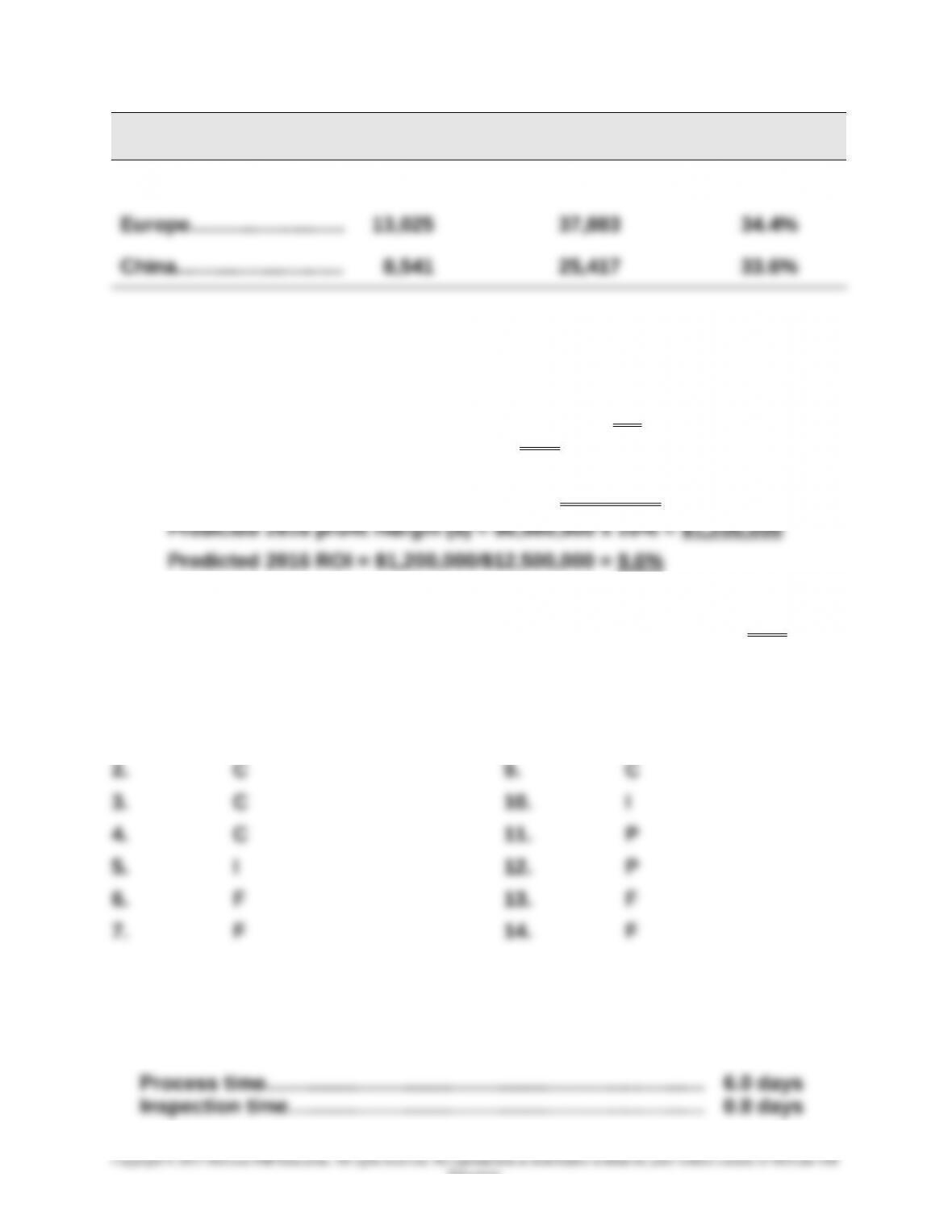

Chapter 24 – Performance Measurement and Responsibility Accounting

Investment center

Operating

income Sales Profit margin

Americas….…………....... $22,817 $62,739 36.4%

Exercise 24-14 (20 minutes)

1. Return on investment = $1,000,000/$12,500,000 = 8%

2. Profit margin = $1,000,000/$5,000,000 = 20%

3. Predicted 2016 sales = $5,000,000 x 120% = $6,000,000

4. Predicted 2016 investment turnover = $6,000,000/$12,500,000 = 0.48

Exercise 24-15 (20 minutes)

1. F 8. P

Exercise 24-16 (15 minutes)

Part 1

24-1428

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Move time……………………………………………………………….…….... 3.2 days

Wait time…………………………………………………………………………. 5.0 days

Manufacturing cycle time…………………………….………………….. 15.0 days

Part 2

Manufacturing cycle efficiency (6.0 days/ 15.0 days)…......... 0.40

This means that Oakwood is spending 40% of its time in value-added

activities, and 60% of its time on non-value-added activities.

Part 3

If move time is reduced by 1.2 days and wait time is reduced by 2.8 days,

manufacturing cycle time will be reduced to 11.0 days. Manufacturing

cycle efficiency will be 0.545, computed as 6.0 days divided by 11.0 days.

Exercise 24-17 (15 minutes)

Part 1

Process time…………………………………………………….……………..16.0 hours

Inspection time……………………………………………………………….. 3.5 hours

Exercise 24-17 (continued)

Part 2

Manufacturing cycle efficiency (16.0 hours/ 50.0 hours)...... 0.32

activities, and 68% of its time on non-value-added activities.

Part 3

To increase the manufacturing cycle efficiency to 0.80 Best Ink needs to

reduce the total manufacturing cycle time to 20 hours without changing the

process time (16 hours/ 0.80 = 20 hours). To do this, they must reduce the

24-1429

Exercise 24-18A (15 minutes)

1. If the trailer division is currently operating at full capacity, its manager

2. If the trailer division is currently producing 20,000 trailers and the

assembly division will order 15,000 more trailers, the Trailer division will

have excess capacity. In this case the range of acceptable transfer prices

Exercise 24-18A (continued)

3. The trailer division would prefer a transfer price of $140 per trailer, since

it provides a $60 ($140 – $80) contribution margin per trailer. At a transfer

price of $80 the trailer division reports a contribution margin of $0 per

trailer. Conversely, the assembly division manager prefers a transfer price

of $80, since it provides a contribution margin of $120 ($200 – $80) per

Exercise 24-19B (20 minutes)

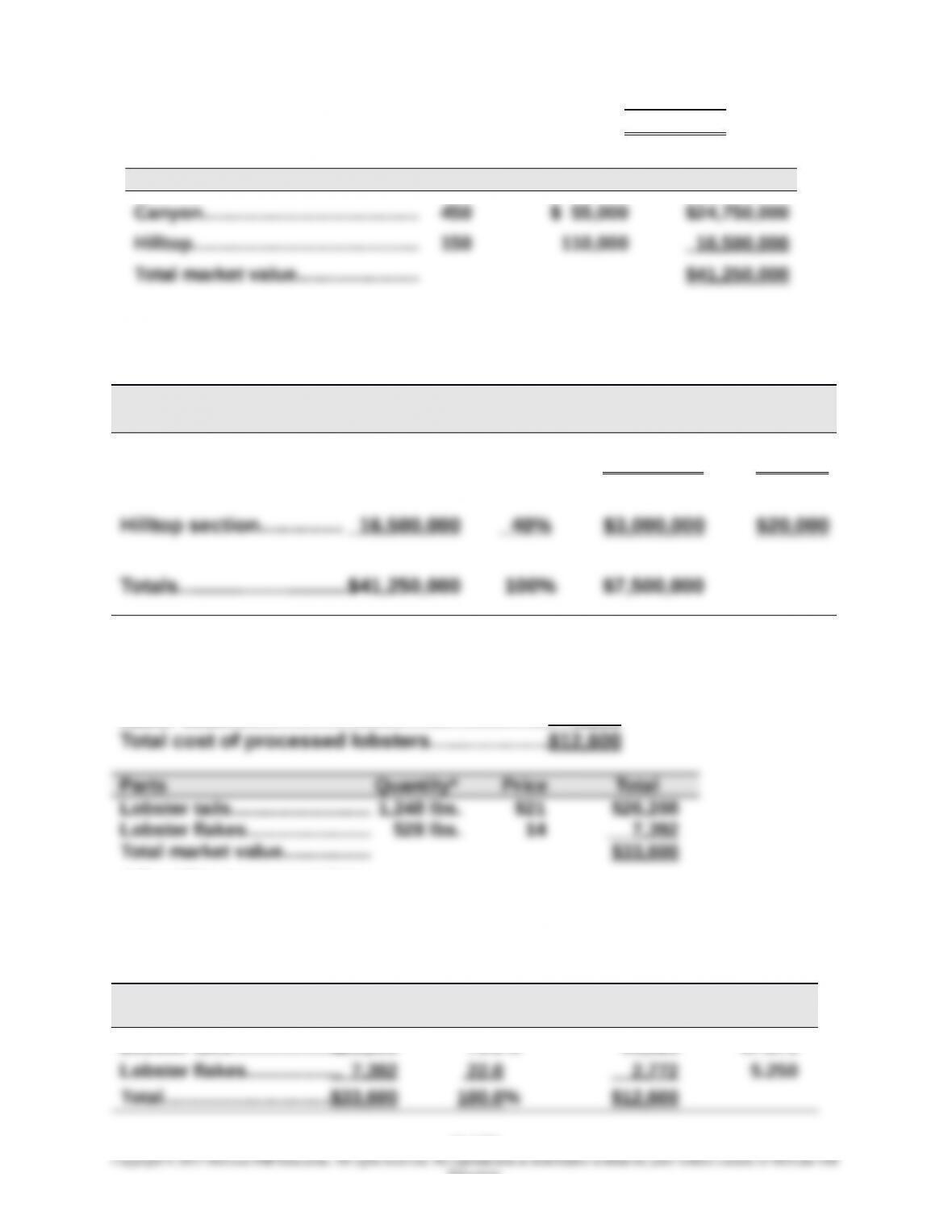

Preliminary calculations

Land cost ………………………………….…………..……………..$4,000,000

24-1430

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

Improvements ……………………………………………….……… 3,500,000

Total cost of lots ………………………………………….………..$7,500,000

Lots Quantity Price Total

Allocated cost—value basis of allocation: $7,500,000

Market % of Allocated Average

Value Total Cost Lot Cost

Canyon section............ $24,750,000 60% $4,500,000 $10,000

Exercise 24-20B (25 minutes)

Preliminary calculations

Lobster cost (2,400 lbs. x $4.50)..………...........$10,800

Labor cost…………………………..…………………….. 1,800

* Quantities are computed as:

52% x 2,400 lbs. = 1,248 lbs.

22% x 2,400 lbs. = 528 lbs.

Allocated cost—value basis allocation: $12,600

Market % of Allocated Cost

Parts Value Total Cost per lb.

Lobster tails………..….......$26,208 78.0% $9,828 $7.875

24-1431

Education.

Chapter 24 – Performance Measurement and Responsibility Accounting

(1) Cost of goods sold

Parts Quantity (given) Cost Total

Lobster tails………………..…….. 1,096 lbs. $7.875 $ 8,631

(2) Cost of ending inventory

Parts Quantity Cost Total

Lobster tails………………..…….. 152 lbs.* $7.875 $ 1,197

Lobster flakes……………………. 204 lbs.** 5.250 1,071

Note: Cost of goods sold ($10,332) plus cost of ending inventory

($2,268) equals the total cost of $12,600.

24-1432