Problem 23-3A (Continued)

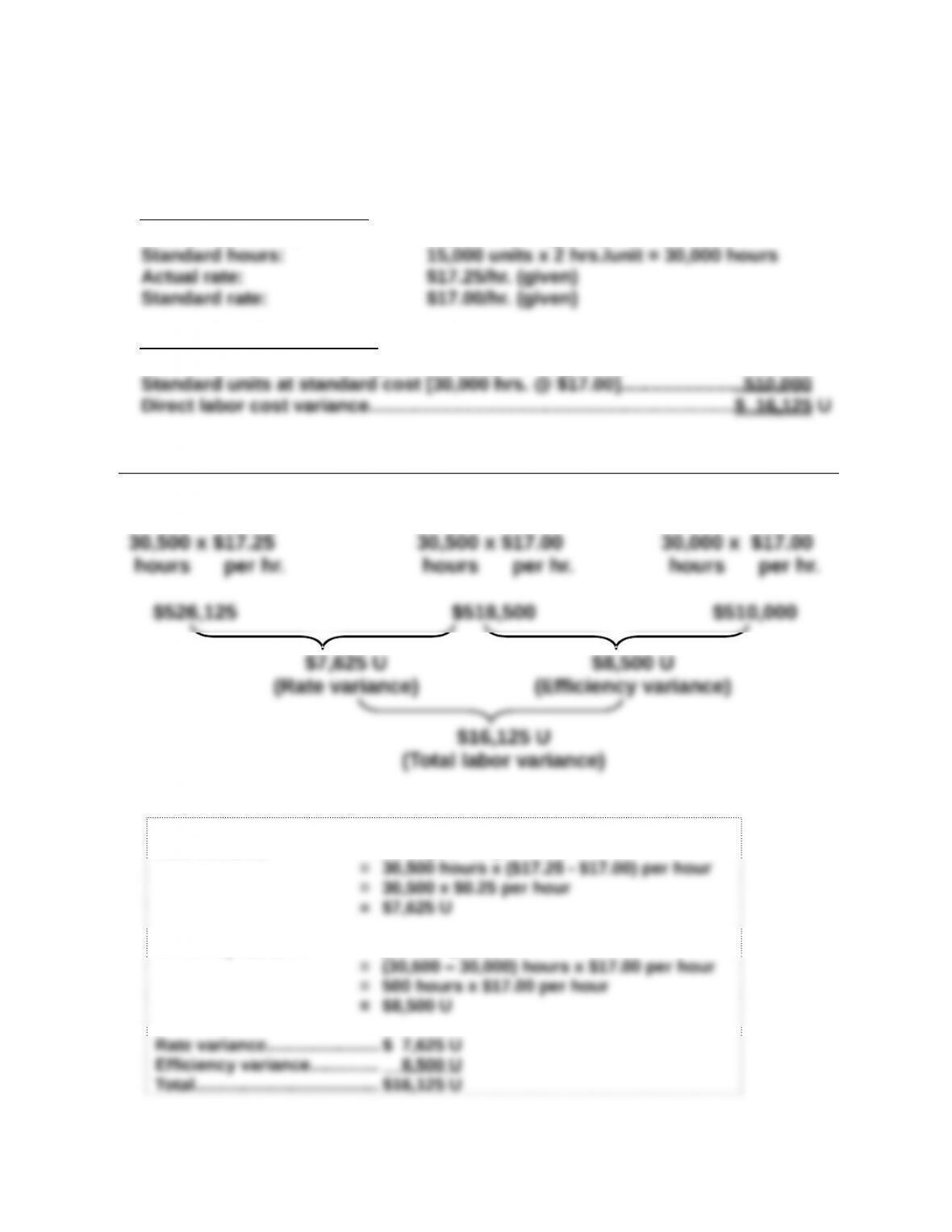

Part 4 Direct labor variances

Preliminary computations

Actual hours used: 30,500 hours (given)

Direct labor cost variances

Actual units at actual cost [30,500 hrs. @ $17.25]………………………………………$526,125

Direct Labor Rate and Efficiency Variances

Actual Costs

AH x AR AH x SR

Standard Costs

SH x SR

Alternate solution format

Rate variance = AH x (AR – SR)

Efficiency variance = (AH – SH) x SR

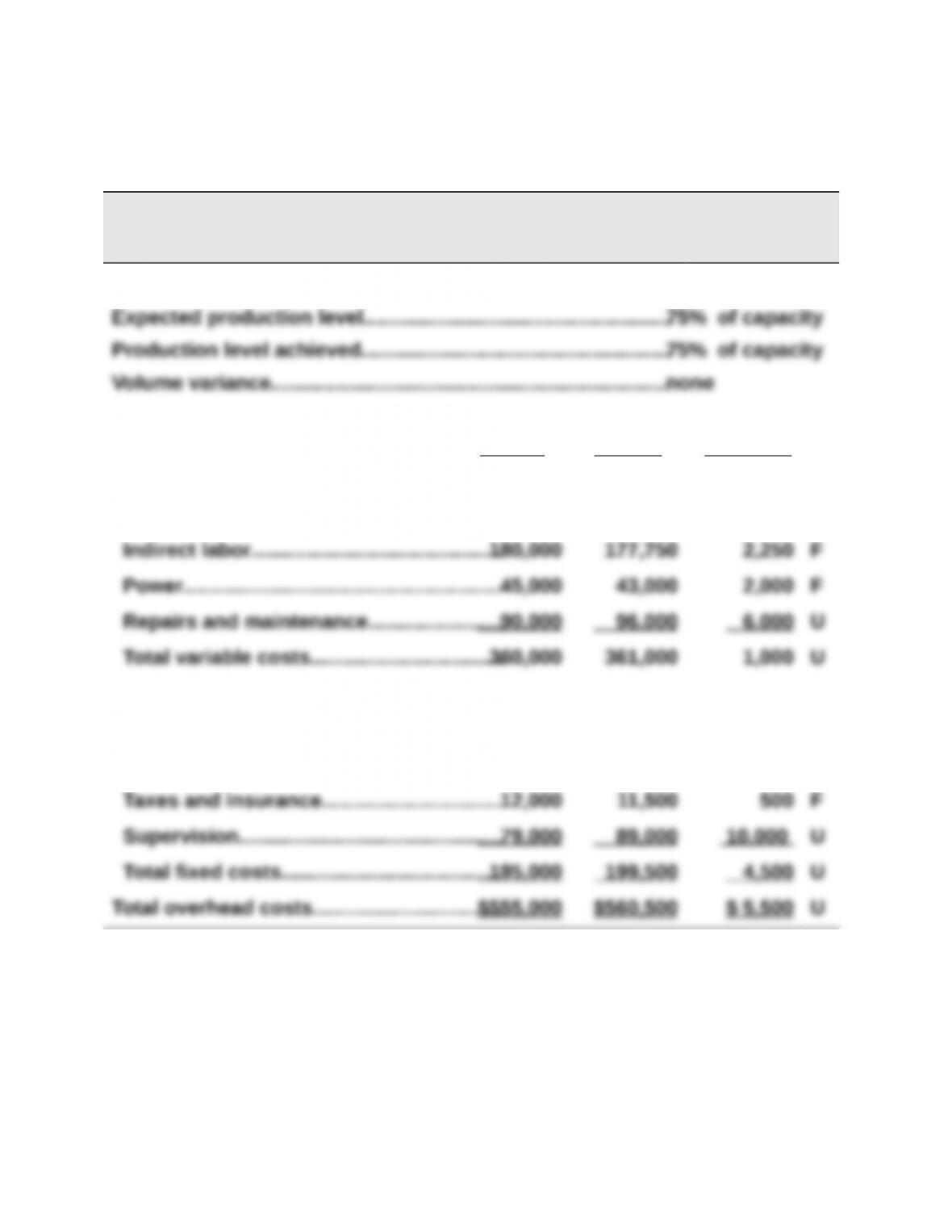

Problem 23-3A (Concluded)

Part 5

ANTUAN COMPANY

Overhead Variance Report

For Month Ended October 31

Volume Variance

Flexible Actual

Controllable Variance Budget Results Variances*

Variable overhead costs

Indirect materials……………………………….$ 45,000 $ 44,250 $ 750 F

Fixed overhead costs

Depreciation—Building………………………24,000 24,000 0

Depreciation—Machinery…………………..80,000 75,000 5,000 F

*F = Favorable variance; and U = Unfavorable variance.

Problem 23-4A (40 minutes)

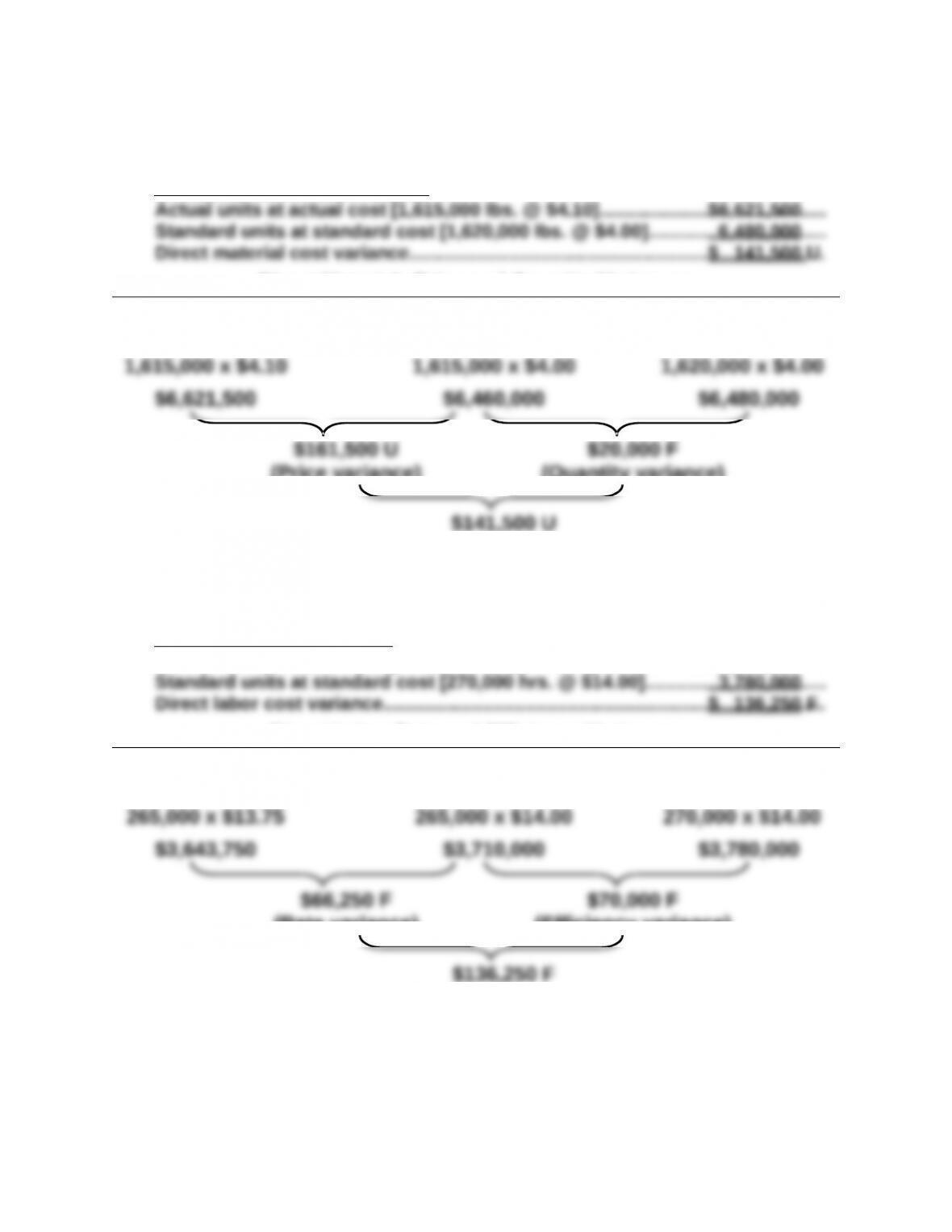

Part 1 Direct Materials Variances

Direct materials cost variances

Direct Materials Price and Quantity Variances

Actual Cost

AQ x AP AQ x SP

Standard Cost

SQ x SP

(Price variance)

(Quantity variance)

(Total materials variance)

Part 2 Direct Labor Variances

Direct labor cost variances

Actual units at actual cost [265,000 hrs. @ $13.75]…………………………………….$3,643,750

Direct Labor Rate and Efficiency Variances

Actual Cost

AH x AR AH x SR

Standard Cost

SH x SR

(Rate variance)

(Efficiency variance)

(Total labor variance)

Problem 23-4A (Continued)

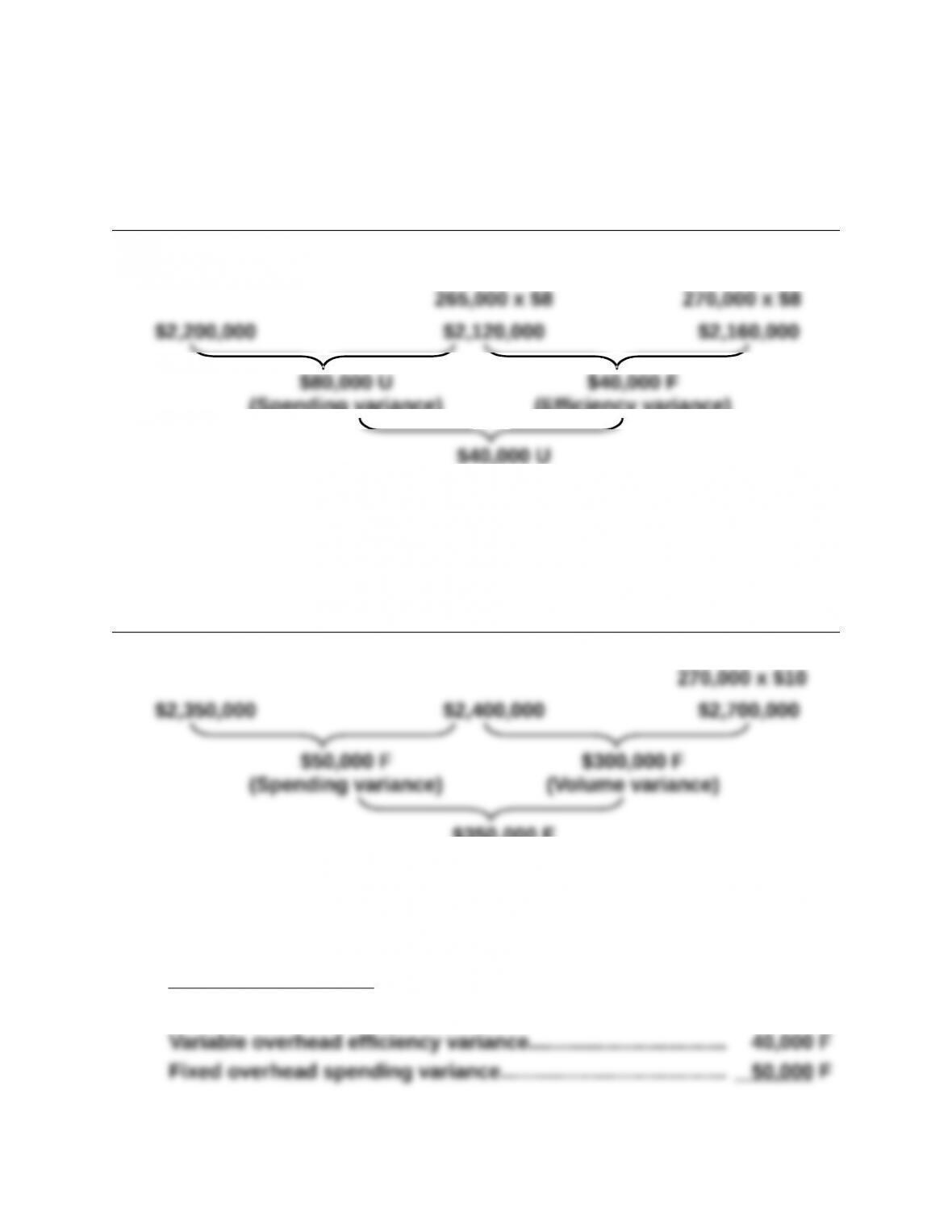

Part 3 Overhead Variances

Controllable variance

Actual overhead [$2,350,000 + $2,200,000]………………………….$4,550,000

Fixed overhead volume variance

Budgeted fixed overhead [given, at 80% capacity]………………$2,400,000

Problem 23-5AA (15 minutes)

(a) Variable overhead

Variable Overhead Spending and Efficiency Variances

Actual Overhead

AH x AVR AH x SVR

Applied Overhead

SH x SVR

(Spending variance)

(Efficiency variance)

(Total variable overhead variance)

(b) Fixed overhead

Fixed Overhead Spending and Volume Variances

Actual Overhead Budgeted Overhead Applied Overhead

(Total fixed overhead variance)

(c) Controllable variance

Variable overhead spending variance…………………………….. $ 80,000 U

Problem 23-6AA (45 minutes)

Part 1

Dec. 31* Work in Process Inventory……………………………………………..100,000

To record materials costs, including

the unfavorable quantity and

favorable price variances.

Dec. 31 Work in Process Inventory……………………………………………..95,800

To record direct labor costs, including

the favorable efficiency variance and

unfavorable rate variance.

Dec. 31 Work in Process Inventory……………………………………………..354,000

To record overhead costs, including

the unfavorable volume and unfavorable

controllable variances.

* Alternatively, some companies compute and record the price variance

when materials are purchased. This would yield two separate entries:

(1) Purchase of materials

Raw Materials Inventory……………………………………………………………………103,000

Problem 23-6AA (Continued)

Part 2

Under management by exception, the manager would first identify the

The largest variance amounts occur for the materials quantity variance, the

direct labor efficiency variance, and the two overhead variances. The

After the relatively larger amounts are explained and actions taken, the

PROBLEM SET B

Problem 23-1B (60 minutes)

Part 1

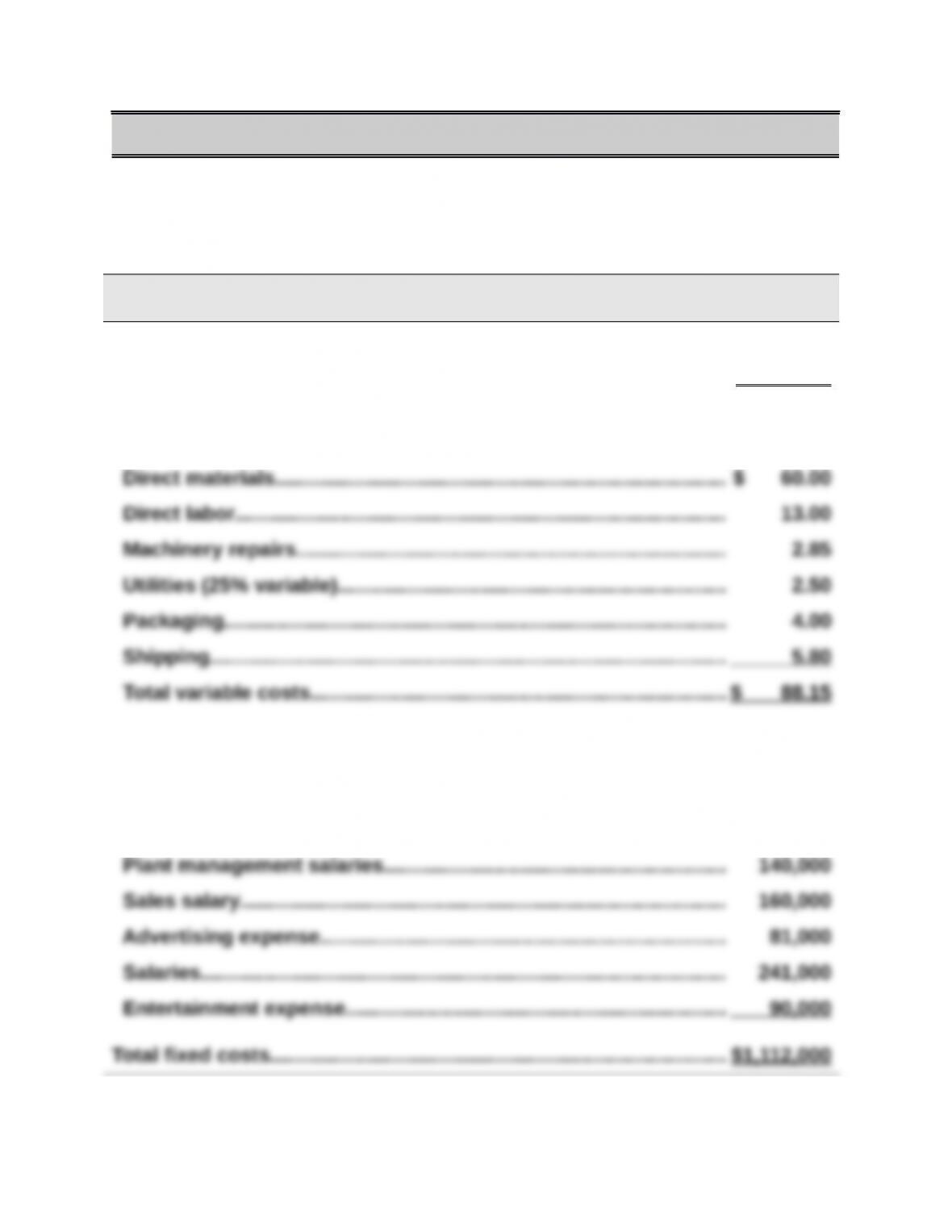

Variable or Fixed Classification

Per Unit

Amount

Variable sales (total divided by 20,000 units)

Sales………………………………………………………………………………….. $ 150.00

Variable costs (total divided by 20,000 units)

Fixed costs

Depreciation—Machinery…………………………………………………….. $ 250,000

Utilities (75% fixed)……………………………………………………………… 150,000

Problem 23-1B (Continued)

Part 2

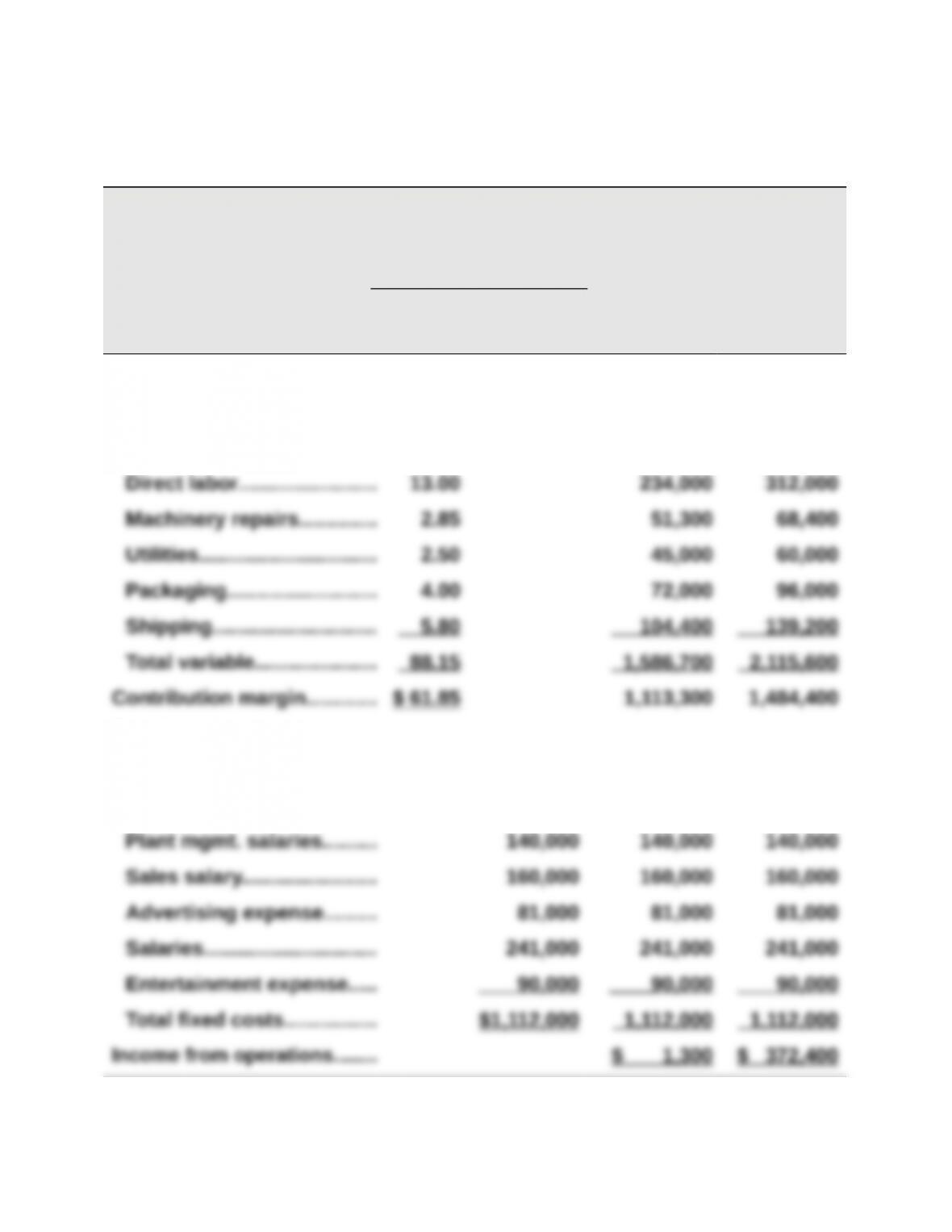

TOHONO COMPANY

Flexible Budgets

For Year Ended December 31, 2015

Flexible Budget Flexible Flexible

Variable

Amount

per Unit

Total

Fixed

Cost

Budget for

Unit Sales

of 18,000

Budget for

Unit Sales

of 24,000

Sales………………………………. $150.00 $2,700,000 $3,600,000

Variable costs

Direct materials…………….. 60.00 1,080,000 1,440,000

Fixed costs

Depreciation—Mach……….. $ 250,000 250,000 250,000

Utilities…………………………. 150,000 150,000 150,000

Problem 23-1B (Continued)

Part 3

Operating income increase for a 20,000 to 28,000 unit sales increase

Potential sales (units)…………………………………………………… 28,000 Units

Contribution margin per unit…………………………………………. x $61.85

*Alternate solution format

Since there is no increase in fixed costs, the expected increase in operating

Part 4

Operating income (loss) at 14,000 units

Potential sales (units)…………………………………………………… 14,000

Contribution margin per unit…………………………………………. x $61.85

Problem 23-2B (60 minutes)

Part 1

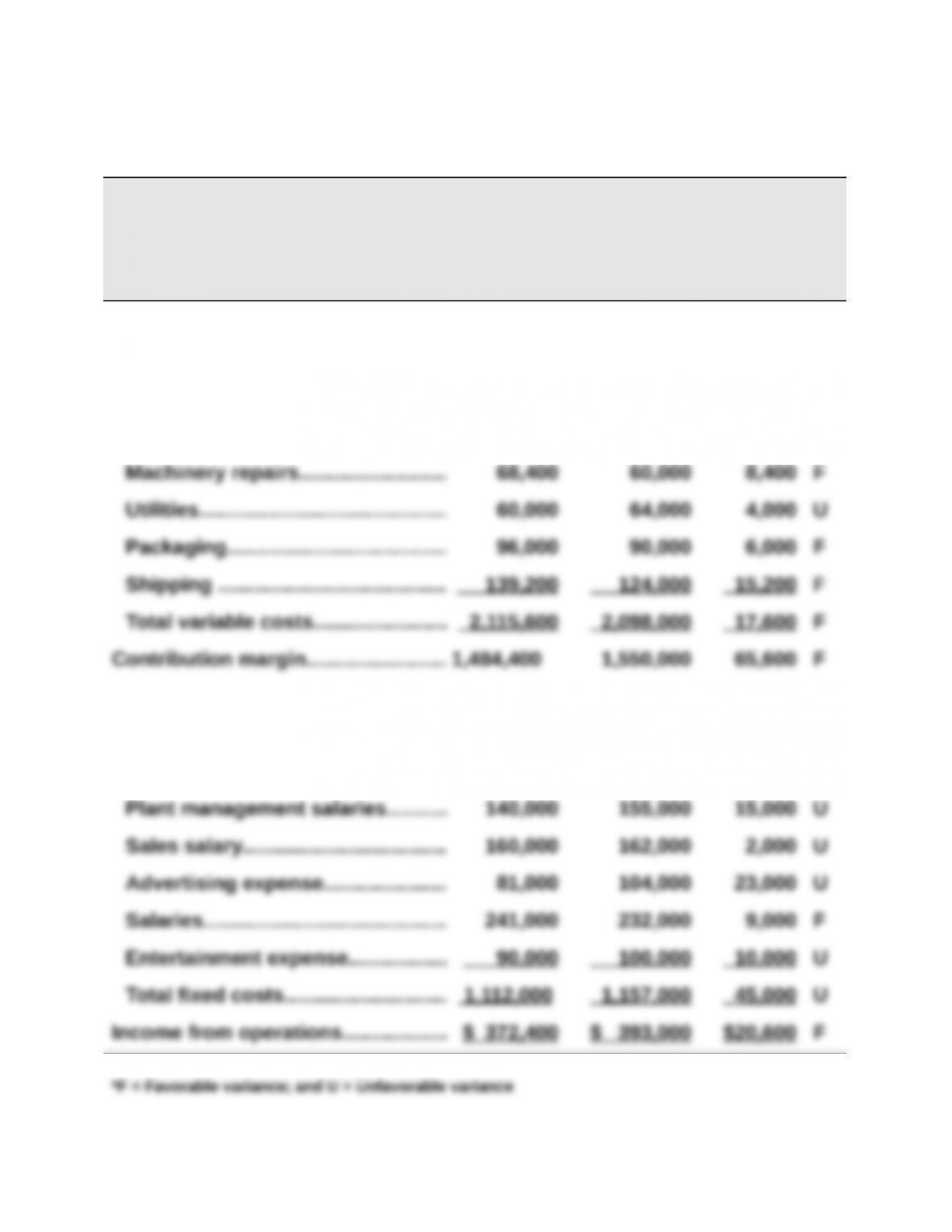

TOHONO COMPANY

Flexible Budget Performance Report

For Year Ended December 31, 2015

Flexible Actual

Budget Results Variances*

Sales (24,000 units)……………………. $3,600,000 $3,648,000 $48,000 F

Variable costs

Direct materials……………………….. 1,440,000 1,400,000 40,000 F

Direct labor……………………………… 312,000 360,000 48,000 U

Fixed costs

Depreciation—Machinery…………. 250,000 250,000 0

Utilities……………………………………. 150,000 154,000 4,000 U