Exercise 23-22 (25 minutes)

Preliminary calculations:

Variable overhead rate per DL hour = $32,000/32,000 = $1 per hour

Part 1

Total actual overhead (given) ………………………… $81,700

Flexible budget overhead

Part 2

Total budgeted fixed overhead (given) ………………

$48,000

Exercise 23-22 (continued)

Part 3

BLAZE CORP.

Overhead Variance Report

For Month Ended March 31

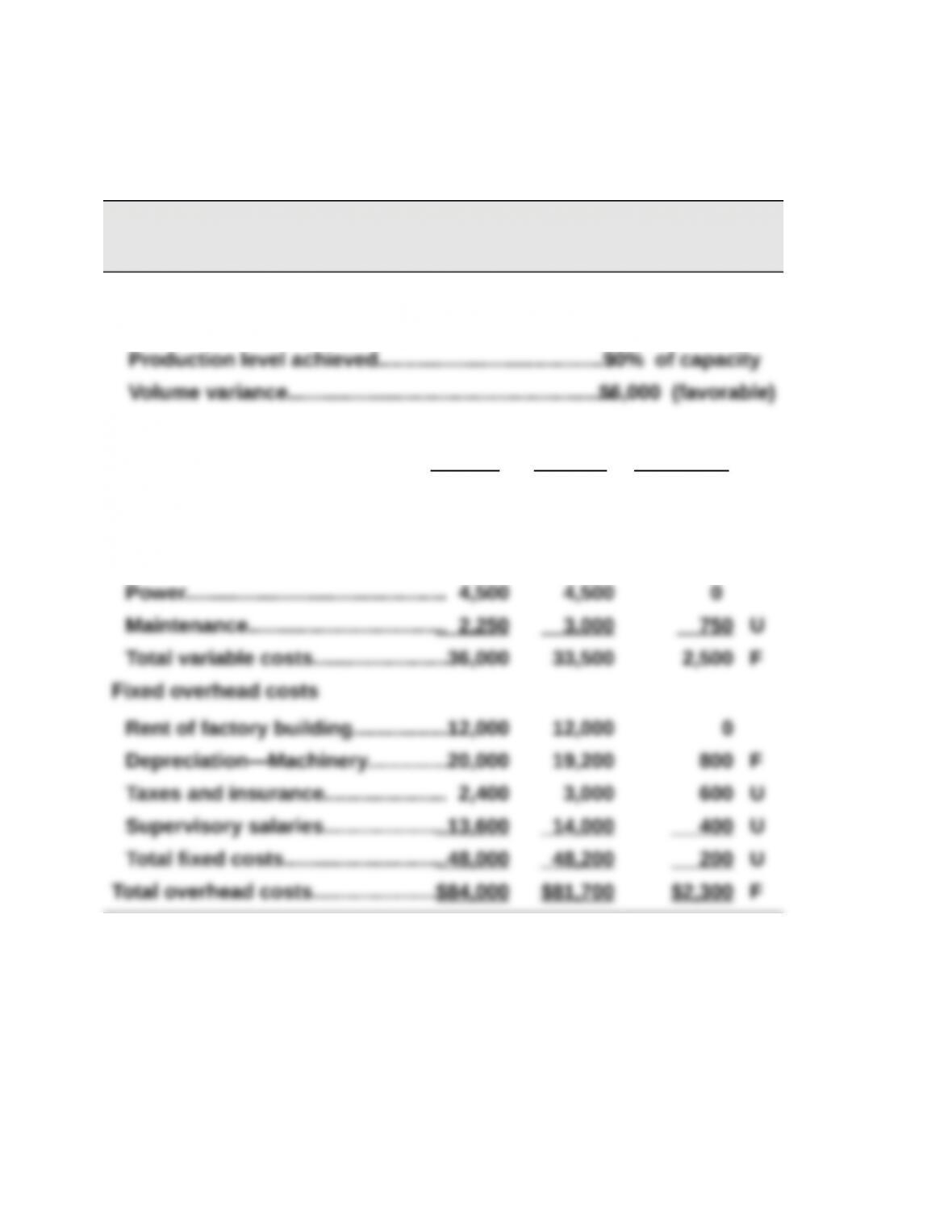

Volume Variance

Expected production level………………………………….80% of capacity

Flexible Actual

Controllable Variance Budget Results Variances*

Variable overhead costs

Indirect materials……………………..$11,250 $10,000 $1,250 F

Indirect labor……………………………18,000 16,000 2,000 F

* F = Favorable variance; and U = Unfavorable variance.

Exercise 23-23 (25 minutes)

1. Sales price and sales volume variances

Sales Actual Sales Flexible Budget Fixed Budget

Units 350 350 365

2. Interpretation

The $35,000 favorable sales price variance implies it sold computers for a

PROBLEM SET A

Problem 23-1A (60 minutes)

Part 1

Variable or Fixed Classification

Amount

per unit

Variable sales (total divided by 15,000 units)

Sales………………………………………………………………………………….. $ 200.00

Variable costs (total divided by 15,000 units)

Direct materials…………………………………………………………………… $ 65.00

Fixed costs

Depreciation—Plant equipment……………………………………………. $ 300,000

Utilities ($195,000 – $45,000 variable)…………………………………….. 150,000

Problem 23-1A (Continued)

Part 2

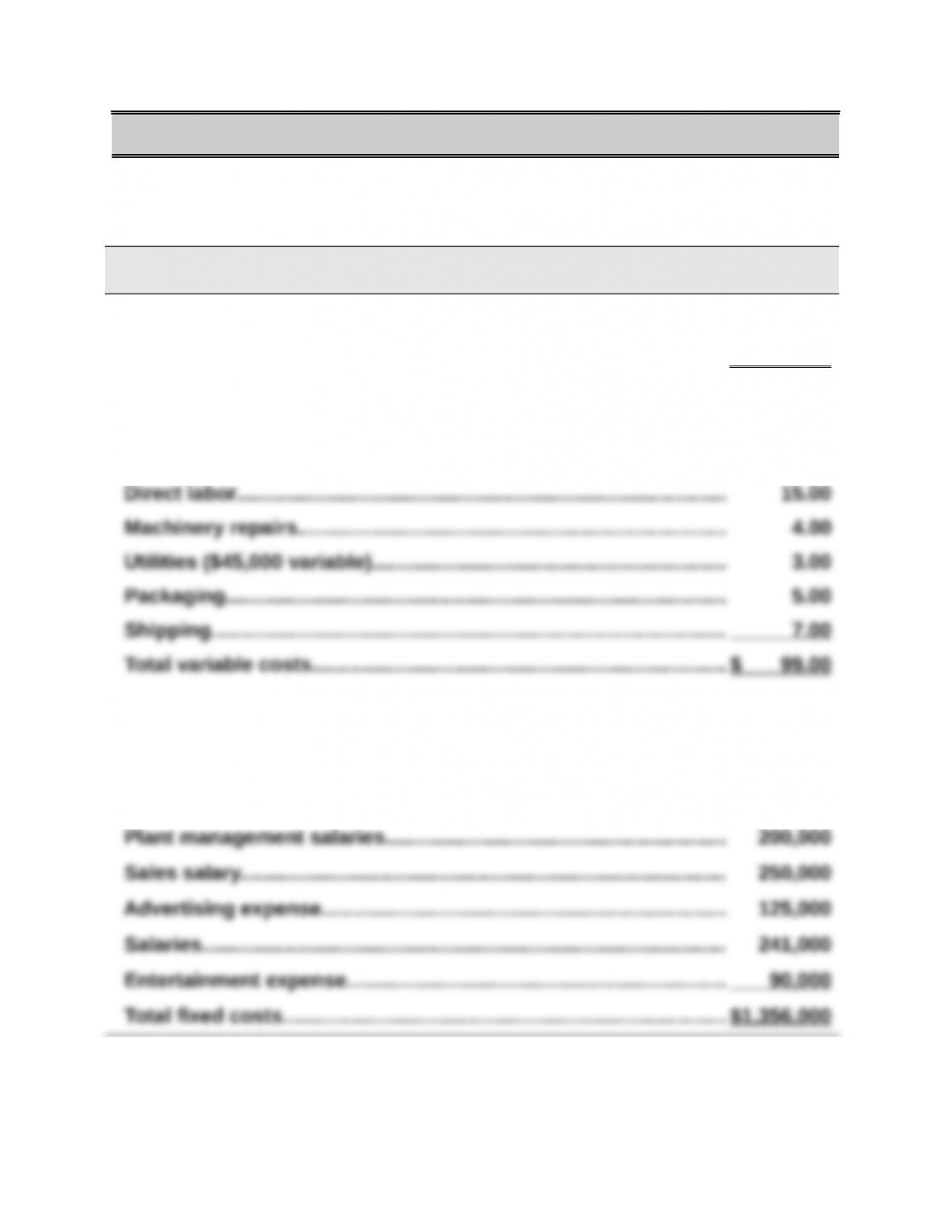

PHOENIX COMPANY

Flexible Budgets

For Year Ended December 31, 2015

Flexible Budget Flexible Flexible

Variable

Amount

per Unit

Total

Fixed

Cost

Budget for

Unit Sales

of 14,000

Budget for

Unit Sales

of 16,000

Sales………………………………. $200.00 $2,800,000 $3,200,000

Variable costs

Direct materials…………….. 65.00 910,000 1,040,000

Fixed costs

Depreciation—Plant Equip.... $ 300,000 300,000 300,000

Utilities…………………………. 150,000 150,000 150,000

Problem 23-1A (Continued)

Part 3

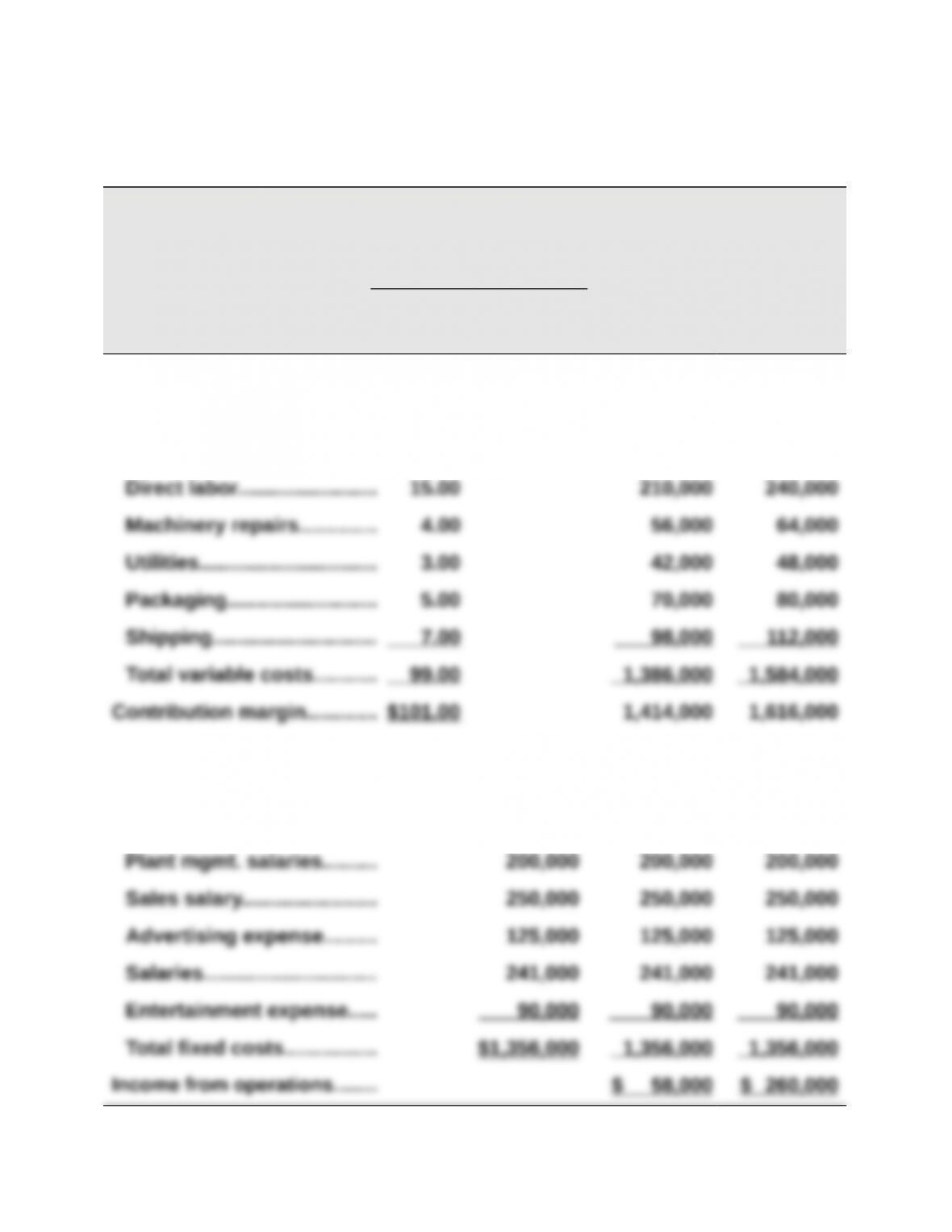

Operating income increase for a 15,000 to 18,000 unit sales increase

Possible sales (units)……………………………………………………. 18,000 Units

Contribution margin per unit…………………………………………. x $101

*Alternate solution format

Unit increase………………………………………………………………………………….. 3,000 Units

Since there is no increase in fixed costs, the expected increase in operating

income is the same $303,000.

Part 4

Operating income (loss) at 12,000 units

Possible sales (units)……………………………………………………. 12,000 Units

Problem 23-2A (45 minutes)

Part 1

PHOENIX COMPANY

Flexible Budget Performance Report

For Year Ended December 31, 2015

Flexible Actual

Budget Results Variances*

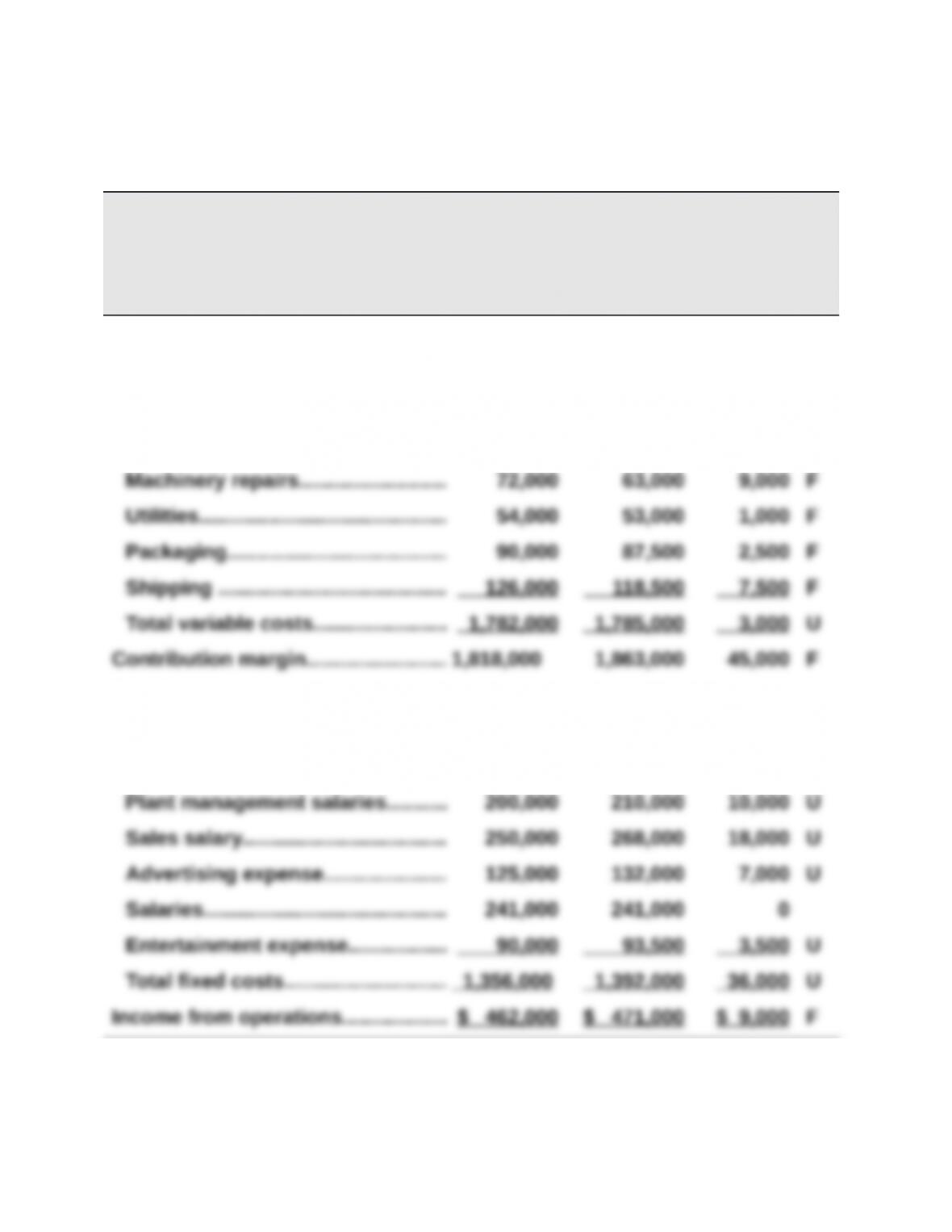

Sales (18,000 units)……………………. $3,600,000 $3,648,000 $48,000 F

Variable costs

Direct materials……………………….. 1,170,000 1,185,000 15,000 U

Direct labor……………………………… 270,000 278,000 8,000 U

Fixed costs

Depreciation—Plant equip………… 300,000 300,000 0

Utilities……………………………………. 150,000 147,500 2,500 F

*F = Favorable variance; and U = Unfavorable variance.

Problem 23-2A (Continued)

Part 2

(a) Analysis of sales variance

Total Per unit

Budgeted sales…………………………………………………….$3,600,000 $200.00

* (rounded)

Interpretation: The sales variance is favorable because the actual price

was higher than planned.

(b) Analysis of direct materials variance

Total Per unit

Budgeted materials………………………………………………$1,170,000 $ 65.00

Interpretation: The direct materials variance is unfavorable for two

Problem 23-3A (60 minutes)

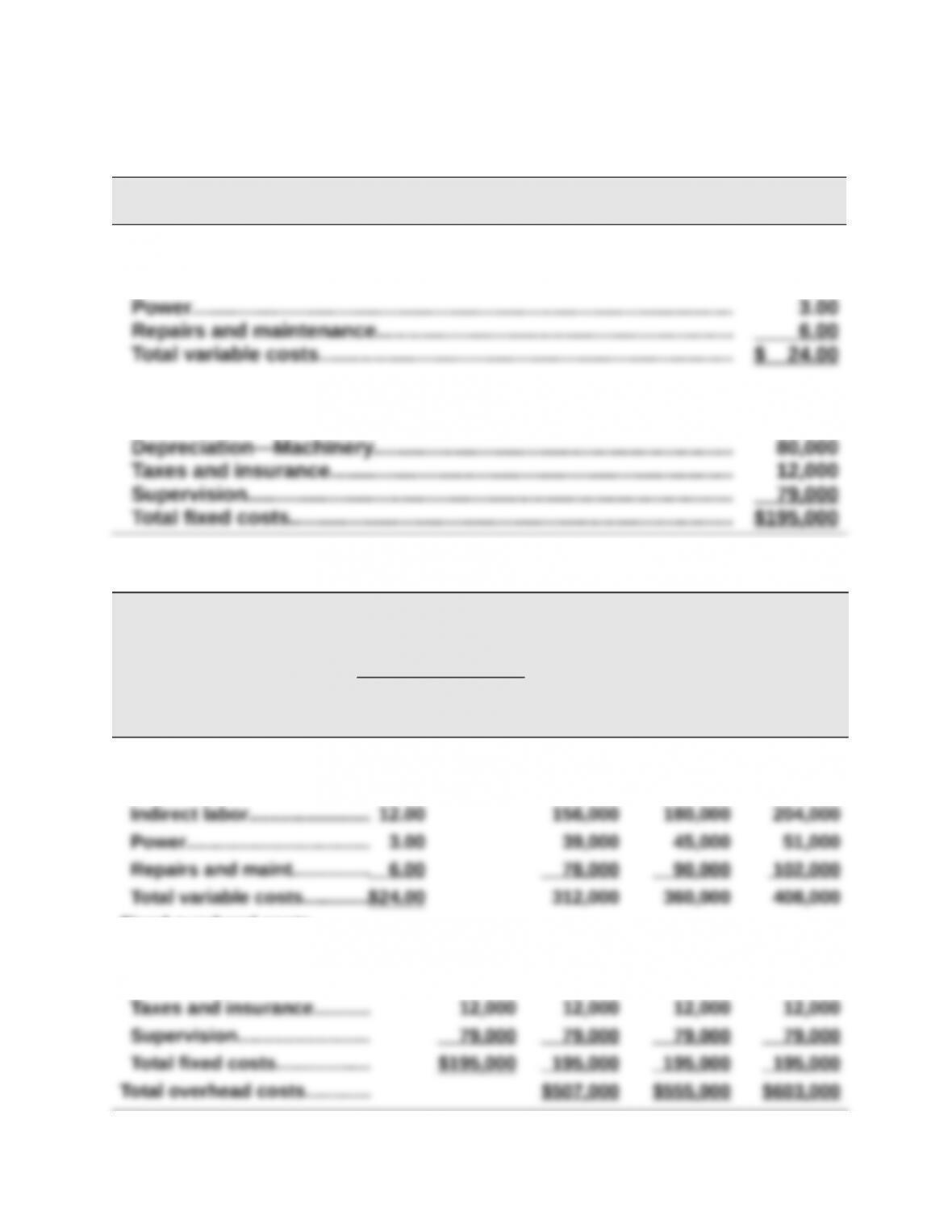

Part 1

Variable or Fixed Classification Amount

Variable costs (total divided by 15,000 units)

Indirect materials………………………………………………………………… $ 3.00

Indirect labor………………………………………………………………………. 12.00

Fixed costs (per month)

Depreciation—Building……………………………………………………….. $ 24,000

Part 2

ANTUAN COMPANY

Flexible Overhead Budgets

For Month Ended October 31

Flexible Budget Flexible Flexible Flexible

Variable

Amount

per Unit

Total

Fixed

Cost

Budget for

Unit Sales

of 13,000

Budget for

Unit Sales

of 15,000

Budget for

Unit Sales

of 17,000

Variable overhead costs

Indirect materials…………….$ 3.00 $ 39,000 $ 45,000 $ 51,000

Fixed overhead costs

Depreciation—Building…... $ 24,000 24,000 24,000 24,000

Depreciation—Mach……….. 80,000 80,000 80,000 80,000

Problem 23-3A (Continued)

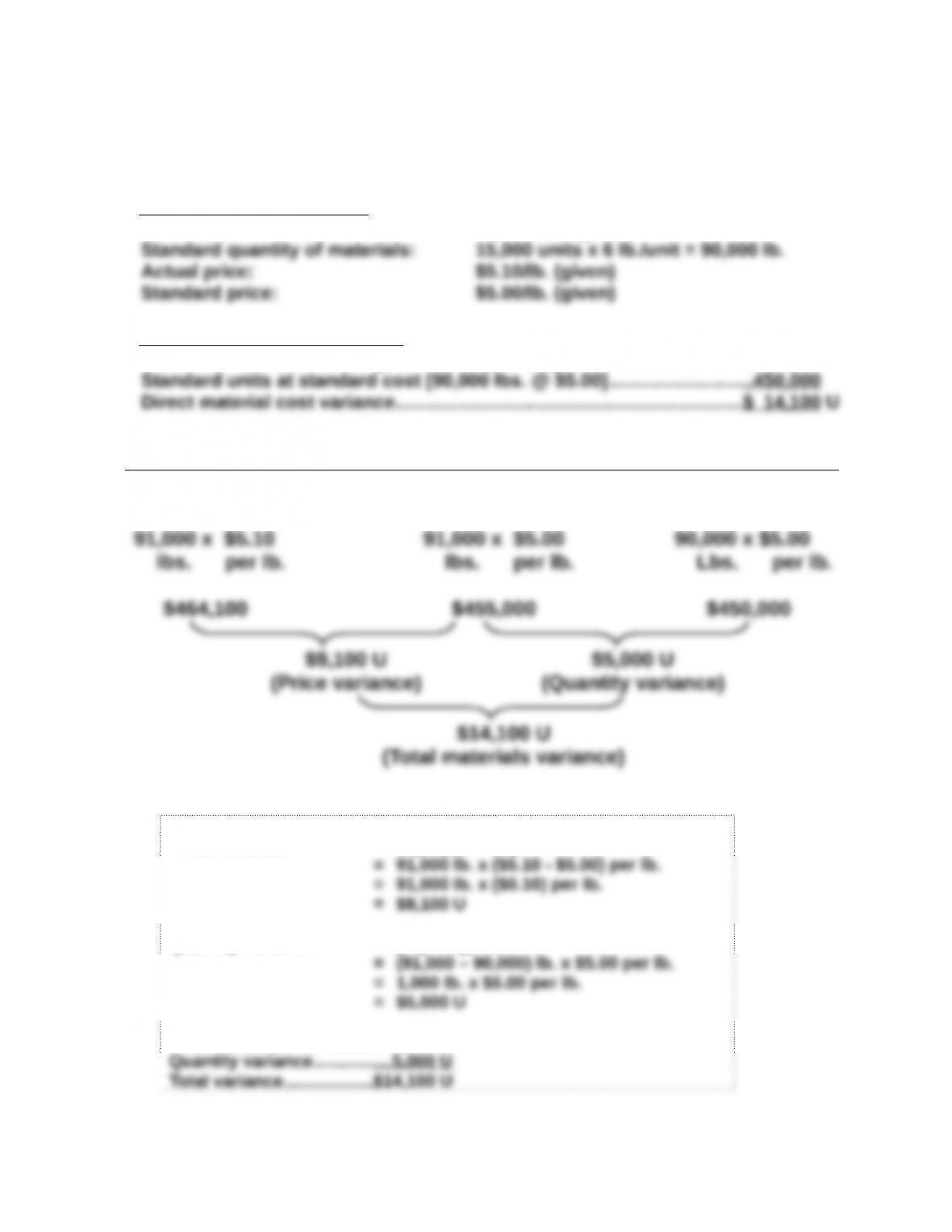

Part 3 Direct Materials Variances

Preliminary computations

Actual material used: 91,000 lbs. (given)

Direct material cost variances

Actual units at actual cost [91,000 lbs. @ $5.10]……………………………….$464,100

Direct Materials Price and Quantity Variances

Actual Costs

AQ x AP AQ x SP

Standard Costs

SQ x SP

Alternate solution format

Price variance = AQ x (AP – SP)

Quantity variance = (AQ – SQ) x SP

Price variance…………………..$ 9,100 U