Exercise 23-15 (25 minutes)

Part 1

Direct materials price variance:

Actual cost of direct materials used (16,000 x $4.05)…………………………$ 64,800

Direct materials quantity variance:

Actual quantity used x Standard price (16,000 x $4.00)……………………..$ 64,000

Part 2

Direct labor rate variance:

Actual hours x Actual rate per hour (5,545 x $19.00***)………………………$105,355

Direct labor efficiency variance:

Actual hours x Standard rate per hour (5,545 x $20.00)……………………..$110,900

Exercise 23-16 (30 minutes)

1.

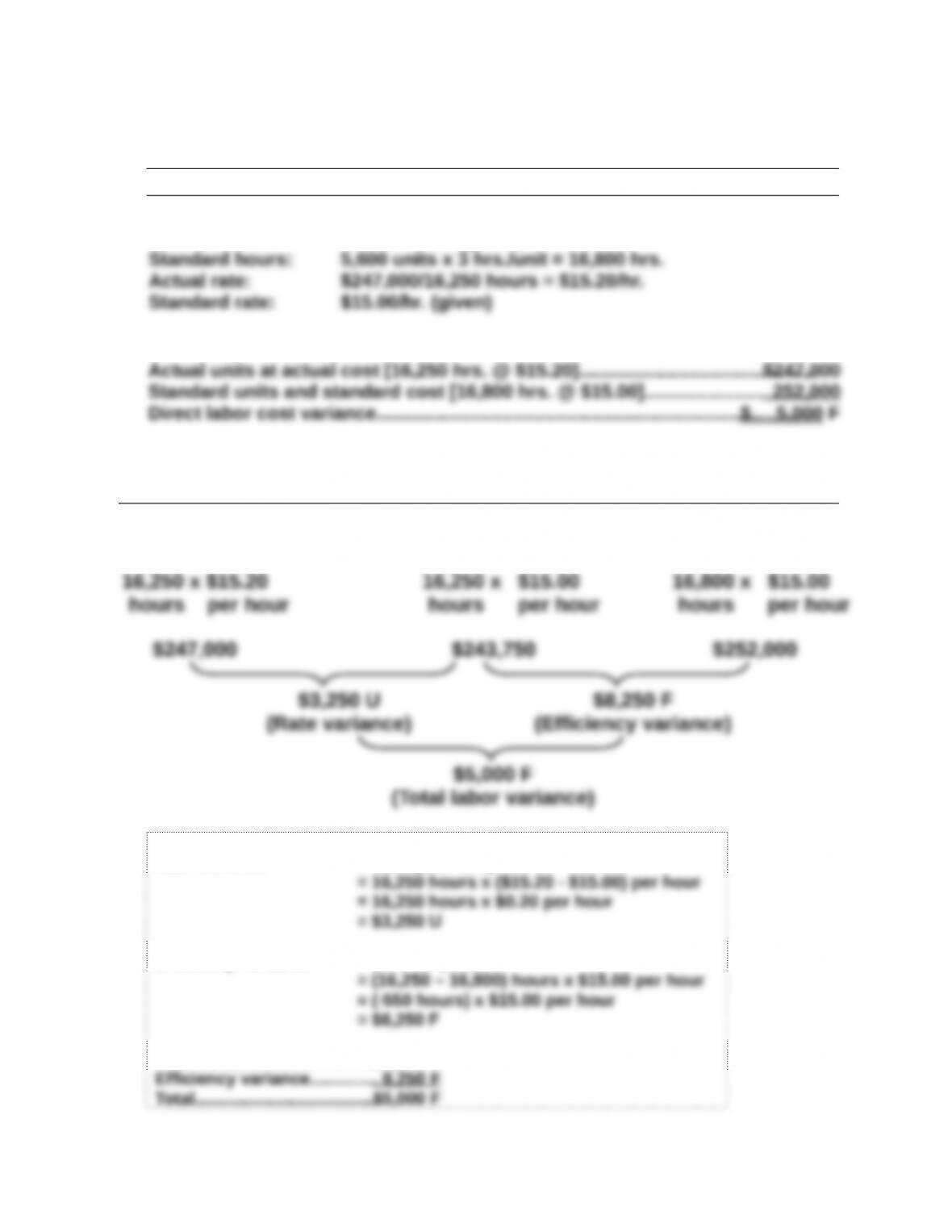

October variances

Preliminary computations

Actual hours: 16,250 hours (given)

Direct labor cost variances

Rate and efficiency variances

Actual Cost

AH x AR AH x SR

Standard Cost

SH x SR

Alternate solution format

Rate variance = AH x (AR – SR)

Efficiency variance = (AH – SH) x SR

Rate variance……………………$3,250 U

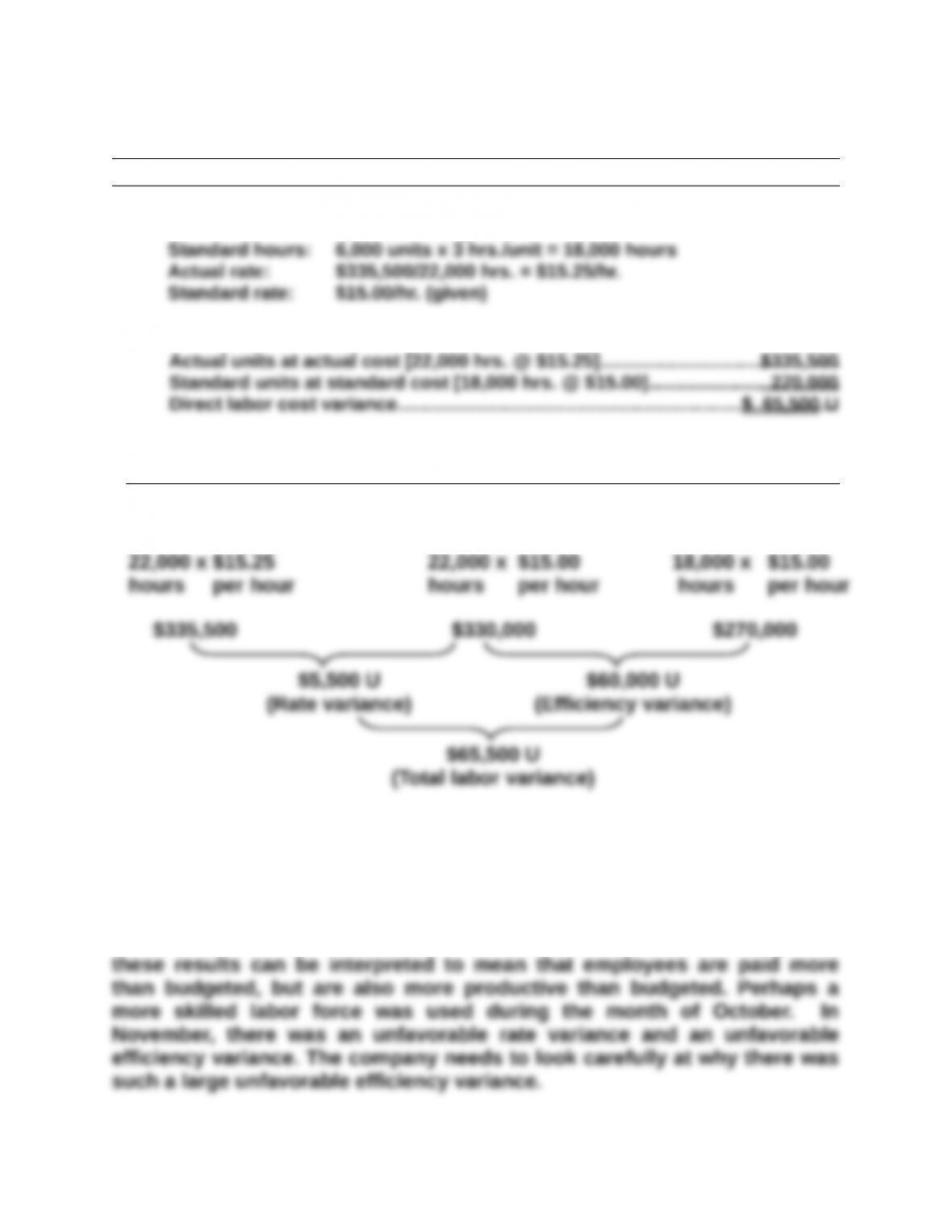

Exercise 23-16 (Concluded)

November variances

Preliminary computations

Actual hours: 22,000 hours (given)

Direct labor cost variances

Rate and efficiency variances

Actual Cost

AH x AR AH x SR

Standard Cost

SH x SR

2.

The unfavorable labor rate variance in October means the actual rate for an

hour of labor is greater than budgeted. The favorable labor efficiency

variance means the actual hours used are less than budgeted. Together,

Exercise 23-17 (20 minutes)

1. Predetermined overhead rate computations

Expected volume………………………………………………………….. 75%

Expected total overhead……………………………………………….. $2,100,000

2. Variable overhead cost variance

Variable overhead cost incurred [given]…………………………………………..$1,375,000

Fixed overhead cost variance

Fixed overhead cost incurred [given]………………………………………$ 628,600

Exercise 23-18A (20 minutes)

1.

Variable overhead spending and efficiency variances

Actual Overhead

AH x AVR AH x SVR

Applied Overhead

SH x SVR

Interpretation:

The $15,000 unfavorable spending variance means the actual cost of

variable overhead is more than budgeted. This unfavorable variance can

The $40,000 favorable efficiency variance occurs because the actual labor

Exercise 23-18A (continued)

2.

Fixed overhead spending and volume variances

Actual Overhead Budgeted Overhead Applied Overhead

Interpretation

The $40,000 unfavorable volume variance is the result of the company

3. The controllable variance is computed as:

Variable overhead spending variance…………………………….. $15,000 U

The controllable variance refers to activities that are considered within

Exercise 23-19 (20 minutes)

Information given

Planned units to be produced = 80% x 50,000 capacity = 40,000 units

hours

1. Total overhead planned at 80% level (25,000 direct labor hours)

Predetermined

Cost

Cost per

Hour

Fixed overhead………………………….. $ 50,000 $ 2.00

2. Total overhead variance

Total actual overhead (given)………………………………………………………….$305,000

Exercise 23-20 (30 minutes)

1. Preliminary variance computations

Variable overhead spending and efficiency variances

Actual Overhead

AH x AVR AH x SVR

Applied Overhead

SH x SVR

Fixed overhead spending and volume variances

Actual Overhead Budgeted Overhead Applied Overhead

(Given) 21,875 x $2

$ *

(Total fixed overhead variance)

* Not computable from information given

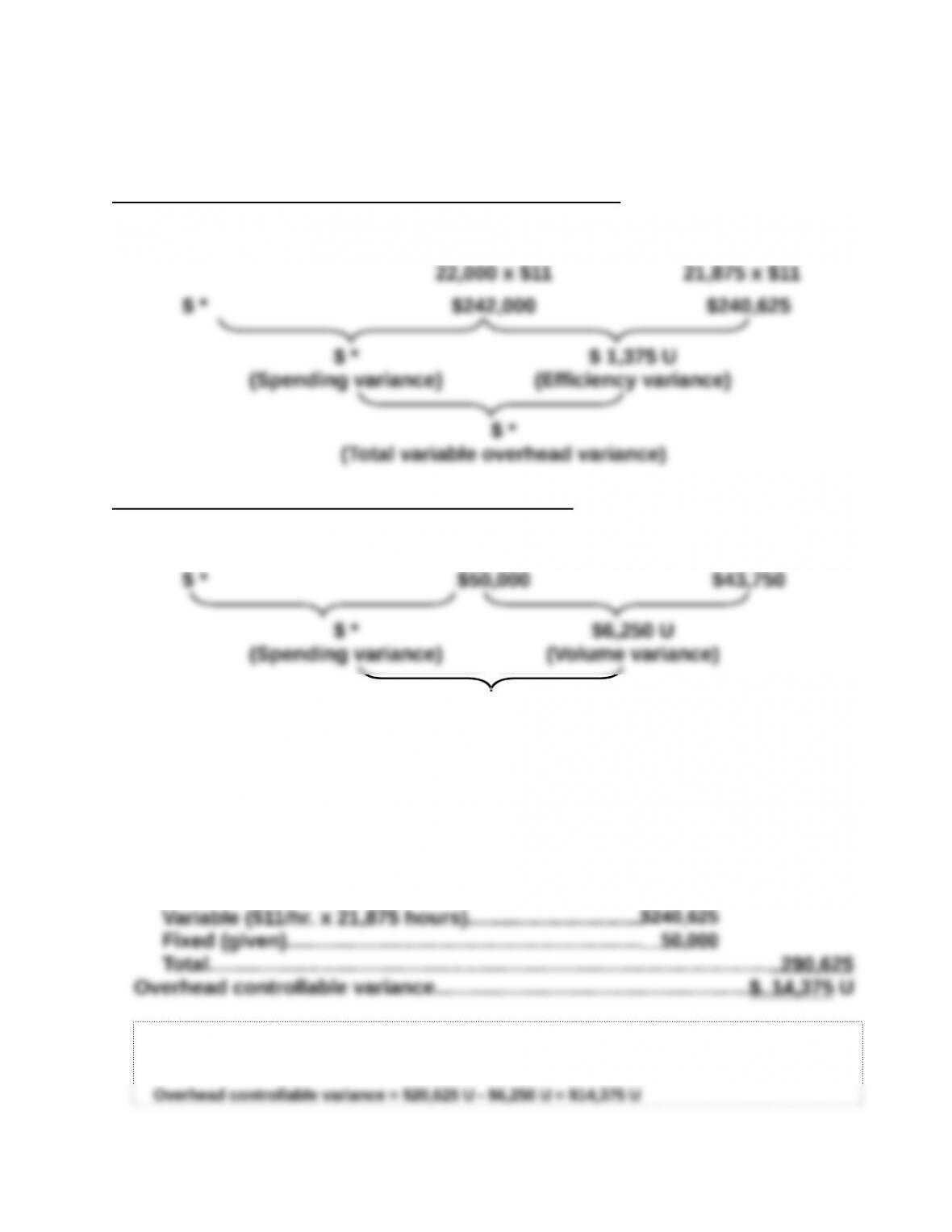

2. Overhead controllable variance*

Total actual overhead (given) $305,000

Flexible budget overhead

* Alternative solution approach: We know the overhead controllable variance is equal to the

total overhead variance less the overhead volume variance. Then, using the results from parts

1 and 2, we can compute the overhead controllable variance as

EX

Exercise 23-21 (25 minutes)

Preliminary calculations:

Variable overhead rate per DL hour = $48,000/24,000 = $2 per hour

Part 1

Total actual overhead (given) ………………………… $99,250

Flexible budget overhead

Variable ($2 per hour x 27,000 hours)…………………. $54,000

Part 2

Exercise 23-21 (continued)

Part 3

JAMES CORP.

Overhead Variance Report

For Month Ended May 31

Volume Variance

Expected production level…………………………………………..80% of capacity

Production level achieved……………………………………………90% of capacity

Volume variance…………………………………………………………$5,550 (favorable)

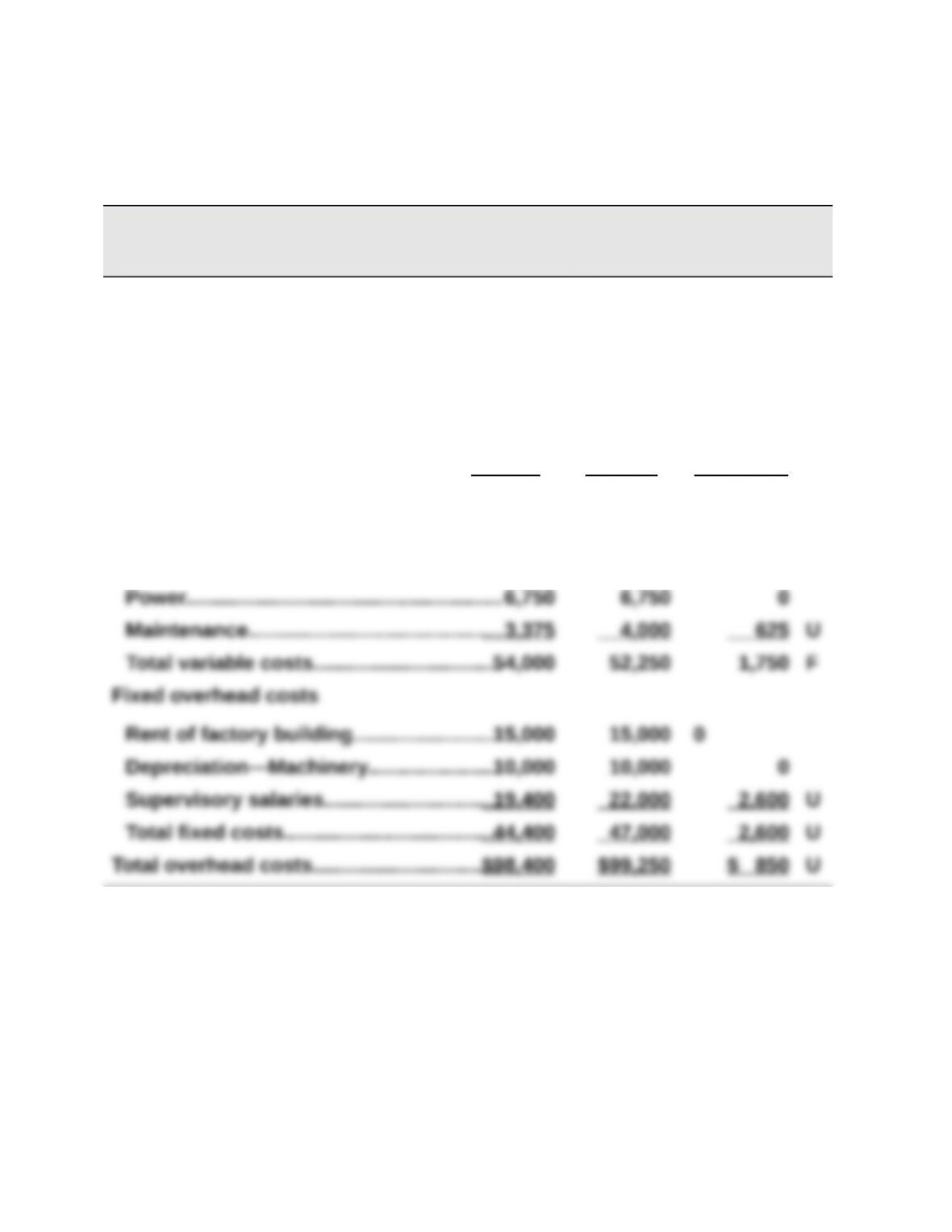

Flexible Actual

Controllable Variance Budget Results Variances*

Variable overhead costs

Indirect materials………………………………$16,875 $15,000 $1,875 F

Indirect labor…………………………………….27,000 26,500 500 F

* F = Favorable variance; and U = Unfavorable variance.