Chapter 23 – Flexible Budgets and Standard Costs

EXERCISES

Exercise 23-1 (20 minutes)

Item Cost

a. Bike frames Variable

b. Screws for assembly Variable

g. Incoming shipping expenses* Variable

h. Taxes on property Fixed

i. Office supplies (This item can be a variable cost, but it usually is

not because it doesn’t often change in direct proportion to changes in

Fixed

incoming shipments, not production.

** Gas used for heating is often a mixed cost rather than strictly variable.

23-1355

Education.

Chapter 23 – Flexible Budgets and Standard Costs

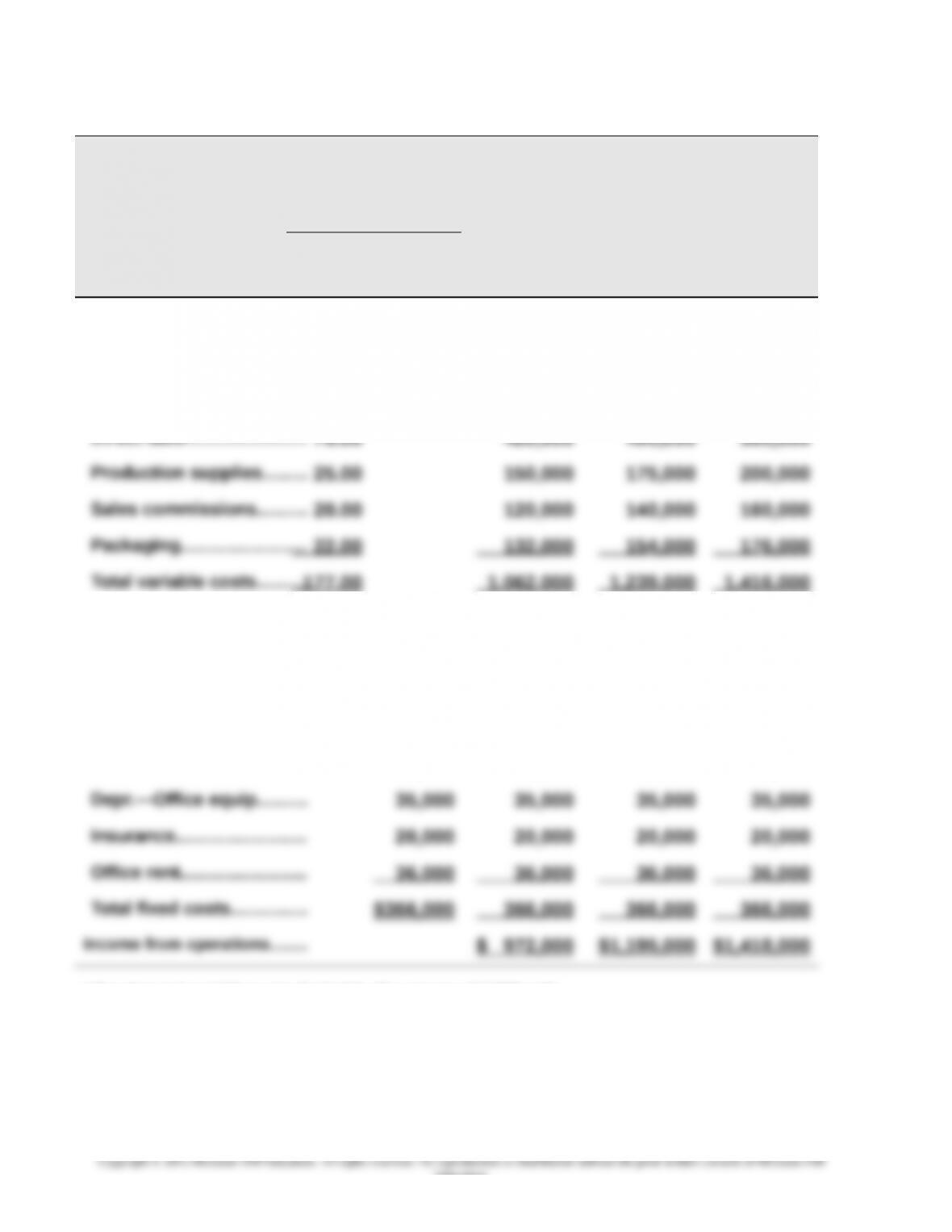

Exercise 23-2 (30 minutes)

TEMPO COMPANY

Flexible Budgets

For Quarter Ended March 31, 2015

Flexible Budget Flexible Flexible Flexible

Variable

Amount

per Unit*

Total

Fixed

Cost

Budget for

Unit Sales

of 6,000

Budget for

Unit Sales

of 7,000

Budget for

Unit Sales

of 8,000

Sales……………..…....…..…...

$400.00 $2,400,000 $2,800,000 $3,200,000

Variable costs

Direct materials…….......... 40.00 240,000 280,000 320,000

Direct labor..………………… 70.00 420,000 490,000 560,000

Contribution margin….......

$223.00 1,338,000 1,561,000 1,784,000

Fixed costs

Plant manager salary....... $ 65,000 65,000 65,000 65,000

Advertising…..…..…..…..... 125,000 125,000 125,000 125,000

Admin. salaries…………….. 85,000 85,000 85,000 85,000

* Equals total variable costs divided by the volume of 7,000 units.

23-1356

Education.

Chapter 23 – Flexible Budgets and Standard Costs

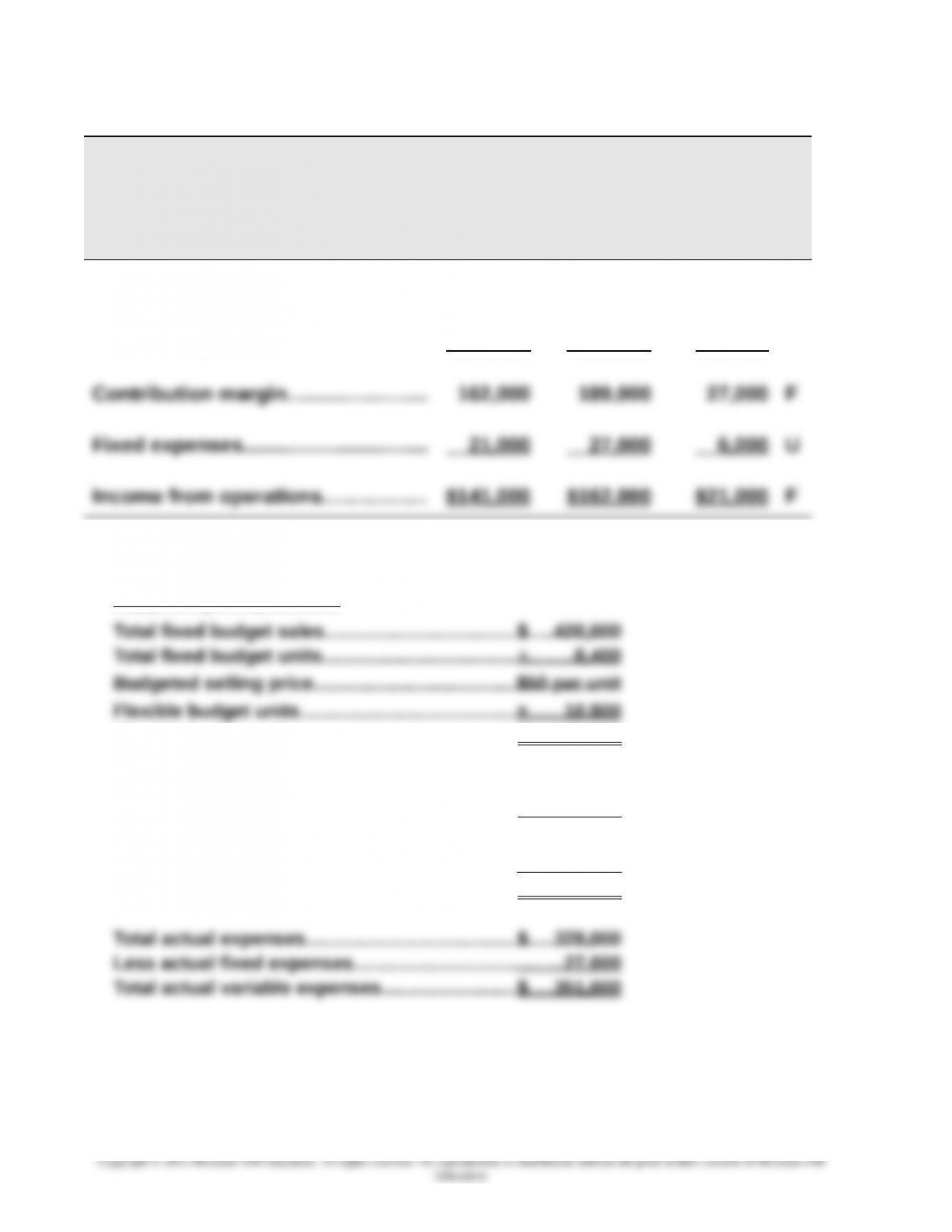

Exercise 23-3 (25 minutes)

SOLITAIRE COMPANY

Flexible Budget Performance Report

For Month Ended June 30

Flexible Actual

Budget Results Variances

Sales (10,800 units)………..…..………. $540,000 $540,000 $ 0

Variable expenses……………..……….. 378,000 351,000 27,000 F

Supporting computations

Flexible budget sales…………..……………………………….……….$ 540,000

Total fixed budget variable expenses…………….….….….…...$ 294,000

Total units budgeted……………………………….………………….…÷ 8,400

Budgeted variable expenses…………..…………..….….….…..…$35 per unit

Flexible budget units……………..…………………….….….…..…...× 10,800

Flexible budget variable expenses………….….…..….….….….$ 378,000

23-1357

Chapter 23 – Flexible Budgets and Standard Costs

Exercise 23-4 (25 minutes)

BAY CITY COMPANY

Flexible Budget Performance Report

For Month Ended July 31

Flexible Actual

Budget Results Variances

Sales (7,200 units)…………...……….... $720,000 $737,000 $17,000 F

Variable expenses……………..……….. 468,000 483,000 15,000 U

Supporting computations

Flexible budget units……………..…….….….….…..….…..× 7,200

Flexible budget sales…………..……………………..….…...$ 720,000

Total fixed budget variable expenses…….….….........$ 487,500

Total units budgeted……………………….….….…..….…...÷ 7,500

Budgeted variable expenses…………..……………………$ 65 per unit

23-1358

Chapter 23 – Flexible Budgets and Standard Costs

Exercise 23-5 (10 minutes)

Exercise 23-6 (5 minutes)

Following management by exception, the company should focus on those

variances that exhibit the greatest differences from the standard. This would

Exercise 23-7 (15 minutes)

Exercise 23-8 (10 minutes)

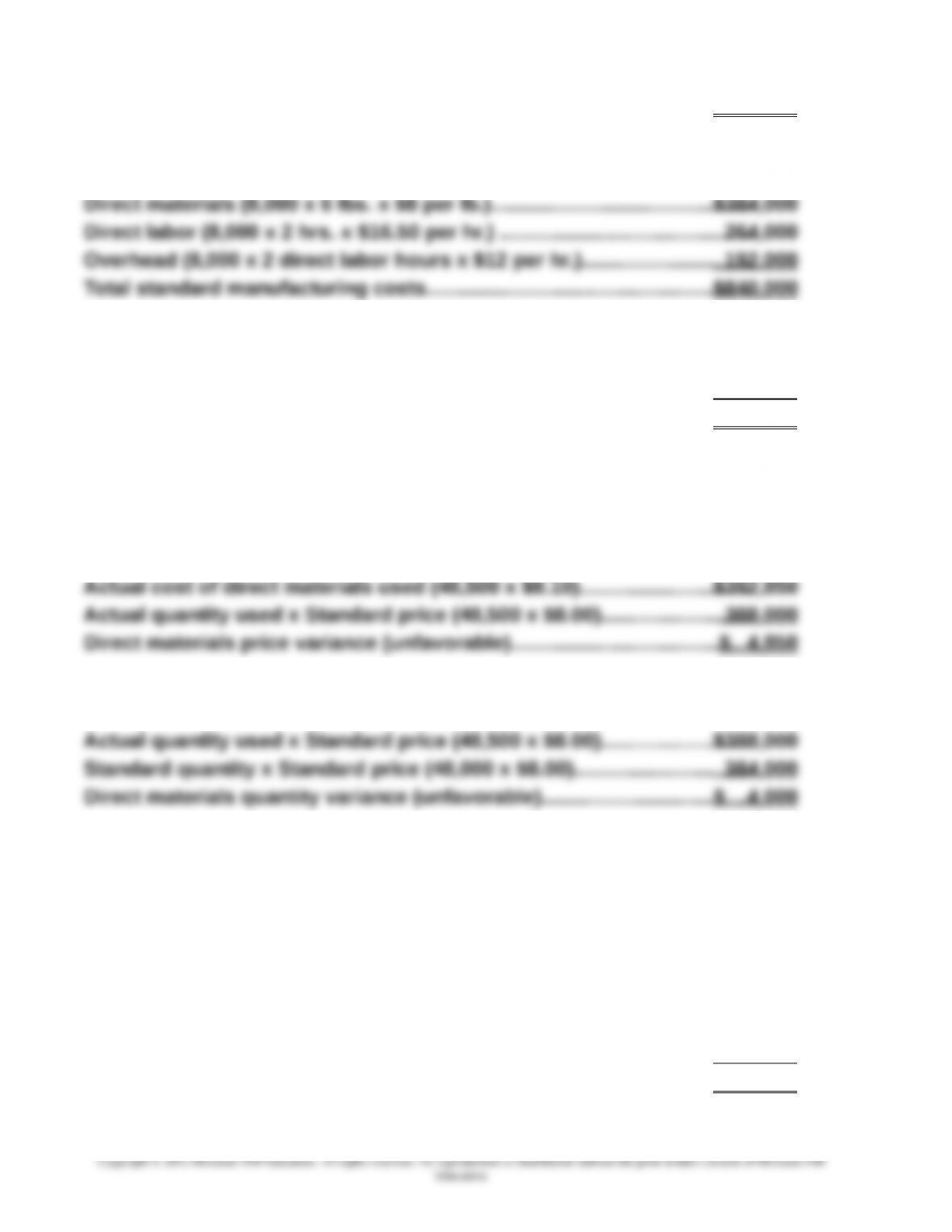

(1) The standard cost for one unit is computed as:

Direct materials (6 lbs. @$8 per lb.)…………….………..………..………. $ 48

Chapter 23 – Flexible Budgets and Standard Costs

Total actual manufacturing costs……………………………………..…………..…..$849,900

Standard overhead costs to produce actual activity:

Total actual manufacturing costs ………………………………..…..…………..…..

Total standard manufacturing costs……………………………..………..…………

$849,900

840,000

Total cost variance (unfavorable) ………………………………..………..………....$ 9,900

Exercise 23-9 (15 minutes)

Direct materials price variance:

Direct materials quantity variance:

*8,000 units x 6 pounds per unit = 48,000 pounds

Exercise 23-10 (15 minutes)

Direct labor rate variance:

Actual hours x Actual rate per hour (15,700 x $16.50)…………………..…….$259,050

Actual hours x Standard rate per hour (15,700 x $16.00)………………….... 251,200

Direct labor rate variance (unfavorable)…………………….………..………..…..$ 7,850

23-1360

Chapter 23 – Flexible Budgets and Standard Costs

Direct labor efficiency variance:

Exercise 23-11 (25 minutes)

Part 1

Direct materials price variance:

Actual cost of direct materials used (138,000 x $3.75)…………....………….$517,500

Actual quantity used x Standard price (138,000 x $4.00)..………..………... 552,000

Direct materials price variance (favorable)…………………………………….….. 34,500

Direct materials quantity variance:

*9,000 units x 15 pounds per unit = 135,000 pounds

Exercise 23-11 (continued)

Part 2 Direct labor rate variance:

Actual hours x Actual rate per hour (31,000 x $15.10)…………………..…….$468,100

Actual hours x Standard rate per hour (31,000 x $15.00)………………….... 465,000

Direct labor rate variance (unfavorable)…………………….………..………..…..$ 3,100

Direct labor efficiency variance:

23-1361

Chapter 23 – Flexible Budgets and Standard Costs

Standard hours x Standard rate per hour (27,000** x $15.00)……………… 405,000

Direct labor efficiency variance (unfavorable)…………….………..………..….$ 60,000

**9,000 units x 3 hours per unit = 27,000 hours

Exercise 23-12 (25 minutes)

Part 1 Direct materials price variance:

Direct materials quantity variance:

Part 2 Direct labor rate variance:

Actual hours x Actual rate per hour (37,600 x $6.05)……………………..…...$227,480

Actual hours x Standard rate per hour (37,600 x $6.00)…………………..…. 225,600

Direct labor rate variance (unfavorable)…………………….………..………..…..$ 1,880

Direct labor efficiency variance:

23-1362

Chapter 23 – Flexible Budgets and Standard Costs

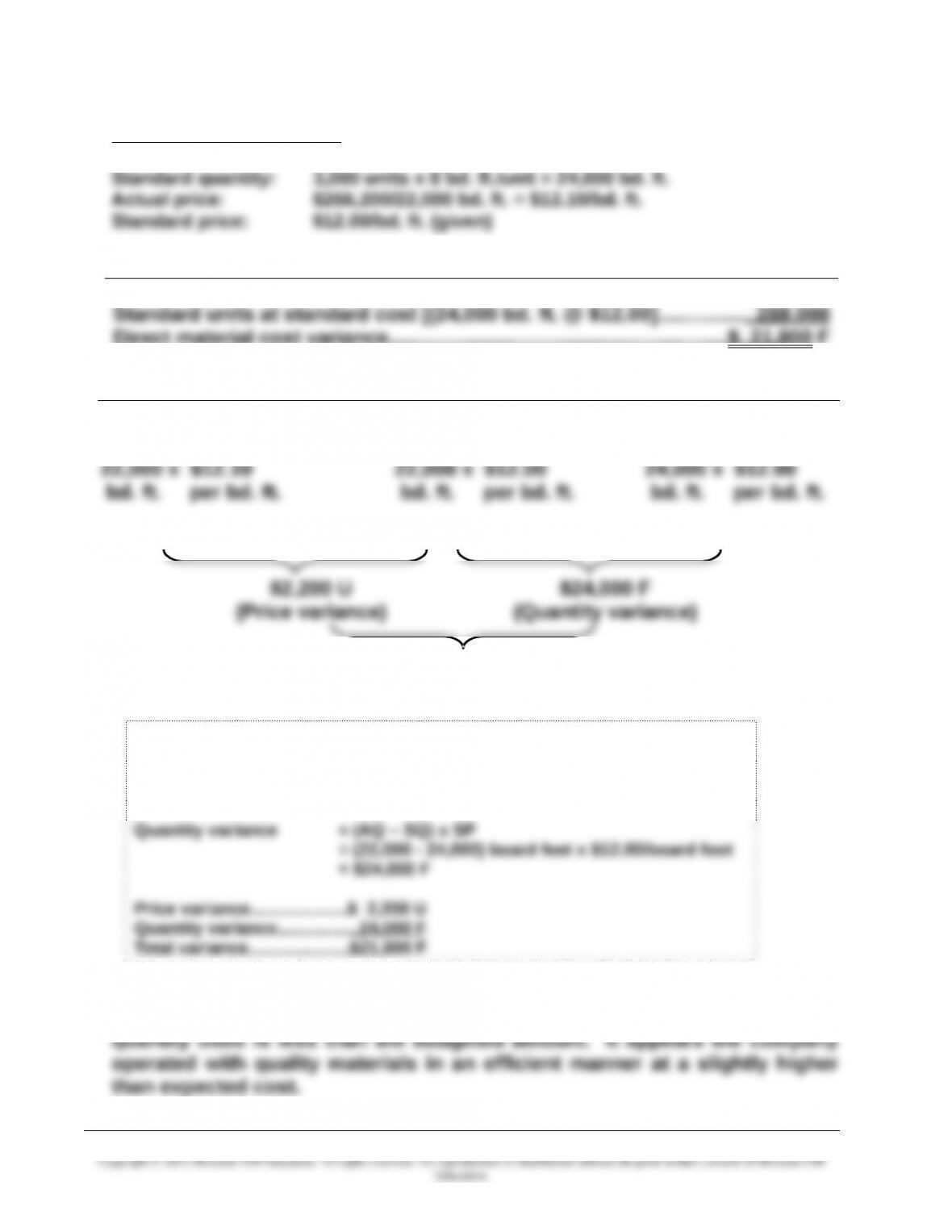

Exercise 23-13 (30 minutes)

1. Preliminary computations

Actual quantity: 22,000 bd. ft. (given)

Direct material cost variances

Actual units at actual cost [22,000 bd. ft. @ $12.10]………………..………….$266,200

Direct material cost variance…………………………………..……..…………..…….$ 21,800 F

Price and quantity variances

Actual Cost

AQ x AP AQ x SP

Standard Cost

SQ x SP

$266,200 $264,000 $288,000

$21,800 F

(Total materials variance)

Alternate solution format

Price variance = AQ x (AP – SP)

= 22,000 board feet x ($12.10 – $12.00)

= $2,200 U

2. The unfavorable price variance means the actual price paid is more than

the budgeted price. The favorable quantity variance means the actual

23-1363