Problem 22-8A (Continued)

Part 4

DIMSDALE SPORTS CO.

General and Administrative Expense Budgets

January, February, and March 2016

January February March Total

Salaries……………………..…….….…….….…….$12,000 $12,000 $12,000 $36,000

Maintenance………………….….…….….…….…2,000 2,000 2,000 6,000

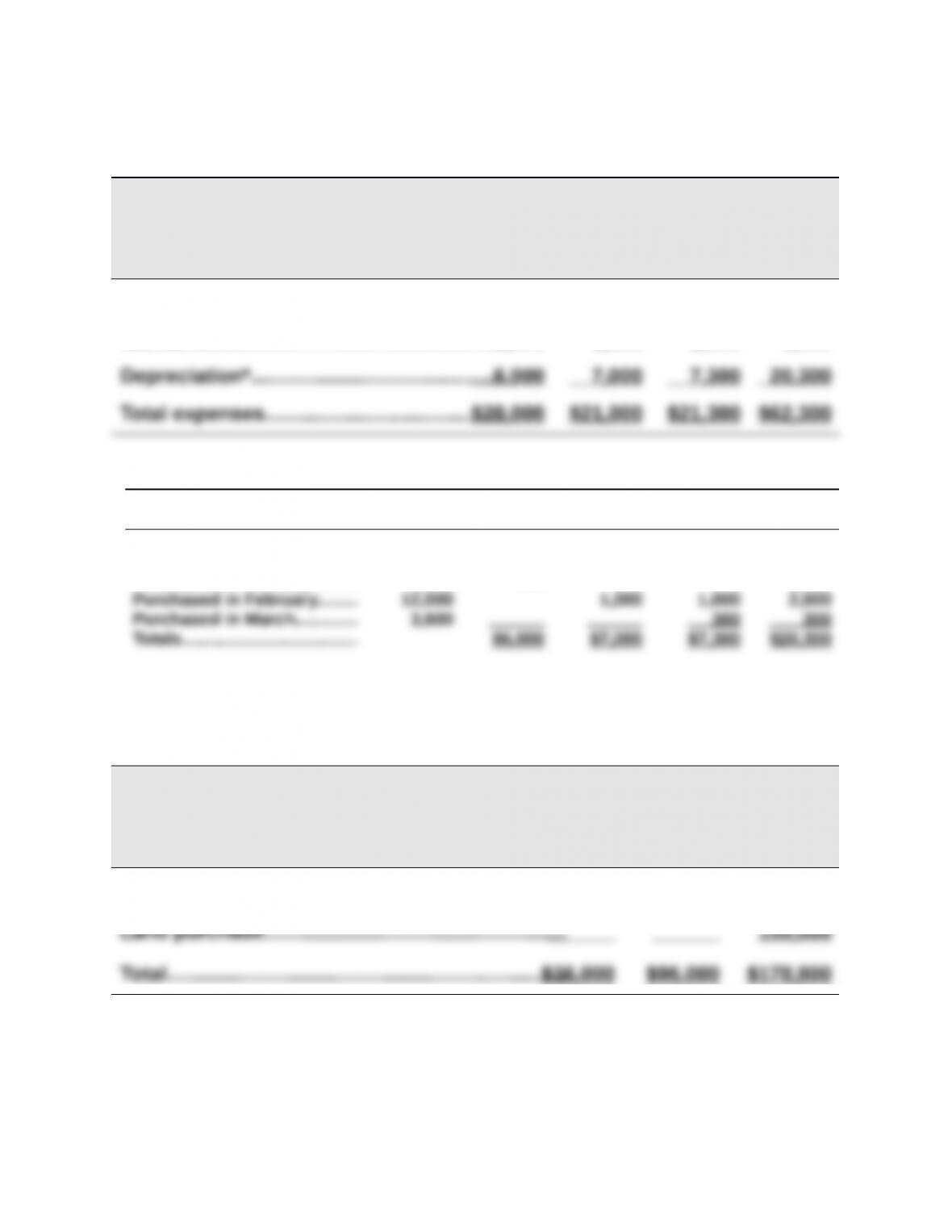

* Depreciation expense calculations

Annual

Amount January February March Total

Equipment owned

on 12/31/2015....…..…....….. $67,500 $5,625 $5,625 $5,625 $16,875

Purchased in January......... 4,500 375 375 375 1,125

Part 5

DIMSDALE SPORTS CO.

Capital Expenditures Budgets

January, February, and March 2016

January February March

Equipment purchases……………………………………$36,000 $96,000 $ 28,800

Problem 22-8A (Continued)

Part 6

DIMSDALE SPORTS CO.

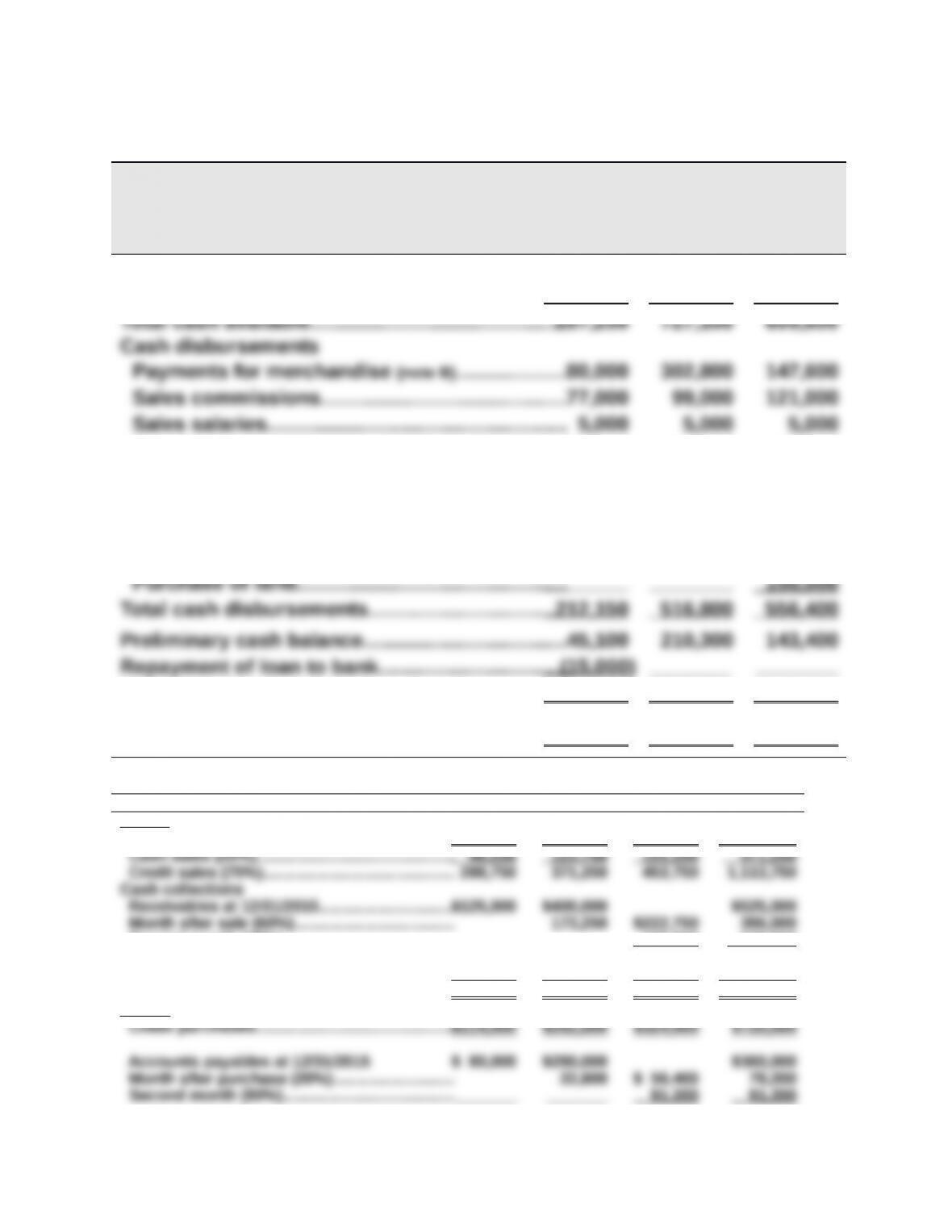

Cash Budgets

January, February, and March 2016

January February March

Beginning cash balance…………….…….….…….….$ 36,000 $ 30,100 $210,300

Cash receipts from customers (note A)..….…....... 221,250 697,000 489,500

General & administrative salaries……….….......12,000 12,000 12,000

Maintenance expense………………………….….….. 2,000 2,000 2,000

Interest ($15,000 x 1%)..…..…..….………………………. 150

Taxes payable……………………………………..….….. 90,000

Purchases of equipment……..…….….…….….…..36,000 96,000 28,800

Ending cash balance……………………………………..$ 30,100 $210,300 $143,400

Loan balance, end of month…………………………..$ 0 $ 0 $ 0

Supporting calculations January February March Total

Note A: Cash receipts from customers

Total sales……………………..….……..…………..….$385,000 $495,000 $605,000 $1,485,000

Second month (40%)……………..…………..…….._______ _______ 115,500 115,500

Total from credit customers….……………..……. 125,000 573,250 338,250 1,036,500

Cash sales…………….……………..……….…..…….. 96,250 123,750 151,250 371,250

Total cash received….……………..………….……..$221,250 $697,000 $489,500 $1,407,750

Note B: Cash payments for merchandise

Problem 22-8A (Continued)

Part 7

DIMSDALE SPORTS CO.

Budgeted Income Statement

For Three Months Ended March 31, 2016

Sales salaries……………………………………..…….….…….. 15,000

General administrative salaries………………………….... 36,000

Maintenance expense……………………………………….…. 6,000

Depreciation expense……………………………………….…. 20,300

Part 8

DIMSDALE SPORTS CO.

Budgeted Balance Sheet

March 31, 2016

ASSETS

Cash…………………………….…….….…….….…. $ 143,400 Cash budget

Accounts receivable…………..…….….……... 602,250 Note C

LIABILITIES AND EQUITY

Accounts payable.…..………………………….. $ 549,600 Note G

Bank loan payable……………………………….. 0 Cash budget

Taxes payable (due 4/15/2016)….….….…… 120,220 Income stmt.

Problem 22-8A (Concluded)

Supporting Footnotes

Note C

Beginning receivables…………………………………………..…..$ 525,000

Credit sales……………………………………………….……….……. 1,113,750

Less cost of goods sold……………………………………….…... (810,000)

Ending inventory*……………………………………….….………...$ 60,000

*Also equals 2,000 units @ $30 = $60,000

Note E

Beginning equipment…………..……..…….……...…....…....….$ 540,000

Beginning accumulated depreciation…......…....…....…....$ 67,500

Depreciation expense…………………………………………….…. 20,300

Total……………………………………………………………….…….….$ 87,800

Note G

Beginning accounts payable………….………....…....…....….$ 360,000

Net income…………………………………………….…….……….…. 180,330

Total……………………………………………………………….…….….$ 426,330

PROBLEM SET B

Problem 22-1B (30 minutes)

Part 1

NSA COMPANY

Production Budget (in units)

Second Quarter

Budgeted ending inventory (bats)…………………………………………….….. 6,000

Part 2

NSA COMPANY

Direct Materials Budget (in lbs, except where noted)

Second Quarter

Materials (aluminum) needed for production (248,000 x 3)…………. 744,000

Materials cost per pound……………………………………………………….…. $4

Total cost of materials purchases (741,000 x $4)…………….….……...$2,964,000

Problem 22-1B (concluded)

Part 3

NSA COMPANY

Direct Labor Budget

Second Quarter

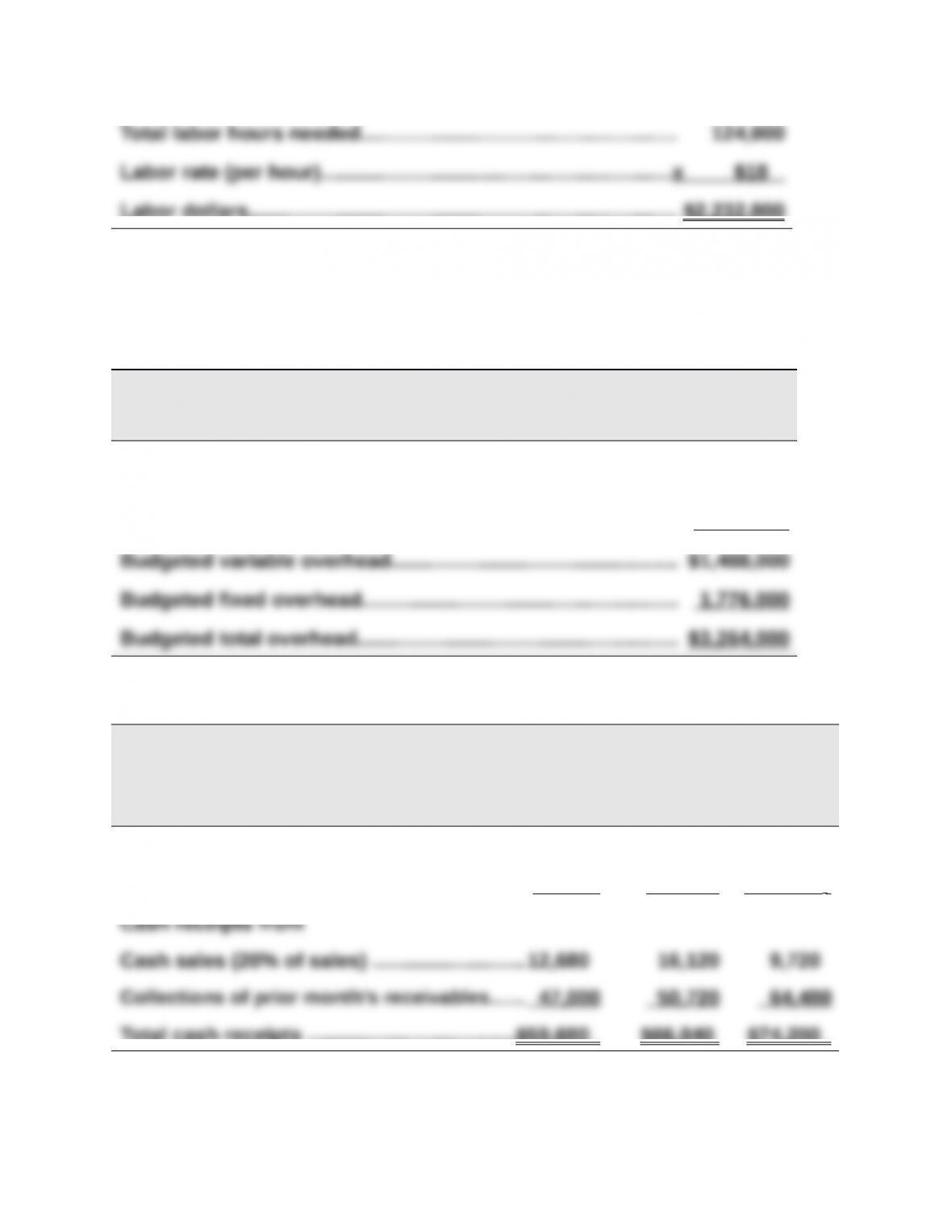

Units to be produced…………………………………………….….….… 248,000

Labor requirements per unit (hours)……………………………….. x 0.50

Labor dollars………………………………………………….….….…….… $2,232,000

Part 4

NSA COMPANY

Factory Overhead Budget

Second Quarter

Total labor hours needed……………………………….….…….….…. 124,000

Variable overhead rate per direct labor hour..….…….…........ x $12

Problem 22-2B (30 minutes)

(1)

A1 MANUFACTURING

Cash Receipts Budget

For July, August, and September

July August Sept.

Sales…………………………………….….…….….…. $63,400 $80,600 $48,600

Less ending accts. receivable (80%).......... 50,720 64,480 38,880

Total cash receipts ………..….….…….….……..$59,680 $66,840 $74,200

Problem 22-2B (continued)

(2)

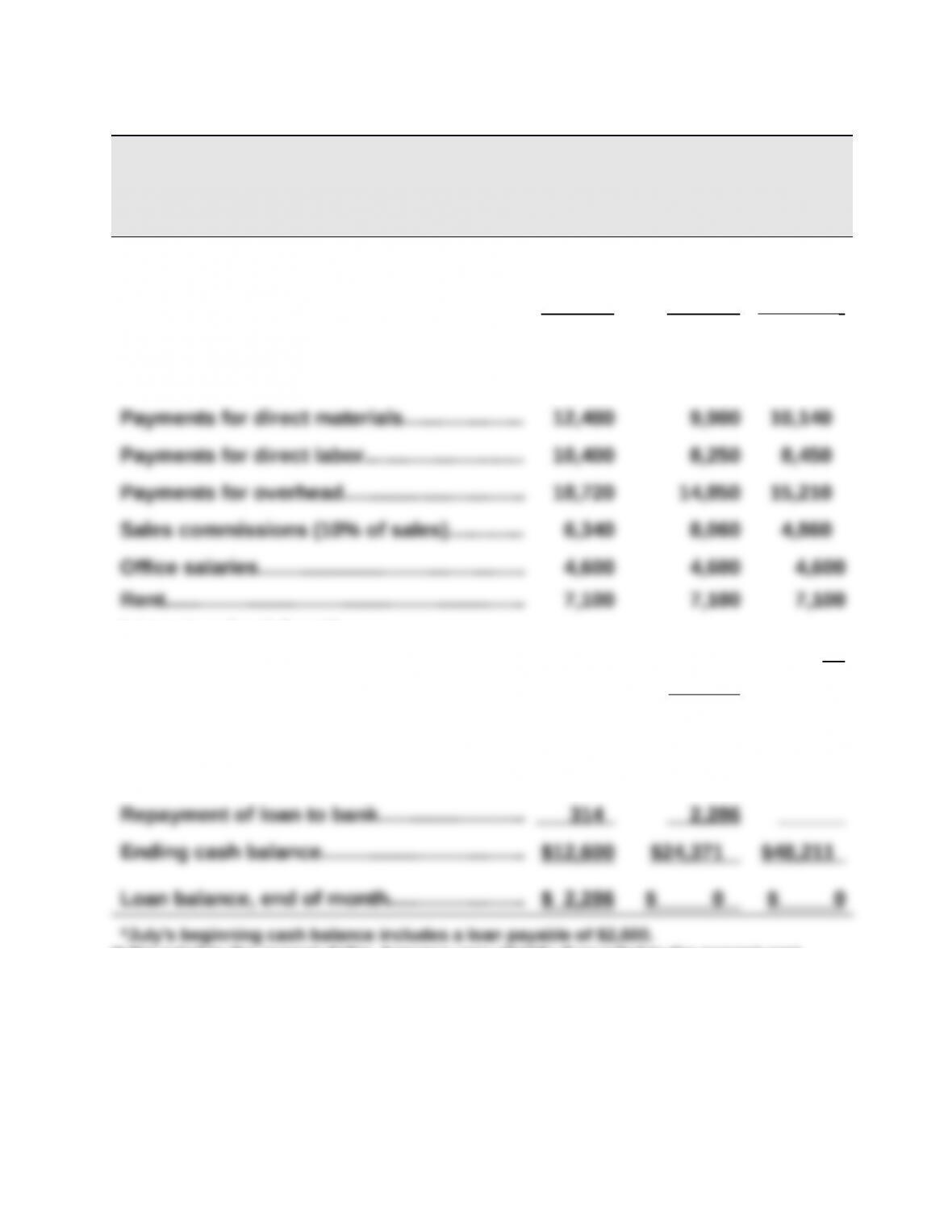

A1 MANUFACTURING

Cash Budget

For July, August, and September

July August Sept.

Beginning cash balance*…………….….……... $12,900 $12,600 $24,371

Cash receipts (from part 1)……………..….….. 59,680 66,840 74,200

Total cash available …………………….…….….. 72,580 79,440 98,571

Cash disbursements

Interest on bank loan**

July ($2,600 x 1%)……………………….….…...

August ($2,286 x 1%)…………………………...

Preliminary cash balance ……….….…….......

26

_______

$12,914

23

$26,657

_______

$48,211

Additional loan from bank……….….…….…...

** Rounded to the nearest dollar. Answers vary slightly if rounded to the nearest cent.