Exercise 20-21 (15 minutes)

PTO MANUFACTURING COMPANY

Cash Budget

For Month Ended September 30

Beginning cash balance……………………………..…….……$ 40,000

Other expenses…………………………………………….…….. 60,000

Accrued taxes…………………………………….…….…….….. 10,000

Interest on bank loan……………………………………….….. 1,000

Total cash disbursements………………………..….…….….. 210,500

Ending cash balance…………………….…….…….…….……. $ 84,500

*($80,000 x 35%) + ($110,000 x 65%)

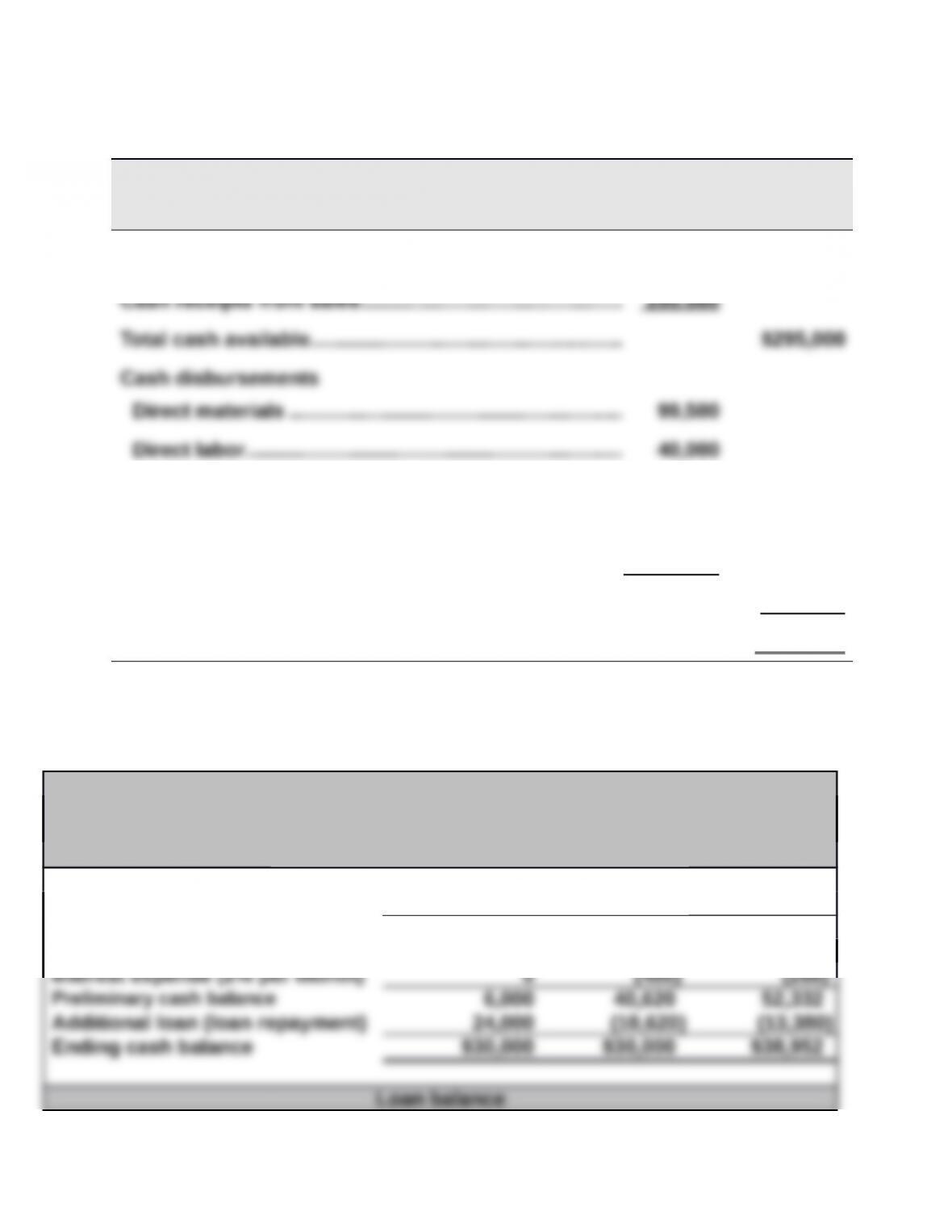

Exercise 22-22 (30 minutes)

Mike’s Motors Corp.

Cash Budget

For July, August, and September

July August September

Beginning cash balance $34,000 $30,000 $30,000

Cash receipts 85,000 111,000 150,000

Total cash available 119,000 141,000 180,000

Cash disbursements (113,000) (99,900) (127,400)

Loan balance, Beg. of month $0 $24,000 $13,380

Additional loan (loan repayment) 24,000 (10,620) (13,380)

Loan balance, Month-end $24,000 $13,380 $0

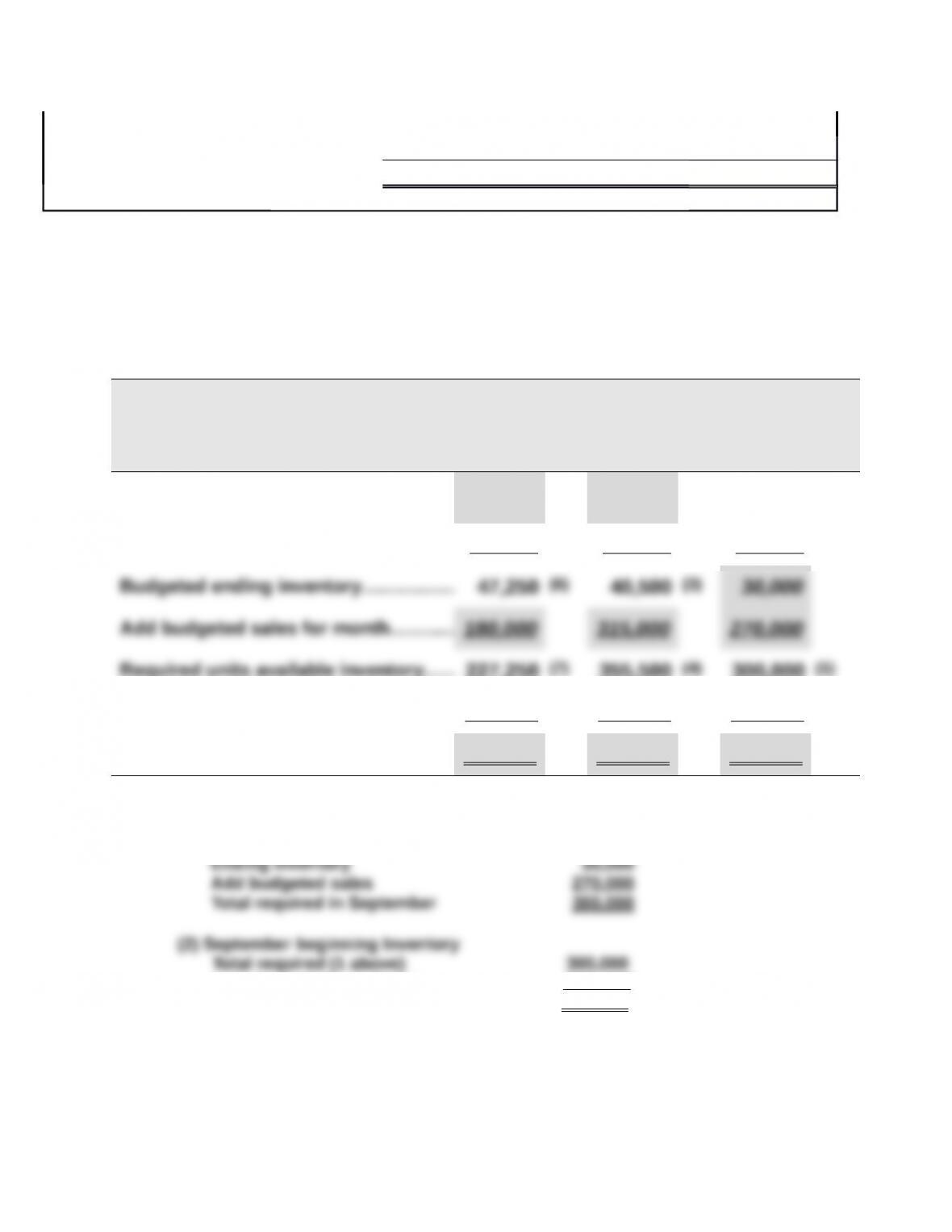

Exercise 22-23 (30 minutes)

1. Merchandise Purchases Budget

Note: Shaded numbers represent known information provided in the exercise.

Walker Company

Merchandise Purchases Budget

For July, August, and September

July August September

Next month’s budgeted sales.............. 315,000 270,000 200,000 (10)

Ratio of inventory to next month sales. x 15% (9) x 15% (9) x 15% (9)

Less beginning inventory…………….….. 27,000 (8) 47,250 (5) 40,500 (2)

Budgeted merchandise purchases..... 200,250 308,250 259,500

The following notes (1) through (10) provide supporting calculations and explanations.

Notes: (1) September required units

Less budgeted purchases (259,500)

September beginning inventory 40,500

(3) September Beginning Inventory = August Ending Inventory

(4) August required units

Ending inventory 40,500

Total required (4 above) 355,500

Less budgeted purchases (308,250)

August beginning inventory 47,250

(6) August Beginning Inventory = July Ending Inventory

(7) July required units

Less budgeted purchases (200,250)

July beginning inventory 27,000

(9) Percent of Sales to be held as Ending Inventory

Ending inventory for August

September Sales

= 40,500 = 15%

270,000

2. Monthly ending inventory is 15% of next month’s sales (see note #9).

3. October budgeted sales = 200,000 (see note #10 above).

Exercise 22-24 (25 minutes)

ACCO COMPANY

Cash Budget

For Month Ended July 31

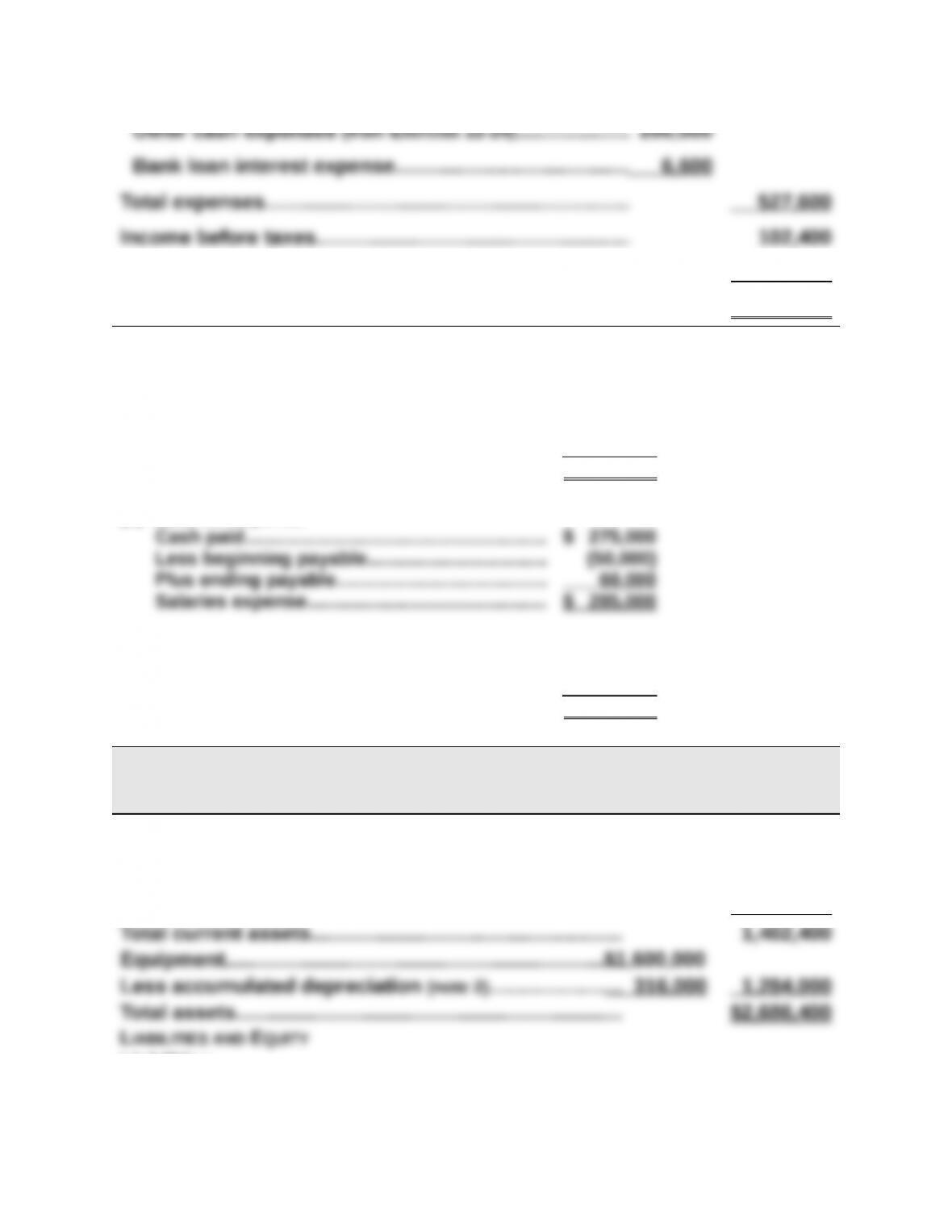

Salaries……………………………………………..…….…….…… 275,000

Other expenses…………………………………………….…….. 200,000

Accrued taxes…………………………………….…….…….….. 80,000

Interest on bank loan……………………………………….….. 6,600

Total cash disbursements………………………..….…….….. 1,291,600

Ending cash balance…………………….…….…….…….……. $ 122,400

Supporting calculations

(2) Cash disbursements in July for merchandise

For June purchases ($700,000 x 40%)……..… $ 280,000

For July purchases ($750,000 x 60%)……...... 450,000

Total………………………………….………………….….. $ 730,000

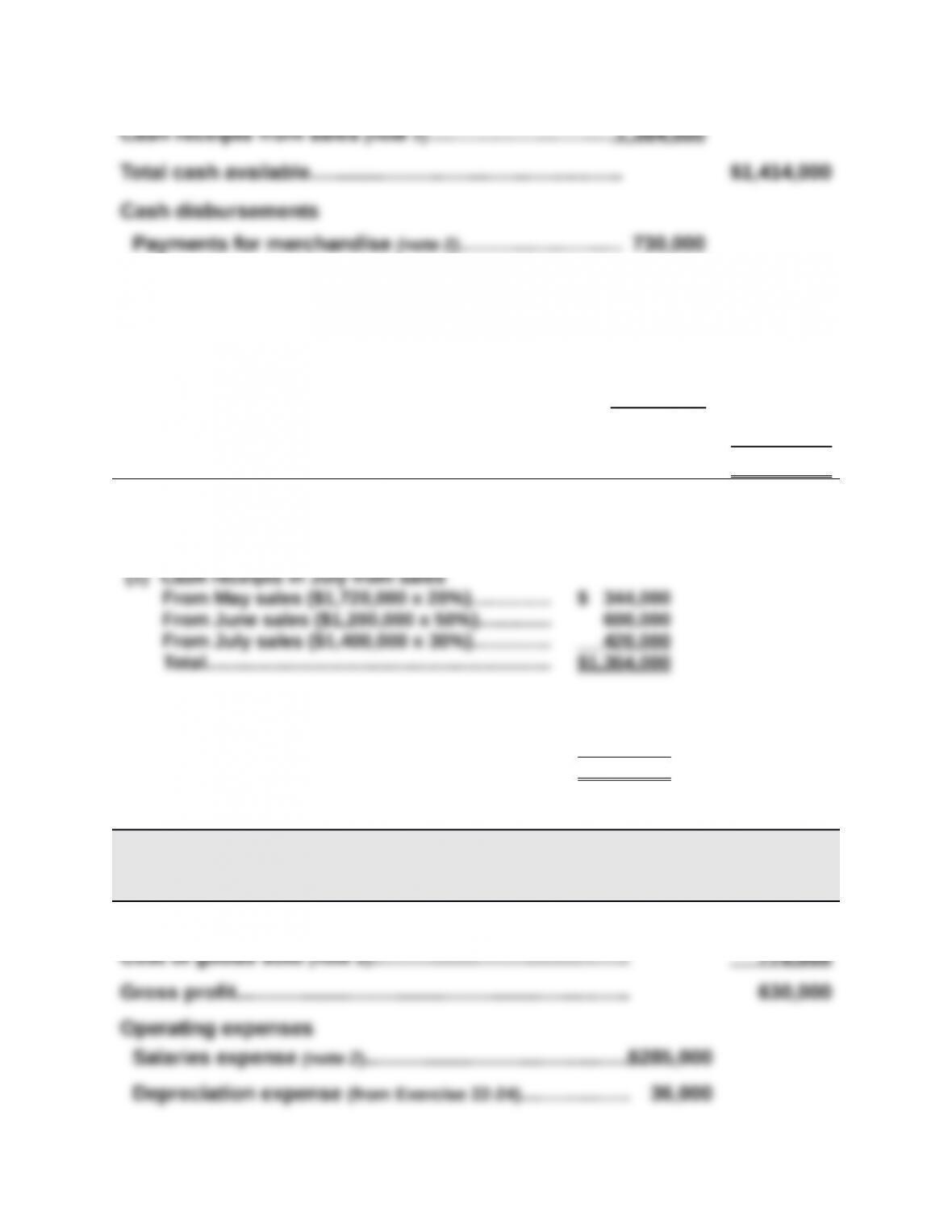

Exercise 22-25 (45 minutes)

ACCO COMPANY

Budgeted Income Statement

For Month Ended July 31

Sales (from Exercise 22-24)……………………….…….…….……. $1,400,000

Income tax expense (note 3)…………………..…….…….……. 30,720

Net income………………………………………………….…….…… $ 71,680

Supporting calculations

(1) Cost of goods sold

Sales…..………….……………………………..…..…….. $1,400,000

Cost percent…….…………………….…………………. 55%

Cost of goods sold…………..……………….…..….. $ 770,000

(2) Salaries expense

(3) Income tax expense

Pre-tax income……..………….……………………….. $ 102,400

Tax rate…………………….……………..………..…..…. 30%

Income tax expense……………….…..…..………... $ 30,720

Exercise 22-25 (Continued)

ACCO COMPANY

Budgeted Balance Sheet

As of July 31

ASSETS

Cash (from Exercise 22-24)…………………………………………. $ 122,400

Accounts receivable (note 1)…………………..…….…….….. 1,220,000

Inventory (given)………………………………………….…….…… 60,000

Liabilities

Accounts payable (note 3)……………………..…….…….….$ 300,000

Salaries payable………………………………………………….. 60,000

Income taxes payable……………………………………….…. 30,720

Total current liabilities…………………………………..….…. 390,720

Bank loan payable………………………..…….…….…….….. 660,000 1,050,720

(1) Accounts receivable

June sales (20% x $1,200,000)………………………………$ 240,000

July sales (70% x $1,400,000)……………..……..…..….. 980,000

Total……………………………………………………….….……….$ 1,220,000

(2) Accumulated depreciation

Percent unpaid……………………………………………………. 40%

Payable………………………………………………………………. $ 300,000

(4) Retained earnings

Beginning……………………………………………………….….. $ 964,000

Net income…………………………………………………………. 71,680

Exercise 22-26 (30 minutes)

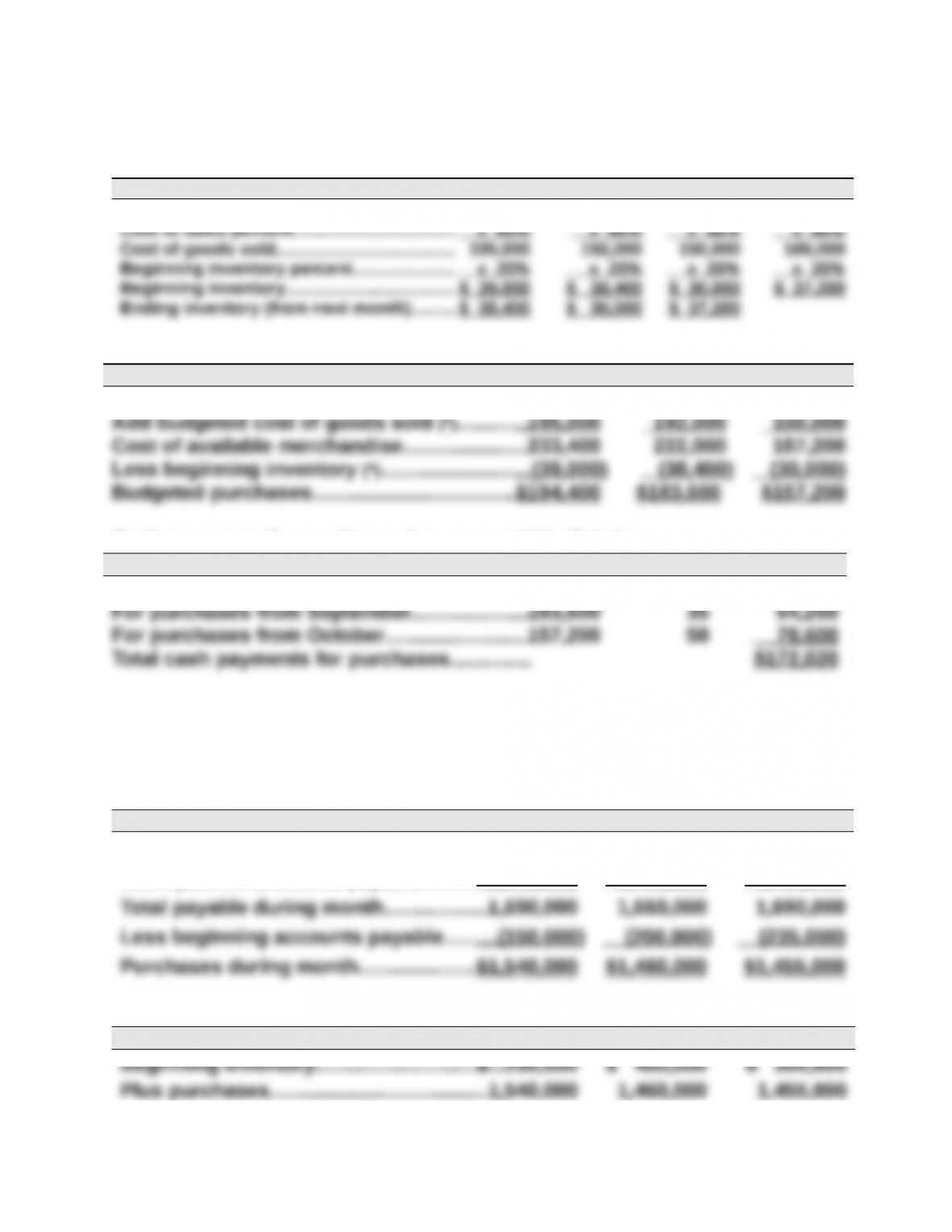

Preliminary calculations (sales, cost of sales, beginning and ending inventory)

August September October November

Sales………………………………………….….……. $325,000 $ 320,000 $250,000 $310,000

Merchandise purchases budgets (* denotes from preliminary calculations)

August September October

Budgeted ending inventory (*)……………….…..$ 38,400 $ 30,000 $ 37,200

Cash payments for purchases (on accounts) in October

Dollars Percent Paid

For purchases from August….….…….…….…..$194,400 15% $ 29,160

Exercise 22-27 (25 minutes)

1. Budgeted merchandise purchases

June July August

Ending accounts payable………………..……$ 200,000 $ 235,000 $ 195,000

Cash paid on accounts payable............... 1,490,000 1,425,000 1,495,000

2. Budgeted cost of goods sold

June July August

1.

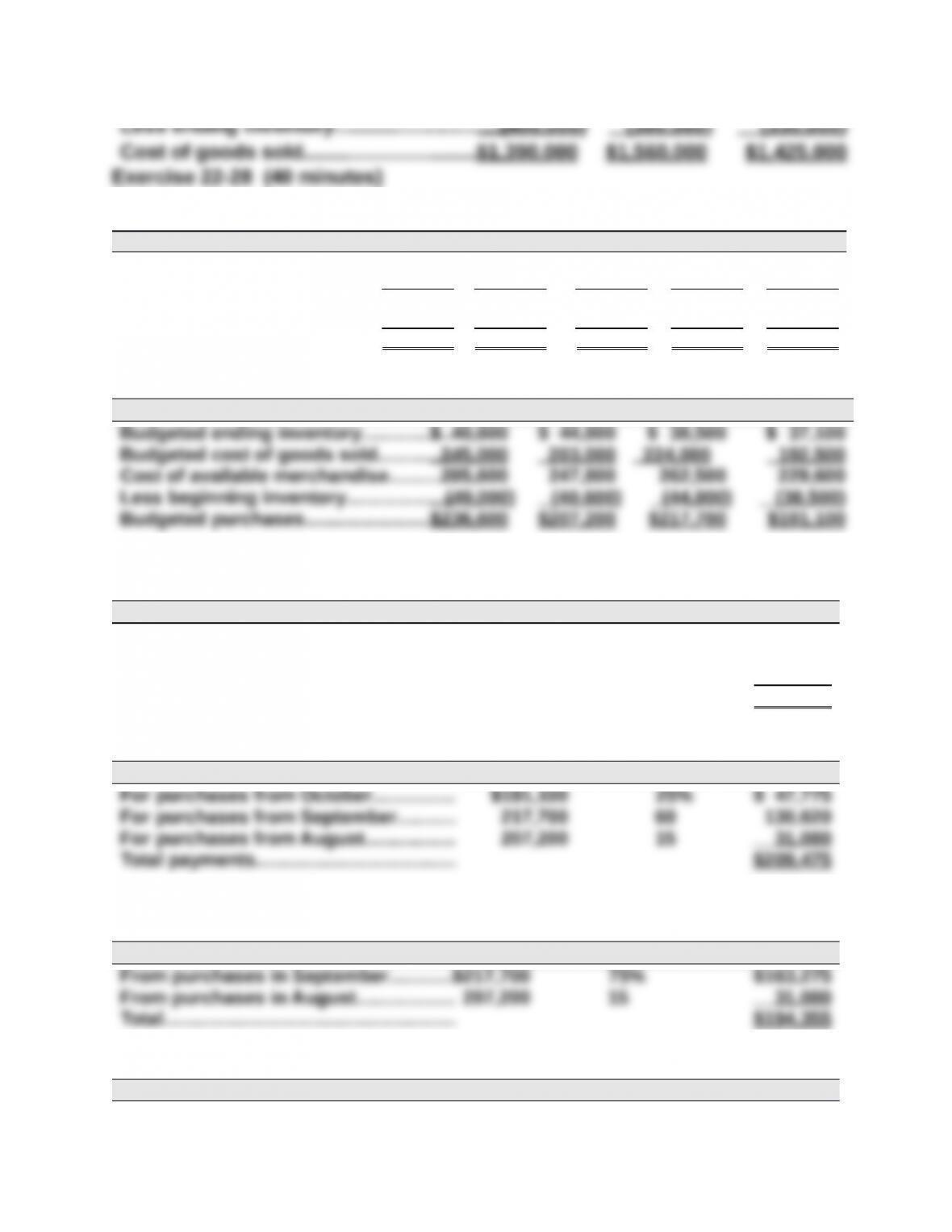

Preliminary calculations (sales, cost of sales, beginning inventory)

July August September October November

Budgeted sales…….…….......…........$350,000 $290,000 $320,000 $275,000 $265,000

Cost to sales percent…......….........x 70% x 70% x 70% x 70% x 70%

Budgeted cost of goods sold........245,000 203,000 224,000 192,500 185,500

Budgeted inventory percent..........x 20% x 20% x 20% x 20% x 20%

Budgeted beginning inventory..…....

$ 49,000 $ 40,600 $ 44,800 $ 38,500 $ 37,100

Budgeted merchandise purchases

July August September October

2.

Budgeted payments on accounts payable in September

Purchases Percent Paid Dollars Paid

For purchases from September…........ $217,700 25% $ 54,425

For purchases from August….............. 207,200 60 124,320

For purchases from July………..………… 236,600 15 35,490

Total payments…………..………….………… $214,235

Budgeted payments on accounts payable in October

Purchases Percent Paid Dollars Paid

3.

Budgeted balance of accounts payable at the end of September

Purchases Percent Unpaid Dollars Unpaid

Budgeted balance of accounts payable at the end of October

Purchases Percent Unpaid Dollars Unpaid