Chapter 22 – Master Budgets and Planning

Chapter 22

Master Budgets and Planning

QUESTIONS

1. A budget helps managers control and monitor a business by 1) communicating

plans to employees, 2) coordinating the activities of different parts of the

2. Two common benchmarks used by managers to evaluate performance are: past

3. Continuous budgeting provides managers a full set of updated budgets each time a

4. Three common short-term horizons for planning and budgeting purposes are:

monthly, quarterly, and annually. A semiannual planning horizon is also popular.

5. Budgeting can be a strong positive motivating force if employees are involved or

consulted in the process. This participation promotes their commitment to reaching

6. Budgeting helps management coordinate and plan business activities by providing

specific guidance for the individual activities of various departments and

employees.

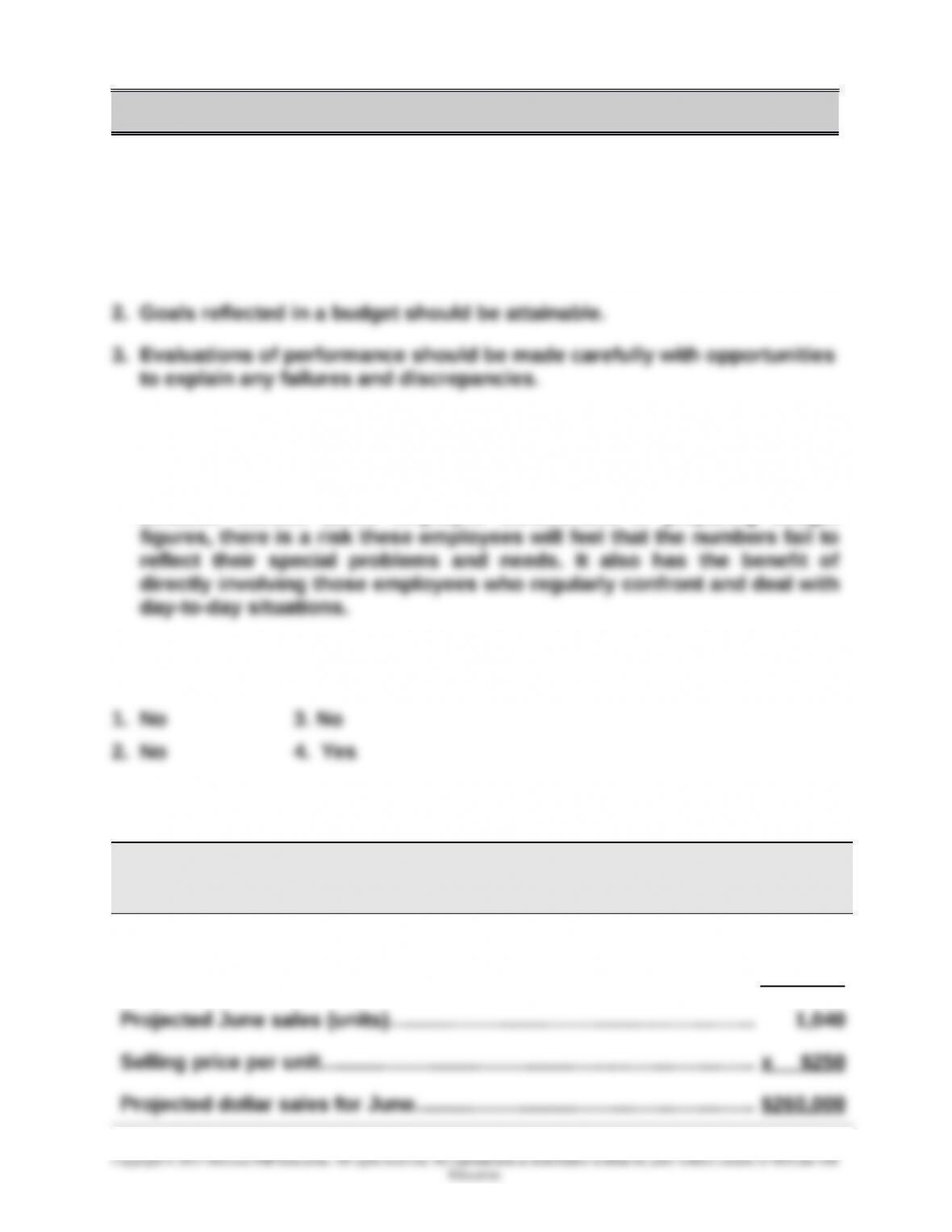

7. The sales budget reflects the expected sales to be made over a period of time, stated

8. A selling expense budget is a plan of the expenses to be incurred to produce the

22-1259

Chapter 22 – Master Budgets and Planning

9. Budgeting promotes good decision making by requiring managers to conduct

research (or analysis) and by focusing their attention on the future.

10. A cash budget shows the planned cash receipts and cash disbursements for each

budget period, including any loans to be received or repaid. Since the operating

11. A production budget shows the number of units to be produced each budget period.

12. A manager of an Apple store would have responsibility for and decision control over

budgeting for his/her store. A manager at the corporate offices may participate in,

but would not likely be involved in the budgeting for individual stores, but would

have responsibility and decision control over administrative budgets.

13. With the exception of the decision to operate, the manager of a Samsung

distribution center is not likely to engage in a substantial amount of long-term

14.

Budget Participant Description

Sales manager………............Information on estimated sales (units and dollars).

Production manager...........Number of units to produce based on estimated sales.

22-1260

Chapter 22 – Master Budgets and Planning

QUICK STUDIES

Quick Study 22-1 (10 minutes)

Three useful guidelines to help motivate employees with budgeting are

1. Employees affected by a budget should be consulted when it is prepared.

Quick Study 22-2 (10 minutes)

1. The bottom-up approach to budgeting is considered more successful

because without active employee involvement in preparing budget

Quick Study 22-3 (5 minutes)

Quick Study 22-4 (10 minutes)

Grace

Sales Budget

For Month Ended June 30

Prior month’s unit sales………………………………………………..………….... 1,000

Plus 4% growth in unit sales………………………………..………..…………... 40

22-1261

Chapter 22 – Master Budgets and Planning

Quick Study 22-5 (10 minutes)

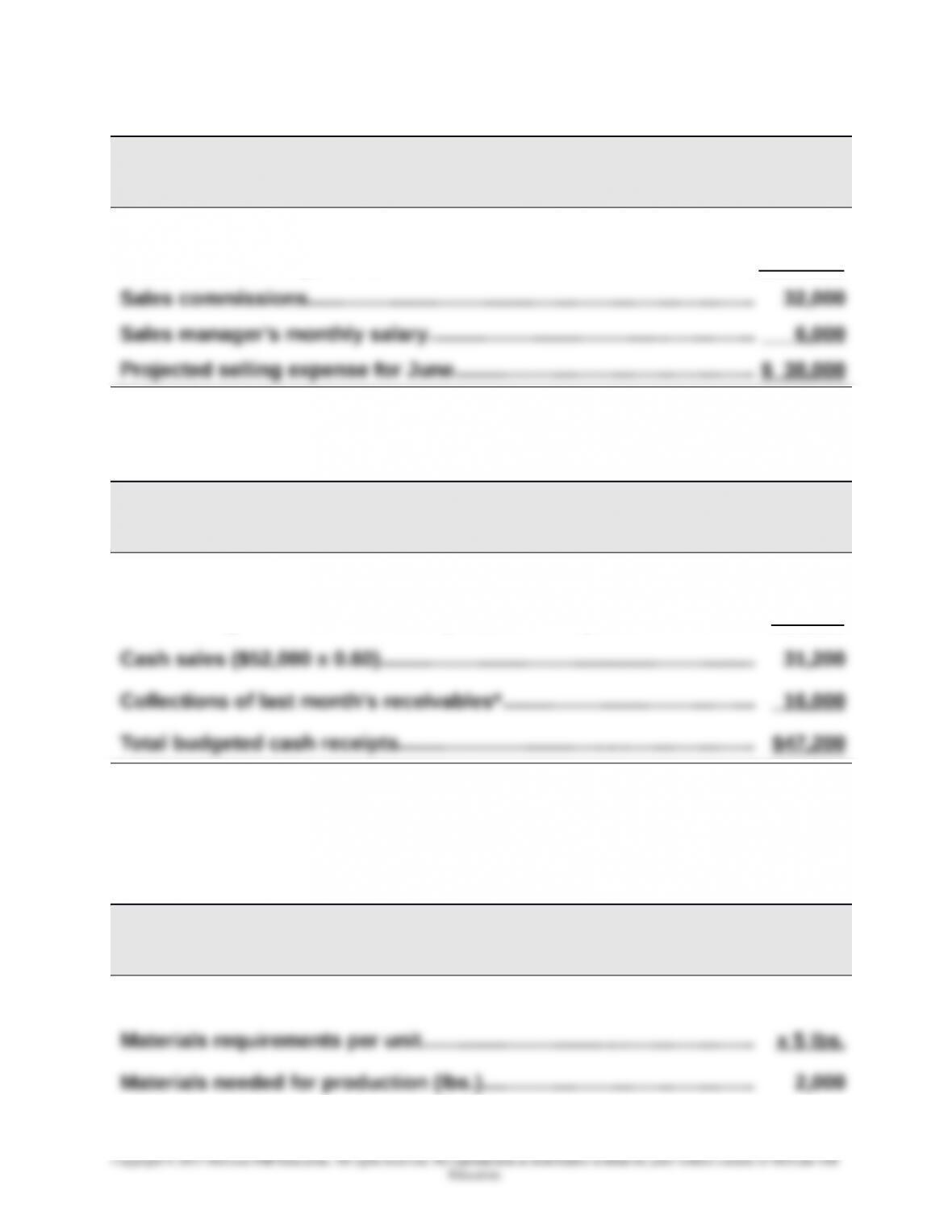

Zilly Co.

Selling Expense Budget

For Month Ended June 30

Budgeted sales…………………………………………………..………..………….... $400,000

Sales commission percent……………………………..…..…………..……….... x 8%

Quick Study 22-6 (10 minutes)

Liza’s

Budgeted Cash Receipts

For Month Ended June 30

Budgeted sales…………………………………………………..………..………….... $52,000

Less ending accounts receivable ($52,000 x 0.40)…………………..…… 20,800

*$40,000 x 40% = $16,000.

Quick Study 22-7 (10 minutes)

ZORTEK CORP.

Direct Materials Budget

For Month Ended January 31

Budget production (units)……………………………………………………….….. 400

22-1262

Chapter 22 – Master Budgets and Planning

Add budgeted ending inventory (200* units x 5 lbs. per unit x 40%).... 400

Total materials requirements (lbs.)……………………….……..…………..…. 2,400

Total cost of direct materials purchases……………………………..………. $4,540

*February’s budgeted production.

Quick Study 22-8 (5 minutes)

TORA CO.

Direct Labor Budget

For Month Ended July 31

Budget production (units)……………………………………………………….….. 1,020

Labor requirements per unit (hours)……………….………..…………..……. x 2

Quick Study 22-9 (10 minutes)

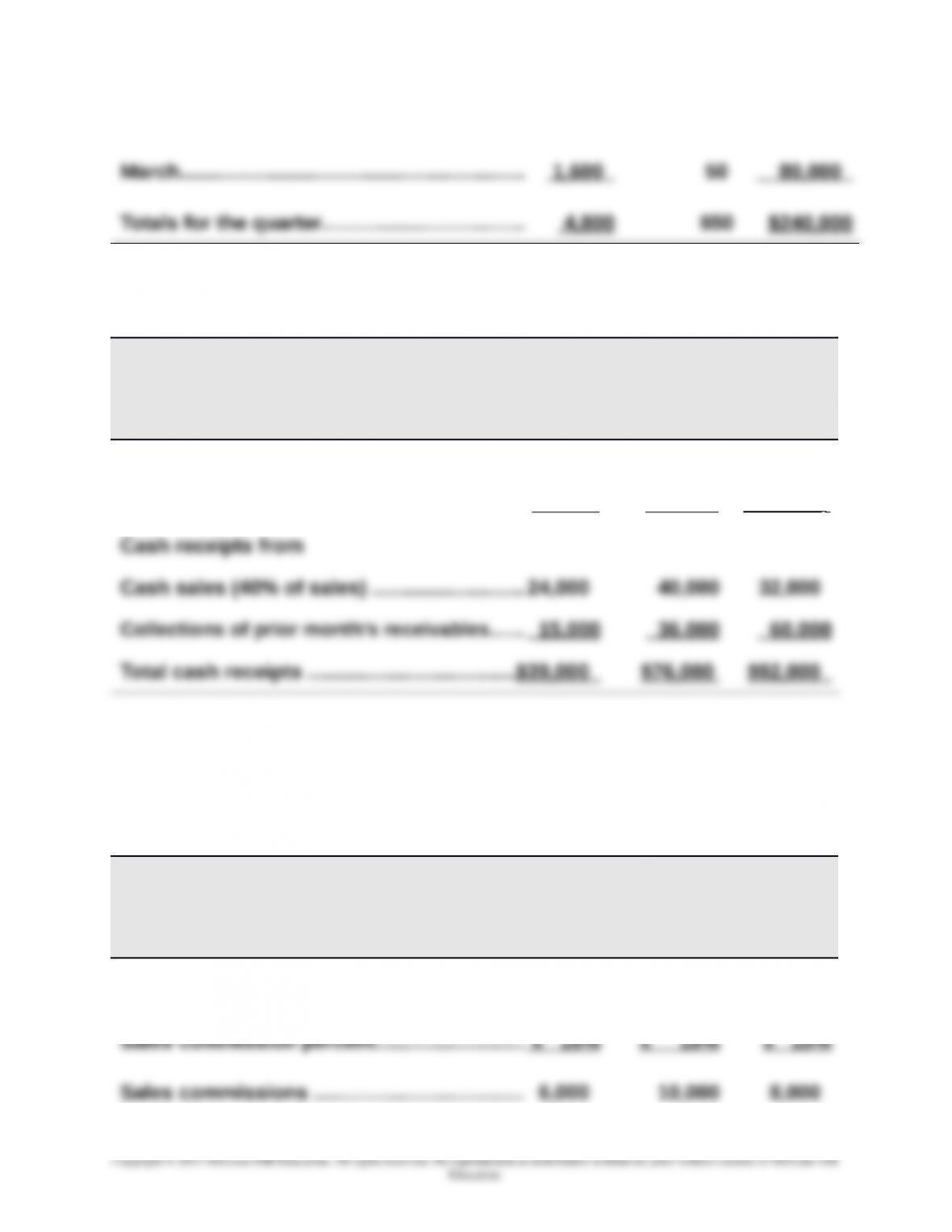

SCORA INC.

Sales Budget

For January, February, and March

Budgeted

Unit Sales

Budgeted

Unit Price

Budgeted

Total Sales

January………………………………………....……… 1,200 $50 $ 60,000

22-1263

Chapter 22 – Master Budgets and Planning

February…………………………………..………..…. 2,000 50 100,000

Quick Study 22-10 (10 minutes)

X-TEL

Cash Receipts Budget

For April, May, and June

April May June

Sales………………………………..…………..………. $60,000 $100,000 $80,000

Less ending accts. receivable (60%).......... 36,000 60,000 48,000

Quick Study 22-11 (10 minutes)

X-TEL

Selling Expense Budget

For April, May, and June

April May June

Budgeted sales………………………………..……. $60,000 $100,000 $80,000

22-1264

Chapter 22 – Master Budgets and Planning

Quick Study 22-12 (10 minutes)

CHAMP, INC.

Production Budget

For Month Ended May 31

Next month’s budgeted sales (units)……………………………….………..… 200

Ratio of inventory to future sales………………………………………………… x 60%

Budgeted ending inventory (units)………………………..…..…………..…… 120

Quick Study 22-13 (10 minutes)

MIAMI SOLAR

Direct Materials Budget

For Month Ended July 31

Budgeted production (units, given)……………………………..……..………. 5,000

Materials requirements per unit……………………………....………..……….. x 3 lbs.

Materials needed for production (lbs.)…………….…………..………..……. 15,000

Materials price per pound……………………………………………..………..….. $ 6

22-1265

Chapter 22 – Master Budgets and Planning

Total cost of direct materials purchases……………………………..………. $91,620

Quick Study 22-14 (10 minutes)

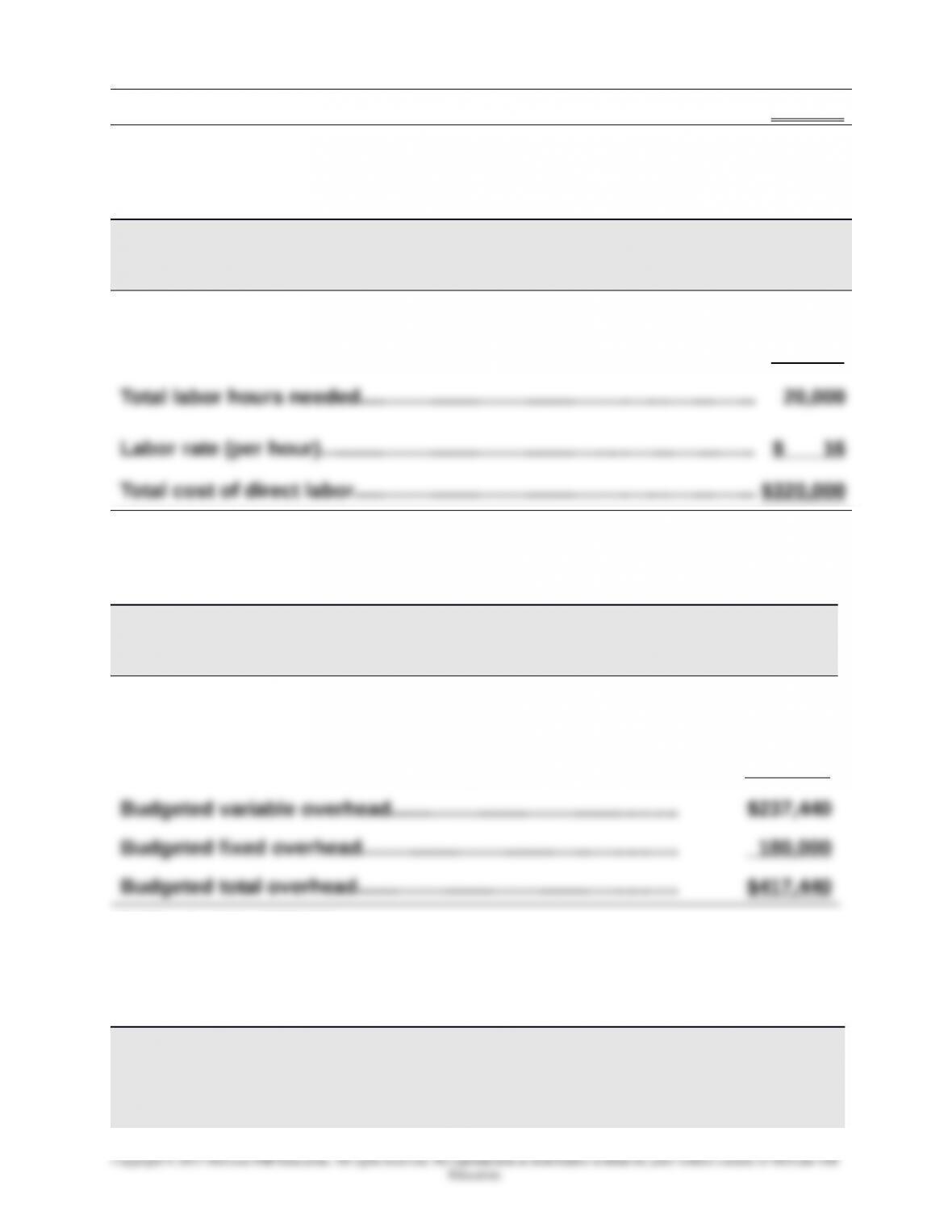

MIAMI SOLAR

Direct Labor Budget

For Month Ended July 31

Budgeted production…………………………………………..…………..………... 5,000

Labor requirements per unit (hours)……………….………..…………..……. x 4

Quick Study 22-15 (10 minutes)

MIAMI SOLAR

Factory Overhead Budget

For Month Ended August 31

Total budgeted direct labor*……………..………..…………..……… $339,200

Variable overhead rate (% of DL cost)…….………..………..…… x 70%

* 5,300 x 4 x $16 = $339,200

Quick Study 22-16 (15 minutes)

ATLANTIC SURF

Production Budget

July and August

July August

22-1266

Chapter 22 – Master Budgets and Planning

Budgeted ending inventories

July (40% x 6,500)…………………………………………..………..….. 2,600

August (40% x 3,500)……………………………………………....…… 1,400

Add budgeted sales……………………………………………….………. 4,000 6,500

Quick Study 22-17 (15 minutes)

Forrest Company

Production Budget

For Month Ended November 30

Next month’s budgeted sales……………………………………….…..………... 350,000

Ratio of inventory to future sales………………………………………………… x 10%

Budgeted ending inventory………………………………….………..………..…. 35,000

Units to be produced………………………………………………………..…..……. 395,000

Quick Study 22-18 (15 minutes)

Hockey Pro

Factory Overhead Budget

For Month Ended May 31

22-1267

Chapter 22 – Master Budgets and Planning

Units to be produced ……………………………………………………….…..……. 3,900

Variable factory overhead rate per unit……………………………..………… x $1.50

22-1268