Problem 22-6B (50 minutes)

SONY STEREO

Cash Budgets

For April, May, and June

April May June

Cash disbursements

Payments on accounts payable**…………... 80,000 188,000 186,000

Payroll………………………………….….….…….….. 16,000 17,000 18,000

Rent……………………………………..….…….….….. 6,000 6,000 6,000

Other expenses………………………….…….….… 64,000 8,000 7,000

Supporting calculations

Collections of credit sales* March April May June

March sales ($180,000)—[25%: 45%: 20%: 9%]…..…....…$ 45,000 $ 81,000 $ 36,000 $ 16,200

Payments on credit purchases** March April May June

March purchases ($100,000)—(0%: 80%: 20%)…….……....…....…....…....$ 0 $ 80,000 $ 20,000 $ –

Total……………………………………………………………………………….…….………$ 0 $ 80,000 $188,000 $186,000

Problem 22-7B (70 minutes)

Part 1

Cash collections of credit sales (accounts receivable)

From sales in Total % Collected March April

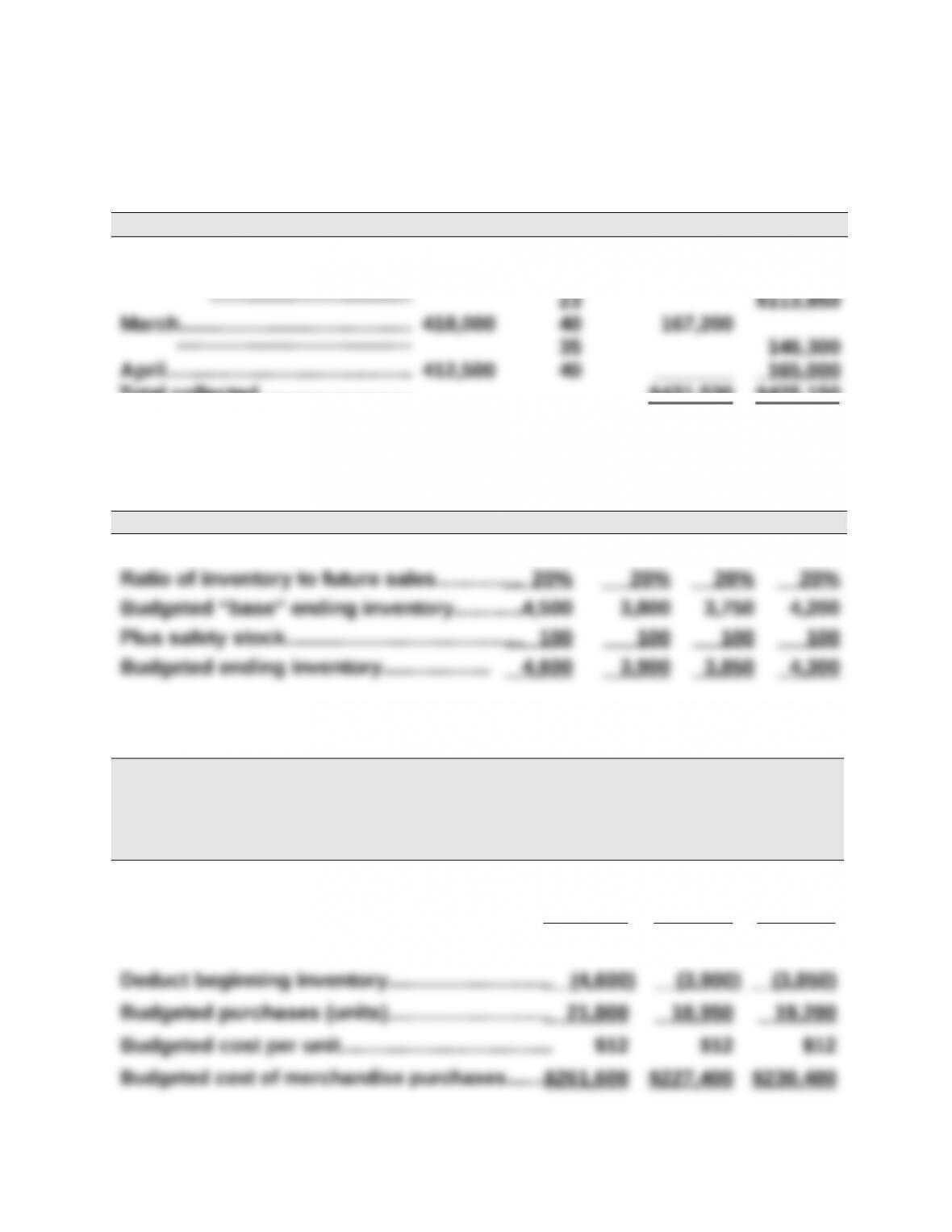

January………………………………..$396,000 23% $ 91,080

February…………..….….…….….… 495,000 35 173,250

Total collected………..…….……... $431,530 $425,150

Part 2

Budgeted ending inventories (in units)

January February March April

Next month’s budgeted sales……………..…..22,500 19,000 18,750 21,000

Problem 22-7B (Continued)

Part 4

Cash payments on product purchases (for March and April)

From purchases in Total % Paid March April

February……………………………..….$261,600 70% $183,120

March…………………………………….. 227,400 30 68,220

Part 5

CONNICK COMPANY

Cash Budget

March and April

March April

Beginning cash balance…………………………………………….…...$ 50,000 $ 58,070

431,530 425,150

Total available cash…………………………….….….…….….…….…..

Cash disbursements

Payments on purchases…………………..…….….…….…….….…251,340 228,300

Selling and administrative expenses……………………..……...160,000 160,000

Interest expense*…………………………………………….…….….….

120 0

411,460 388,300

*Interest expense: March = $12,000 x 12% /12 = $120

Part 6

Analysis Component: Information about the supply of cash in the near future

would be helpful to the management of Connick Company. A good cash

Problem 22-8B (130 minutes)

Part 1

ISLE CORPORATION

Sales Budgets

January, February, and March 2016

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

January 2016…………………………………….….…….. 6,000 $45 $ 270,000

Part 2

ISLE CORPORATION

Merchandise Purchases Budgets

January, February, and March 2016

January February March Total

Next month’s budgeted sales……………. 8,000 10,000 9,000

Ratio of inventory to future sales......... x 25% x 25% x 25%

Budgeted cost per unit….…..………........ $ 30 $ 30 $ 30 $ 30

Budgeted merchandise purchases

…….

$90,000 $255,000 $292,500 $637,500

Part 3

ISLE CORPORATION

Selling Expense Budgets

January, February, and March 2016

January February March Total

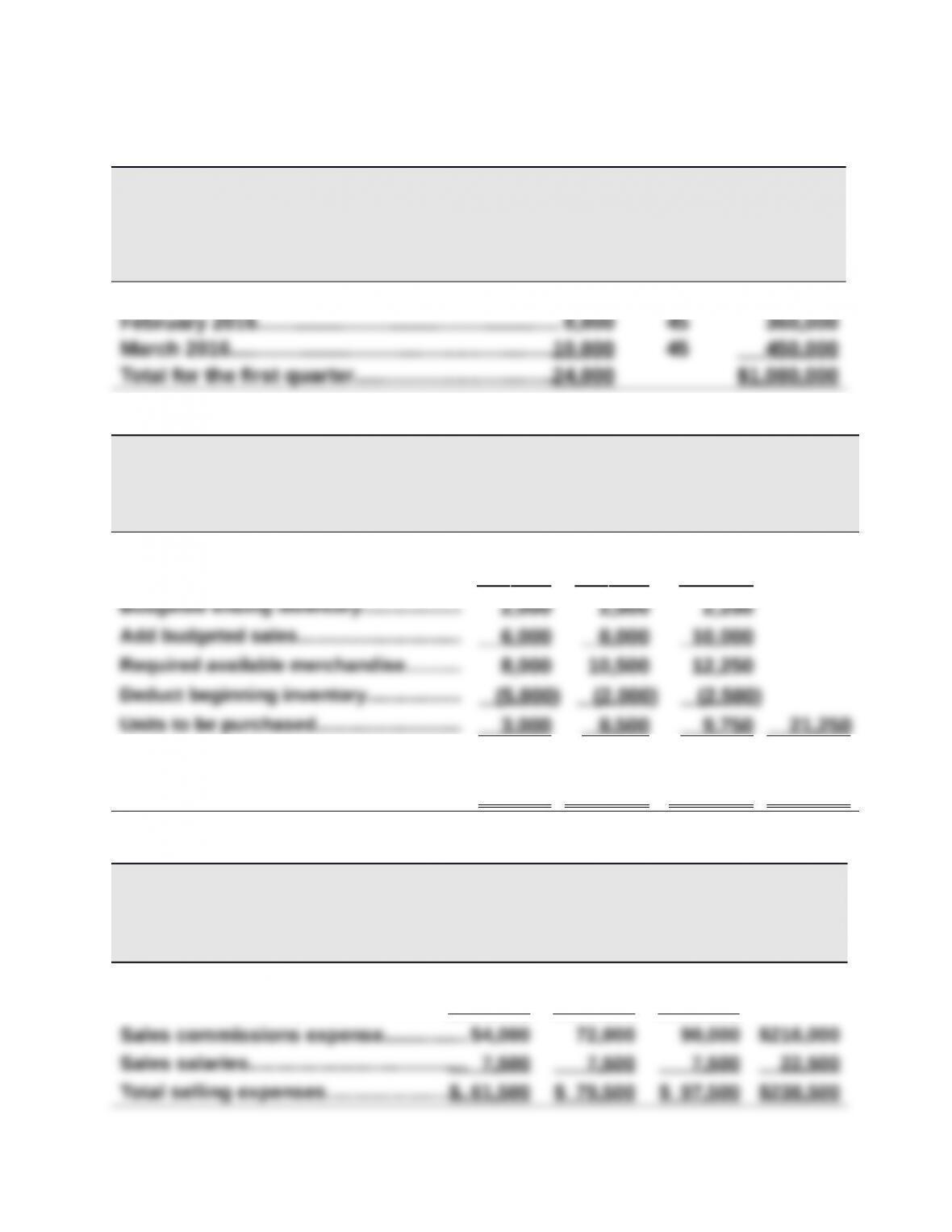

Budgeted sales………..…..……..……..…..$270,000 $360,000 $450,000

Sales commission percent..................x 20% x 20% x 20%

Problem 22-8B (Continued)

Part 4

ISLE CORPORATION

General and Administrative Expense Budgets

January, February, and March 2016

January February March Total

Salaries……………………..…….….…….….…….$12,000 $12,000 $12,000 $36,000

Maintenance………………….….…….….…….…3,000 3,000 3,000 9,000

* Depreciation expense calculations

Annual

Amount January February March Total

Equipment owned

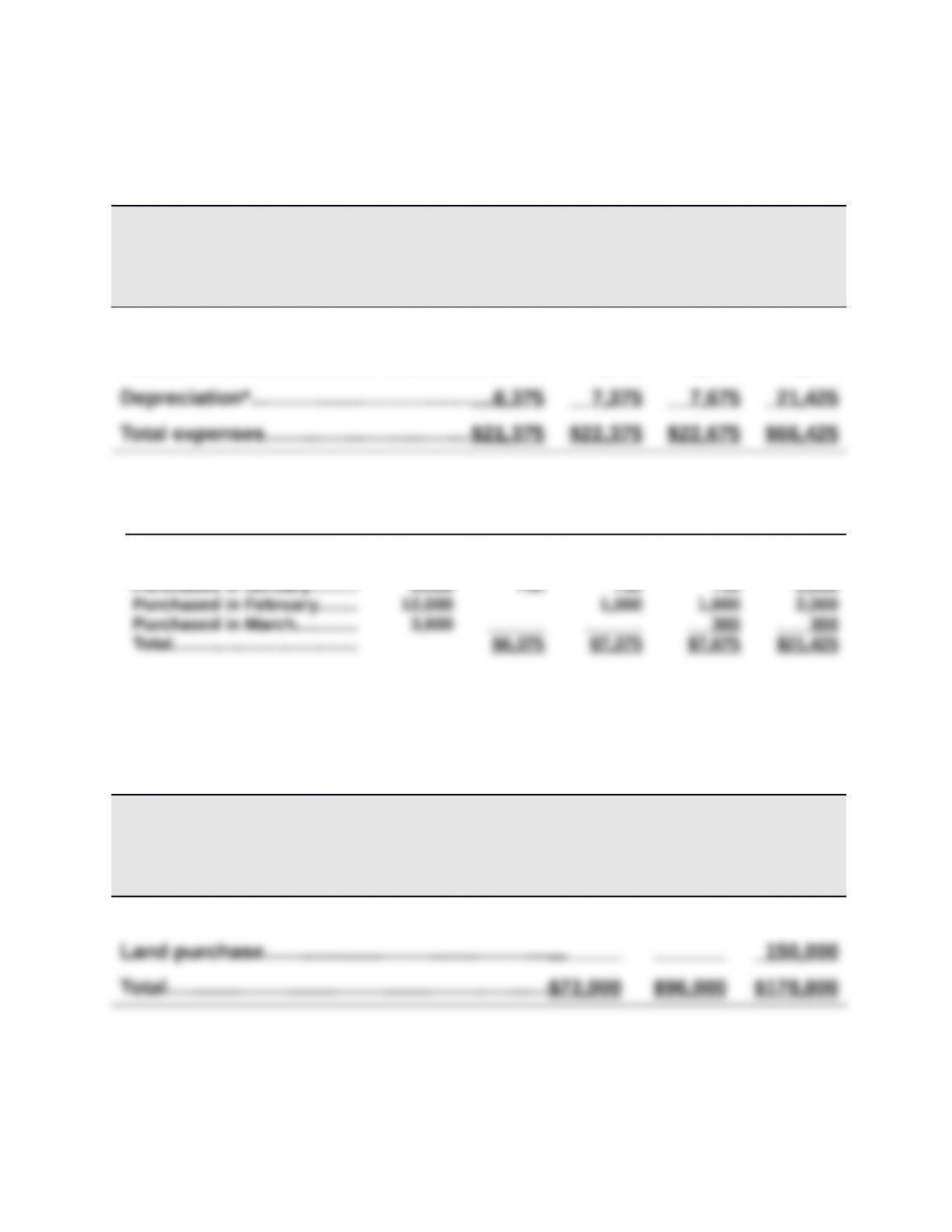

on 12/31/2015....…....…....... $67,500 $5,625 $5,625 $5,625 $16,875

Part 5

ISLE CORPORATION

Capital Expenditures Budgets

January, February, and March 2016

January February March

Equipment purchases……………………………………$72,000 $96,000 $ 28,800

Problem 22-8B (Continued)

Part 6

ISLE CORPORATION

Cash Budgets

January, February, and March 2016

January February March

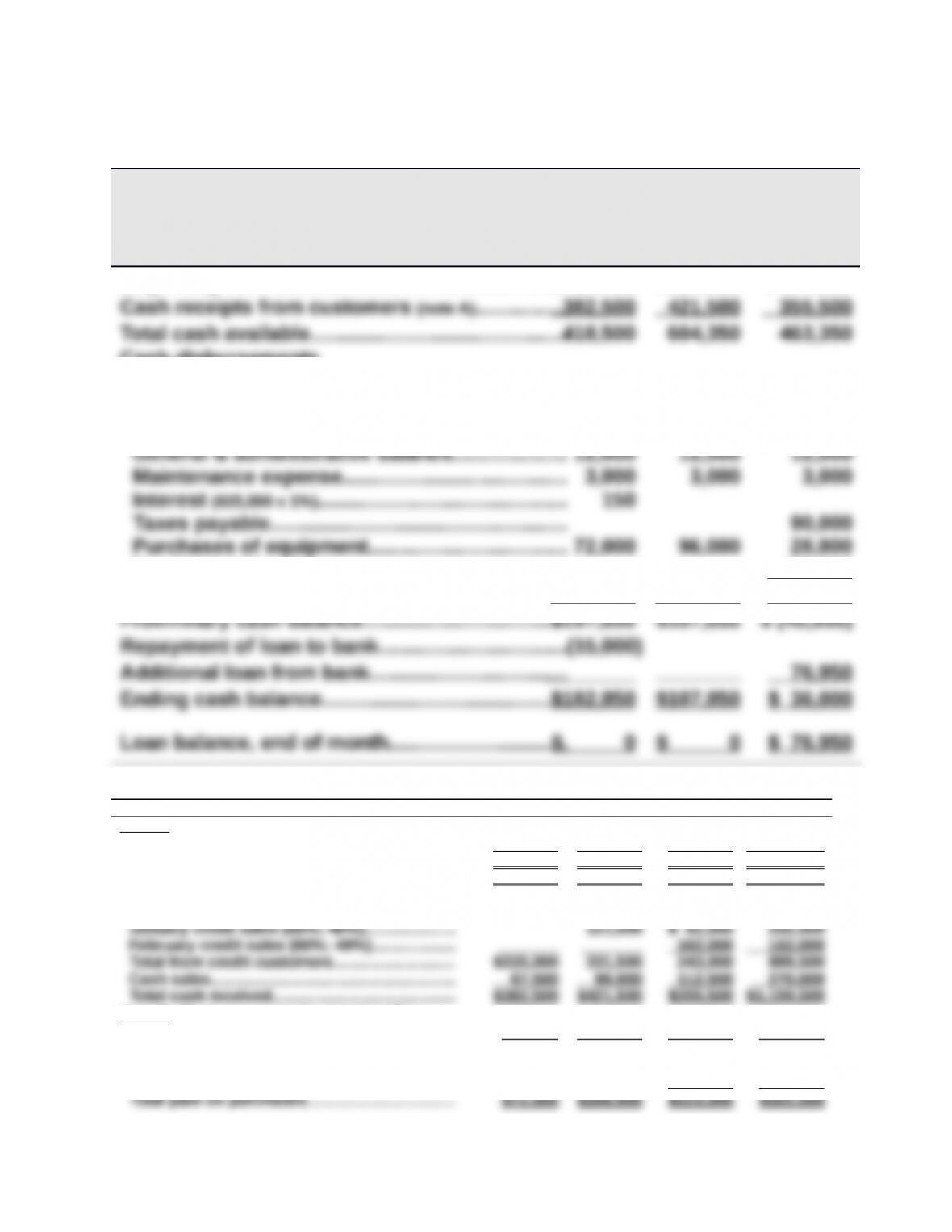

Beginning cash balance…………….…….….…….…. $ 36,000 $182,850 $ 107,850

Cash disbursements

Payments for merchandise (note B)……………….. 72,000 306,000 123,000

Sales commissions………………………………..…… 54,000 72,000 90,000

Sales salaries…………………….…….….…….….…… 7,500 7,500 7,500

Purchase of land…………………………….….…….…

________ ________ 150,000

Total cash disbursements………..…….….…….…... 220,650 496,500 504,300

Supporting calculations January February March Total

Note A: Cash receipts from customers

Total sales……..…………….………..………..………. $270,000 $360,000 $450,000 $1,080,000

Cash sales (25%)……………..…..………..………... $ 67,500 $ 90,000 $112,500 $ 270,000

Credit sales (75%)…………..……………..….……... $202,500 $270,000 $337,500 $ 810,000

Cash collections

Receivables at 12/31/2015 (60%; 40%)…........ $315,000 $210,000 $ 525,000

Note B: Cash payments for merchandise

Credit purchases…………….…………..………..…. $90,000 $255,000 $292,500 $637,500

Accounts payable at 12/31/2015 (20%; 80%). $72,000 $288,000 $360,000

January purchases (20%; 80%)…………..…….. 18,000 $72,000 90,000

February purchases (20%)…………………..……. _______ _______ 51,000 51,000

Problem 22-8B (Continued)

Part 7

ISLE CORPORATION

Budgeted Income Statement

For Three Months Ended March 31, 2016

Sales…………………………………………………………………….. $1,080,000

Cost of goods sold (24,000 units @ $30)…….…….….… 720,000

Gross profit…………………………………………………………... 360,000

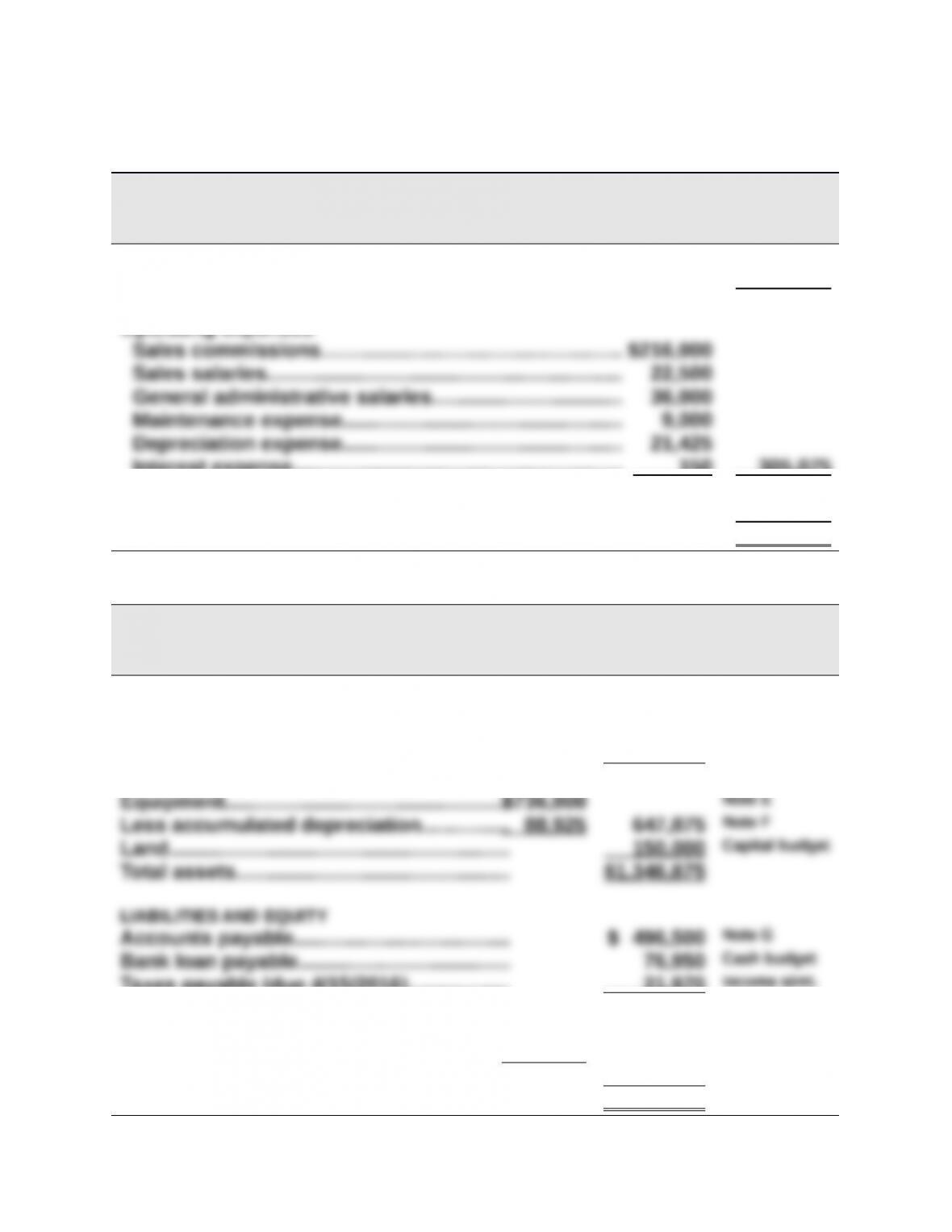

Operating expenses

Interest expense…………………….…….….…….….…….…. 150 305,075

Income before taxes……………………..….….…….….……... 54,925

Income taxes (40%)…………………………………………..…... 21,970

Net income……………………………………………………..….…. $ 32,955

Part 8

ISLE CORPORATION

Budgeted Balance Sheet

March 31, 2016

ASSETS

Cash…………………………….…….….…….….…. $ 36,000 Cash budget

Accounts receivable…………..…….….……... 445,500 Note C

Inventory………………………………..….…….…. 67,500 Note D

Total current assets……………….….…….….. 549,000

Taxes payable (due 4/15/2016)……..…….… 21,970 Income stmt.

Total liabilities.…..……………………………….. 595,420

Common stock………………….…….….…….…$472,500 Unchanged

Retained earnings……………………….…….… 278,955 Note H

Total stockholders’ equity………….…….….. 751,455

Total liabilities and equity..….….……......... $1,346,875

Problem 22-8B (Concluded)

Supporting Footnotes

Note C

Beginning receivables…………………………………………………….…..$ 525,000

Credit sales………………………………………………………………………… 810,000

Less collections……………………………………………………….………... (889,500)

Ending receivables…….……..……..…….……..…..…....…....…....…....$ 445,500

Note F

Beginning accumulated depreciation…………………………………...$ 67,500

Depreciation expense…………………………………………….…….…….. 21,425

Total……………………………………………………………………………………$ 88,925

Note G

Beginning accounts payable………………………………………………..$ 360,000

Purchases…………………………………………………………………….….… 637,500

Payments………………………………………………………………..….……... (501,000)

Ending accounts payable…………………………………………..…….….$ 496,500

Note H