Problem 22-6B (50 minutes)

SONY STEREO

Cash Budgets

For April, May, and June

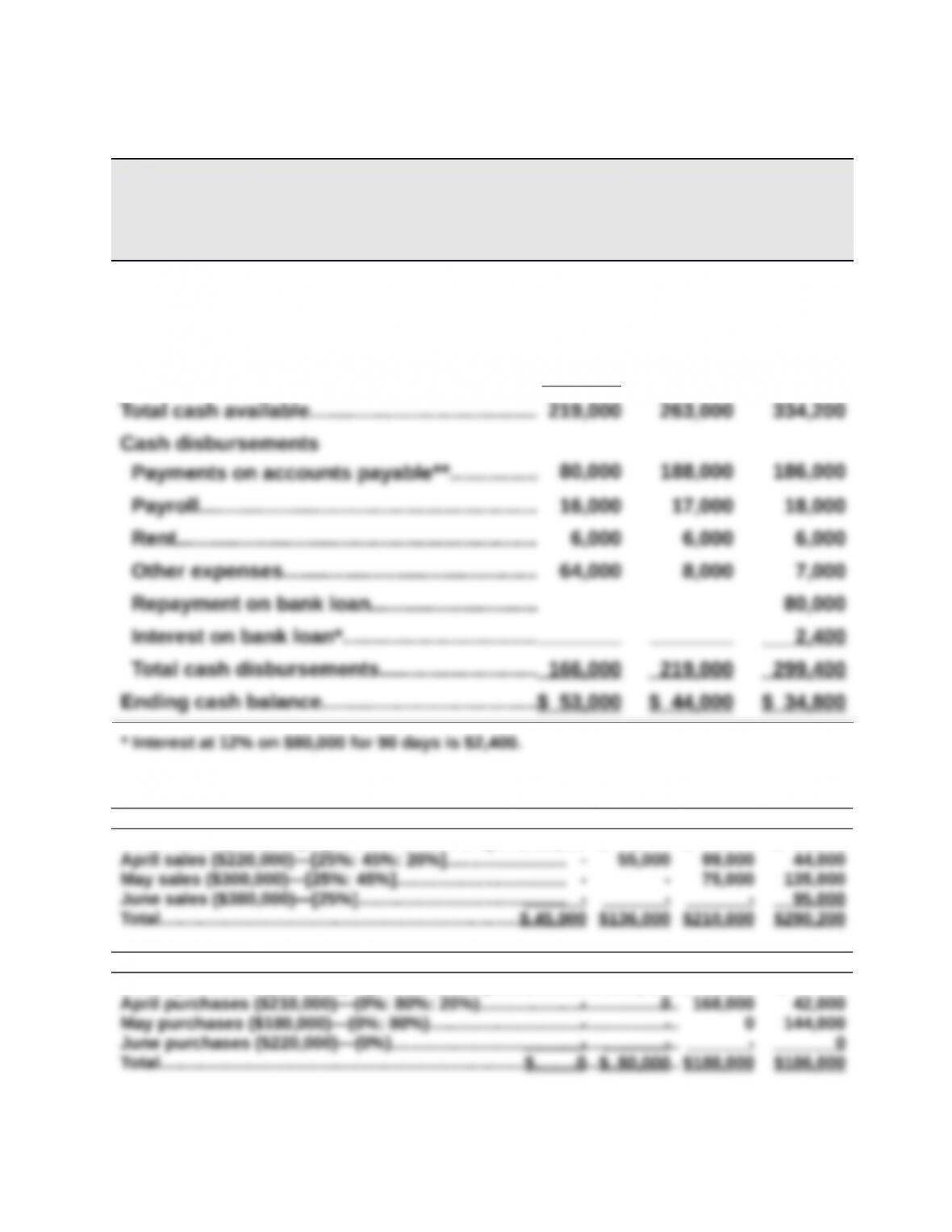

April May June

Beginning balance………………………………….. $ 3,000 $ 53,000 $ 44,000

Cash receipts

Collection on accounts receivable*………… 136,000 210,000 290,200

Receipts from bank loan……………………….. 80,000 _______ _______

Supporting calculations

Collections of credit sales* March April May June

March sales ($180,000)—[25%: 45%: 20%: 9%]……………$ 45,000 $ 81,000 $ 36,000 $ 16,200

Payments on credit purchases** March April May June

March purchases ($100,000)—(0%: 80%: 20%)………………………………….$ 0 $ 80,000 $ 20,000 $ –

Problem 22-7B (70 minutes)

Part 1

Cash collections of credit sales (accounts receivable)

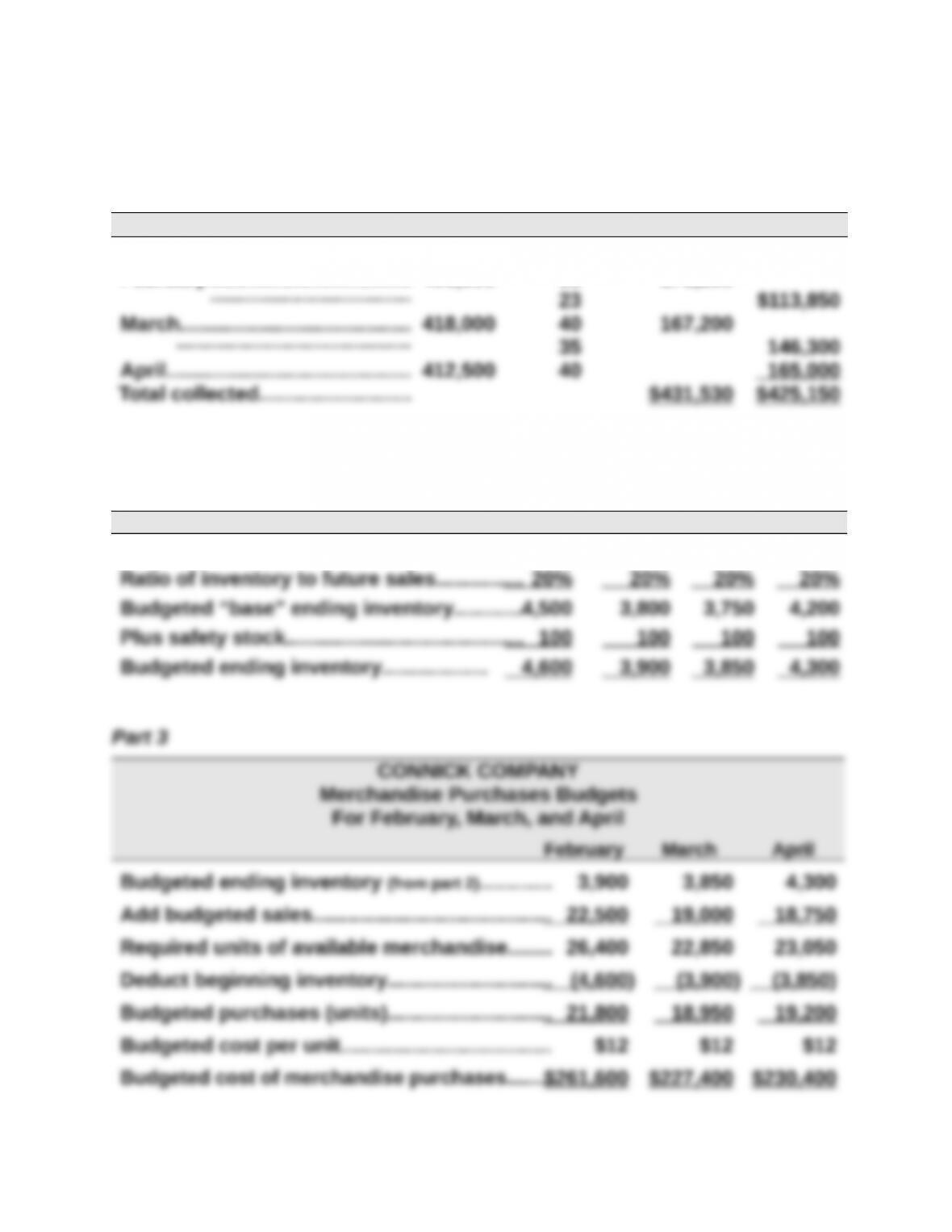

From sales in Total % Collected March April

January……………………………….$396,000 23% $ 91,080

February…………………………….. 495,000 35 173,250

Part 2

Budgeted ending inventories (in units)

January February March April

Next month’s budgeted sales…………………22,500 19,000 18,750 21,000

Problem 22-7B (Continued)

Part 4

Cash payments on product purchases (for March and April)

From purchases in Total % Paid March April

February………………………………..$261,600 70% $183,120

Part 5

CONNICK COMPANY

Cash Budget

March and April

March April

Beginning cash balance………………………………………………..$ 50,000 $ 58,070

Cash receipts from customers……………………………………….

431,530 425,150

Total available cash……………………………………………………….

481,530 483,220

Cash disbursements

Part 6

Analysis Component: Information about the supply of cash in the near future

would be helpful to the management of Connick Company. A good cash

Problem 22-8B (130 minutes)

Part 1

ISLE CORPORATION

Sales Budgets

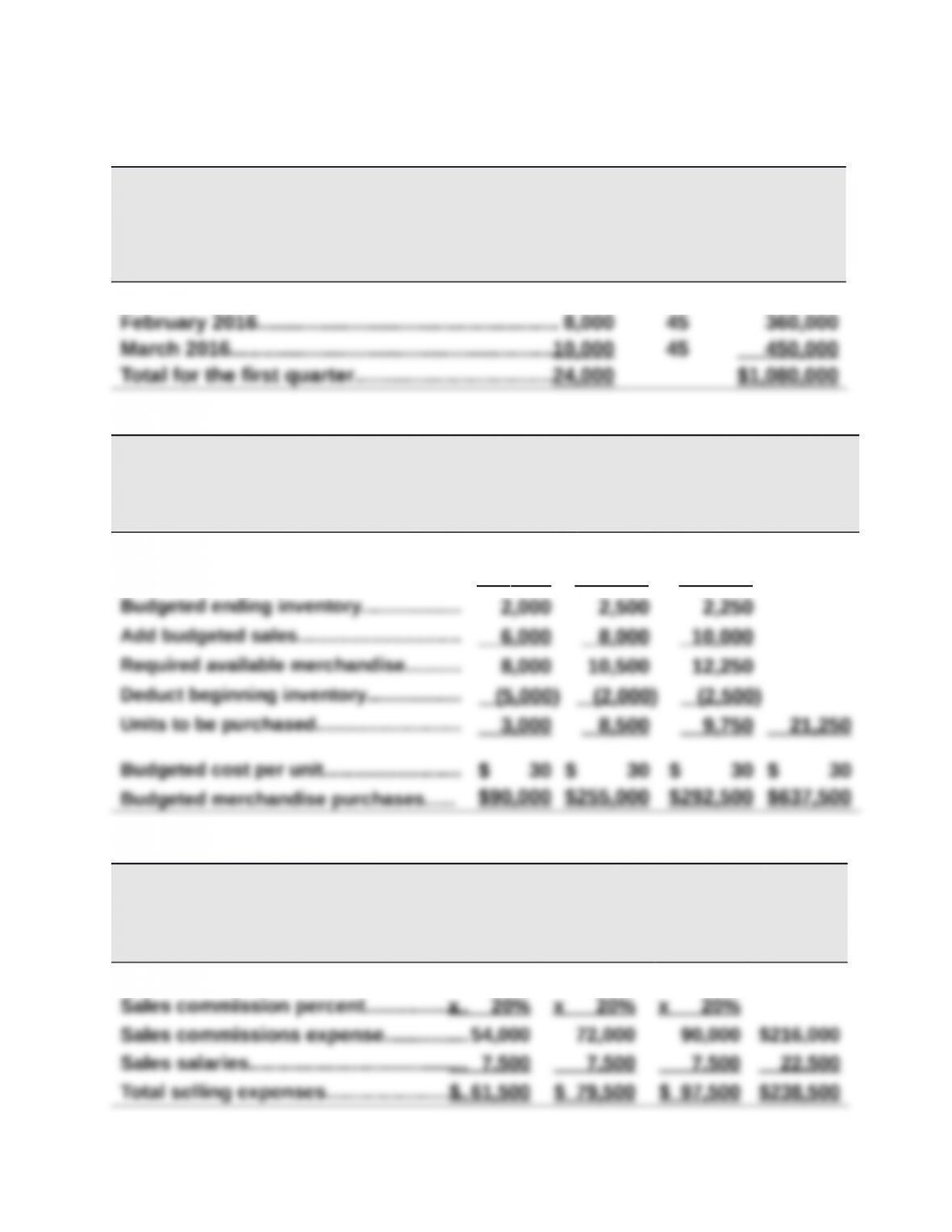

January, February, and March 2016

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

January 2016……………………………………………… 6,000 $45 $ 270,000

Part 2

ISLE CORPORATION

Merchandise Purchases Budgets

January, February, and March 2016

January February March Total

Next month’s budgeted sales…………… 8,000 10,000 9,000

Ratio of inventory to future sales……… x 25% x 25% x 25%

Part 3

ISLE CORPORATION

Selling Expense Budgets

January, February, and March 2016

January February March Total

Budgeted sales……………………………….$270,000 $360,000 $450,000

Problem 22-8B (Continued)

Part 4

ISLE CORPORATION

General and Administrative Expense Budgets

January, February, and March 2016

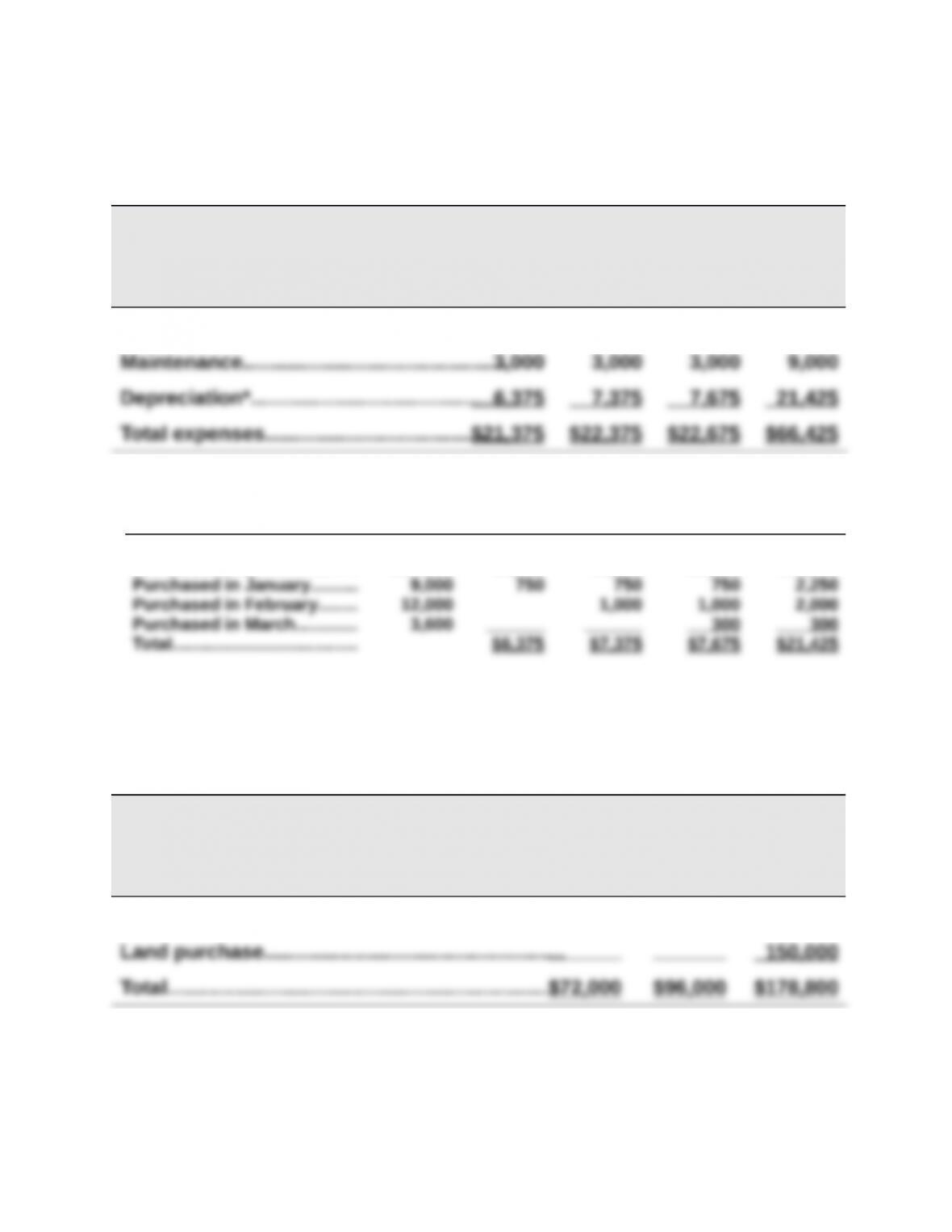

January February March Total

Salaries………………………………………………$12,000 $12,000 $12,000 $36,000

* Depreciation expense calculations

Annual

Amount January February March Total

Equipment owned

on 12/31/2015…………………. $67,500 $5,625 $5,625 $5,625 $16,875

Part 5

ISLE CORPORATION

Capital Expenditures Budgets

January, February, and March 2016

January February March

Equipment purchases………………………………….$72,000 $96,000 $ 28,800

Problem 22-8B (Continued)

Part 6

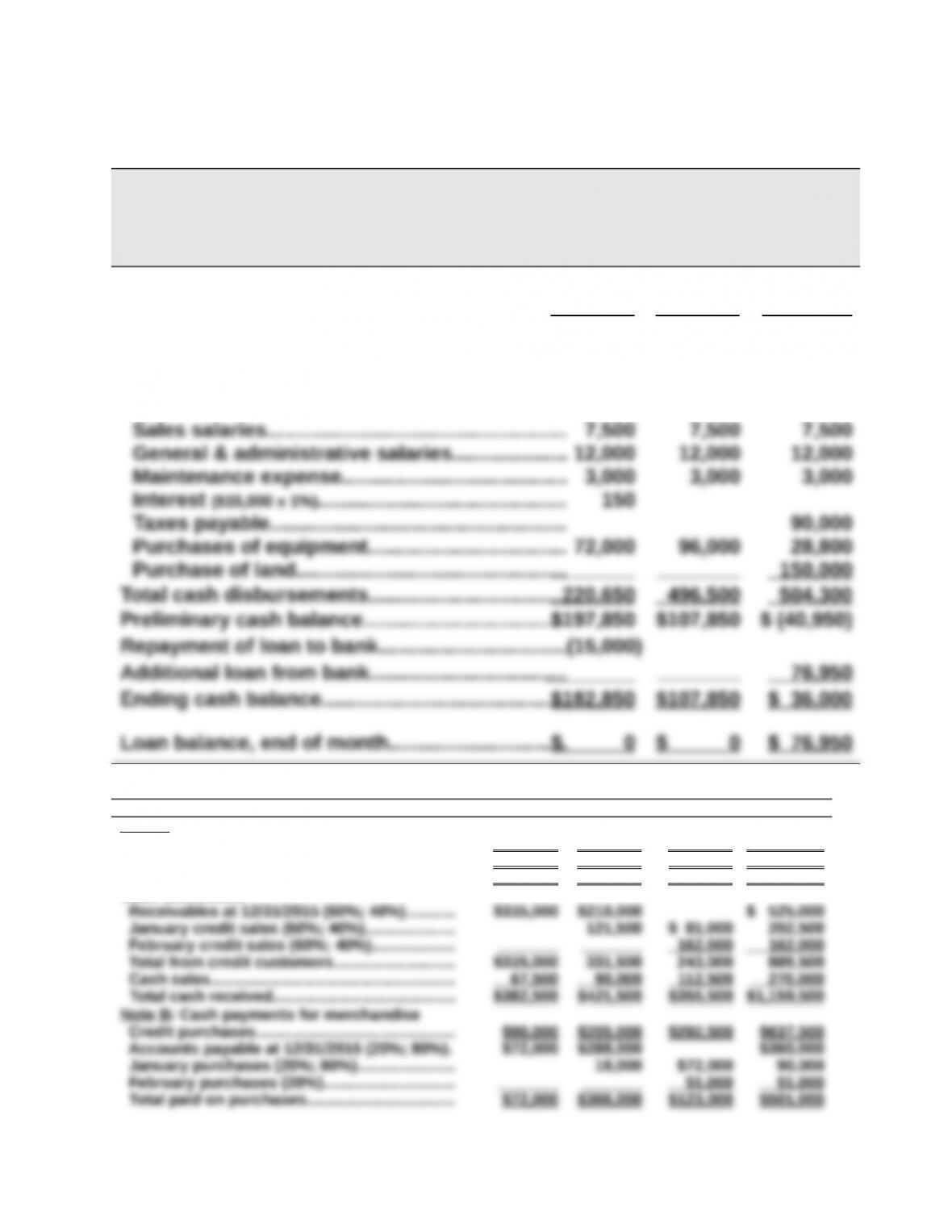

ISLE CORPORATION

Cash Budgets

January, February, and March 2016

January February March

Beginning cash balance………………………………. $ 36,000 $182,850 $ 107,850

Cash receipts from customers (note A)……………. 382,500 421,500 355,500

Total cash available……………………………………..418,500 604,350 463,350

Cash disbursements

Payments for merchandise (note B)………………. 72,000 306,000 123,000

Sales commissions……………………………………. 54,000 72,000 90,000

Supporting calculations January February March Total

Note A: Cash receipts from customers

Total sales……………………………………………….. $270,000 $360,000 $450,000 $1,080,000

Cash sales (25%)……………………………………… $ 67,500 $ 90,000 $112,500 $ 270,000

Credit sales (75%)…………………………………….. $202,500 $270,000 $337,500 $ 810,000

Cash collections

Problem 22-8B (Continued)

Part 7

ISLE CORPORATION

Budgeted Income Statement

For Three Months Ended March 31, 2016

Sales…………………………………………………………………… $1,080,000

Cost of goods sold (24,000 units @ $30)……………….. 720,000

Gross profit…………………………………………………………. 360,000

Operating expenses

Part 8

ISLE CORPORATION

Budgeted Balance Sheet

March 31, 2016

ASSETS

Cash………………………………………………….. $ 36,000 Cash budget

Accounts receivable…………………………… 445,500 Note C

Inventory……………………………………………. 67,500 Note D

Total current assets……………………………. 549,000

Problem 22-8B (Concluded)

Supporting Footnotes

Note C

Beginning receivables…………………………………………………………..$ 525,000

Note D

Beginning inventory………………………………………………………………$ 150,000

Note E

Beginning equipment…………………………………………………………….$ 540,000

Note F

Beginning accumulated depreciation…………………………………….$ 67,500

Note G

Beginning accounts payable…………………………………………………$ 360,000

Note H

Beginning retained earnings………………………………………………….$ 246,000