Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 22-3B (50 minutes)

Part 1

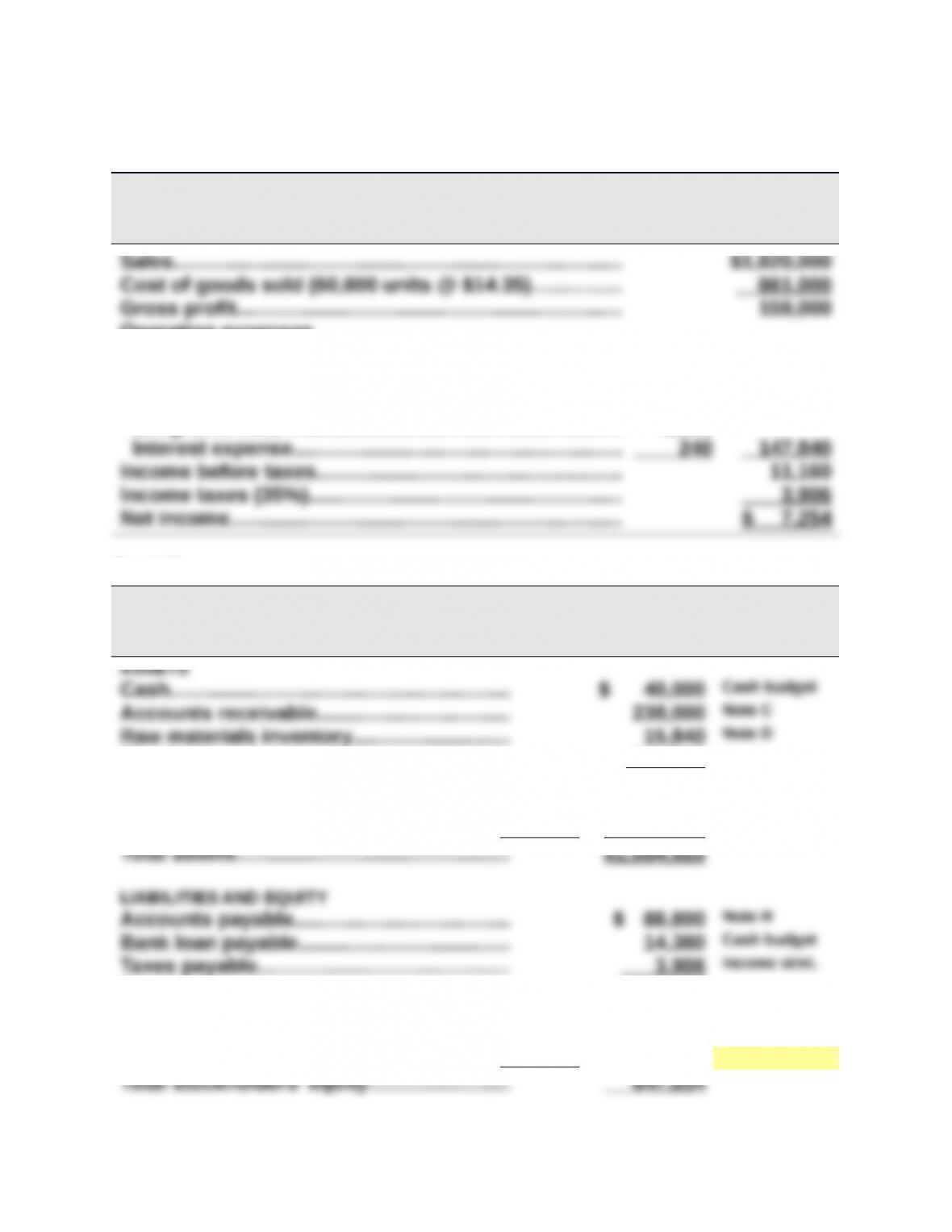

HCS MFG.

Budgeted Income Statement

For Months of July, August, and September, 2015

Sales commissions (10%)...................... 126,500 139,150 153,065

Advertising ($200,000 x 1.25)................ 250,000 250,000 250,000

Store rent................................................. 24,000 24,000 24,000

Administrative salaries.......................... 40,000 40,000 40,000

Depreciation-Office equipment............. 50,000 50,000 50,000

Units (@ $115) Sold (@ $60)

June ($1,300,000/$130)...............................10,000

July..............................................................11,000 $1,265,000 $660,000

August.........................................................12,100 1,391,500 726,000

September...................................................13,310 1,530,650 798,600

Part 2: Analysis Component

The plan for increasing sales volume by reducing the price and increasing

advertising would cause the company to generate less net income in each of the

Problem 22-4B (130 minutes)

Part 1

NABAR MANUFACTURING

Sales Budgets

July, August, and September 2015

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

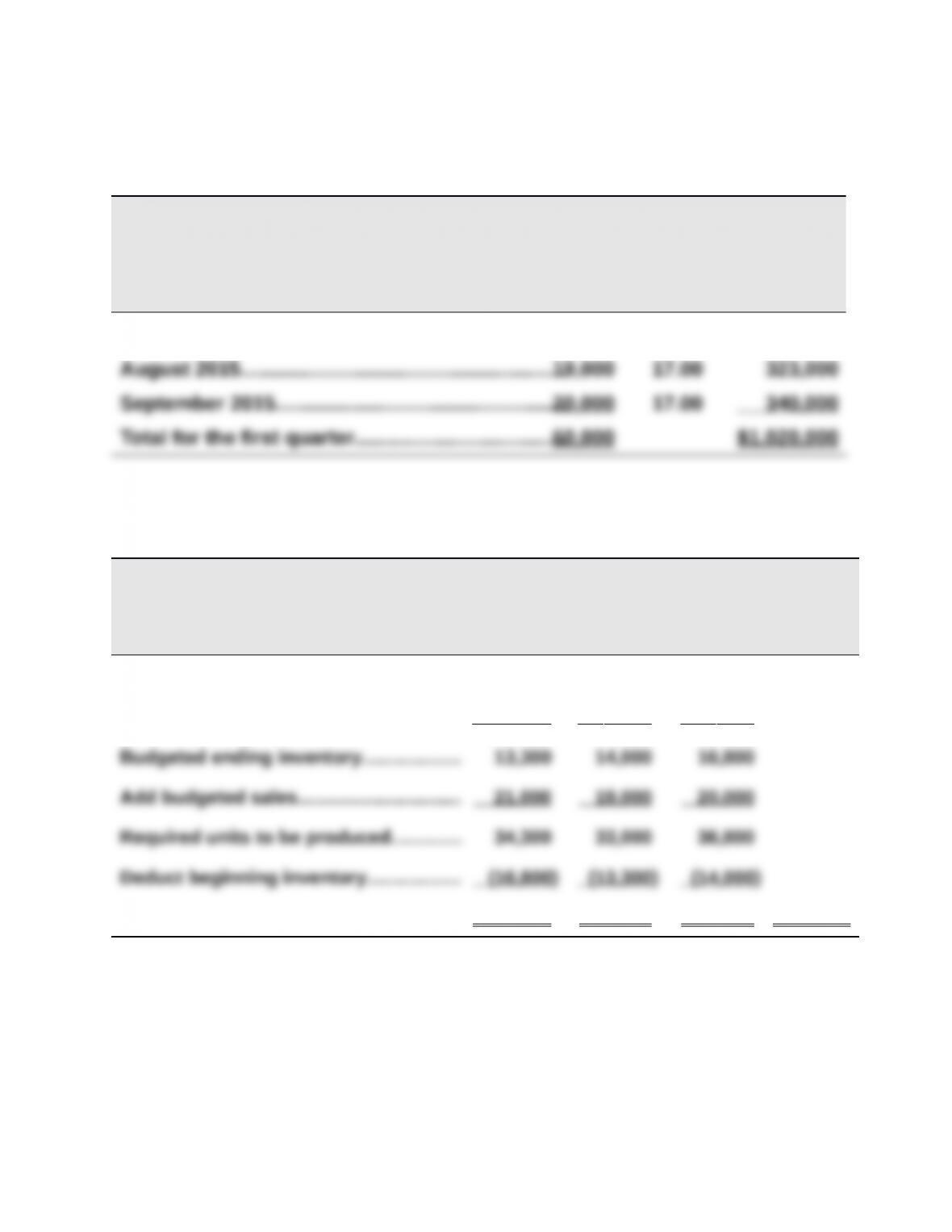

July 2015...............................................................21,000 $17.00 $ 357,000

Part 2

NABAR MANUFACTURING

Production Budget

July, August, and September 2015

July August Sept. Total

Next month’s budgeted sales................ 19,000 20,000 24,000

Ratio of inventory to future sales......... x 70% x 70% x 70%

Units to be produced.............................. 17,500 19,700 22,800 60,000

Problem 22-4B (continued)

Part 3

NABAR MANUFACTURING

Raw Materials Budget

July, August, and September 2015

July August Sept. Total

Production budget (units)...................... 17,500 19,700 22,800

Materials requirement per unit.............. x 0.50 x 0.50 x 0.50

Materials needed for production........... 8,750 9,850 11,400

Part 4

NABAR MANUFACTURING

Direct Labor Budget

July, August, and September 2015

July August Sept. Total

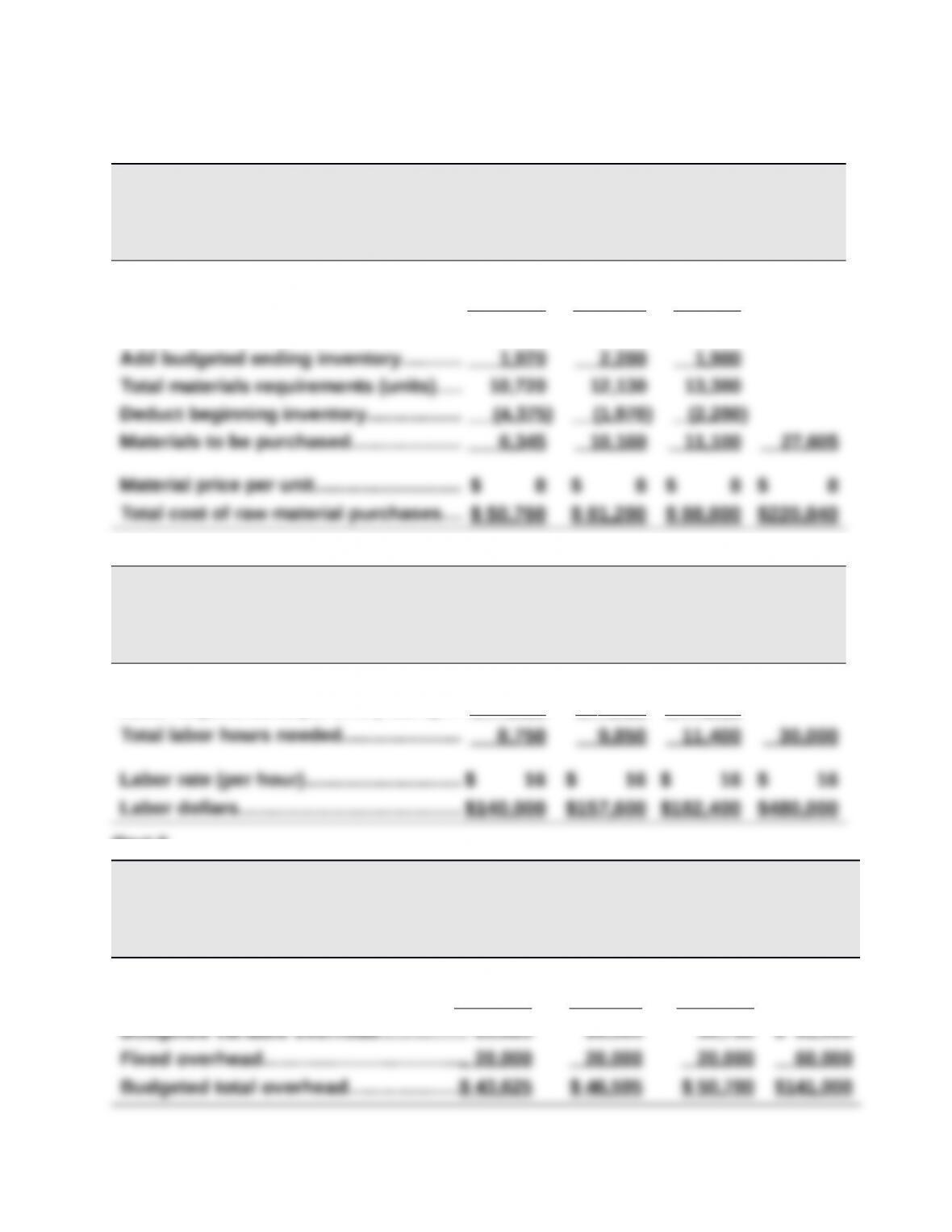

Budgeted production (units)................. 17,500 19,700 22,800

Labor requirements per unit (hours).... x 0.50 x 0.50 x 0.50

Part 5

NABAR MANUFACTURING

Factory Overhead Budget

July, August, and September 2015

July August Sept. Total

Budgeted production (units)................ 17,500 19,700 22,800

Variable factory overhead rate*...........

x $1.35 x $1.35 x $1.35

*$2.70 per direct labor hour x 0.50 direct labor hours per unit

Problem 22-4B (continued)

Part 6

NABAR MANUFACTURING

Selling Expense Budgets

July, August, and September 2015

July August Sept. Total

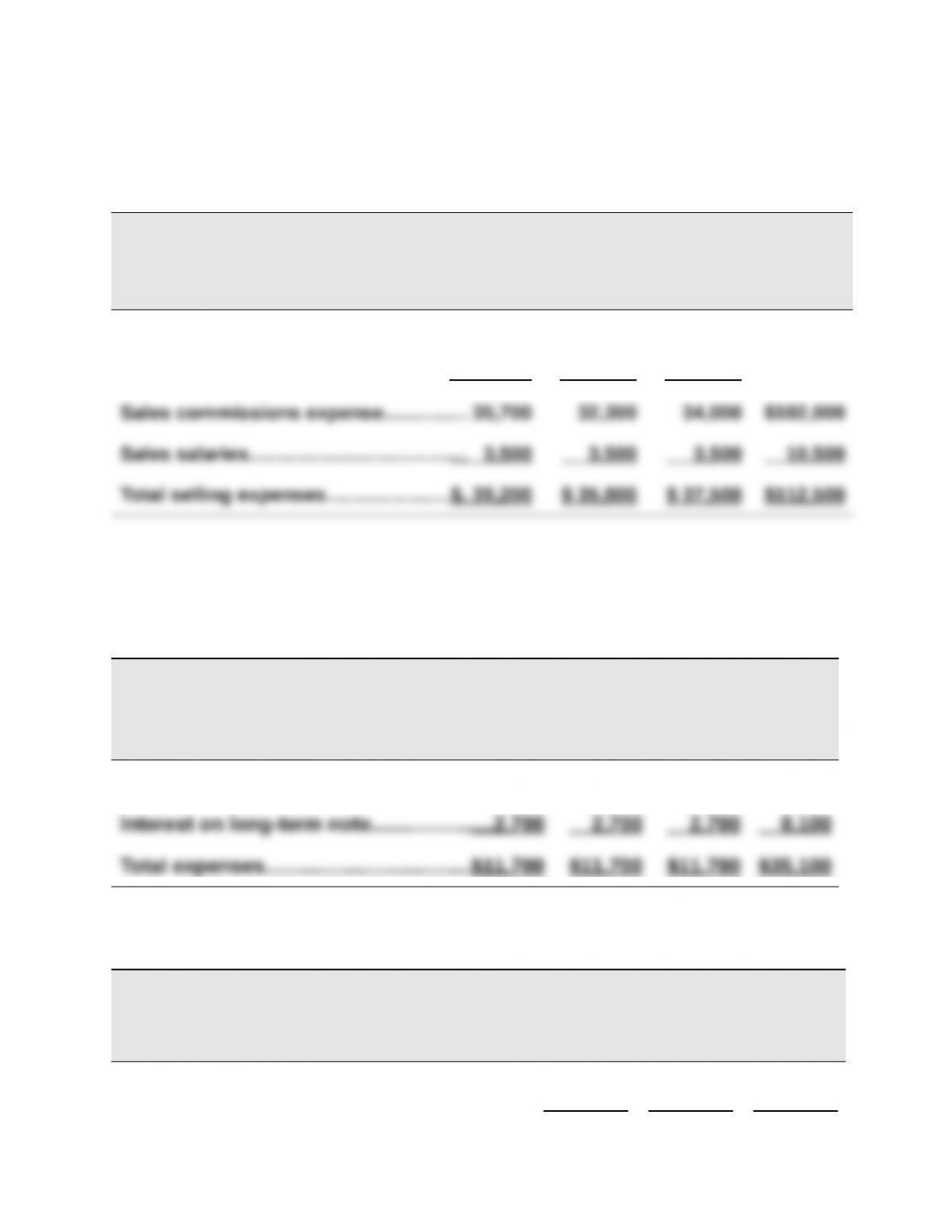

Budgeted sales.....................................$357,000 $323,000 $340,000

Sales commission percent..................x 10% x 10% x 10%

Part 7

NABAR MANUFACTURING

General and Administrative Expense Budgets

July, August, and September 2015

July August Sept. Total

Salaries.......................................................$ 9,000 $ 9,000 $ 9,000 $27,000

Problem 22-4B (Continued)

Part 8

NABAR MANUFACTURING

Cash Budgets

July, August, and September 2015

July August Sept.

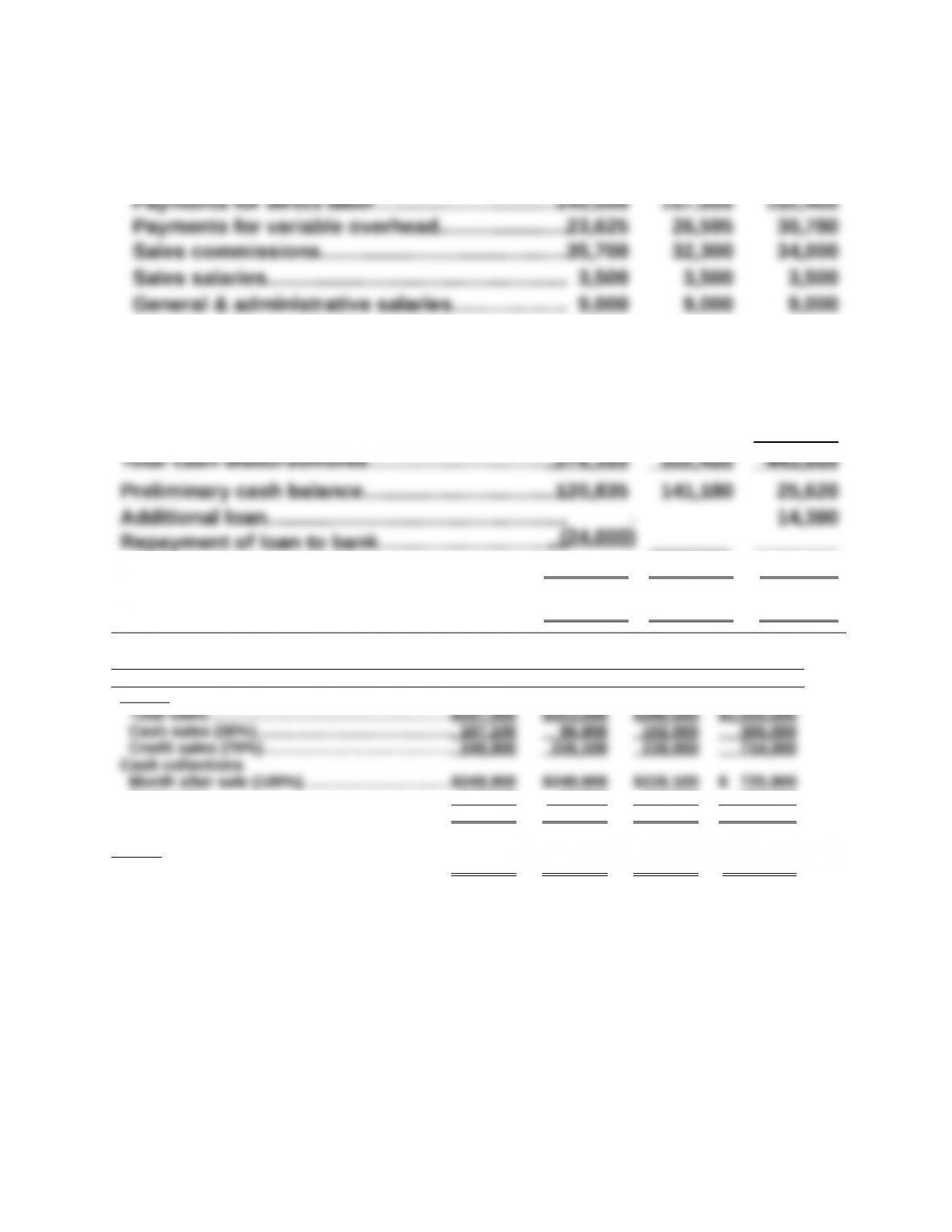

Beginning cash balance......................................$ 40,000 $ 96,835 $141,180

Cash receipts from customers (note A)................ 357,000 346,800 328,100

Total cash available..............................................397,000 443,635 469,280

Cash disbursements

Payments for raw materials (note B)...................51,400 50,760 81,280

Income taxes......................................................

Dividends............................................................

10,000

20,000

Loan interest ($24,000 x 1%)................................... 240

Long-term note interest ($300,000 x .0.9%)............

Purchase of equipment.....................................

2,700

_______

2,700

_______

2,700

100,000

Ending cash balance............................................$ 96,835 $141,180 $ 40,000

Loan balance, end of month................................$ 0 $ 0 $ 14,380

Supporting calculations July August Sept. Total

Note A: Cash receipts from customers

Cash sales........................................................ 107,100 96,900 102,000 306,000

Total cash received..........................................$357,000 $346,800 $328,100 $1,031,900

Note B: Cash payments for raw materials

Month after purchase (100%)..........................$ 51,400 $ 50,760 $ 81,280 $ 183,440

Problem 22-4B (Continued)

Part 9

NABAR MANUFACTURING

Budgeted Income Statement

For Three Months Ended September 30, 2015

Operating expenses

Sales commissions..................................................... $102,000

Sales salaries............................................................... 10,500

General administrative salaries.................................. 27,000

Long-term note interest.............................................. 8,100

Part 10

NABAR MANUFACTURING

Budgeted Balance Sheet

September 30, 2015

Finished goods inventory.........................

241,080

Note E

Total current assets................................... 534,920

Equipment...................................................$820,000 Note F

Less accumulated depreciation............... 300,000 520,000 Note G

Total current liabilities............................... 107,086

Long-term note payable............................

Common stock...........................................$600,000

300,000

Unchanged

Retained earnings...................................... 47,834 Note I

Total liabilities and equity......................... $1,054,920

Problem 22-4B (Concluded)

Supporting Footnotes

Note C

Beginning receivables....................................................... $ 249,900

Credit sales........................................................................ 714,000

Less collections................................................................. (725,900)

Ending receivables............................................................ $ 238,000

Note D

**30,000 units x $8 per unit

Note E

Beginning finished goods inventory................................ $ 241,080

Note G

Beginning accumulated depreciation.............................. $ 240,000

Depreciation expense........................................................ 60,000

Total.................................................................................... $ 300,000

Note I

NABAR MANUFACTURING

Budgeted Statement of Retained Earnings

For Three Months Ended September 30, 2015

Retained earnings, beginning......................... $60,580

Problem 22-5B (60 minutes)

Part 1

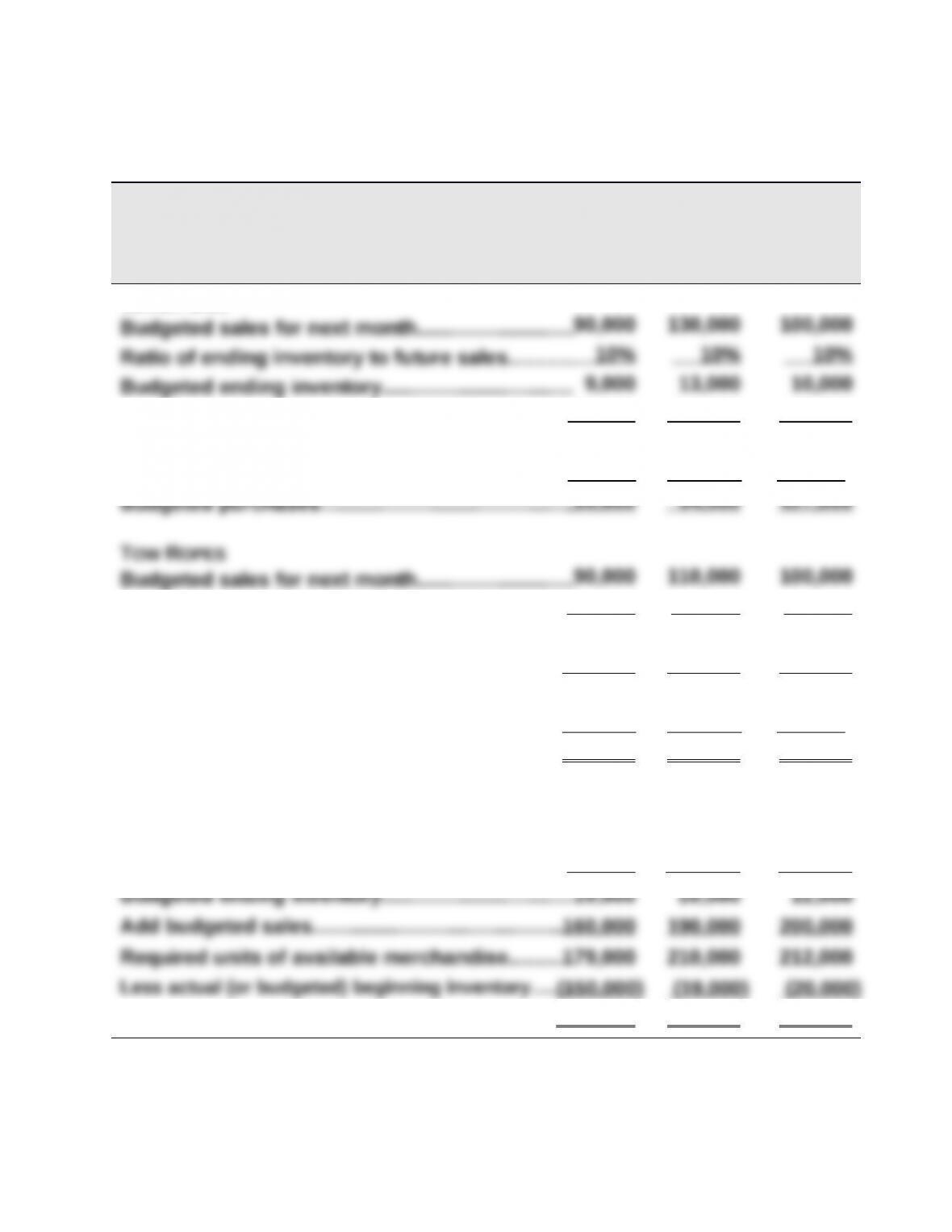

H2O SPORTS CORPORATION

Merchandise Purchases Budgets

For April, May, and June

April May June

WATER SKIS

Add budgeted sales..............................................

70,000 90,000 130,000

Required units of available merchandise...........79,000 103,000 140,000

Less actual (or budgeted) beginning inventory........

(40,000) (9,000) (13,000)

Ratio of ending inventory to future sales...........

10% 10% 10%

Budgeted ending inventory.................................. 9,000 11,000 10,000

Add budgeted sales..............................................

100,000 90,000 110,000

Required units of available merchandise...........

109,000 101,000 120,000

Less actual (or budgeted) beginning inventory........

(90,000) (9,000) (11,000)

Budgeted purchases.............................................

19,000 92,000 109,000

LIFE JACKETS

Budgeted sales for next month............................190,000 200,000 120,000

Ratio of ending inventory to future sales........... 10% 10% 10%

Budgeted purchases............................................. 29,000 191,000 192,000

Problem 22-5B (Concluded)

Part 2. Analysis Component

The factor that causes the first month’s purchases to be so much smaller is

the excess inventory that accumulated just prior to the budgeting period.

For example, 40,000 units of water skis are in April’s beginning inventory;

This overstocking factor could exist for a number of reasons, including:

Management may have simply lost sight of inventory levels, thereby

allowing them to reach inappropriately high levels.

There may have been some potentially disruptive factor (such as a

strike, bad weather, or political uncertainty) that would have temporarily

interrupted the smooth delivery of products from the supplier. Thus,