Problem 21-4B (75 minutes)

Part 1 Instructor note: Use the equation in Exhibit 21.12

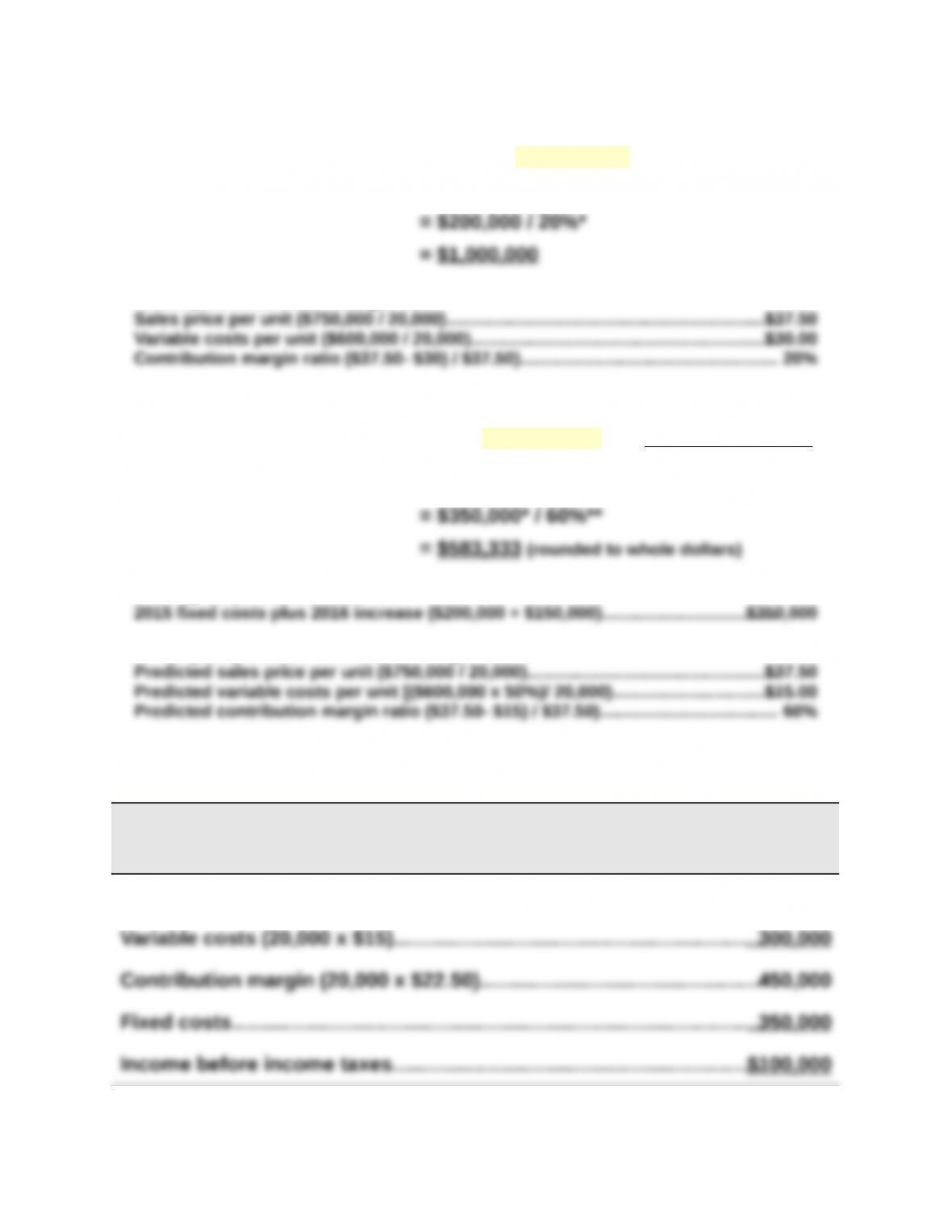

2015 break-even in dollar sales = Fixed costs / Contribution margin ratio

*To compute contribution margin ratio

Part 2 Instructor note: Use equation in Exhibit 21.12 with predicted numbers

2016 break-even in dollar sales = Fixed costs / Contribution margin ratio

*To compute predicted fixed costs

**To compute predicted contribution margin ratio

Part 3

RIVERA COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (20,000 x $37.50)……………………………………………………………….$750,000

Problem 21-4B (Continued)

Part 4 Instructor note: Use equations in Exhibit 21.22 and 21.23 with predicted

numbers

(Fixed costs + Pretax income)

Required sales in dollars = Contribution margin ratio

(Fixed costs + Pretax income)

Required sales in units = Contribution margin per unit

* 2015 fixed costs plus 2016 increase ($200,000 + $150,000)…………………………..$350,000

Part 5

RIVERA COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (24,445 units x $37.50)……………………………………………… $916,688

*Slightly greater than the targeted $200,000 pretax income due to rounding of units from

part 4.

Problem 21-5B (65 minutes)

Part 1 Instructor note: Use the equation in Exhibit 21.12

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Product BB:

*To compute contribution margin ratio

Sales price per unit

Product BB ($800,000 / 50,000)……………………………………………………………………….

BB

$16.00

TT

Part 2

Forecasted contribution margin income statements for each product

assuming sales decline to 33,000 units with no change in unit sales price

STAM CO.

Forecasted Contribution Margin Income Statement

Product BB Product TT

Sales*……………………………………………………………….. $528,000 $ 528,000

Unit sales price and variable costs are computed in Part 1 and used in these computations:

Product TT variable costs = 33,000 units x $2.

Problem 21-5B (Continued)

Forecasted contribution margin income statements for each product

assuming sales increase to 64,000 units with no change in unit sales price:

STAM CO.

Forecasted Contribution Margin Income Statement

Product BB Product TT

Sales*………………………………………………………………..$1,024,000 $1,024,000

Variable costs**…………………………………………………. 716,800 128,000

Unit sales price and variable costs are computed in Part 1 and used in these computations:

Part 4

If sales were to greatly increase, Product TT would experience the greater

increase in income because it would gain more contribution margin per

Part 5

Factors that could cause Product BB to have lower fixed costs include:

Labor arrangement that pays workers for units produced.

In contrast, the fixed costs for Product TT could be higher because of:

Problem 21-6B (45 minutes)

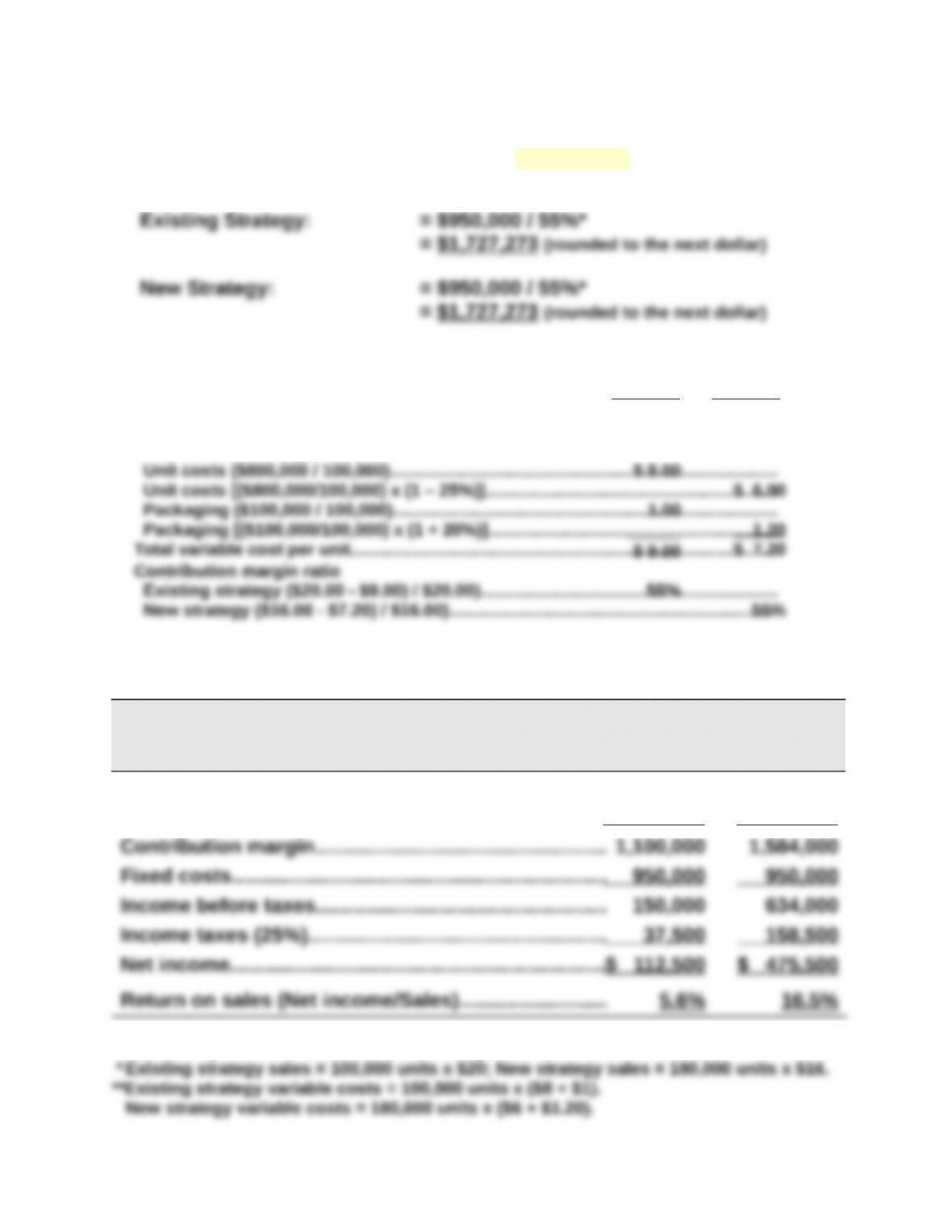

Part 1 Instructor note: Use the equation in Exhibit 21.12

Break-even in dollar sales = Fixed costs / Contribution margin ratio

*To compute contribution margin ratio

Sales price per unit

Existing strategy…………………………………………………………………………………………….

New strategy [$20.00 x (1 – 20%)]……………………………………………………………………

Existing

Strategy

$20.00

New

Strategy

$16.00

Total variable costs per unit

Part 2

BEST COMPANY

Forecasted Contribution Margin Income Statement

Existing Strategy New Strategy

Sales*………………………………………………………………..$2,000,000 $2,880,000

Variable costs**…………………………………………………. 900,000 1,296,000

Unit sales price and variable costs are computed in Part 1 and used here:

Problem 21-7B (50 minutes)

Part 1 BREAK–EVEN ANALYSIS ASSUMING USE OF SAME MATERIALS

Step 1: Compute break-even in composite units—Use equation in Exhibit 21.29

Break-even in composite units = Fixed costs/Contribution margin per composite unit

* To compute the contribution margin per composite unit

Unit Sales Price Unit Variable Costs

6 units of Product 1

@ $40 per unit……………………………………………

@ $30 per unit……………………………………………

$240

$180

4 units of Product 2

Thus:

Step 2: Compute break-even in individual product unit sales

Unit sales of Product 1 at break-even: 1,875 x 6 = 11,250 units

Step 3: Compute break-even in individual product dollar sales

Dollar sales of Product 1 at break-even: 11,250 units x $40 = $450,000

Crossfoot Step 3 total with that from formula:

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Problem 21-7B (Continued)

Part 2 BREAK–EVEN ANALYSIS ASSUMING USE OF NEW MATERIALS

Step 1: Compute break-even in composite units—Use equation in Exhibit 21.29

Break-even in composite units = Fixed costs/Contribution margin per composite unit

*To compute the contribution margin per composite unit

Unit Sales Price Unit Variable Costs

6 units of Product 1

@ $40 per unit………………………………………………..

@ ($30 – $10) per unit……………………………………..

$240

$120

4 units of Product 2

Thus:

Step 2: Compute break-even in individual product unit sales

Unit sales of Product 1 at break-even: 1,429 x 6 = 8,574 units

Step 3: Compute break-even in individual product dollar sales

Dollar sales of Product 1 at break-even: 8,574 units x $40 = $342,960

Crossfoot Step 3 total with that from formula ($171 of rounding differences):

Break-even in $ sales = Fixed costs / Contribution margin ratio

Part 3

When a business invests in fixed assets, as in this case, there is an increase

in its risk level (more fixed costs must be recovered). However, investments