Problem 21-5A (Continued)

Part 3 Forecasted contribution margin income statements for each product

assuming sales increase to 60,000 units with no change in unit sales price

HENNA CO.

Forecasted Contribution Margin Income Statement

Product T Product O

Sales*………………………………………………………………..$2,400,000 $2,400,000

Variable costs**…………………………………………………. 1,920,000 300,000

Unit sales price and variable costs are computed in Part 1 and used in these computations:

Part 4

If sales were to greatly decrease, Product O would suffer the greater loss

because it would lose more contribution margin per unit than Product T

Part 5

Factors that could cause Product T to have lower fixed costs might include:

In contrast, fixed costs for Product O may be higher because of:

Problem 21-6A (45 minutes)

Part 1 Instructor note: Use the equation in Exhibit 21.12

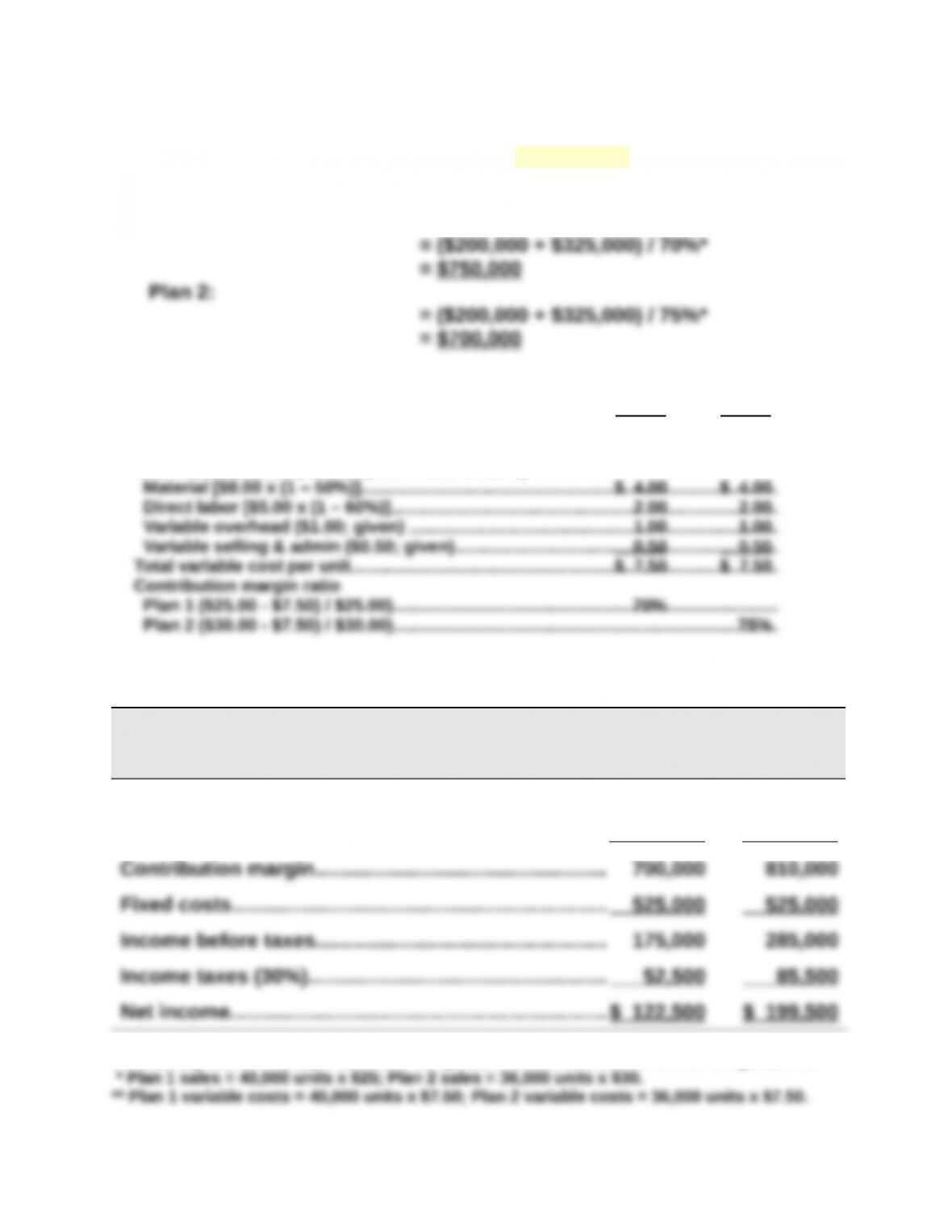

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Plan 1:

*To compute contribution margin ratio

Sales price per unit

Plan 1 (no change)………………………………………………………………………………………….

Plan 2 [$25.00 x (1 + 20%)]………………………………………………………………………………

Plan 1

$25.00

Plan 2

$30.00

Total variable costs per unit (both Plans 1 and 2)

Part 2

BURCHARD CO.

Forecasted Contribution Margin Income Statement

Plan 1 Plan 2

Sales*………………………………………………………………..$1,000,000 $1,080,000

Variable costs**…………………………………………………. 300,000 270,000

Unit sales price and variable costs are computed in Part 1 and used in these computations:

Problem 21-7A (50 minutes)

Part 1 BREAK–EVEN ANALYSIS ASSUMING USE OF SAME MATERIALS

Step 1: Compute break-even in composite units—Use equation in Exhibit 21.29

Break-even in composite units = Fixed costs/Contribution margin per composite unit

*To compute the contribution margin per composite unit

Unit Sales Price Unit Variable Costs

5 units of Red

@ $20 per unit……………………………………………

@ $12 per unit……………………………………………

$100

$ 60

4 units of White

Thus:

Step 2: Compute break-even in individual product unit sales

Step 3: Compute break-even in individual product dollar sales

Crossfoot Step 3 total with that from formula ($235 rounding difference):

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Problem 21-7A (Continued)

Part 2 BREAK–EVEN ANALYSIS ASSUMING USE OF NEW MATERIALS

Step 1: Compute break-even in composite units—Use equation in Exhibit 21.29

Break-even in composite units = Fixed costs/Contribution margin per composite unit

= 1,364 composite units (rounded to the next whole unit)

*To compute the contribution margin per composite unit

Unit Sales Price Unit Variable Costs

5 units of Red

@ $20 per unit………………………………………………..

@ ($12 – $6) per unit……………………………………….

$100

$ 30

4 units of White

Variable cost of a composite unit………………………

Thus:

Step 2: Compute break-even in individual product unit sales

Unit sales of Red at break-even: 1,364 x 5 = 6,820 units

Step 3: Compute break-even in individual product dollar sales

Dollar sales of Red at break-even: 6,820 units x $20 = $136,400

Crossfoot Step 3 total with that from formula ($139 rounding difference):

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Part 3

When a business invests in fixed assets, as in this case, there is an

PROBLEM SET B

Problem 21-1B (25 minutes)

Parts 1 and 2

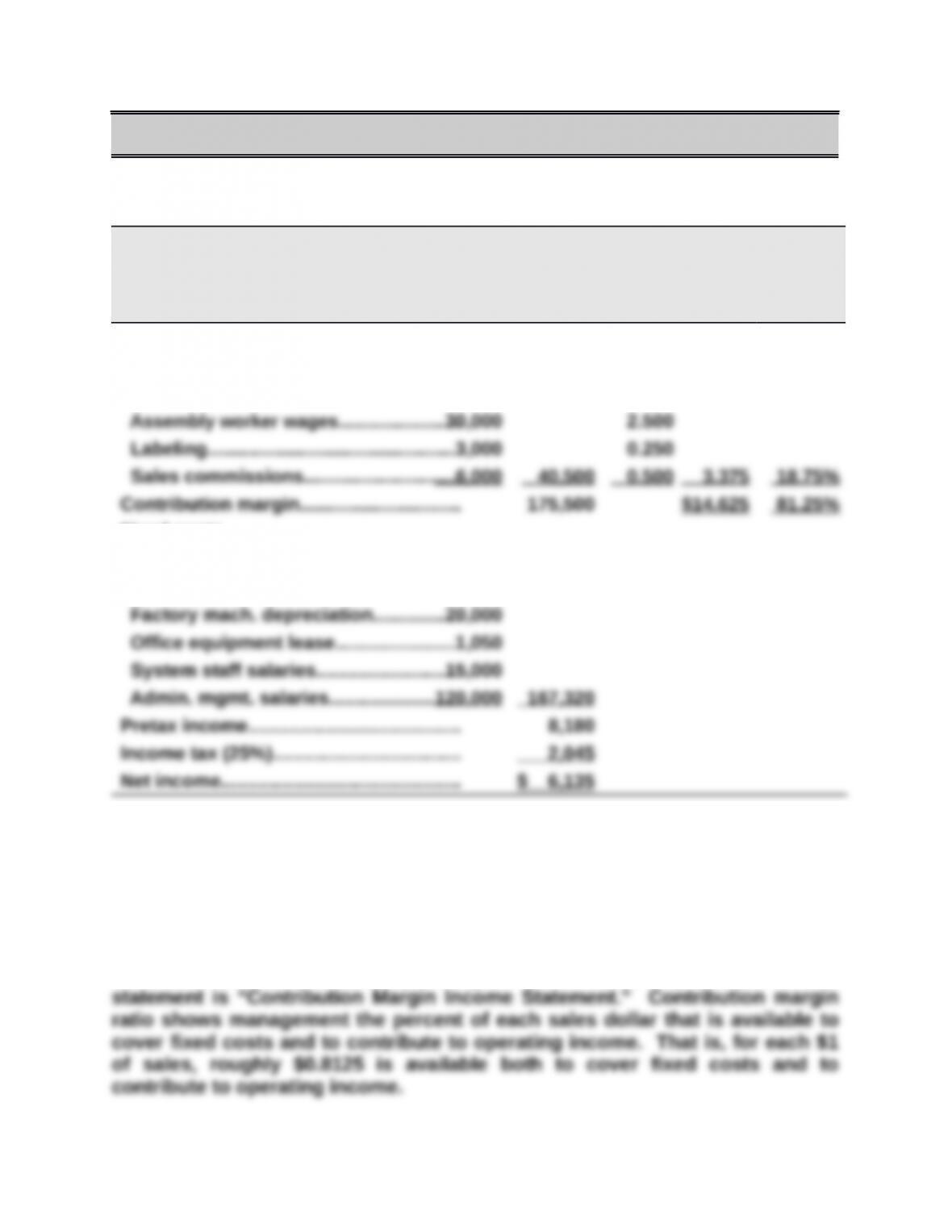

Gilmore Company

Contribution Margin Income Statement

For Year Ended December 31, 2015

(12,000 units) Per unit % of sales

Sales ($18 x 12,000)………………………. $216,000 $18.000 100.00%

Variable costs

Plastic for CD sets……………………….$ 1,500 $0.125

Fixed costs

Rent on factory………………………………6,750

Factory cleaning service…………………4,520

The contribution margin per unit is $14.625, and the contribution margin ratio is

81.25%.

Part 3 Analysis Component

Contribution margin shows how much of total sales are available to cover

fixed costs and contribute to operating income. This is why the title for this

Sun Company

20

40

60

80

100

$120

Sales Dollars

Total

Costs

Problem 21-2B (45 minutes)

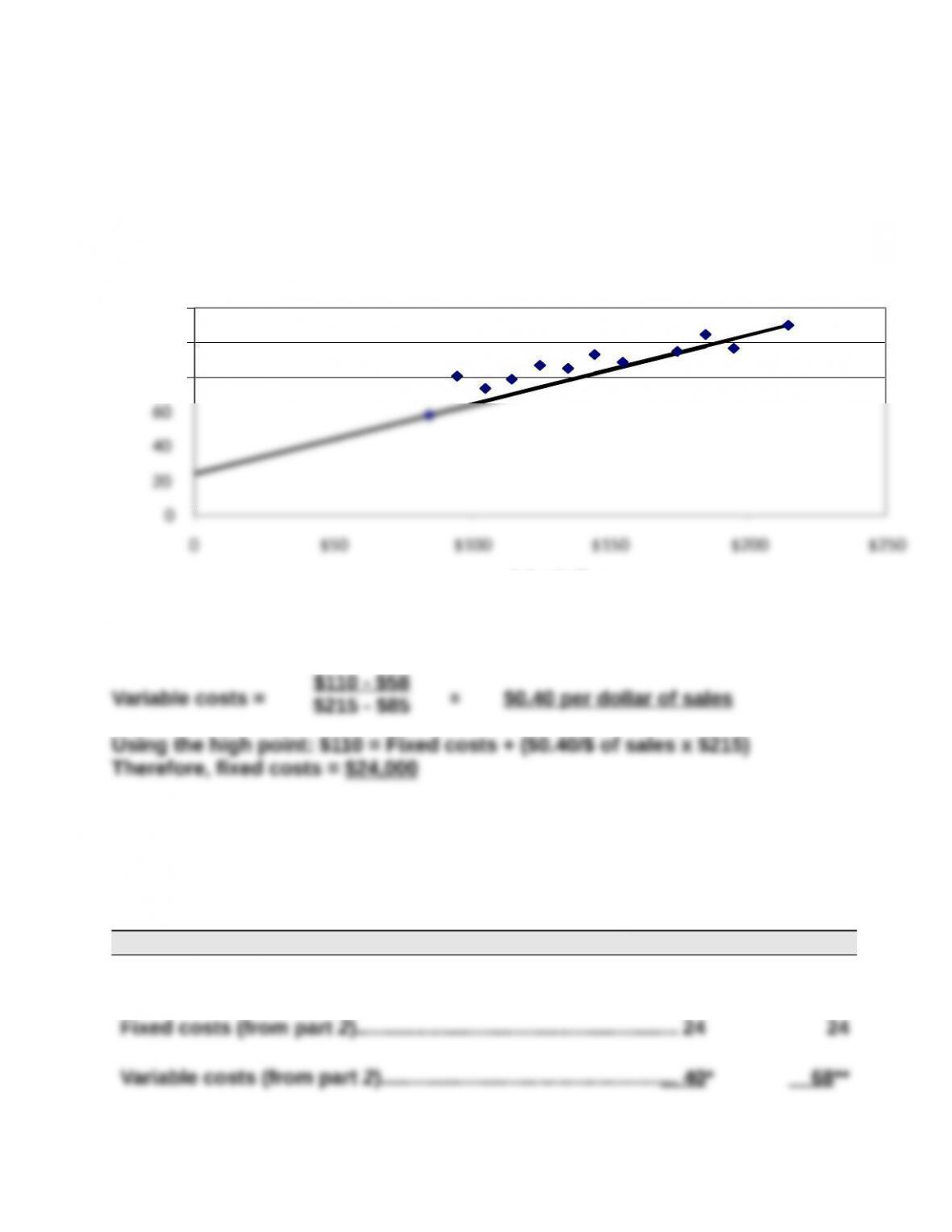

Parts 1 and 2

The scatter diagram and its estimated line of cost behavior appear below.

Sales and cost amounts are in thousands of dollars.

Part 2 Calculation of variable and fixed costs

Part 3

The estimates in Part 2 can be used to predict the total costs that will be

incurred at sales levels of $100 and $170 (both in thousands).

(‘000s) Predictions

Sales (given)…………………………………………………………………$100 $170

Fixed costs (from part 2)……………………………………………….. 24 24

Variable costs (from part 2)…………………………………………… 40* 68**

$110 – $58

Problem 21-3B (40 minutes)

Part 1

(a) Instructor note: Use the equation in Exhibit 21.11

Break-even in unit sales = Fixed costs / Contribution margin per unit

(b) Instructor note: Use the equation in Exhibit 21.12

Break-even in dollar sales = Fixed costs / Contribution margin ratio

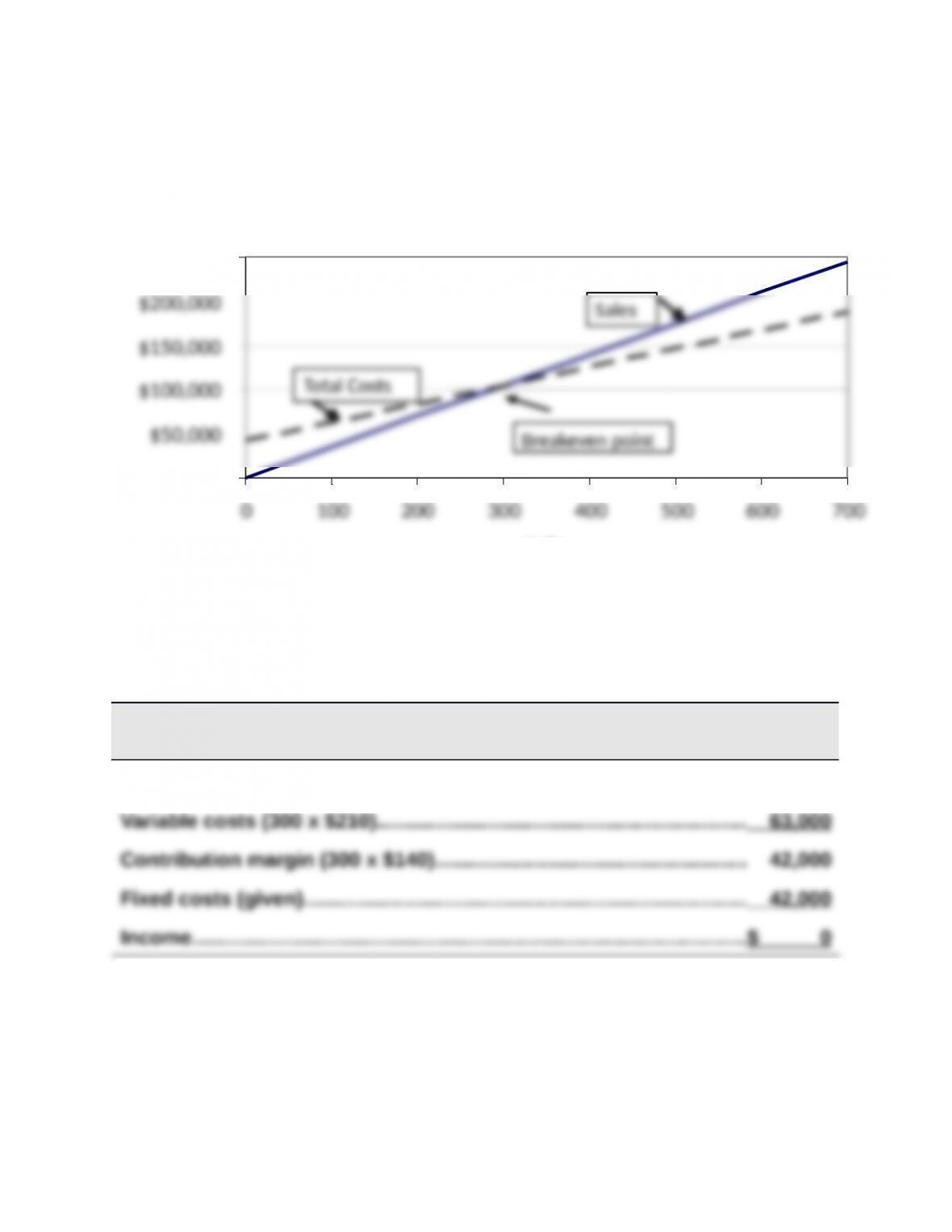

Hip-Hop Company CVP chart

$200,000

$250,000

Units

Problem 21-3B (Continued)

Part 2

Part 3

HIP-HOP CO.

Contribution Margin Income Statement (at Break-Even) — Keyboards

Sales (300 x $350)…………………………………………………………………….$105,000