Chapter 21 – Cost-Volume-Profit Analysis

Exercise 21-25 (10 minutes)

1. Degree of operating leverage = Total contribution margin

Pretax income

= $432,000/$108,000

= 4.0

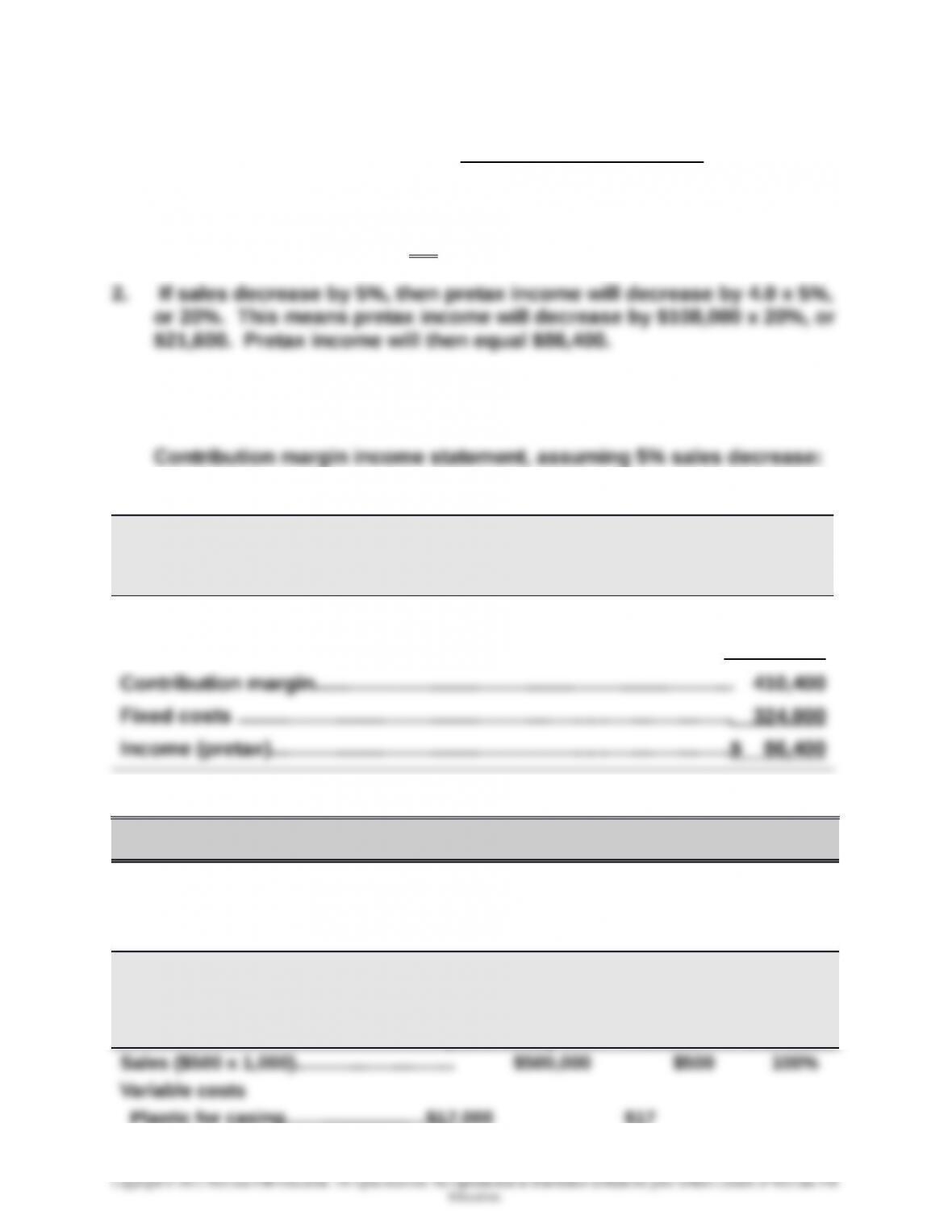

3. If sales decrease by 5%, a total of 9,120 (computed as 9,600 x 95%)

units will be sold.

HUDSON CO.

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (9,120 x $225)…………………………………………………………………$2,052,000

Variable costs (9,120 x $180)…………………………………………………… 1,641,600

PROBLEM SET A

Problem 21-1A (25 minutes)

Parts 1 and 2

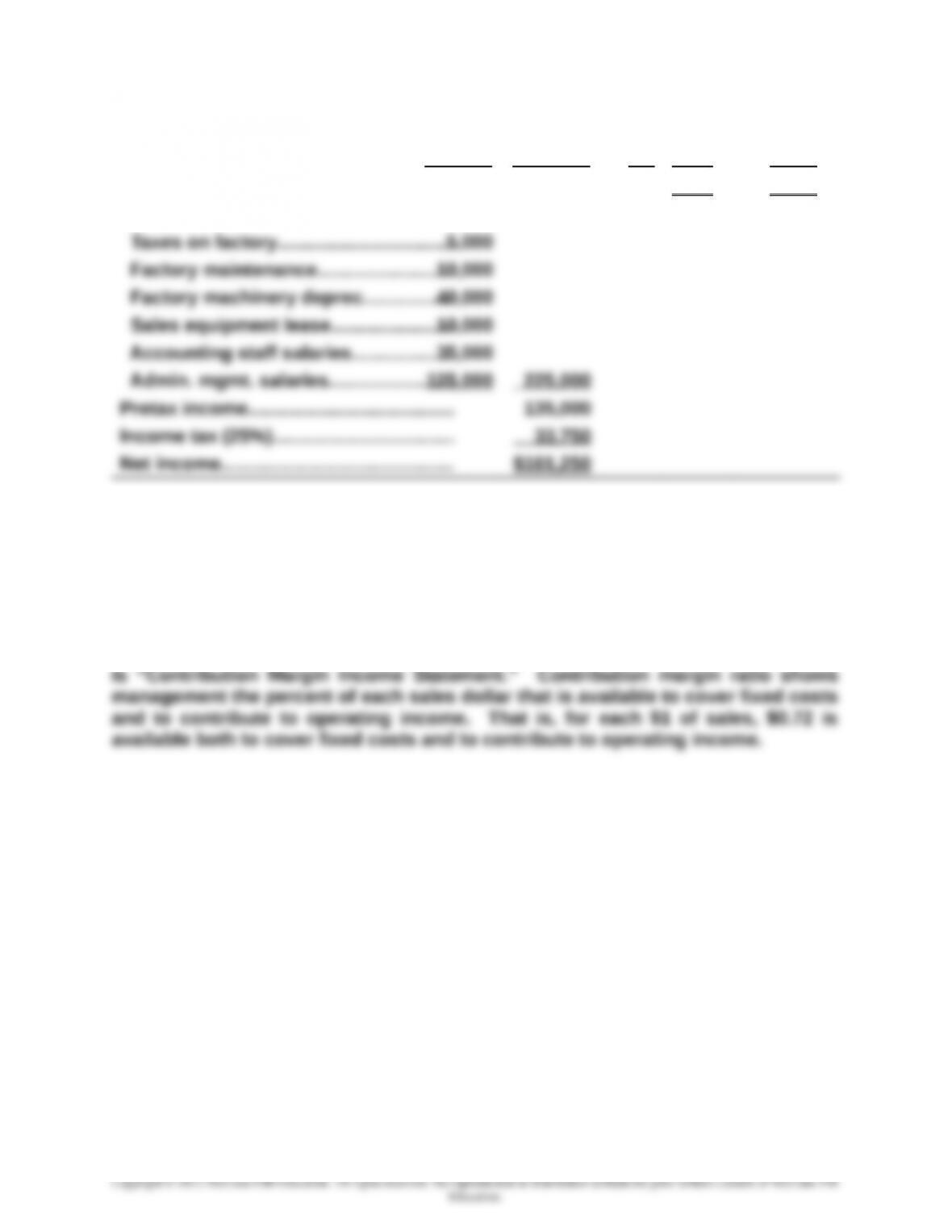

Tight Drums Company

Contribution Margin Income Statement

For Year Ended December 31, 2015

(1,000 units) Per unit % of sales

Plastic for casing…………………………$17,000 $17

21-1209

Chapter 21 – Cost-Volume-Profit Analysis

Assembly worker wages…………..…….82,000 82

Drum stands……..………………………..26,000 26

Sales commissions……………….……. 15,000 140,000 15 140 28%

Contribution margin……………………… 360,000 $360 72%

Fixed costs

The contribution margin per unit is $360, and the contribution margin ratio is 72%.

Part 3 Analysis Component

Contribution margin shows how much of total sales are available to cover fixed

costs and contribute to operating income. This is why the title for this statement

21-1210

Chapter 21 – Cost-Volume-Profit Analysis

Problem 21-2A (45 minutes)

Parts 1 and 2

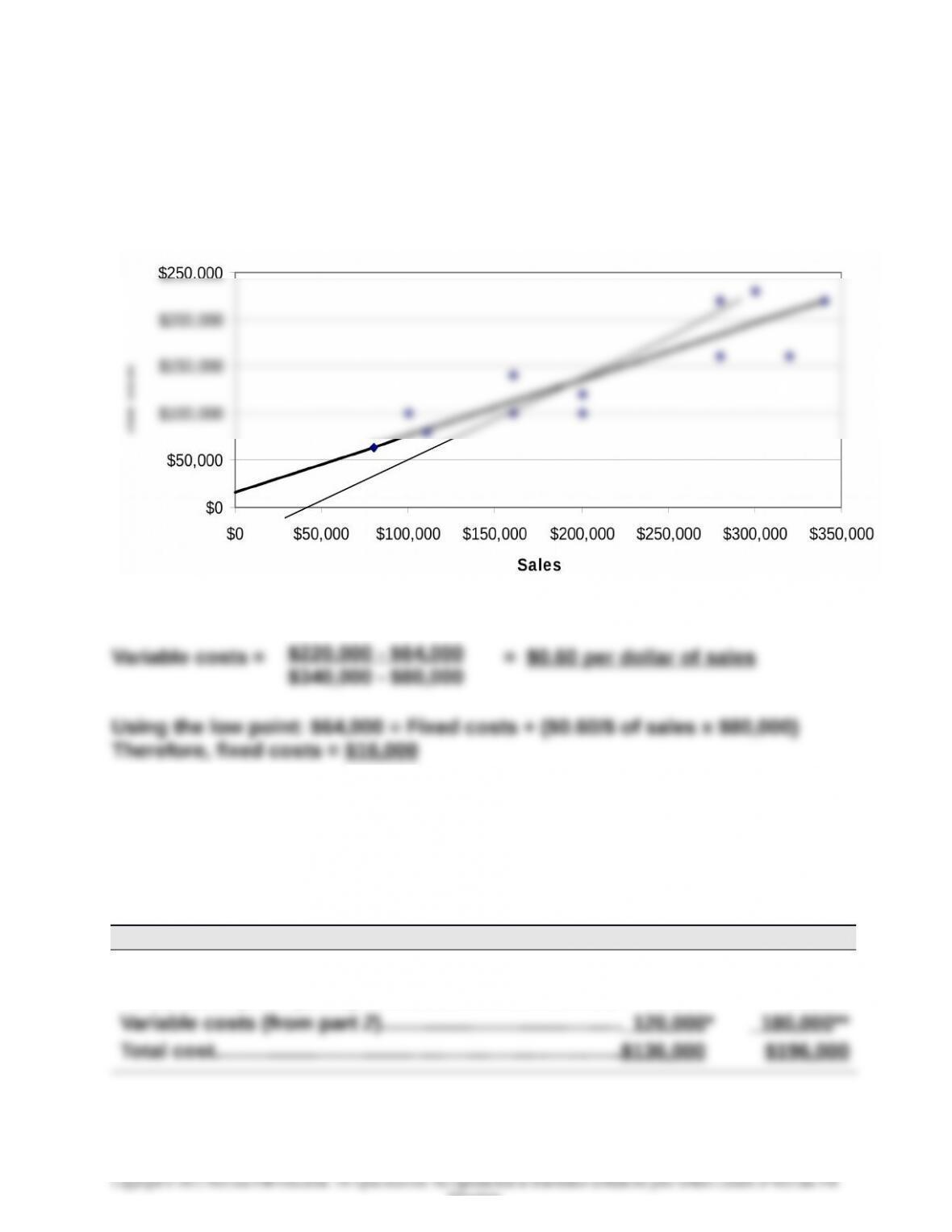

The scatter diagram and its estimated line of cost behavior appear below.

Part 2 – Calculation of variable and fixed costs

Part 3

The estimates in Part 2 can be used to predict the total costs that will be

incurred at sales levels of $200,000 and $300,000.

Predictions

Sales (given)…………………………………………….……………$200,000 $300,000

Fixed costs (from part 2)……………………….………………. 16,000 16,000

* ($200,000 sales) x ($0.60 per sales dollar).

** ($300,000 sales) x ($0.60 per sales dollar).

21-1211

Education.

Alden Co.

Chapter 21 – Cost-Volume-Profit Analysis

Problem 21-3A (40 minutes)

Part 1

(a) Instructor note: Use the equation in Exhibit 21.11

*Contribution margin per unit = $200 – $140 = $60 per 100 yards

(b) Instructor note: Use the equation in Exhibit 21.12

(Alternatively: = 4,500 units x $200 = $900,000)

*Contribution margin ratio = $60 / $200 = 30%

Problem 21-3A (Continued)

Part 2

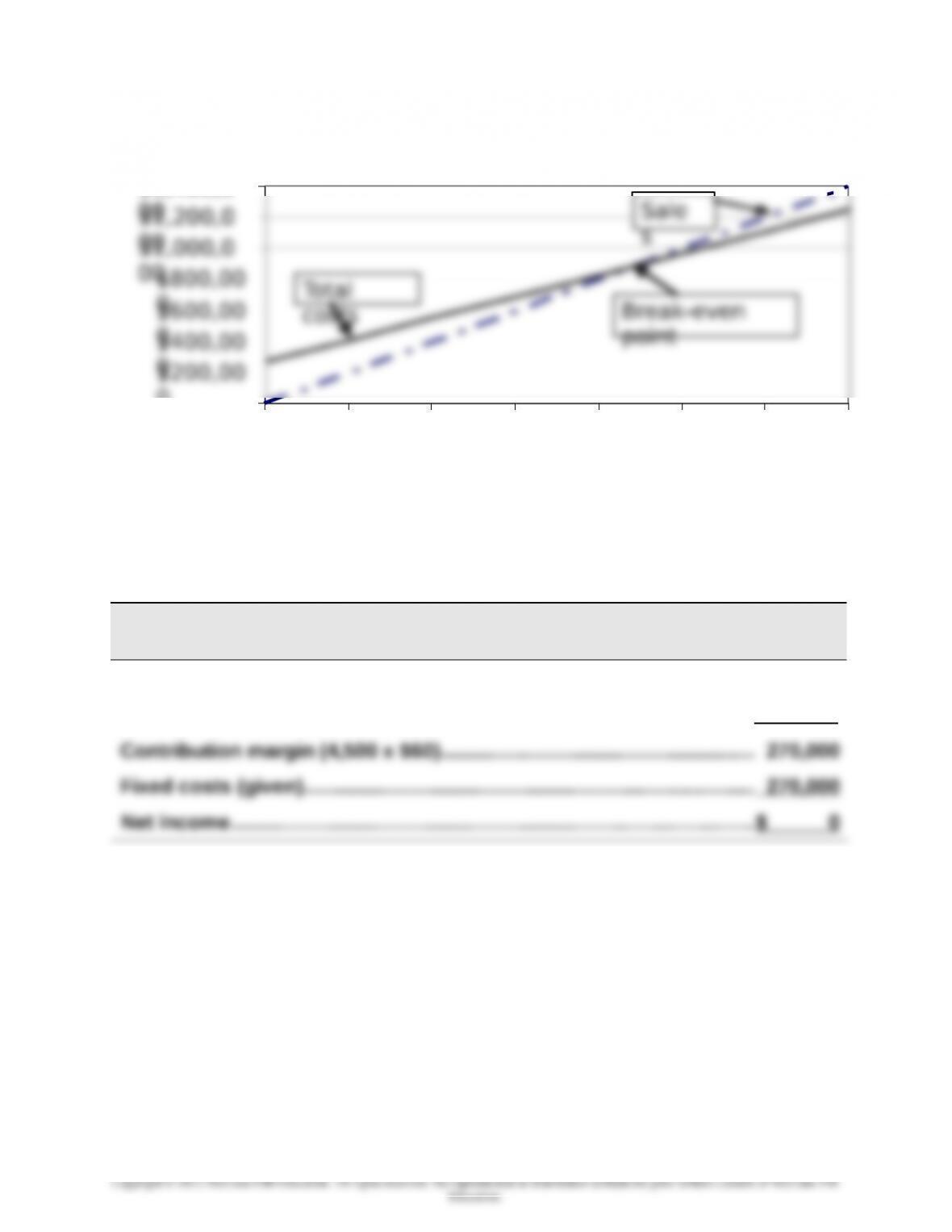

CVP Chart for Praveen Company

21-1212

$

0

0

$400,00

0

$800,00

$1,000,0

00

$1,200,0

00

$1,400,0

0 1,00

0

2,00

0

3,00

0

4,00

0

5,00

0

6,00

0

7,00

0

Units (100

yards)

s

Chapter 21 – Cost-Volume-Profit Analysis

Part 3

PRAVEEN CO.

Contribution Margin Income Statement (at Break-Even) — Product XT

Sales (4,500 x $200)……………………………………………………….……………$900,000

Variable costs (4,500 x $140)……………………………………..……………….. 630,000

21-1213

Chapter 21 – Cost-Volume-Profit Analysis

Problem 21-4A (75 minutes)

Part 1 Instructor note: Use the equation in Exhibit 21.12

*To compute contribution margin ratio

Sales price per unit ($1,000,000 / 20,000)..………….………………….............................$50

Variable costs per unit ($800,000 / 20,000)…..……………….……………........................$40

Contribution margin ratio ($50- $40) / $50)……………………………………………………...20%

Part 2 Instructor note: Use the equation in Exhibit 21.12 with predicted

numbers

*To compute predicted fixed costs

2015 fixed costs plus 2016 increase ($250,000 + $200,000)………………..................$450,000

**To compute predicted contribution margin ratio

Predicted sales price per unit (no change in sales price)…….…….………................$50

Predicted variable costs per unit ($40 x 50%)..……………….…………………….............$20

Predicted contribution margin ratio ($50- $20) / $50).…….…………….......................60%

Part 3

ASTRO COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

21-1214

Chapter 21 – Cost-Volume-Profit Analysis

Problem 21-4A (Continued)

Part 4 Instructor note: Use equations in Exhibits 21.22 and 21.23 with

predicted numbers

(Fixed costs + Target pretax income)

Required sales in units = Contribution margin per unit

= ($450,000 + $200,000) / ($50 – $20)

= $650,000 / $30

= 21,667 units (rounded to whole units)

* 2015 fixed costs plus 2016 increase ($250,000 + $200,000)……..……………........$450,000

** Predicted contribution margin ratio ($50- $30) / $50)—from part 2................... 60%

† Taken from “required sales in dollars” above

Part 5

ASTRO COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (21,667 units x $50)………………………………………….……………….$1,083,350

Income before income taxes*………………………………………………….….$ 200,010

*Slightly greater than the targeted $200,000 income due to rounding of units.

21-1215

Education.

Chapter 21 – Cost-Volume-Profit Analysis

Problem 21-5A (65 minutes)

Part 1 Instructor note: Use the equation in Exhibit 21.12

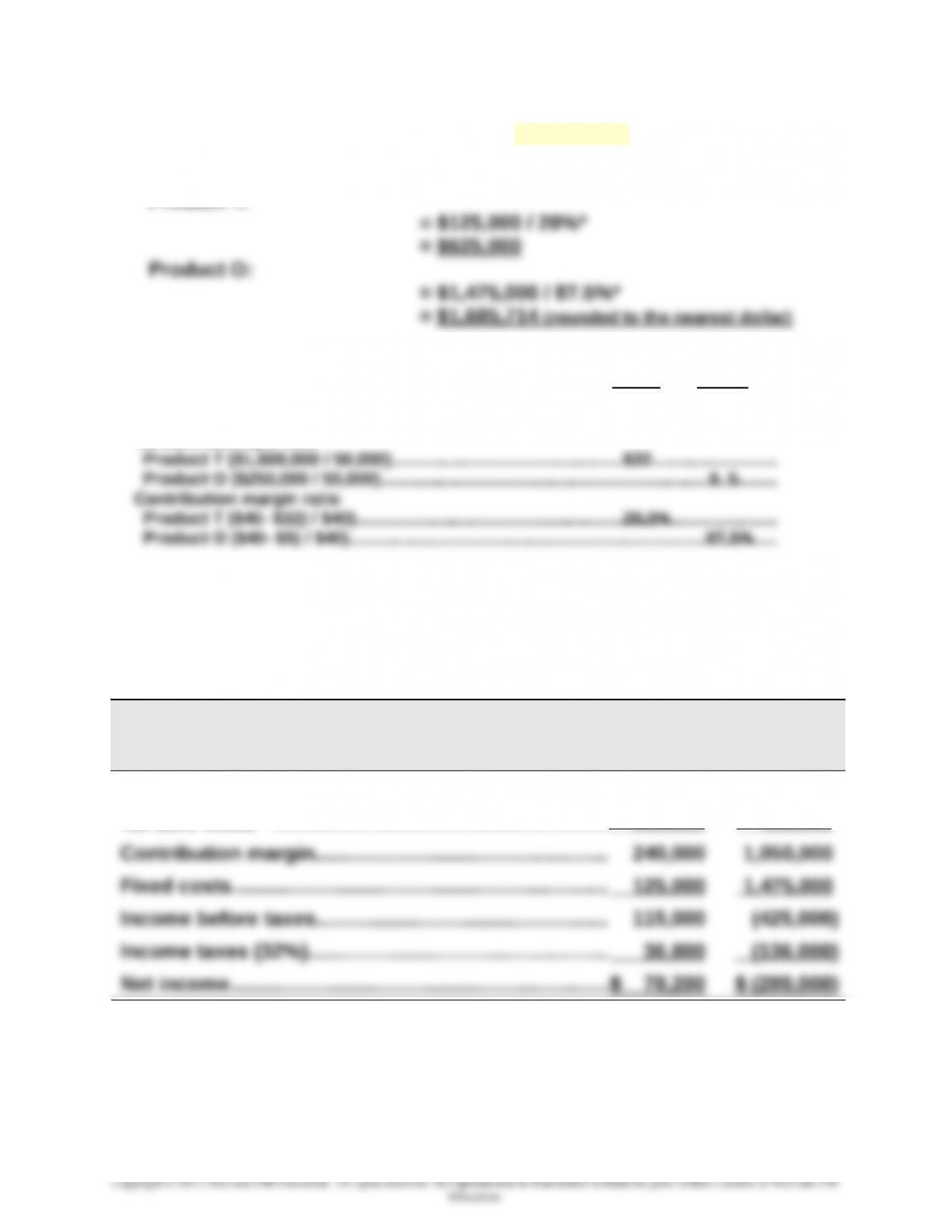

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Product T:

*To compute contribution margin ratio

Sales price per unit

Product T ($2,000,000 / 50,000)……………………………………………………………………..

Product O ($2,000,000 / 50,000)………………………………………………………..…………..

__T__

$40

__O__

$40

Variable costs per unit

Part 2

Forecasted contribution margin income statements for each product

assuming sales declines to 30,000 units with no change in unit sales price

HENNA CO.

Forecasted Contribution Margin Income Statement

Product T Product O

Sales*…………………………………………………………..……..$1,200,000 $1,200,000

Variable costs**…………………………………………………… 960,000 150,000

Unit sales price and variable costs are computed in Part 1 and used in these computations:

* Product T sales = 30,000 units x $40; Product O sales = 30,000 units x $40.

** Product T variable costs = 30,000 units x $32; Product O variable costs = 30,000 units x $5.

21-1216

Chapter 21 – Cost-Volume-Profit Analysis

Problem 21-5A (Continued)

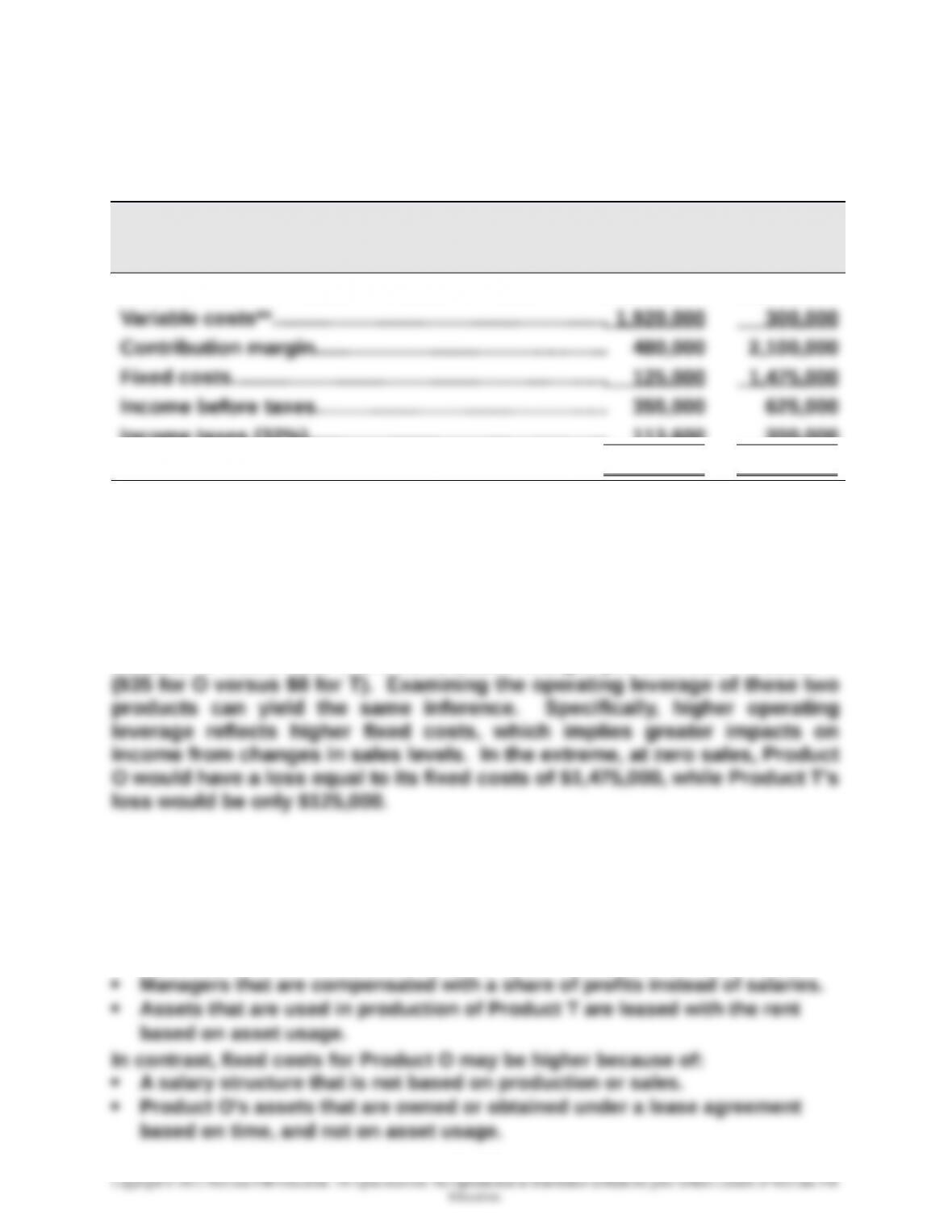

Part 3 Forecasted contribution margin income statements for each product

assuming sales increase to 60,000 units with no change in unit sales price

HENNA CO.

Forecasted Contribution Margin Income Statement

Product T Product O

Sales*…………………………………………………………..……..$2,400,000 $2,400,000

Income taxes (32%)…………………………..………………… 113,600 200,000

Net income……………………………………..…………………..$ 241,400 $ 425,000

Unit sales price and variable costs are computed in Part 1 and used in these computations:

* Product T sales = 60,000 units x $40; Product O sales = 60,000 units x $40.

** Product T variable costs = 60,000 units x $32; Product O variable costs = 60,000 units x $5.

Part 4

If sales were to greatly decrease, Product O would suffer the greater loss

because it would lose more contribution margin per unit than Product T

Part 5

Factors that could cause Product T to have lower fixed costs might include:

Labor arrangement that pays workers for units produced.

Sales representatives that work totally on commission.

21-1217

Chapter 21 – Cost-Volume-Profit Analysis

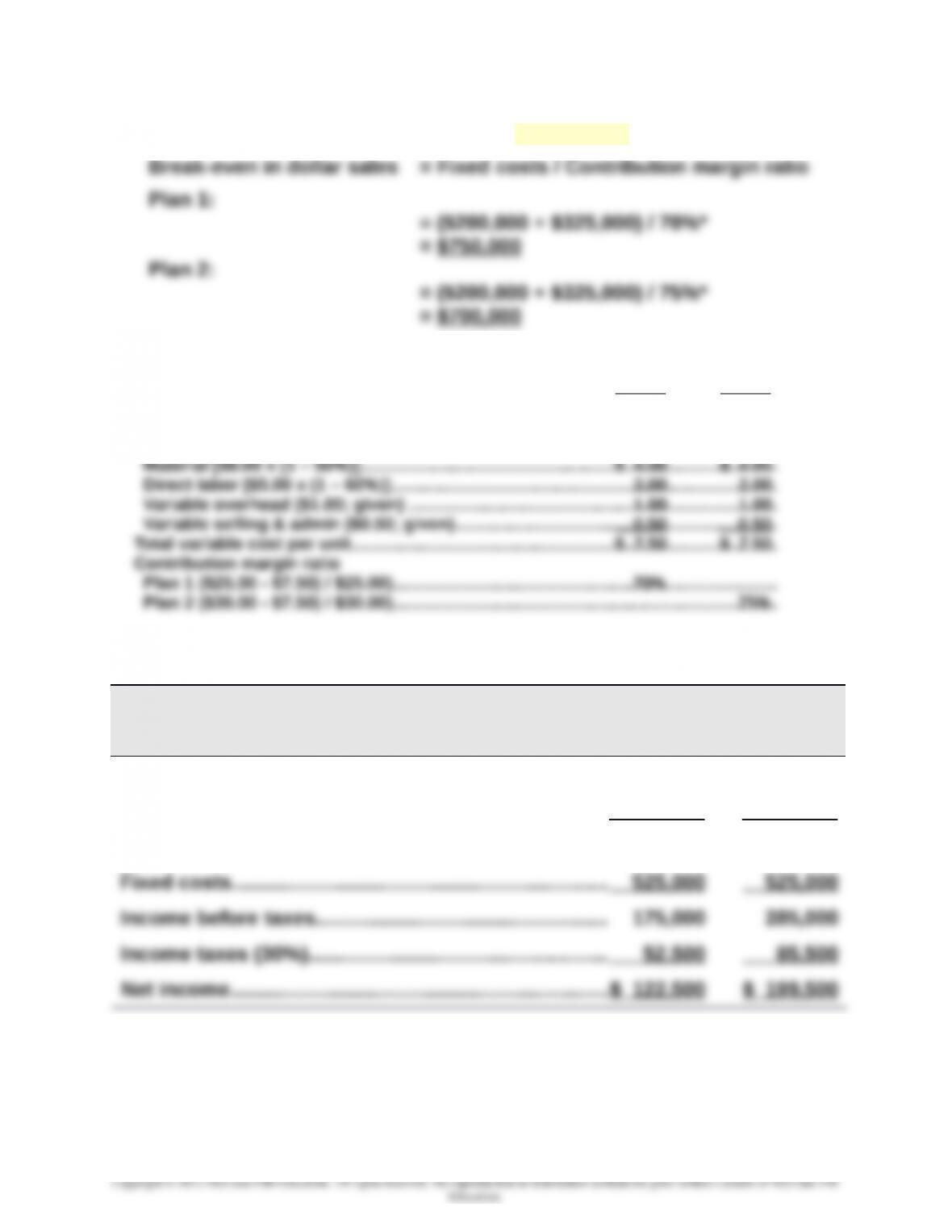

Problem 21-6A (45 minutes)

Part 1 Instructor note: Use the equation in Exhibit 21.12

*To compute contribution margin ratio

Sales price per unit

Plan 1 (no change)……………………………………………………………………………………….

Plan 2 [$25.00 x (1 + 20%)]………………………………………………………………….…..……

Plan 1

$25.00

Plan 2

$30.00

Total variable costs per unit (both Plans 1 and 2)

Part 2

BURCHARD CO.

Forecasted Contribution Margin Income Statement

Plan 1 Plan 2

Sales*…………………………………………………………..……..$1,000,000 $1,080,000

Variable costs**…………………………………………………… 300,000 270,000

Contribution margin………………………………..………….. 700,000 810,000

Unit sales price and variable costs are computed in Part 1 and used in these computations:

* Plan 1 sales = 40,000 units x $25; Plan 2 sales = 36,000 units x $30.

** Plan 1 variable costs = 40,000 units x $7.50; Plan 2 variable costs = 36,000 units x $7.50.

21-1218