Chapter 21 – Cost-Volume-Profit Analysis

Exercise 21-6 (20 minutes)

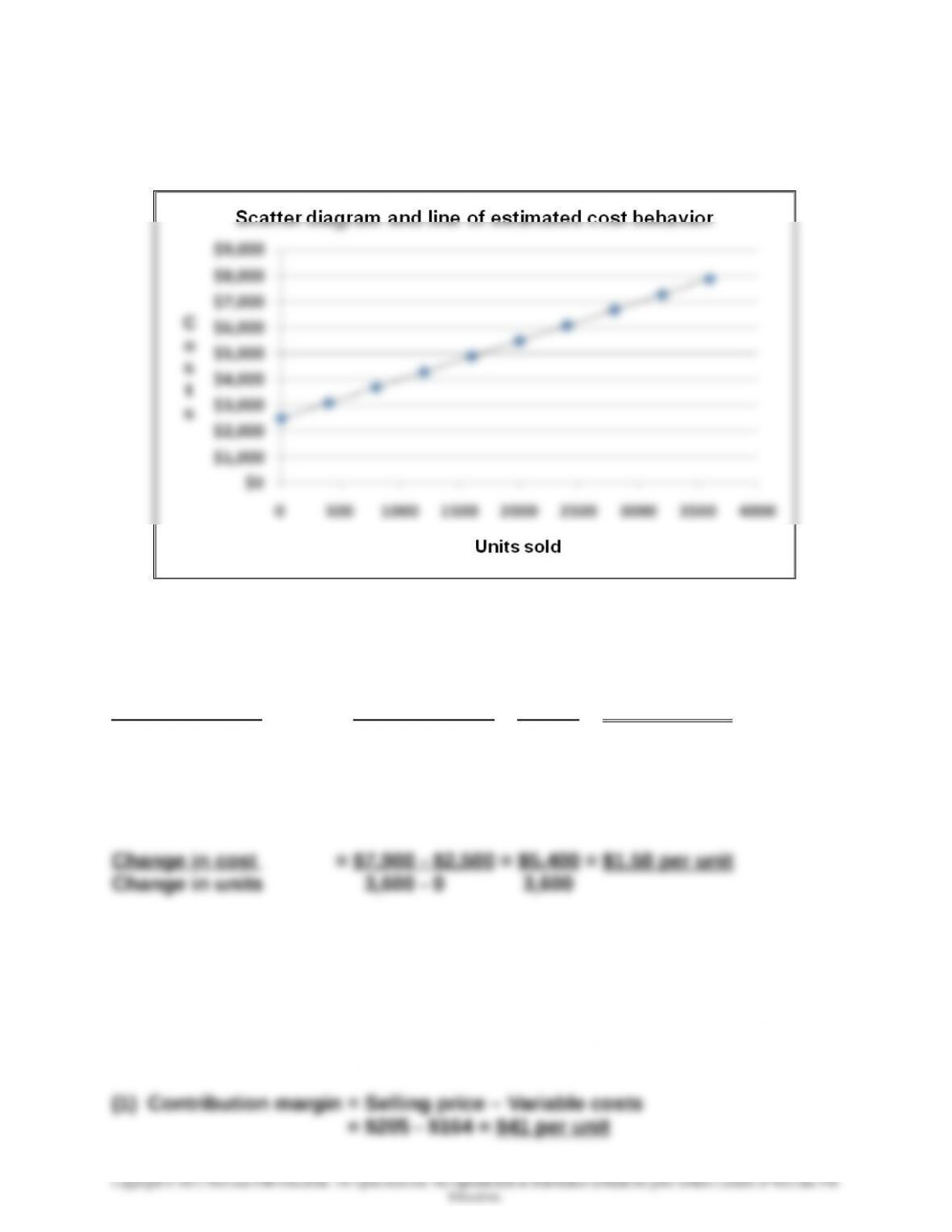

The scatter diagram and line of estimated cost behavior appear below.

Selecting 0 and 2,400 units sold as the activity levels yields $2,500 as the

estimate of fixed costs and the following estimate of variable costs per

unit:

Change in cost = $6,100 – $2,500 = $3,600 = $1.50 per unit

Change in units 2,400 – 0 2,400

Using the high-low method yields $2,500 as the estimate of fixed costs and

variable costs per unit of:

Exercise 21-7A (20 minutes)

Using Excel® to estimate an ordinary least squares regression yields an

intercept of $2,500 and a slope of $1.50. The cost equation is thus $2,500

plus $1.50 per unit sold.Exercise 21-8 (10 minutes)

21-1209

0

$500,00

0

$1,000,0

00

00

$3,500,0

00

$4,000,0

00

0 5,00

0

10,00

0

15,000 20,00

0

25,00

0

Unit

s

Sale

Chapter 21 – Cost-Volume-Profit Analysis

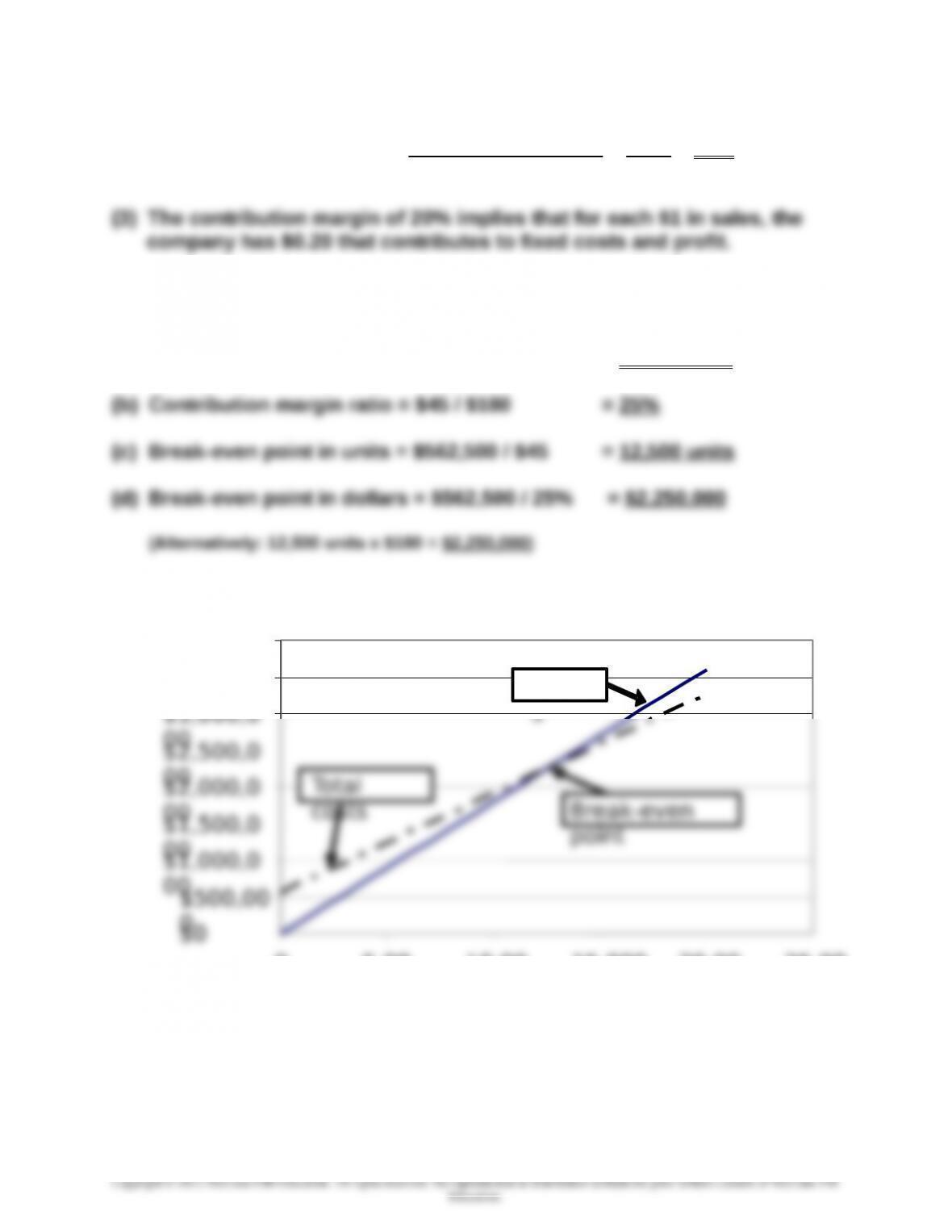

(2) Contribution margin ratio = Contribution margin = $41 = 20%

Sales price $205

Exercise 21-9 (30 minutes)

(a) Contribution margin per unit = $180 – $135 = $45 per unit

Exercise 21-10 (15 minutes)

21-1210

Chapter 21 – Cost-Volume-Profit Analysis

Exercise 21-11 (20 minutes)

1.

BLANCHARD COMPANY

Contribution Margin Income Statement (at Break-Even)

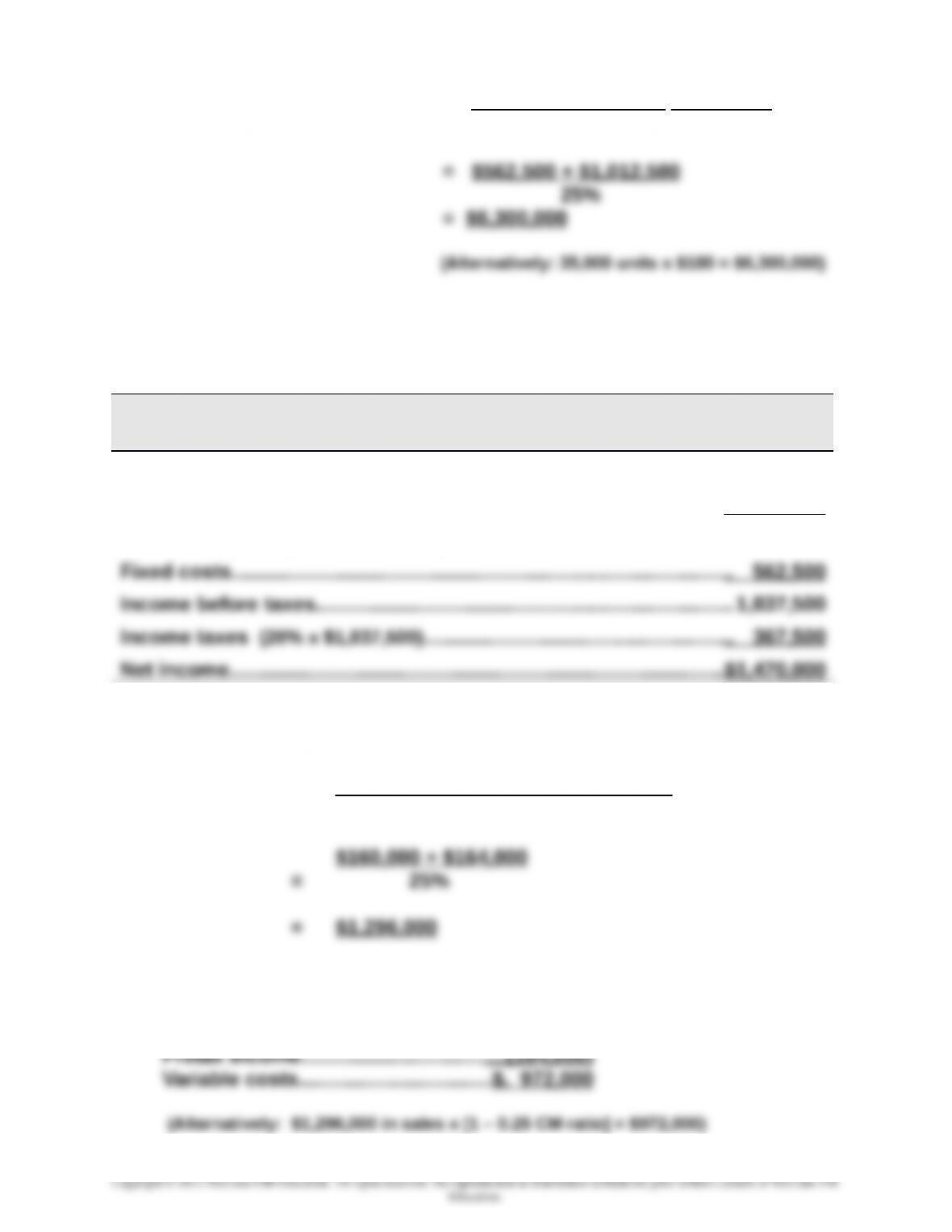

2. Sales (in dollars) to break even with increased fixed costs

Break-even = (Original fixed costs + Additional fixed costs)

Contribution margin ratio

= ($562,500 + $135,000) / 25%

= $2,790,000

Exercise 21-12 (25 minutes)

21-1211

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Fixed Target

costs income

+

Chapter 21 – Cost-Volume-Profit Analysis

2. Dollar sales at target income = costs income

Contribution margin ratio

Exercise 21-13 (20 minutes)

BLANCHARD COMPANY

Forecasted Contribution Margin Income Statement

Sales (40,000 x $200)……………………………………………..………………...$8,000,000

Variable costs (40,000 x $140)……………………..……………..……………. 5,600,000

Contribution margin (40,000 x $60)……………………………………………2,400,000

Exercise 21-14 (10 minutes)

1. Fixed costs + Target pretax income

Dollar sales = Contribution margin ratio

2.

Sales……………………..…..………………...$1,296,000

Fixed costs………………………………..….(160,000)

21-1212

Chapter 21 – Cost-Volume-Profit Analysis

Exercise 21-15 (30 minutes)

(a) Total expected variable costs

= Variable costs per unit x units produced and sold

= $60* x 200,000 units

= $12,000,000

(b) To solve, set up a brief contribution margin income statement

Sales (given)………………………………………………………..…………$17,000,000

Variable costs (from part a)……………………………………………..(12,000,000)

Fixed costs……………………………………………………..……………..( ? )

Pretax income (given)……………………………………………………..$ 1,250,000

Exercise 21-16 (10 minutes)

1. Break-even in units = Fixed costs / Contribution margin per unit

= $324,000 / ($225 – $180) = 7,200 units

Exercise 21-17 (15 minutes)

1. Dollar sales for target income = Fixed costs + Target income

Contribution margin ratio

21-1213

Chapter 21 – Cost-Volume-Profit Analysis

2. Margin of safety (%) = Expected sales – breakeven sales

Expected sales

Exercise 21-18 (15 minutes)

HUDSON CO.

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (9,600 x $225)……………………………………………..………………....$2,160,000

Variable costs (9,600 x $171*)…………………………………………..……… 1,641,600

*Revised variable costs = $180 – $9 = $171 per unit

Exercise 21-19 (10 minutes)

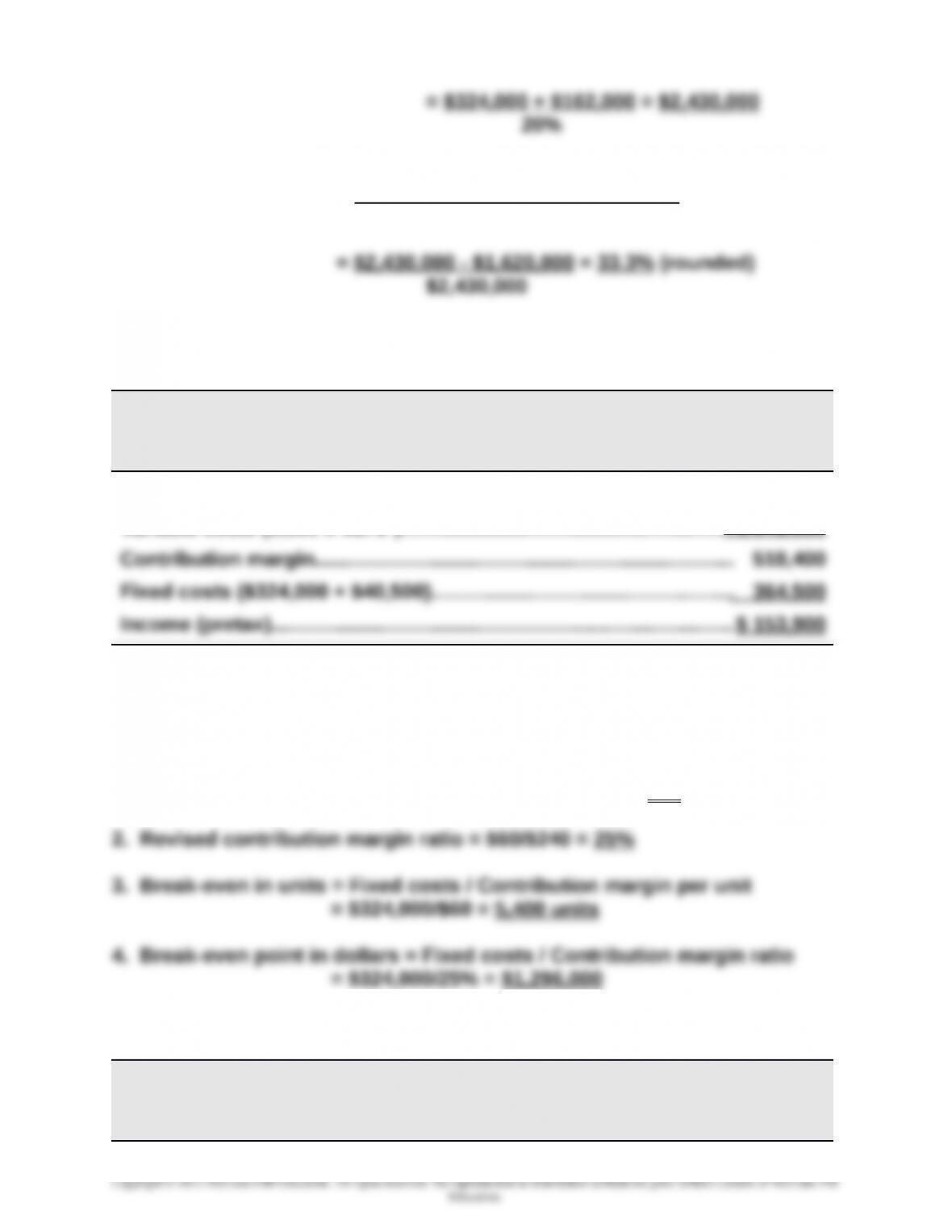

1. Revised contribution margin per unit = $240 – $180 = $60

Exercise 21-20 (15 minutes)

HUDSON CO.

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

21-1214

Chapter 21 – Cost-Volume-Profit Analysis

Sales (11,000 x $225)……………………………………….…………..………….$2,475,000

Variable costs (11,000 x $180)………………………..………………..……… 1,980,000

Exercise 21-21 (20 minutes)

1. Pretax income = Sales – Variable costs – Fixed costs

2. Instructor note: Use equation in Exhibit 21.23;

Unit sales = Fixed costs + Target pretax income

Contribution margin per unit

Exercise 21-22 (25 minutes)

1. Selling price per composite unit

8 windows @ $200 per unit…………………………………..………………....$1,600

2 doors @ $500 per unit…………………………………………..……………… 1,000

Selling price per composite unit………………..…..………………..………$2,600

2. Variable costs per composite unit

21-1215

3. Break-even point in composite units

4. Unit sales of windows and doors at break-even point

Windows: 8 x 1,000 units (from 3)..……….......8,000 units

21-1216

Chapter 21 – Cost-Volume-Profit Analysis

Exercise 21-23 (25 minutes)

1. Selling price per composite unit

5 Easy returns @ $50 each…………………………..……………..………… $ 250

3 Moderate returns @ $125 each………………………………………...…. 375

2 Business returns @ $275 each………………………………………...….

Selling price per composite unit…………………………..………………..

550

$1,175

2. Variable costs per composite unit

3. Break-even point in composite units

4. Unit sales of Easy, Moderate, and Business returns at break-even point

Exercise 21-24 (30 minutes)

Instructor note: This exercise is solved in 3 steps

21-1217

Chapter 21 – Cost-Volume-Profit Analysis

Step 1.

Company A

Contribution Margin Income Statement

Sales (given)……………………………………………..………………..…. $6,000,000

Variable costs [$6,000,000 x (100% – 60%)]…………………….... 2,400,000

Company A’s DOL = Contribution margin in dollars / Pretax income

= $3,600,000 / $1,000,000

= 3.6

Step 2.

Company B

Contribution Margin Income Statement

Sales (given)……………………………………………..………………..…. $4,500,000

Company B’s DOL = Contribution margin in dollars / Pretax income

= $1,125,000 / $750,000

= 1.5

Step 3.

Interpretation: Company A benefits more from a 20% increase in sales.

This is because we expect a 20% increase in sales to yield a 72%

increase in income (computed as 3.6 x 20%). For Company B we expect

21-1218