Exercise 21-6 (20 minutes)

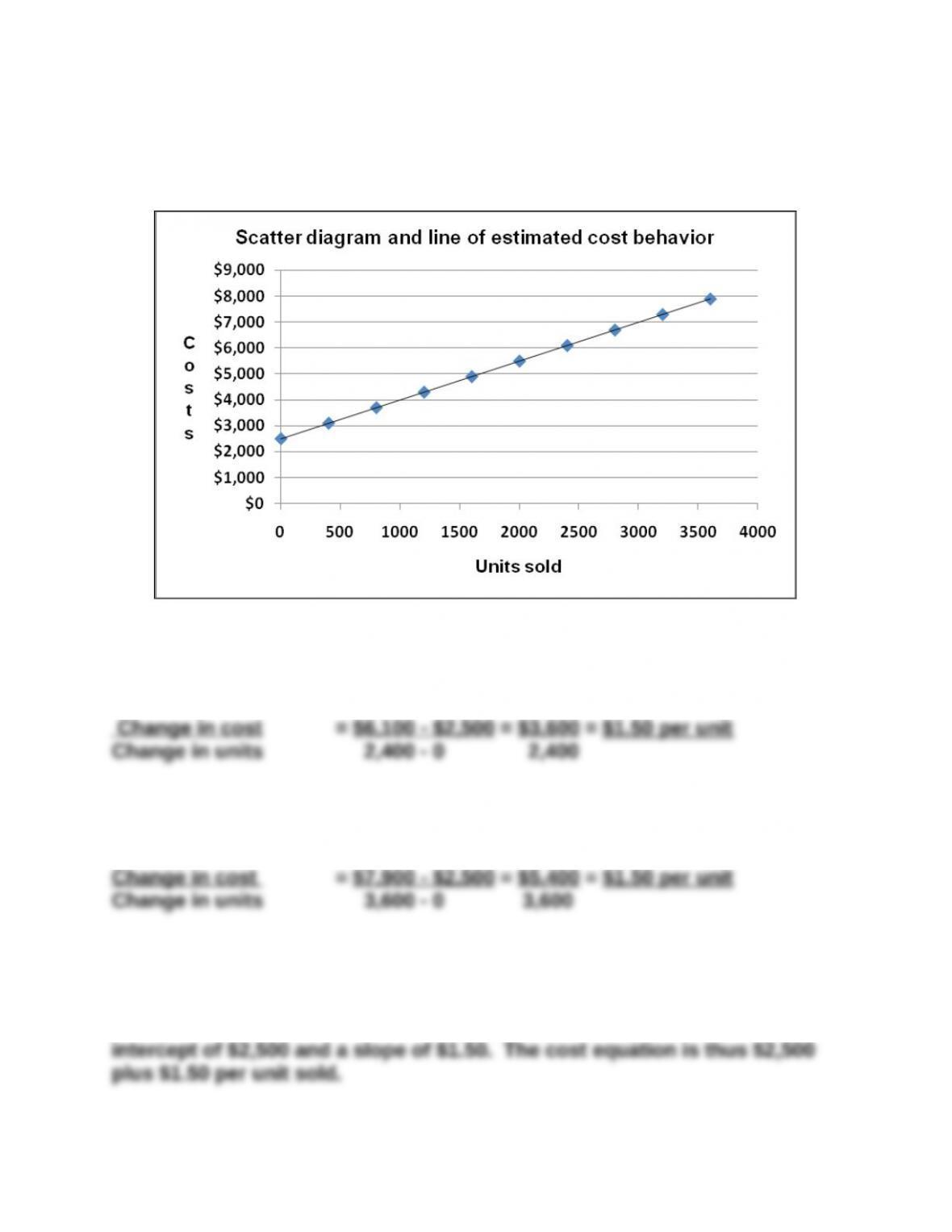

The scatter diagram and line of estimated cost behavior appear below.

Selecting 0 and 2,400 units sold as the activity levels yields $2,500 as the

estimate of fixed costs and the following estimate of variable costs per

unit:

Using the high-low method yields $2,500 as the estimate of fixed costs and

variable costs per unit of:

Exercise 21-7A (20 minutes)

Using Excel® to estimate an ordinary least squares regression yields an

Exercise 21-8 (10 minutes)

(1) Contribution margin = Selling price – Variable costs

(3) The contribution margin of 20% implies that for each $1 in sales, the

company has $0.20 that contributes to fixed costs and profit.

Exercise 21-9 (30 minutes)

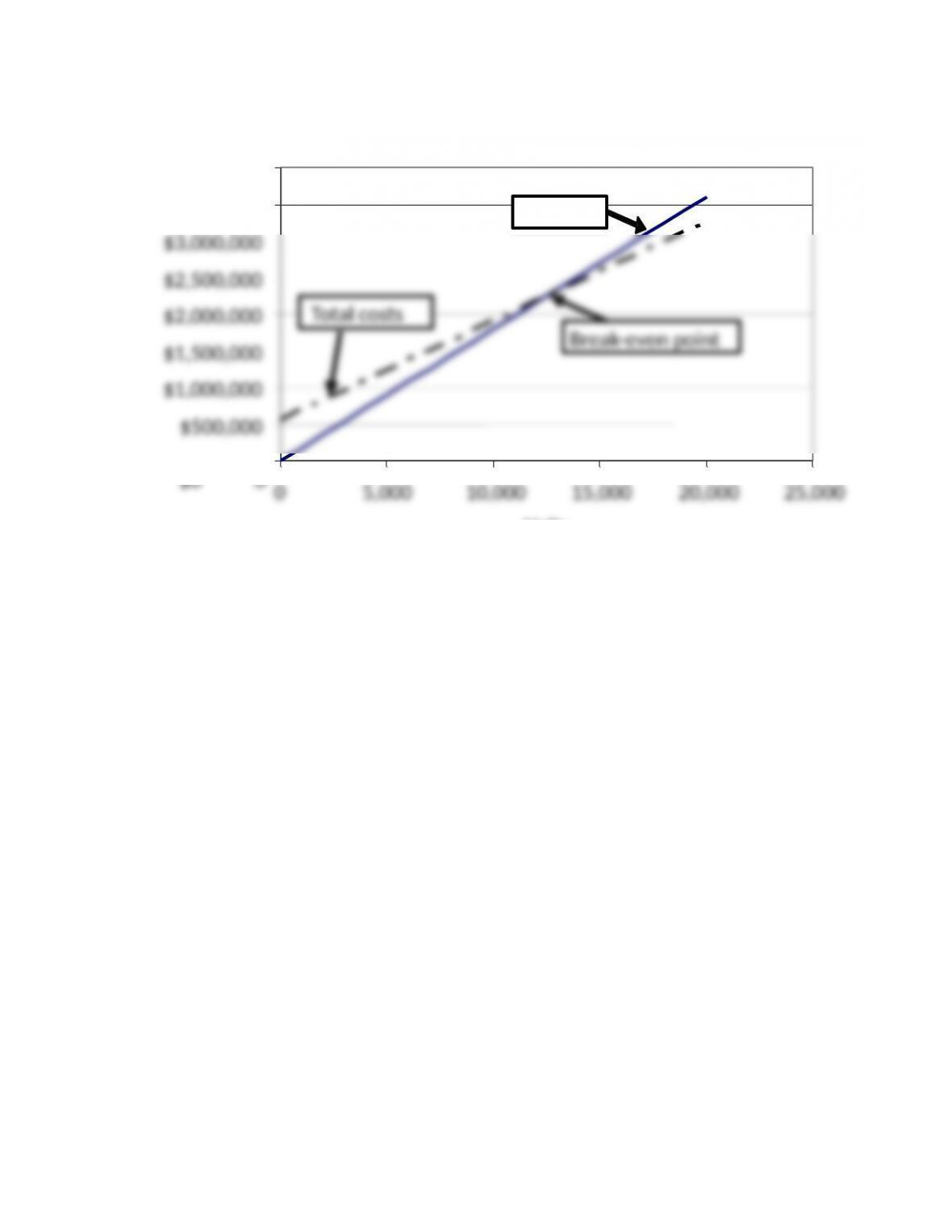

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

Units

Sales

Total costs

Break-even point

Exercise 21-10 (15 minutes)

Exercise 21-11 (20 minutes)

1.

BLANCHARD COMPANY

Contribution Margin Income Statement (at Break-Even)

Sales (12,500 x $180)………………………………………………………………$2,250,000

2. Sales (in dollars) to break even with increased fixed costs

Break-even = (Original fixed costs + Additional fixed costs)

Contribution margin ratio

Exercise 21-12 (25 minutes)

1. Unit sales at target income =

Fixed + Target

2. Dollar sales at target income = costs income

Contribution margin ratio

Exercise 21-13 (20 minutes)

BLANCHARD COMPANY

Forecasted Contribution Margin Income Statement

Sales (40,000 x $200)………………………………………………………………$8,000,000

Variable costs (40,000 x $140)…………………………………………………. 5,600,000

Fixed Target

costs income

Contribution margin/unit

+

Exercise 21-14 (10 minutes)

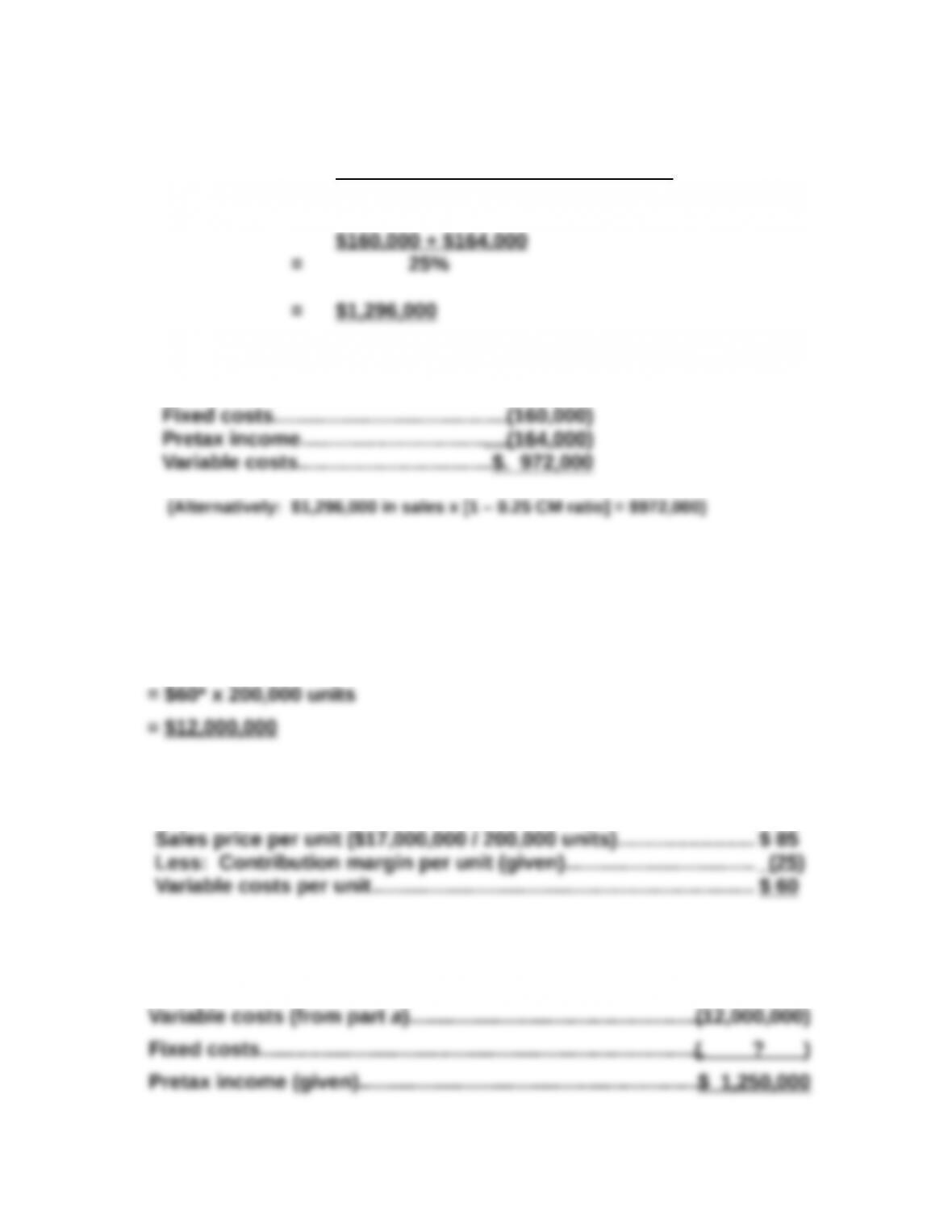

1. Fixed costs + Target pretax income

Dollar sales = Contribution margin ratio

2.

Sales……………………………………………$1,296,000

Exercise 21-15 (30 minutes)

(a) Total expected variable costs

= Variable costs per unit x units produced and sold

*The $60 variable costs per unit is computed by determining (i) sales

price per unit and (ii) subtracting contribution margin per unit:

(b) To solve, set up a brief contribution margin income statement

Sales (given)…………………………………………………………………$17,000,000

Exercise 21-16 (10 minutes)

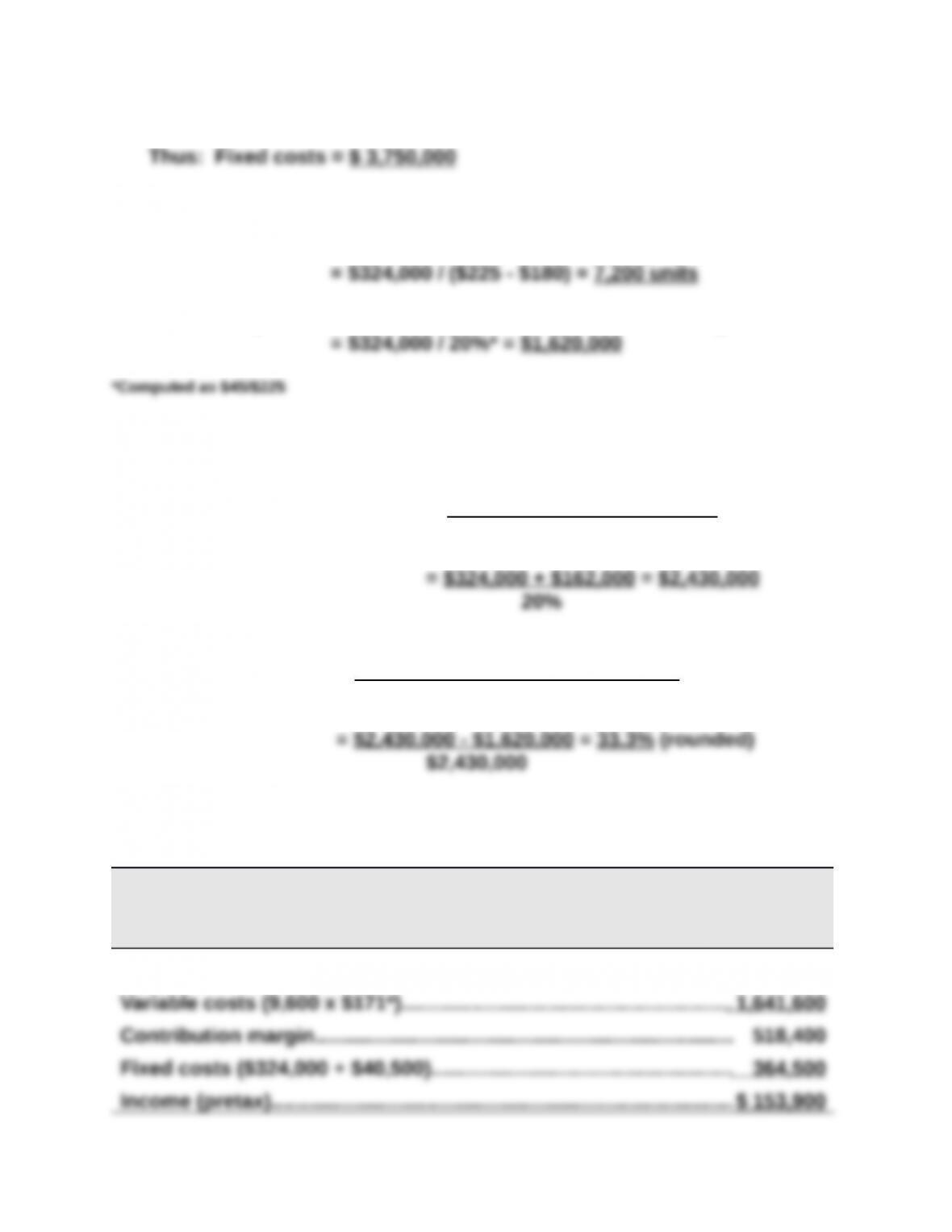

1. Break-even in units = Fixed costs / Contribution margin per unit

2. Break-even point in dollars = Fixed costs / Contribution margin ratio

Exercise 21-17 (15 minutes)

1. Dollar sales for target income = Fixed costs + Target income

Contribution margin ratio

2. Margin of safety (%) = Expected sales – breakeven sales

Expected sales

Exercise 21-18 (15 minutes)

HUDSON CO.

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (9,600 x $225)……………………………………………………………….$2,160,000

Exercise 21-19 (10 minutes)

3. Break-even in units = Fixed costs / Contribution margin per unit

4. Break-even point in dollars = Fixed costs / Contribution margin ratio

Exercise 21-20 (15 minutes)

HUDSON CO.

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (11,000 x $225)………………………………………………………………$2,475,000

Variable costs (11,000 x $180)………………………………………………… 1,980,000

Exercise 21-21 (20 minutes)

1. Pretax income = Sales – Variable costs – Fixed costs

2. Instructor note: Use equation in Exhibit 21.23;

Unit sales = Fixed costs + Target pretax income

Contribution margin per unit

Exercise 21-22 (25 minutes)

1. Selling price per composite unit

8 windows @ $200 per unit…………………………………………………….$1,600

2. Variable costs per composite unit

8 windows @ $125 per unit…………………………………………………….$1,000

3. Break-even point in composite units

Fixed costs .

= Contribution margin per composite unit

4. Unit sales of windows and doors at break-even point