Problem 20-6A (45 minutes)

1. Units in beginning inventory………………………………….. 37,500

2. Equivalent units of production—FIFO

Direct

Equivalent units of production—FIFO Materials Conversion

Units to complete beginning Work in Process

Direct materials (37,500 x 40%)…………….……….….... 15,000

3. Cost per equivalent unit of direct materials and conversion—FIFO

Direct

Cost per equivalent unit—FIFO Materials Conversion

Costs incurred this period……………….……….……….….$ 505,035 $ 396,568

Problem 20-6A (Concluded)

4. Assignment of costs to output of department—FIFO

Costs of goods transferred out

Cost of beginning work in process inventory.…….….

Direct materials………………………………..…….……….….$74,075.00

Conversion……………………………………….……….………. 28,493.00 $ 102,568.00

Direct materials (150,000 EUP x $2.58 per EUP)......387,000.00

Conversion (150,000 EUP x $2.17 per EUP)............. 325,500.00

Total cost of units started and completed..……….…. 712,500.00

Total costs of goods transferred out……………………... 902,593.00

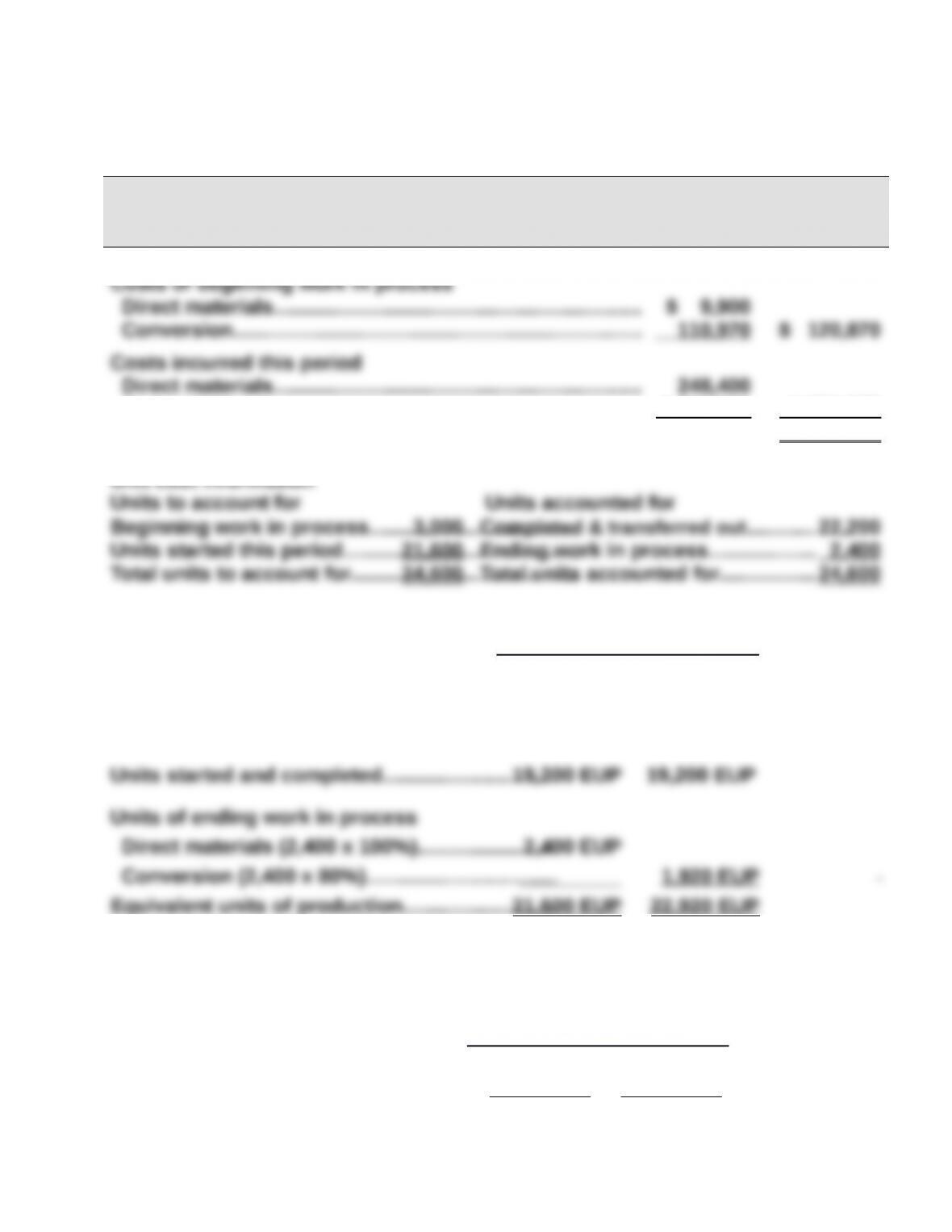

Problem 20-7A (80 minutes)

Part 1

DENGO CO.—Roasting Department

Process Cost Summary – FIFO Method

For Month Ended October 31

Costs Charged to Production

Conversion…………………………………………………………….... 1,082,970 1,331,370

Total costs to account for…………………………………………… $1,452,240

Equivalent units of production

Direct

Materials Conversion

Units to complete beginning WIP

Direct materials (3,000 x 0%)…………………..…… 0 EUP

Conversion (3,000 x 60%)………………..…….……. 1,800 EUP

[Continued on next page]Problem 20-7A (Continued)

Cost per EUP

Direct

Materials Conversion

Costs incurred this period..…............. $ 248,400 $1,082,970

÷ EUP……………………………………..……… ÷ 21,600 ÷ 22,920

Cost per EUP…………………….……….….. $11.50 per

EUP

$47.25 per

EUP

Cost assignment and reconciliation

Costs transferred out

Cost of beginning Work in Process……..….……….….. $ 120,870

Cost to complete beginning Work in Process

Costs of ending Work in Process

Direct materials (2,400 EUP x $11.50 per EUP)....... 27,600

Conversion (1,920 EUP x $47.25 per EUP).............. 90,720 118,320

Total costs accounted for…………..….……….……….….. $1,452,240

Part 2

Oct. 31 Work in Process Inventory—Blending……………………………

1,333,920

departments.

Problem 20-7A (Concluded)

Part 3

If equivalent units of production for a production department’s ending

inventory for October are understated, then total equivalent units of

production is also understated. This means the cost per equivalent unit for

PROBLEM SET B

Problem 20-1B (45 minutes)

Part 1: Cost of goods transferred and cost of goods sold

Beginning work in process inventory…………………………….…….….. $156,000

Direct materials used in production……………………………………..….. 120,000

Direct labor used in production…………………………………………..…... 350,000

Overhead applied (75% of direct labor cost)…………………….………. 262,500

Total production costs…………………………………………………………….. 888,500

Less ending finished goods inventory……………………….……….…… (198,000)

Cost of goods sold (b) ………………………………………………..……….…. $600,500

Part 2: Summary journal entries

a.

June 30 Raw Materials Inventory …………………………….……….…200,000

Accounts Payable ……………………………………………. 200,000

Raw Materials Inventory ……………….….……….…….. 42,000

Used indirect materials.