Chapter 20 – Process Costing

Exercise 20-22 (10 minutes)

1. Work in Process Inventory……………………..…….…….….75,000

Factory Payroll Payable……………………………..…….. 75,000

Incurred direct labor costs.

Exercise 20-23 (5 minutes)

1. Factory Overhead …………………………………………..……..38,750

Cash …………………………………………………………….…. 38,750

Incurred and paid overhead costs.

Exercise 20-24 (5 minutes)

1. Finished Goods Inventory………………………..…….……...135,600

Work in Process Inventory-Assembly……………….. 135,600

Transfer goods from production to finished goods.

Exercise 20-25 (25 minutes)

20-1123

Chapter 20 – Process Costing

1.

Oct. 31 Work in Process Inventory…………………………….…….…522,000

Raw Materials Inventory………………..….…….…….…. 522,000

Direct materials used in production.

2.

4.

Oct. 31 Finished Goods Inventory ………………………..…….……..595,000

Work in Process Inventory……………………….…….… 595,000

Transfer goods from production to finished

goods.

5.

Exercise 20-26 (25 minutes)

a. Purchased raw materials on credit at a cost of $52,000.

b. Used direct materials costing $42,000 in production.

20-1124

Chapter 20 – Process Costing

h. Applied overhead to production at the rate of 105% ($33,600/$32,000) of

direct labor cost.

Exercise 20-27 (10 minutes)

A hybrid costing system contains features of both process costing and job

order costing. A hybrid system of processes requires a hybrid costing

system to properly cost products or services.

PROBLEM SET A

Problem 20-1A (45 minutes)

Part 1: Cost of goods transferred and cost of goods sold

Beginning work in process inventory……………………….…….. $ 435,000

Direct materials used in production…………………………….….. 157,500

20-1125

Chapter 20 – Process Costing

Beginning finished goods inventory …………………………..….. $ 633,000

Plus goods transferred from production ………………….…….. 1,754,500

Part 2: Summary journal entries

a.

May 31 Raw Materials Inventory …………………………….…….……250,000

Accounts Payable ……………………………………………. 250,000

Purchased raw materials.

20-1126

Chapter 20 – Process Costing

Problem 20-1A (Continued)

d.

May 31 Work in Process Inventory ……………………….….…….….780,000

Factory Payroll Payable……………………………..…….. 780,000

Incurred direct labor costs.

e.

g.

May 31 Factory Overhead …………………………………………….…...87,000

Other Accounts ……………………………………………….. 87,000

Incurred other overhead costs.

h.

j.

May 31 Accounts Receivable …………………………..….…….……...2,500,000

Sales ……………………………………………….…….…….…. 2,500,000

Sold finished goods.

May 31 Cost of Goods Sold ………………………………………..….….1,782,500

Finished Goods Inventory …………………..…….…….. 1,782,500

To record cost of goods sold for May.

20-1127

Chapter 20 – Process Costing

Problem 20-2A (50 minutes)

Part 1

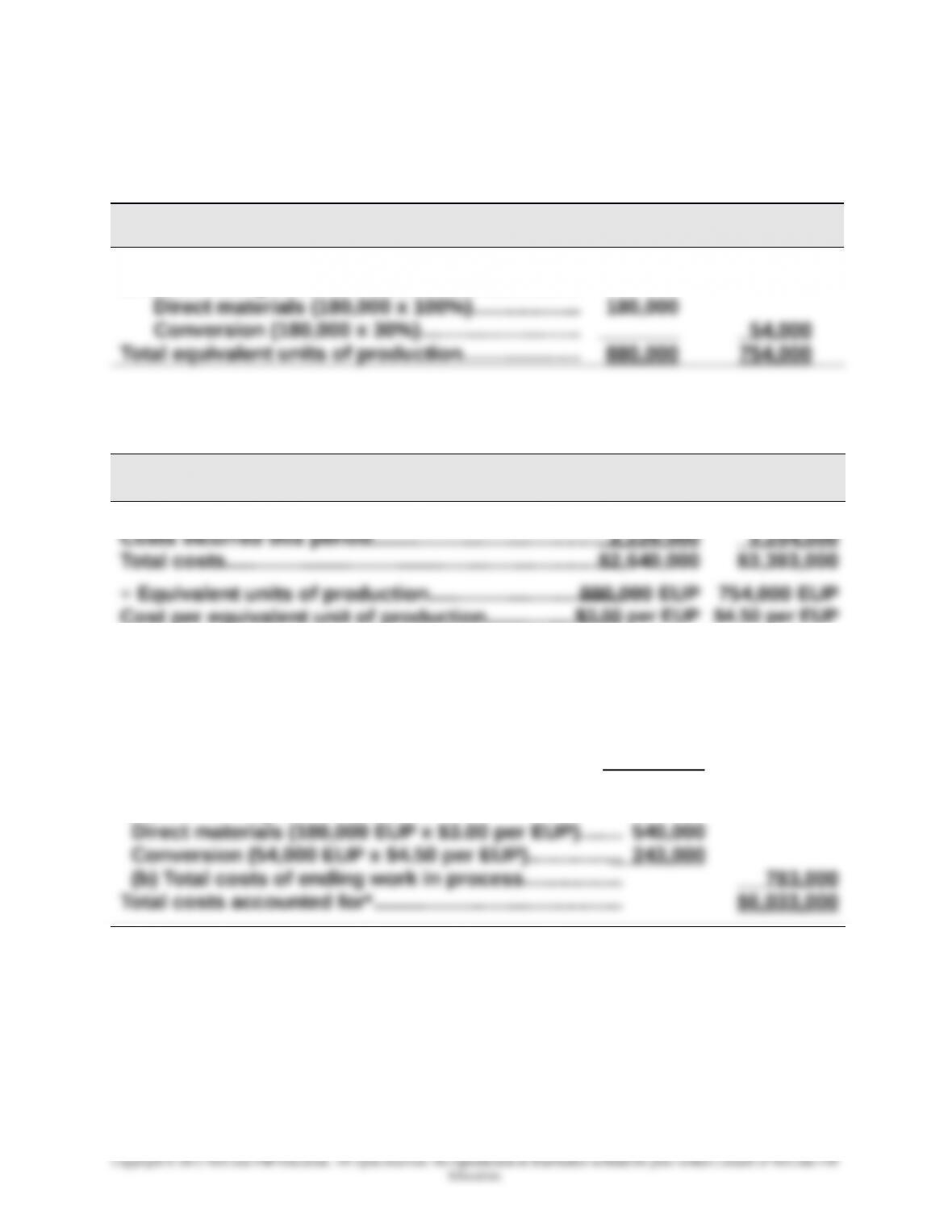

(a) and (b) Equivalent units with respect to direct materials and conversion

Direct

Equivalent units of production (EUP) Materials Conversion

Units completed and transferred out……………….. 700,000 700,000

Units of ending Work in Process…..…….…….…….

Part 2

Cost per equivalent unit of production

Direct

Materials Conversion

Costs of beginning Work in Process…..…….…….….....$ 420,000 $ 139,000

Part 3 Assigning product costs to units

Costs transferred out

Direct materials (700,000 EUP x $3.00 per EUP).......$2,100,000

Conversion (700,000 EUP x $4.50 per EUP).............. 3,150,000

(a) Total costs transferred out……..….…….…….…….… $5,250,000

Costs of ending work in process

*This equals the sum of the total direct materials cost and the

total conversion costs ($2,640,000 + $3,393,000 = $6,033,000).

20-1128

Chapter 20 – Process Costing

Problem 20-2A (Concluded)

Part 4

MEMORANDUM

TO:

FROM:

DATE:

RE: Percentage of Completion Error Analysis

If the units in ending inventory are 60% complete instead of 30% with

respect to conversion, the number of equivalent units in ending inventory

with respect to conversion is understated, and the total equivalent units

Regarding financial statements, this error causes an overstatement of cost

of goods sold and an understatement of net income on the income

20-1129

Chapter 20 – Process Costing

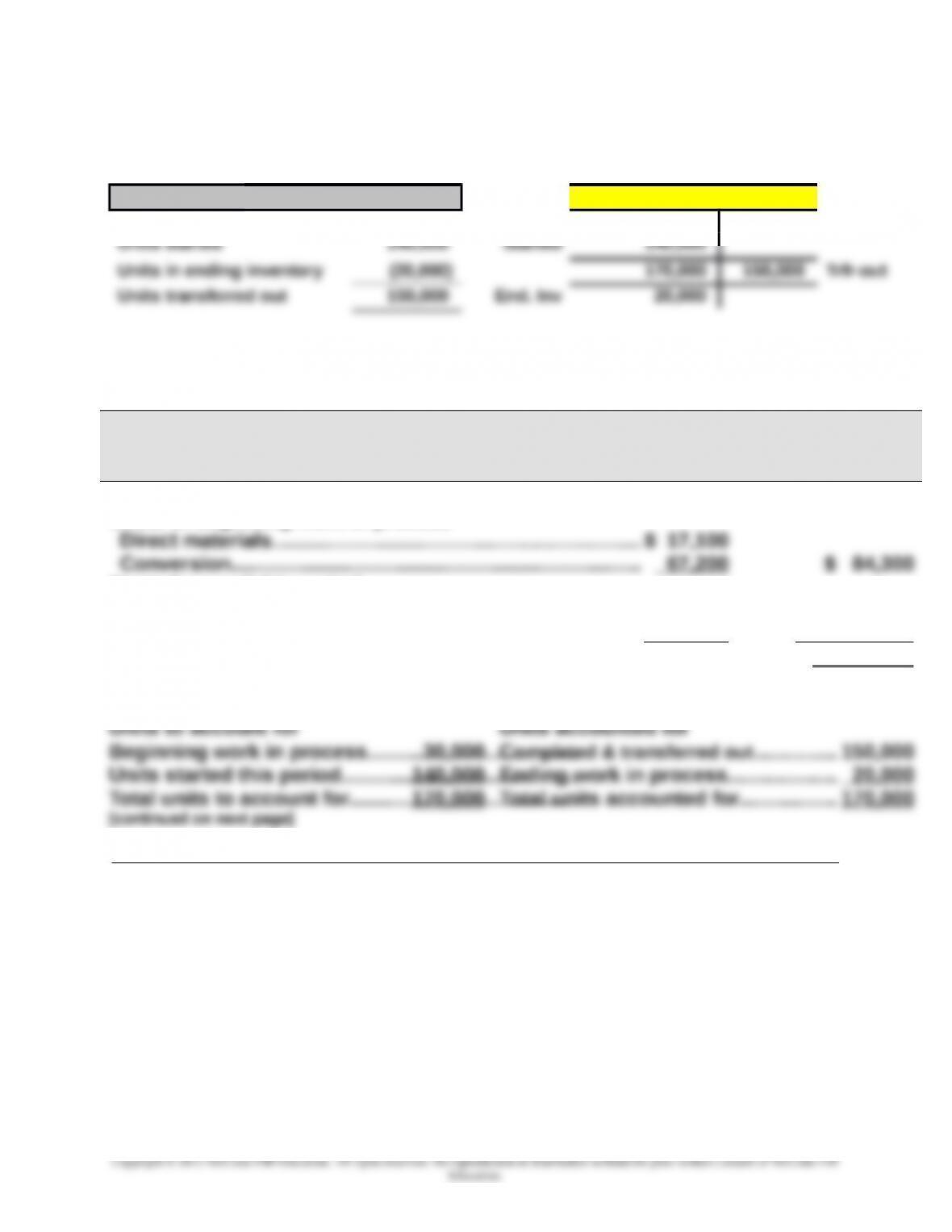

Problem 20-3A (75 minutes)

Part 1

Weighted average

Units Fast Co. – units

Units in Beg. inventory 30,000 Beg. Inv 30,000

FAST CO.

Process Cost Summary – Weighted Average Method

For the month ended October 31

Costs Charged to Production

Costs of beginning work in process

Costs incurred this period

Direct materials……………………………..….…….……….……... 144,400

Conversion costs………………………………..….……….…….… 862,400 1,006,800

Total costs to account for…………………………………………… $1,091,100

Unit cost information

20-1130