Problem 20-2A (50 minutes)

Part 1

(a) and (b) Equivalent units with respect to direct materials and conversion

Direct

Equivalent units of production (EUP) Materials Conversion

Units completed and transferred out………………. 700,000 700,000

Units of ending Work in Process……………………..

Part 2

Cost per equivalent unit of production

Direct

Materials Conversion

Costs of beginning Work in Process………………………$ 420,000 $ 139,000

Part 3 Assigning product costs to units

Costs transferred out

Direct materials (700,000 EUP x $3.00 per EUP)…….$2,100,000

Conversion (700,000 EUP x $4.50 per EUP)……..…… 3,150,000

(a) Total costs transferred out…………………………….. $5,250,000

Costs of ending work in process

Problem 20-2A (Concluded)

Part 4

MEMORANDUM

TO:

FROM:

DATE:

RE: Percentage of Completion Error Analysis

If the units in ending inventory are 60% complete instead of 30% with

respect to conversion, the number of equivalent units in ending inventory

Regarding financial statements, this error causes an overstatement of cost

of goods sold and an understatement of net income on the income

statement for November. On the November 30 balance sheet, the Work in

Process inventory and retained earnings are understated; therefore total

assets and equity are also understated.

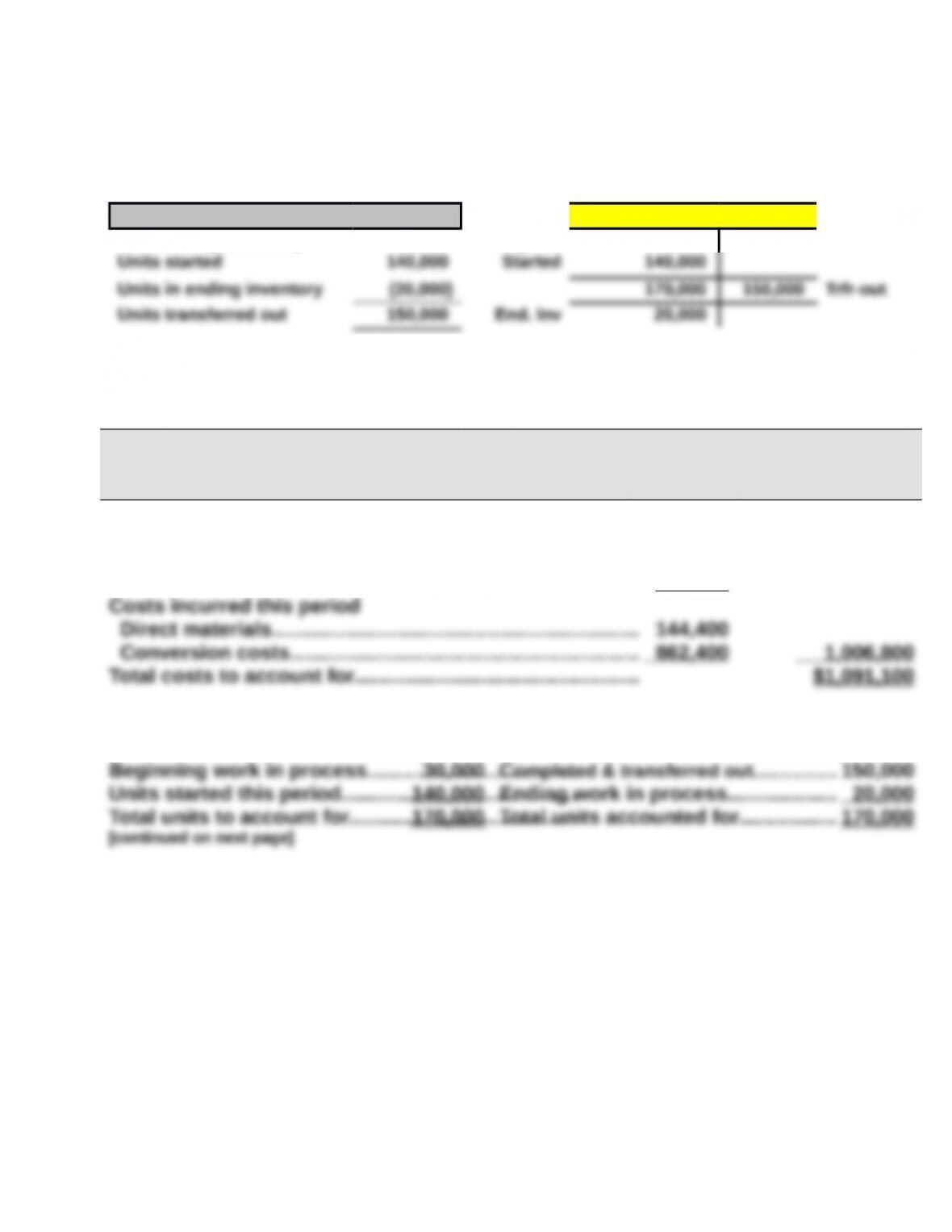

Problem 20-3A (75 minutes)

Part 1

Weighted average

Units Fast Co. – units

Units in Beg. inventory 30,000 Beg. Inv 30,000

FAST CO.

Process Cost Summary – Weighted Average Method

For the month ended October 31

Costs Charged to Production

Costs of beginning work in process

Direct materials………………………………………………………. $ 17,100

Conversion…………………………………………………………….. 67,200 $ 84,300

Unit cost information

Units to account for Units accounted for

Problem 20-3A (concluded)

Equivalent units of production

Direct

Materials Conversion

Units completed & transferred out….. 150,000 EUP 150,000 EUP

Units of ending work in process

Cost per EUP

Direct

Materials Conversion

Cost of beginning work in process….. $17,100 $67,200

Cost assignment and reconciliation

Costs transferred out

Direct materials (150,000 EUP x $0.95 per EUP)..… $142,500

Part 2

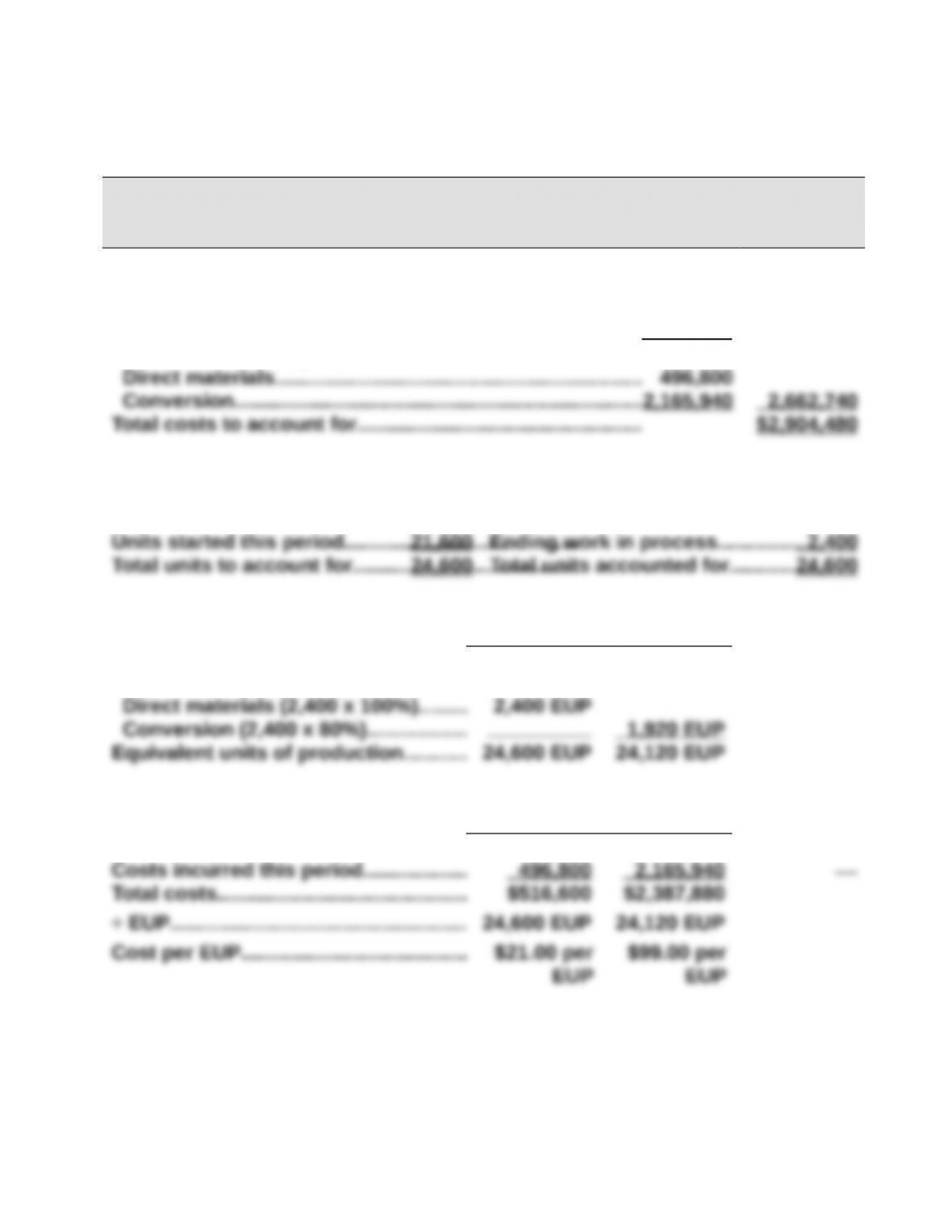

Problem 20-4A (80 minutes)

Part 1

TAMAR CO.

Process Cost Summary – Weighted Average Method

For Month Ended May 31

Costs Charged to Production

Costs of beginning work in process

Direct materials……………………………………………………….$ 19,800

Conversion…………………………………………………………….. 221,940 $ 241,740

Costs incurred this period

Unit cost information

Units to account for Units accounted for

Beginning work in process………………………………3,000 Completed & transferred out…………22,200

Equivalent units of production

Direct

Materials Conversion

Units completed & transferred out……. 22,200 EUP 22,200 EUP

Units of ending work in process………

Cost per EUP

Direct

Materials Conversion

Cost of beginning work in process..... $ 19,800 $ 221,940

[Continued on next page]

Problem 20-4A (Concluded)

Cost assignment and reconciliation

Costs transferred out

Direct materials (22,200 EUP x $21.00 per EUP)……………..$ 466,200

Part 2

May 31 Finished Goods Inventory……………………………………..2,664,000

Part 3

3a. Two major estimates are the: i) overhead allocation rate, and ii)

percentage of completion for materials and conversion.

3b. Management might want an overhead allocation rate that assigns the

least amount of overhead applied to their respective production