Chapter 20 – Process Costing

Exercise 20-12 (30 minutes)

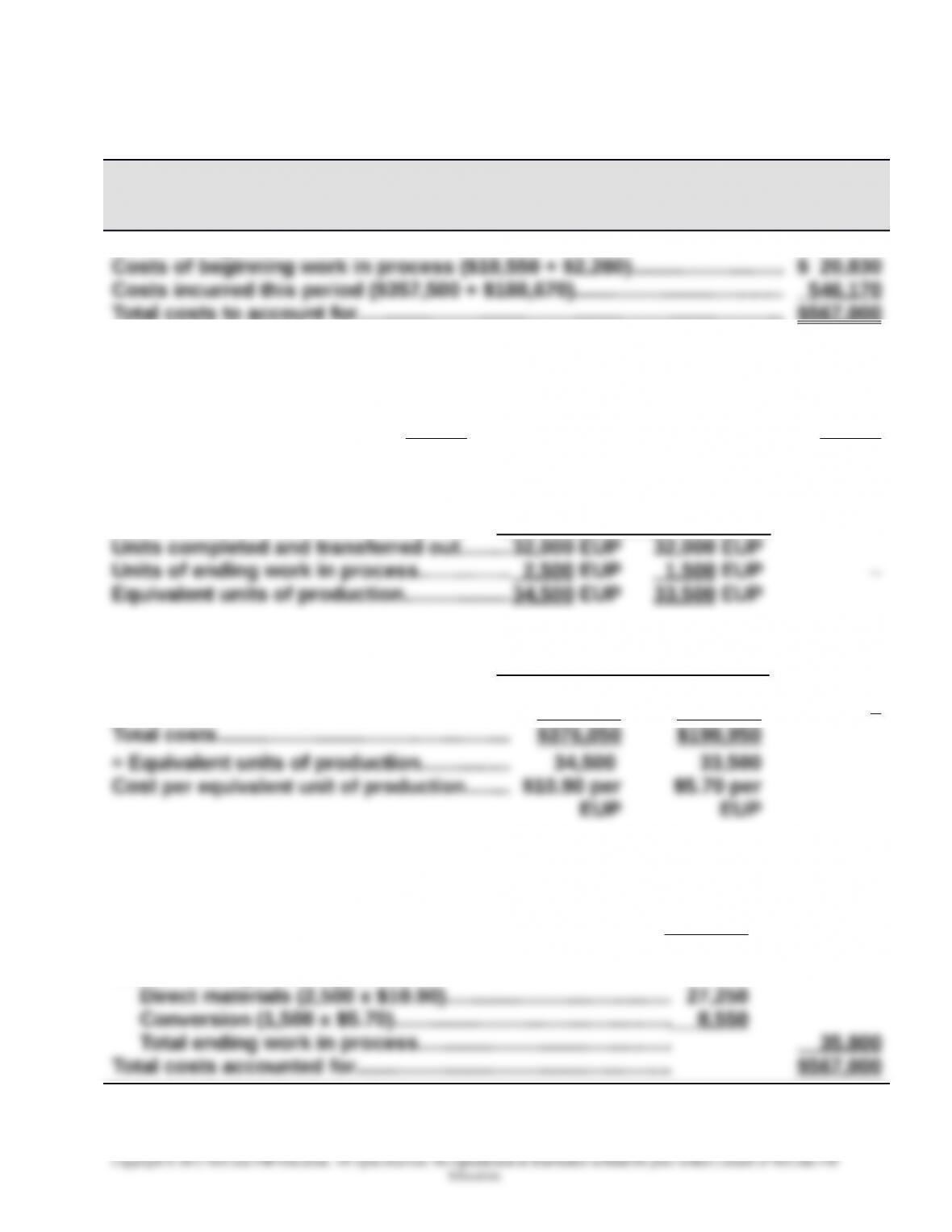

ASHAD COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended July 31

Costs Charged to Production

Unit Information

Units to Account For Units Accounted For

Beginning work in process………………..

2,000 Completed & transferred out…………………………………….……………………......................

32,000

Units started this period…………………….

32,500 Ending work in process…………………………………………..…………………………….............

2,500

Total units to account for….……………….

34,500 Total units accounted for………………………………………………………………………………....

34,500

Equivalent Units of Production (EUP)

Direct

Materials Conversion

Cost per EUP

Direct

Materials Conversion

Costs of beginning work in process………. $ 18,550 $ 2,280

Costs incurred this period…………….………. 357,500 188,670

Cost per equivalent unit of production…….. $10.90 per

EUP

$5.70 per

EUP

Cost Assignment and Reconciliation

Costs transferred out

Direct materials (32,000 x $10.90)…………………….………….$348,800

Conversion (32,000 x $5.70)…………………….…………………. 182,400

Total transferred out $531,200

Cost of ending work in process

Exercise 20-13 (40 minutes)

20-1123

Chapter 20 – Process Costing

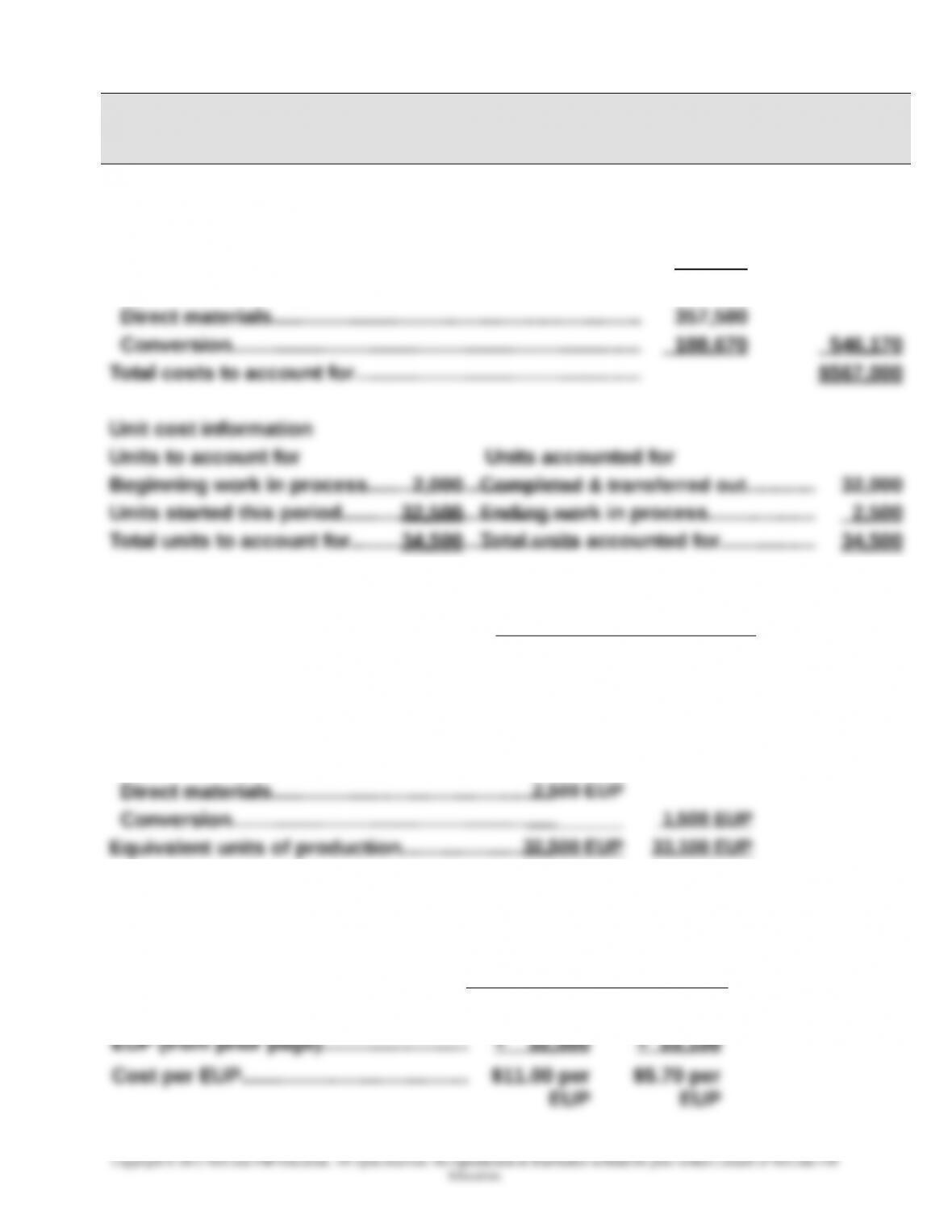

ASHAD COMPANY

Process Cost Summary – FIFO Method

For Month Ended July 31

Costs Charged to Production

Costs of beginning work in process

Direct materials……………………………..………………………… $ 18,550

Conversion…………………………………………………………….... 2,280 $ 20,830

Costs incurred this period

Equivalent units of production

Direct

Materials

Conversion

Units to complete beginning WIP

Direct materials (2,000 x 0%)…………………..…… 0 EUP

Conversion (2,000 x 80%)………………..………….. 1,600 EUP

Units started and completed……………..…………..

30,000 EUP 30,000 EUP

Units of ending work in process

[Continued on next page]Exercise 20-13 (Concluded)

Cost per EUP

Direct

Materials

Conversio

n

Costs incurred this period..…............. $ 357,500 $ 188,670

Cost per EUP…………………………………. $11.00 per

EUP

$5.70 per

EUP

20-1124

Chapter 20 – Process Costing

Cost assignment and reconciliation

Costs of units started and completed this period

Direct materials (30,000 EUP x $11.00 per EUP)..... 330,000

Conversion (30,000 EUP x $5.70 per EUP).............. 171,000 501,000

Total cost of work finished this period………………… 530,950

Exercise 20-14 (30 minutes)

Part 1: Cost of goods transferred and cost of goods sold

Weaving Sewing Finished

Department Department Goods

Beginning inventory…………………………….. $ 300,000 $ 570,000 $1,266,000

Direct materials…………………………………… 240,000 75,000

Direct labor…………………………………………. 1,200,000 360,000

Less ending inventory—Sewing ..…….... (700,000)

TRANSFERRED TO FINISHED GOODS (b) ........ $3,215,000 3,215,000

Less ending inventory—Finished goods.... (1,206,000)

20-1125

Chapter 20 – Process Costing

COST OF GOODS SOLD (c) …………………..….. $3,275,000

Part 2: Summary journal entries.

June 30 Accounts Receivable …………………………………………….4,000,000

Sales ………………………………………………..…………….. 4,000,000

Sold finished goods.

Exercise 20-15 (25 minutes)

Summary journal entries (all dated June 30)

a. Raw Materials Inventory ………………………………………..500,000

Accounts Payable ……………………………………………. 500,000

Purchased raw materials.

d. Work in Process Inventory—Weaving ………………….…1,200,000

Work in Process Inventory—Sewing ………………..…….360,000

Factory Payroll Payable …………………………….…….. 1,560,000

20-1126

Chapter 20 – Process Costing

Used direct labor.

Incurred other overhead costs.

g. Work in Process Inventory—Weaving ………………….…960,000

Work in Process Inventory—Sewing ………………..…….540,000

Factory Overhead…………………………………………….. 1,500,000

Applied overhead using predetermined

rates.

Exercise 20-16 (25 minutes)

ELLIOTT COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended March 31

Costs Charged to Production

Costs of beginning work in process

Direct materials……………………………..………………………… $ 2,500

Conversion…………………………………………………………….… 6,360 $ 8,860

Unit information

Units to account for Units accounted for

Beginning work in process…………….…………………2,000 Completed & transferred out..………...17,000

Equivalent units of production

Direct

Materials Conversion

20-1127

Education.

Chapter 20 – Process Costing

Units completed & transferred out..... 17,000 EUP 17,000 EUP

Units of ending work in process

Direct materials (5,000 x 100%)........ 5,000 EUP

Conversion (5,000 x 35%)……………… __________ 1,750 EUP

Equivalent units of production........... 22,000 EUP 18,750 EUP

Cost per EUP

Direct

Materials Conversion

[Continued on next page]

20-1128