Chapter 20 – Process Costing

Exercise 20-4 (30 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

Units of

Product

2. Beginning inventory is 40% complete with respect to materials.

Ending inventory is 75% complete with respect to materials.

Units of

EUP for Materials Product

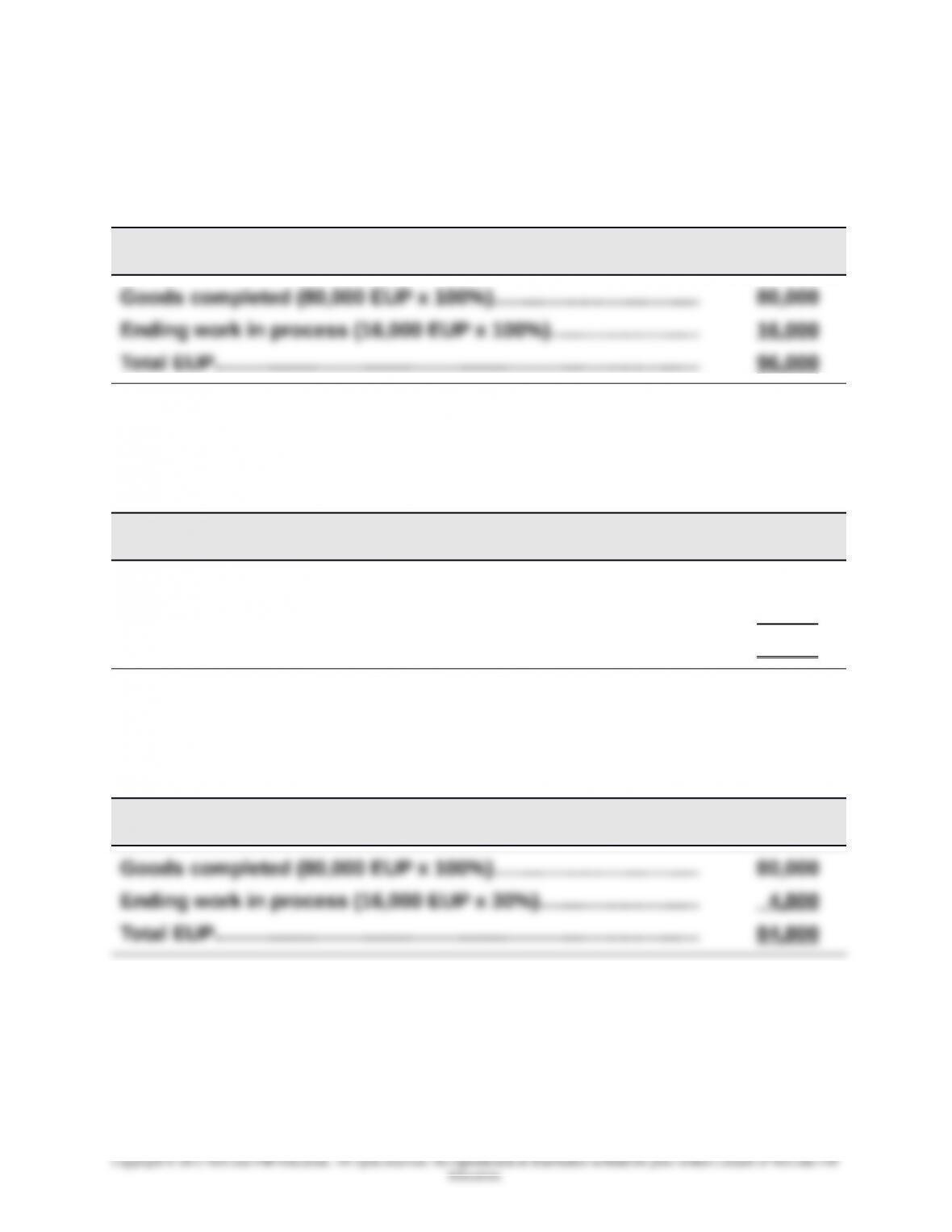

Goods completed (80,000 EUP x 100%)………….………….………. 80,000

Ending work in process (16,000 EUP x 75%)…..….………….…… 12,000

Total EUP……………………………………………………..…….……….……. 92,000

3. Beginning inventory is 60% complete with respect to materials.

Ending inventory is 30% complete with respect to materials.

Units of

EUP for Materials Product

20-1123

Chapter 20 – Process Costing

Exercise 20-5 (30 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

Units of

Product

To complete beginning work in process (24,000 EUP x 0%)......... 0

2. Beginning inventory is 40% complete with respect to materials.

Ending inventory is 75% complete with respect to materials.

Units of

EUP for Materials Product

To complete beginning work in process (24,000 EUP x 60%)....... 14,400

3. Beginning inventory is 60% complete with respect to materials.

Ending inventory is 30% complete with respect to materials.

Units of

EUP for Materials Product

To complete beginning work in process (24,000 EUP x 40%)....... 9,600

20-1124

Chapter 20 – Process Costing

Exercise 20-6 (30 minutes)

1.

Equivalent units of production—Weighted average

Direct

Materials Conversion

Units completed & transferred out (295,000 x 100%)...........295,000 295,000

Units of ending work in process

2.

Cost per equivalent unit—Weighted average

Direct

Materials Conversion

Costs of beginning work in process………………………... $ 44,800 $ 15,300

Costs incurred this period………………………………….…… 1,231,200 896,700

3.

Cost assignment—Weighted average

Costs of units transferred out

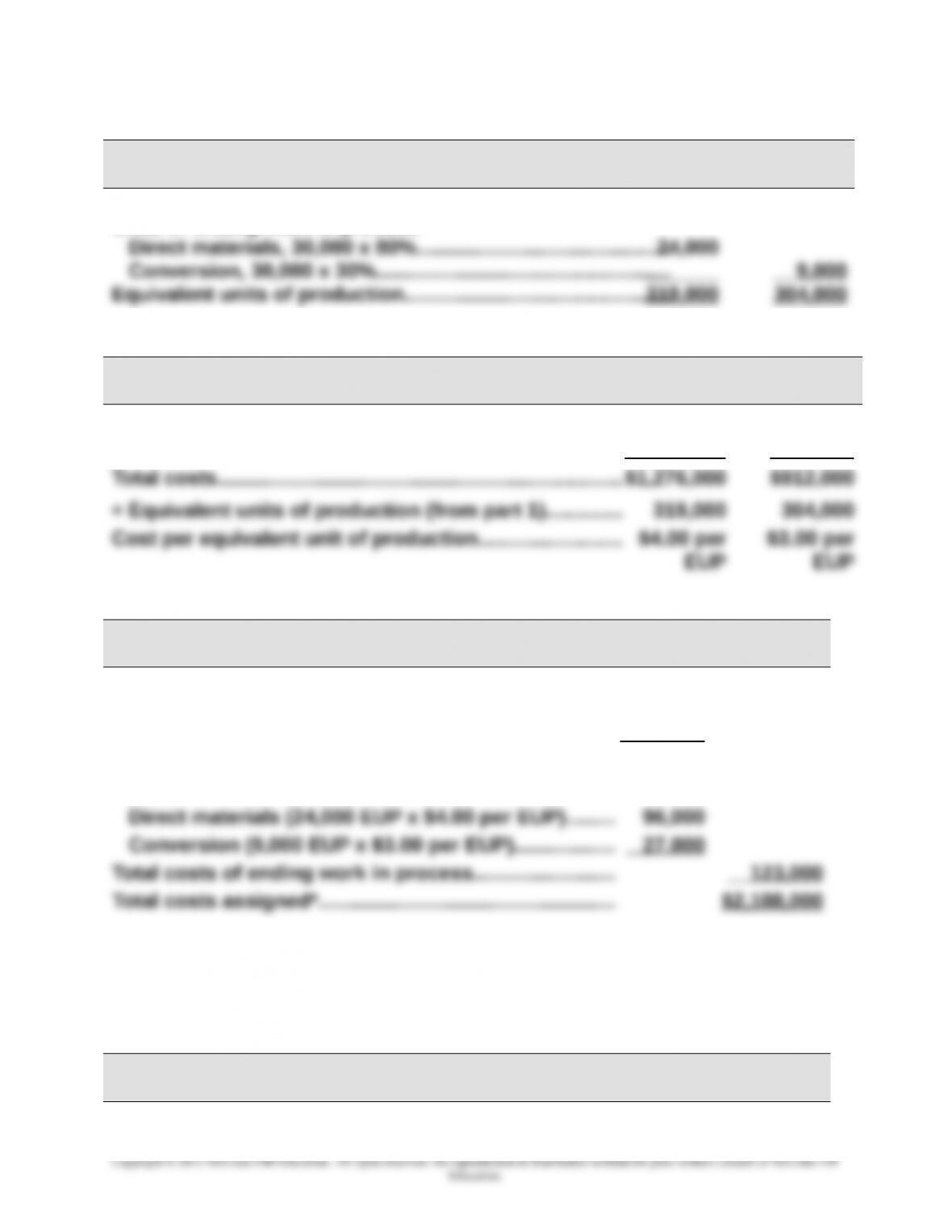

Direct materials (295,000 EUP x $4.00 per EUP)......$1,180,000

Conversion (295,000 EUP x $3.00 per EUP)………….. 885,000

Total costs transferred out…………………….….……….….. $2,065,000

Costs of ending work in process

*Equals costs to account for of $2,188,000, computed as $60,100 + $1,231,200 + $896,700

Exercise 20-7 (30 minutes)

1.

Equivalent units of production—FIFO

Direct

Materials Conversion

20-1125

Chapter 20 – Process Costing

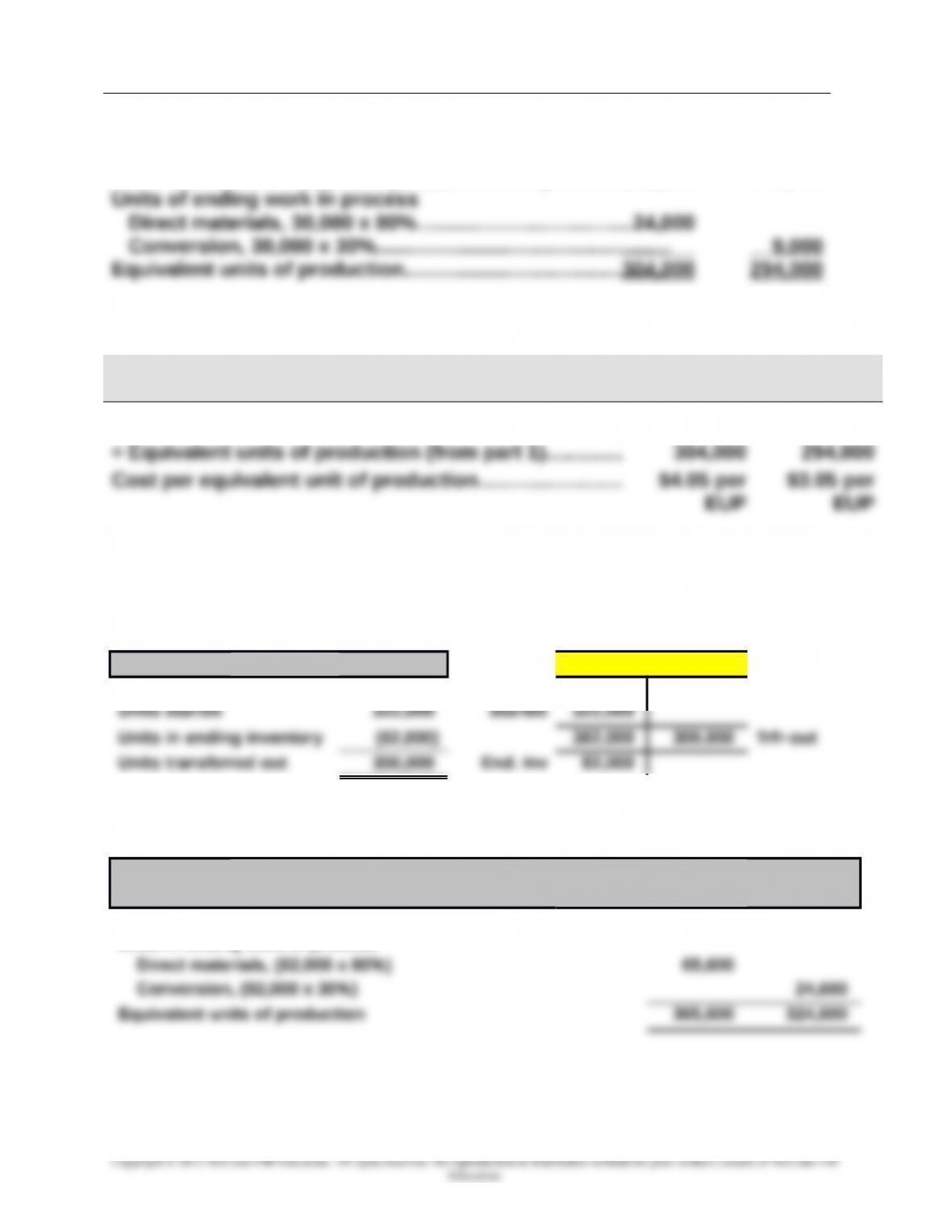

Units to complete beginning work in process

Direct materials (25,000 x 40%)……………………………………..

Conversion (25,000 x 60%)……………………………….…….…….

Units started and completed (270,000 x 100%).…………........

10,000

270,000

15,000

270,000

2.

Cost per equivalent unit—FIFO

Direct

Materials Conversion

Costs incurred this period………………………………….…… $1,231,200 $896,700

Exercise 20-8 (20 minutes)

1. Units transferred out

Units Dept. 1 – units

Units in Beg. inventory 60,000 Beg. Inv 60,000

2. EUP

Equivalent units of production – weighted-average

Direct

Materials Conversion

Units completed & transferred out (300,000 x 100%)……… 300,000 300,000

Units in ending work in process

Exercise 20-9 (20 minutes)

20-1126

Chapter 20 – Process Costing

1. Cost per EUP

Cost per equivalent unit – weighted-average

Direct

Materials Conversion

Costs of beginning inventory $118,472 $48,594

Costs incurred this period 850,368 649,296

Exercise 20-9 (continued)

2.

Cost assignment and reconciliation – weighted-average

Costs of units transferred out

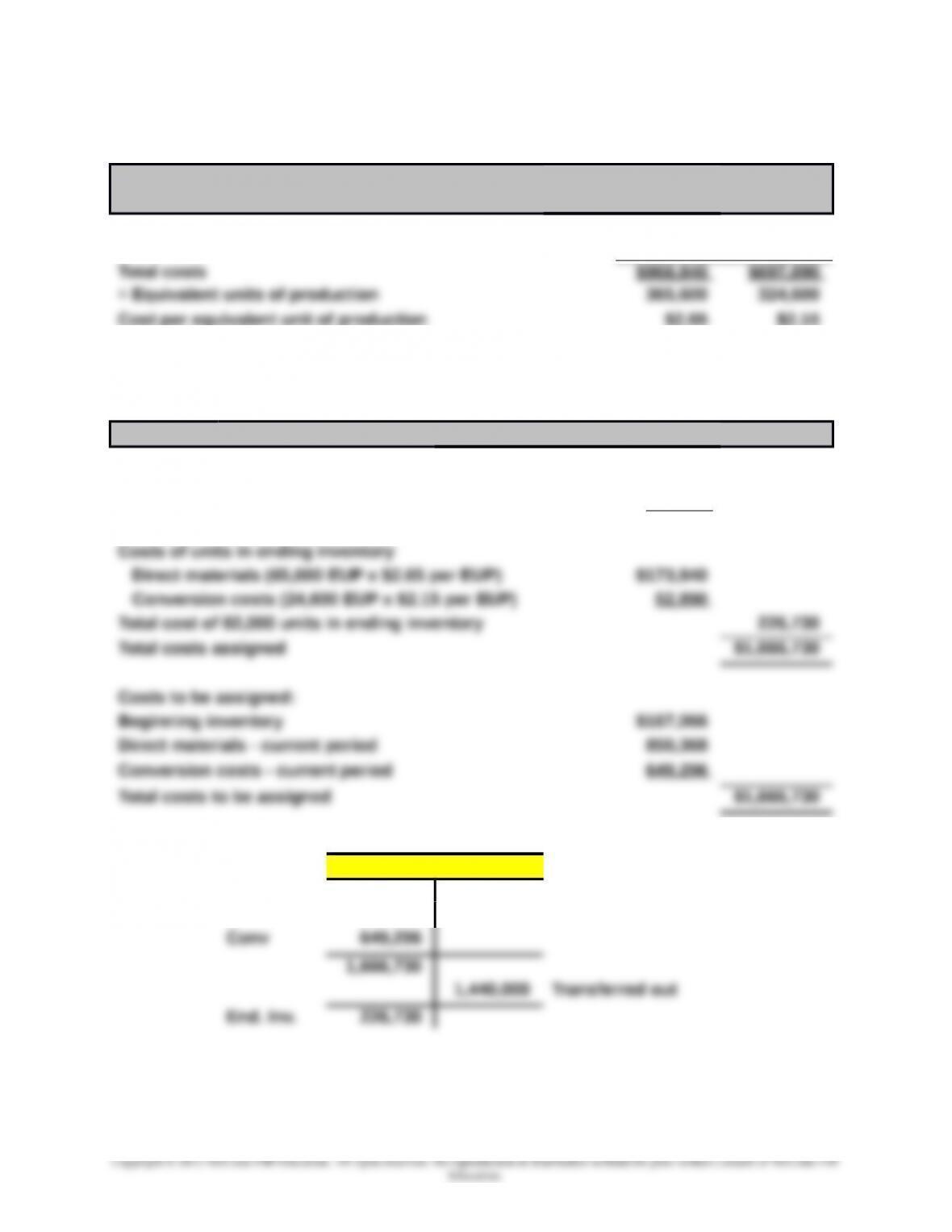

Direct materials (300,000 EUP x $2.65 per EUP) $795,000

Conversion costs (300,000 EUP x $2.15 per EUP) 645,000

Total cost of 300,000 units transferred out $1,440,000

Dept. 1 – WIP

Beg. Inv 167,066

DM 850,368

Exercise 20-10 (20 minutes)

20-1127

Chapter 20 – Process Costing

1.

Units Units

Units in beginning inventory 60,000 60,000 60,000

2.

Equivalent units of production – FIFO

Direct

Materials Conversion

Complete beginning inventory (60,000 x 40% Mtl, 60% Conv.) 24,000 36,000

1.

Cost per equivalent unit – FIFO

Direct

Materials Conversion

Costs incurred this period 850,368 649,296

÷ Equivalent units of production 329,600 300,600

Cost per equivalent unit of production $2.58 $2.16

Exercise 20-11 (continued)

2.

Cost assignment and reconciliation – FIFO

Cost of 60,000 units from beginning inventory

Beginning inventory $ 167,066

20-1128

Chapter 20 – Process Costing

Total cost of 300,000 units transferred out $1,444,346

Costs of units in ending inventory

Direct materials (65,600 EUP x $2.58 per EUP) $169,248

Conversion costs (24,600 EUP x $2.16 per EUP) 53,136

Dept. 1 – WIP

Beg. Inv 167,066

DM 850,368

20-1129