Quick Study 20-20 (10 minutes)

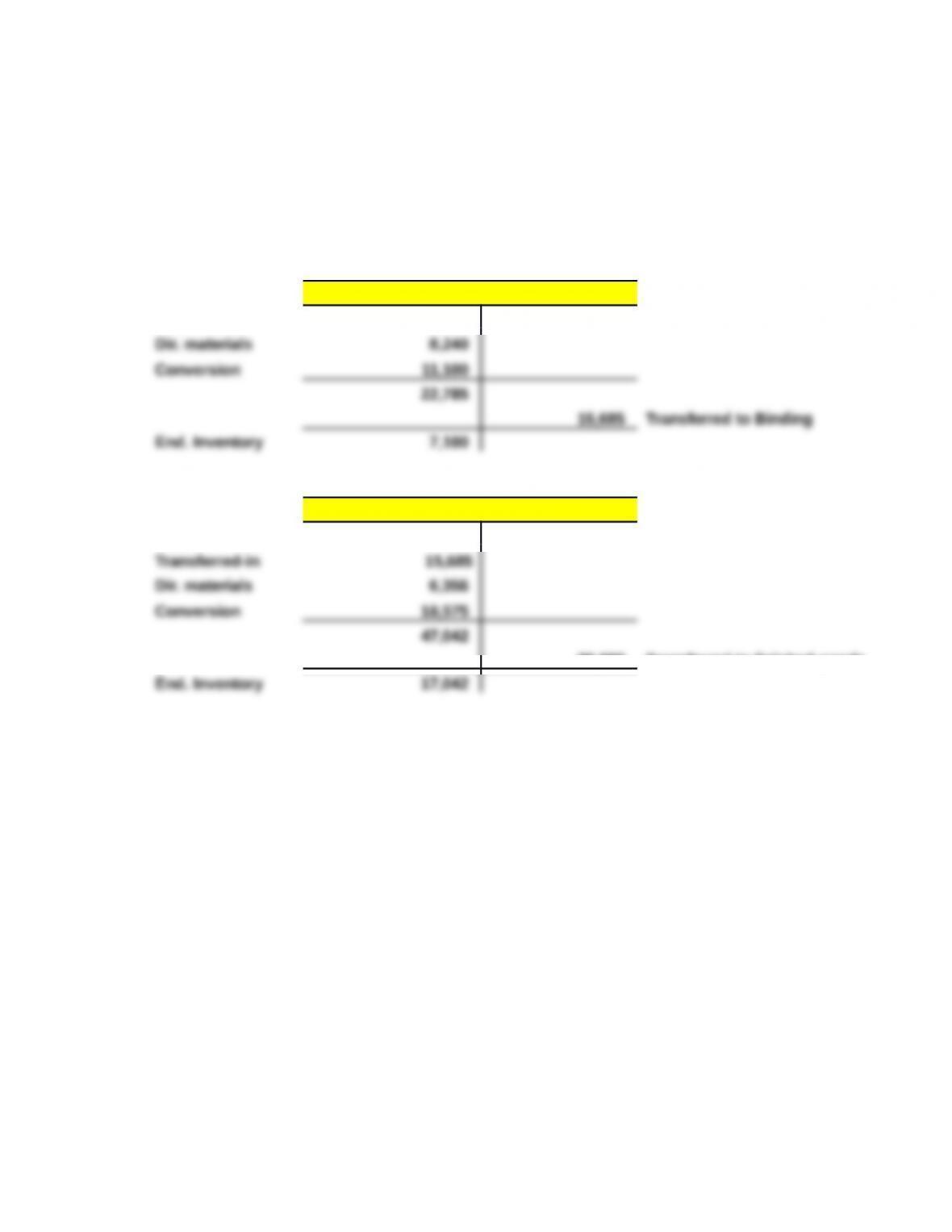

The ending balance in Work in Process Inventory—Cutting is $7,100 and

the ending balance in Work in Process Inventory—Binding is $17,042, as

computed below.

Work in Process—Cutting

Beg. Inventory 3,445

Work in Process—Binding

Beg. Inventory 6,426

30,000 Transferred to finished goods

Quick Study 20-21 (15 minutes)

Equivalent units under the FIFO method

Equivalent

EUP for materials—FIFO Units

Equivalent units to complete beginning WIP (2,000 x 30%)…………. 600

* Units completed – Units in beginning work in process = Units started and completed,

17,000 – 2,000 = 15,000. Units completed = Units in beginning work in process + Units

Cost per equivalent unit—FIFO

Direct

Materials

Costs incurred this period……………………………………… $27,900

Quick Study 20-22 (15 minutes)

Assignment of direct materials costs to output of department—FIFO

Costs transferred out

Costs to complete beginning WIP…………………………

Cost of units started and completed this period

Total costs of units transferred out………………………. $26,350

Cost of ending work in process inventory

Quick Study 20-23 (10 minutes)

1. Raw Materials Inventory………………………………………..62,000

Purchase of raw materials inventory.

2. Work in Process Inventory…………………………………….50,000

Quick Study 20-24 (10 minutes)

1. Work in Process Inventory…………………………………….125,000

2. Factory Overhead…………………………………………………10,000

3. Factory Payroll Payable………………………………………..135,000

Quick Study 20-25 (15 minutes)

1. Factory Overhead………………………………………………… 9,000

2. Factory Overhead…………………………………………………156,000

3. Work in Process Inventory…………………………………….175,000

Quick Study 20-26 (10 minutes)

Finished Goods Inventory……………………………………..275,000

Quick Study 20-27 (5 minutes)

If the company is successful in reducing water usage, its raw materials

cost (water) should decline. Likewise, assuming water used in its cleaning

EXERCISES

Exercise 20-1 (10 minutes)

1. Process operation 7. Job order operation

2. Process operation 8. Process operation

Note: Reasonable arguments can be made to classify #7 and #11 as being made

in a process operation, and #8 in a job order operation, in some cases.

Exercise 20-2 (10 minutes)

a. Job order operation. e. Job order operation.

Exercise 20-3 (10 minutes)

1. F 5. G

Exercise 20-4 (30 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

Units of

Product

2. Beginning inventory is 40% complete with respect to materials.

Ending inventory is 75% complete with respect to materials.

Units of

EUP for Materials Product

Goods completed (80,000 EUP x 100%)…………………………….. 80,000

3. Beginning inventory is 60% complete with respect to materials.

Ending inventory is 30% complete with respect to materials.

Units of

EUP for Materials Product

Goods completed (80,000 EUP x 100%)…………………………….. 80,000

Exercise 20-5 (30 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

Units of

Product

To complete beginning work in process (24,000 EUP x 0%)……… 0

2. Beginning inventory is 40% complete with respect to materials.

Ending inventory is 75% complete with respect to materials.

Units of

EUP for Materials Product

To complete beginning work in process (24,000 EUP x 60%)……. 14,400

3. Beginning inventory is 60% complete with respect to materials.

Ending inventory is 30% complete with respect to materials.

Units of

EUP for Materials Product

To complete beginning work in process (24,000 EUP x 40%)……. 9,600

Exercise 20-6 (30 minutes)

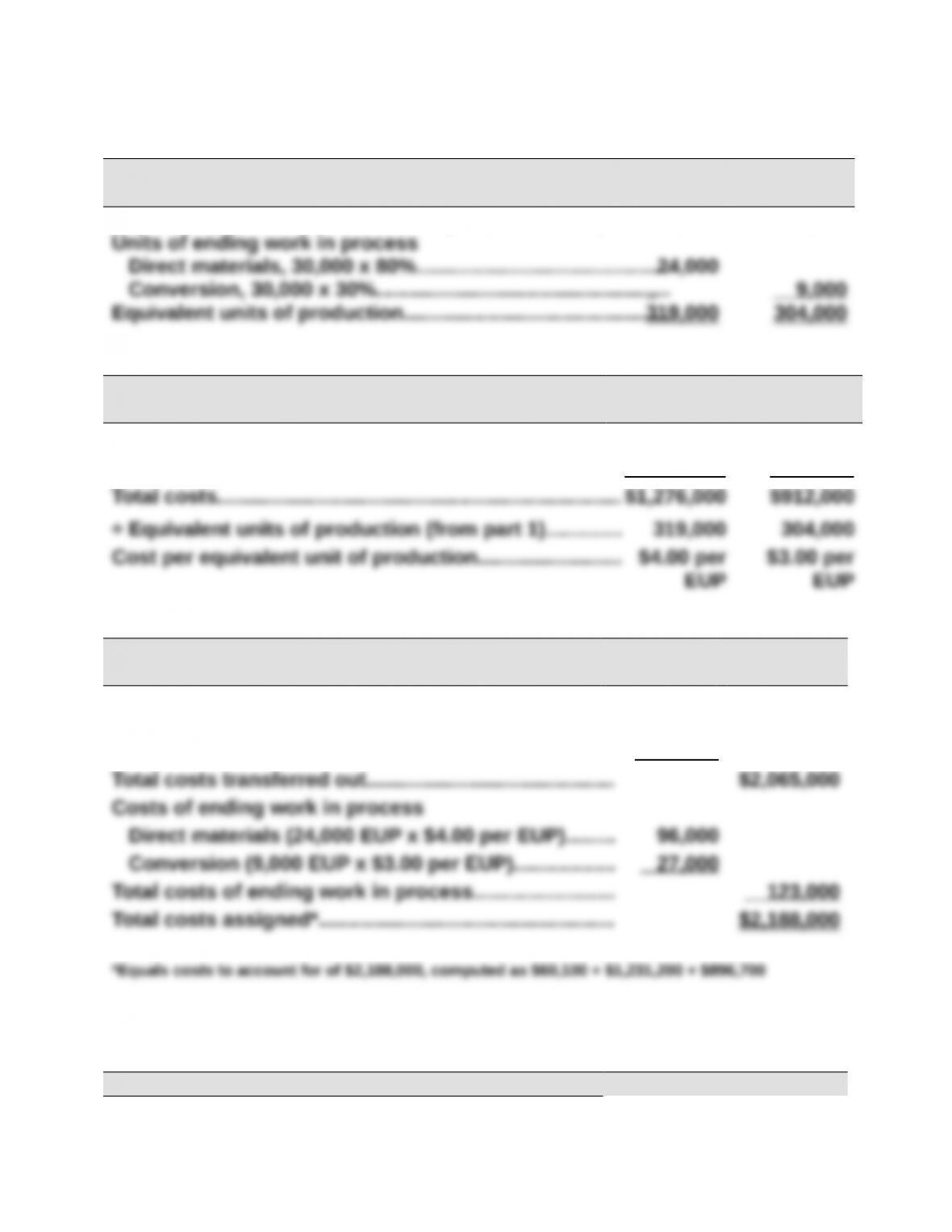

1.

Equivalent units of production—Weighted average

Direct

Materials Conversion

Units completed & transferred out (295,000 x 100%)………..295,000 295,000

2.

Cost per equivalent unit—Weighted average

Direct

Materials Conversion

Costs of beginning work in process……………………….. $ 44,800 $ 15,300

Costs incurred this period……………………………………… 1,231,200 896,700

3.

Cost assignment—Weighted average

Costs of units transferred out

Direct materials (295,000 EUP x $4.00 per EUP)…… $1,180,000

Conversion (295,000 EUP x $3.00 per EUP)…………. 885,000

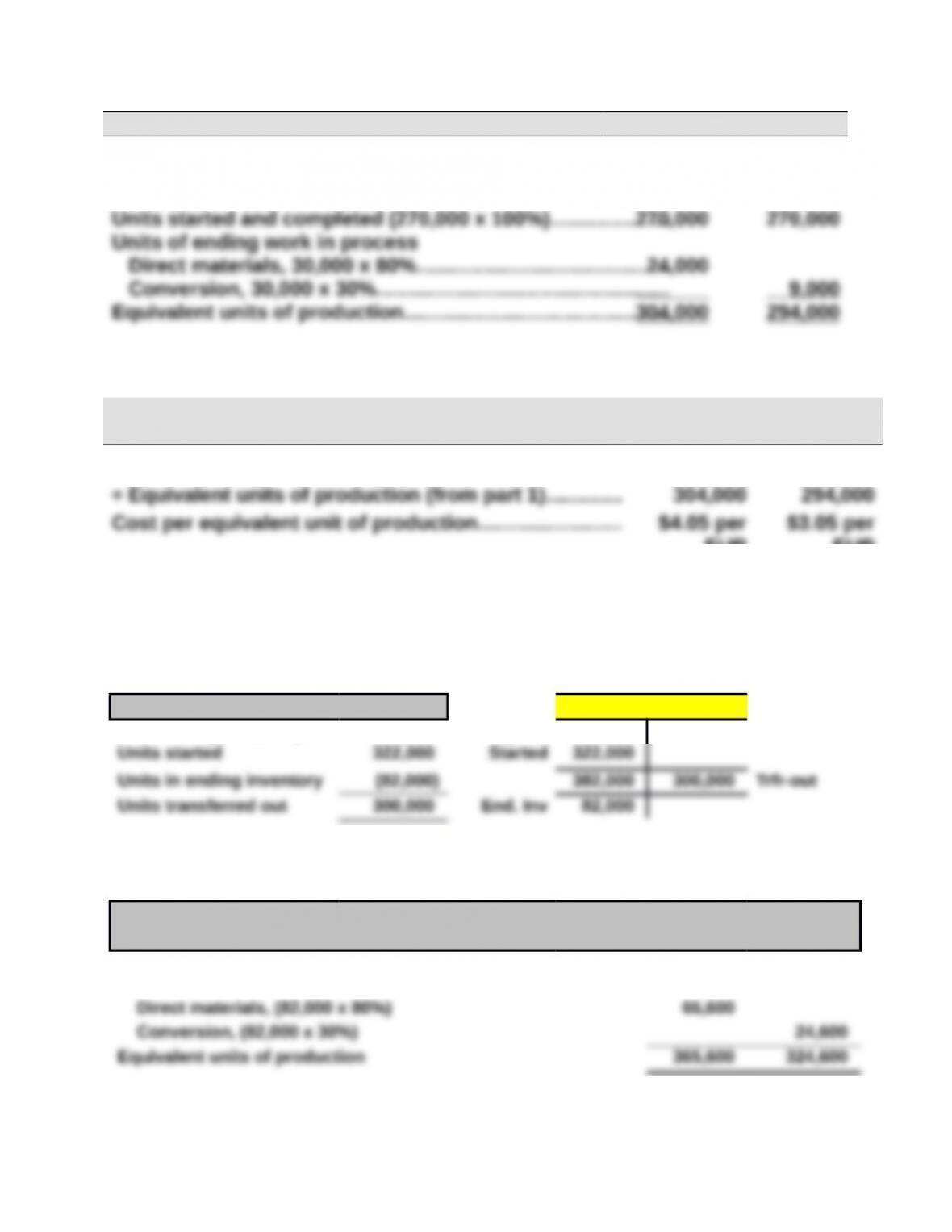

Exercise 20-7 (30 minutes)

1.

Direct

Equivalent units of production—FIFO Materials Conversion

Units to complete beginning work in process

Direct materials (25,000 x 40%)……………………………………

Conversion (25,000 x 60%)…………………………………………..

10,000

15,000

2.

Cost per equivalent unit—FIFO

Direct

Materials Conversion

Costs incurred this period……………………………………… $1,231,200 $896,700

EUP

EUP

Exercise 20-8 (20 minutes)

1. Units transferred out

Units Dept. 1 – units

Units in Beg. inventory 60,000 Beg. Inv 60,000

2. EUP

Equivalent units of production – weighted-average

Direct

Materials Conversion

Units completed & transferred out (300,000 x 100%)……… 300,000 300,000

Units in ending work in process