Chapter 02 – Analyzing and Recording Transactions

Exercise 2-6 (15 minutes)

a. Beginning accounts payable (credit)…………..…………………..…..…. $152,000

Purchases on account in October (credits)…………….….….…..…... 281,000

b. Beginning accounts receivable (debit)…………..…………………….…. $102,500

Sales on account in October (debits)……………..….…..….….…..…... ?

c. Beginning cash balance (debit)……………………………..…………….….$ ?

Cash received in October (debits)……………………………..……………. 102,500

Exercise 2-7 (25 minutes)

Aug. 1 Cash…………………………………………………………. 6,500

Photography Equipment…………………..……..… 33,500

M. Harris, Capital……………………………….... 40,000

Owner investment in business.

31 Utilities Expense……………………………………….. 675

Cash………………………………………………….… 675

Paid for August utilities.

2-59

Chapter 02 – Analyzing and Recording Transactions

Exercise 2-8 (30 minutes)

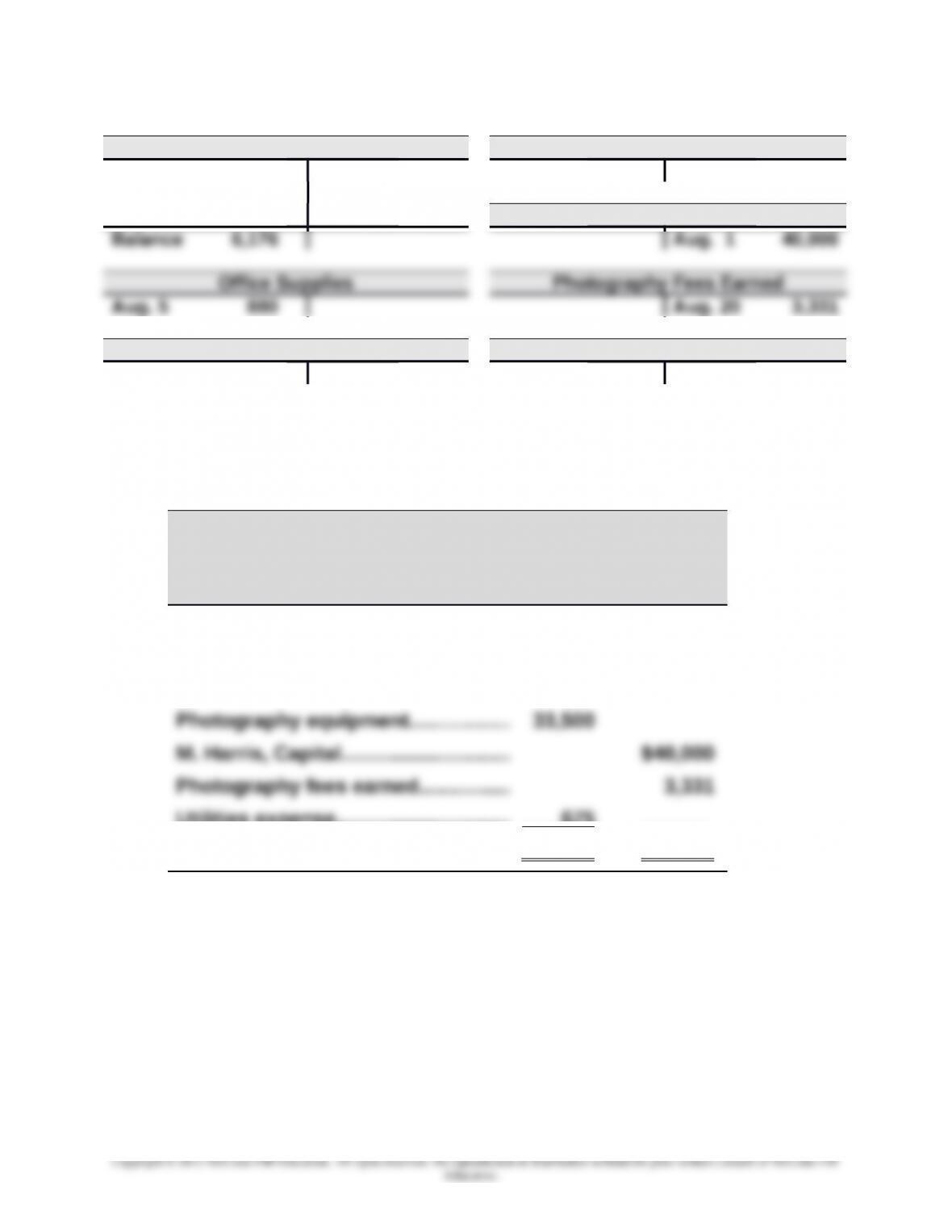

Cash Photography Equipment

Aug. 1 6,500 Aug. 2 2,100 Aug. 1 33,500

20 3,331 5 880

31 675 M. Harris, Capital

Prepaid Insurance Utilities Expense

Aug. 2 2,100 Aug. 31 675

POSE-FOR-PICS

Trial Balance

August 31

Debit Credit

Cash….…..…..……………………………… $ 6,176

Office supplies…………………………… 880

Prepaid insurance…………..………….. 2,100

Utilities expense…………………………. 675 ______

Totals……………………………….………… $43,331 $43,331

2-60

Chapter 02 – Analyzing and Recording Transactions

Exercise 2-9 (30 minutes)

a. Cash……………………………………………………………….… 100,750

K. Spade, Capital………………………………………… 100,750

Owner invested in the business.

Purchased office equipment on credit.

d. Cash……………………………………………………………….… 15,500

Fees Earned……………………………………………….. 15,500

Received cash from customer for services.

Billed customer for services provided.

g. Rent Expense………………………………………………….... 1,225

Cash………………………………………..………..………. 1,225

Paid for this period’s rental charge.

Owner withdrew cash for personal use.

2-61

Chapter 02 – Analyzing and Recording Transactions

Exercise 2-9 (concluded)

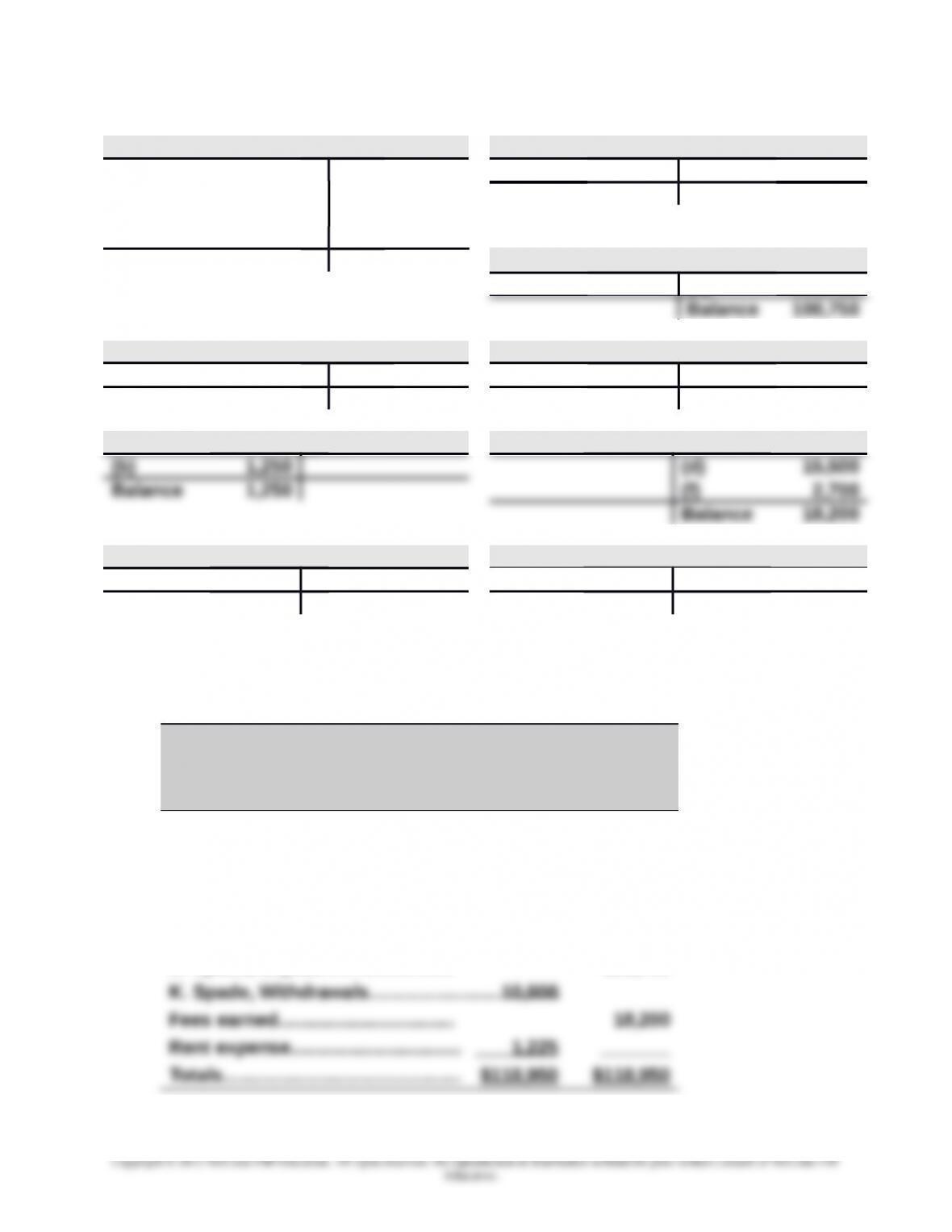

Cash Accounts Payable

(a) 100,750 (b) 1,250 (e) 10,050 (c) 10,050

(d) 15,500 (e) 10,050 Balance 0

(h) 1,125 (g) 1,225

(i) 10,000

Balance 94,850 K. Spade, Capital

(a) 100,750

Accounts Receivable K. Spade, Withdrawals

(f) 2,700 (h) 1,125 (i) 10,000

Balance 1,575 Balance 10,000

Office Supplies Fees Earned

Office Equipment Rent Expense

(c) 10,050 (g) 1,225

Balance 10,050 Balance 1,225

Exercise 2-10 (15 minutes)

SPADE COMPANY

Trial Balance

May 31, 2015

Debit Credit

Cash……….……………….…..….….…. $ 94,850

Accounts receivable……………..… 1,575

Office supplies…………….….…..…. 1,250

Office equipment……..….….…...... 10,050

Accounts payable…………….….…. $ 0

K. Spade, Capital…….…..….…...... 100,750

2-62

Chapter 02 – Analyzing and Recording Transactions

Exercise 2-11 (20 minutes)

Transactions that created expenses:

b. Salaries Expense………………………………..… 1,233

Cash……………………………………………..… 1,233

Paid salary of receptionist.

[Note: Expenses are outflows or using up of assets (or the creation of

liabilities) that occur in the process of providing goods or services to

customers.]

Transactions a, c, and e are not expenses for the following reasons:

a. This transaction decreased assets in settlement of a previously

existing liability, and equity did not change. Cash payment does not

mean the same as using up of assets (expense is recorded when the

supplies are used).

2-63

Chapter 02 – Analyzing and Recording Transactions

Exercise 2-12 (20 minutes)

Transactions that created revenues:

b. Accounts Receivable………………………..…………. 2,300

Services Revenue……………………………..…… 2,300

Provided services on credit.

[Note: Revenues are inflows of assets (or decreases in liabilities)

received in exchange for goods or services provided to customers.]

Transactions that did not create revenues along with the reasons are:

a. This transaction brought in cash, but this is an owner investment.

f. This transaction brought in cash and increased assets, but it also

increased a liability by the same amount (no goods or services were

provided to generate revenue).

Exercise 2-13 (25 minutes)

a. Belle created a new business and invested $6,000 cash, $7,600 of

equipment, and $12,000 in automobiles.

g. Paid $820 cash for gas and oil expenses.

2-64

Chapter 02 – Analyzing and Recording Transactions

Exercise 2-14 (30 minutes)

a. Cash……………………………………………………………….… 6,000

Equipment………………………………………………..………. 7,600

Automobiles……………………………………………………… 12,000

D. Belle, Capital……………………………………....…. 25,600

Owner investment in company.

e. Cash……………………………………………………………….… 4,500

Delivery Services Revenue………….……..………. 4,500

Received cash from customer for services

provided.

2-65

Chapter 02 – Analyzing and Recording Transactions

Exercise 2-15 (20 minutes)

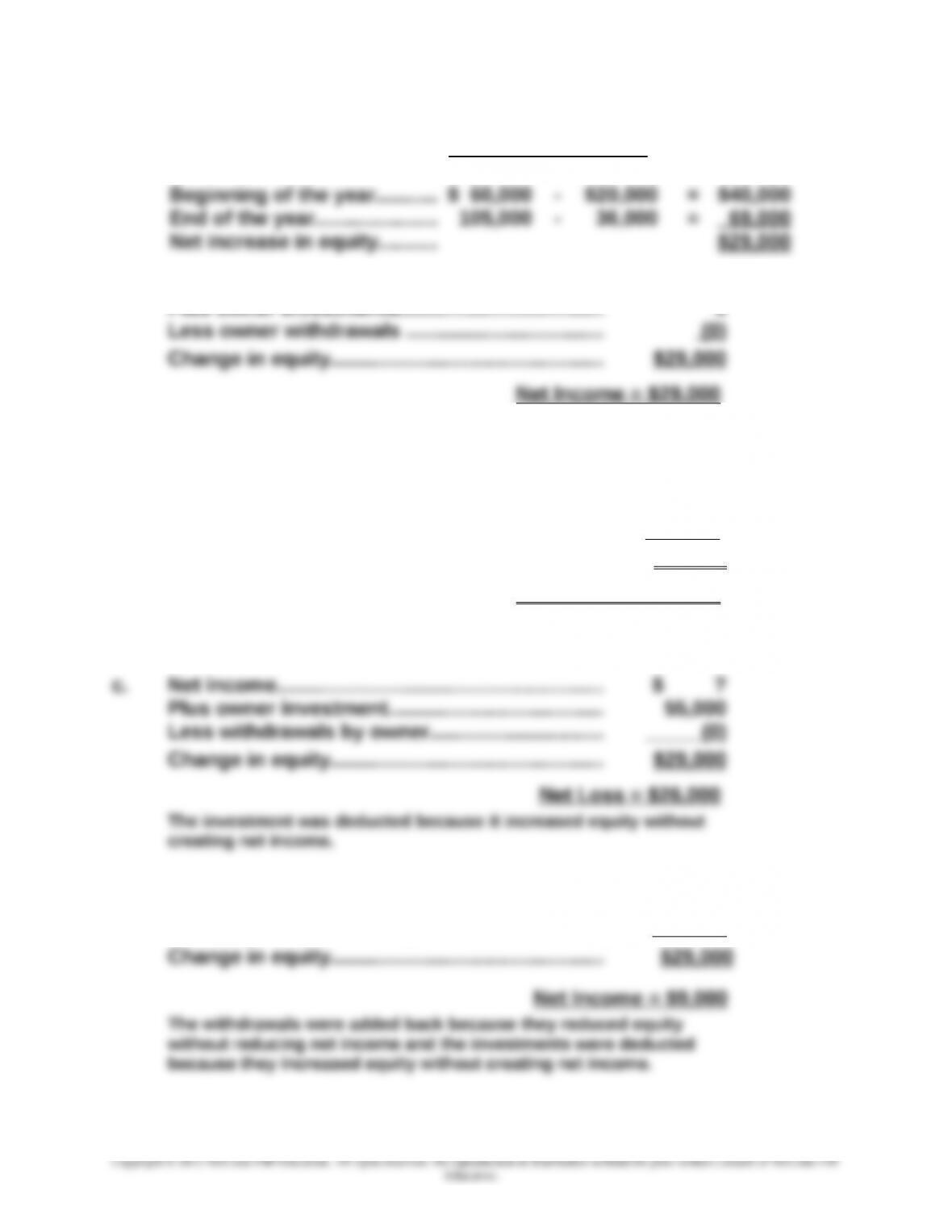

Calculation of change in equity for part a through part d

Assets –Liabilities =Equity

a. Net income…………………………………..…………..… $ ?

Plus owner investments………….……..…………… 0

Since there were no additional investments or withdrawals, the net

income for the year equals the net increase in owner’s equity.

b. Net income……………………………………………….... $ ?

Plus owner investments………….……..…………… 0

Less owner withdrawals ($1,250/mo. x 12 mo.) (15,000)

Change in equity…………….…………..……………... $29,000

Net Income = $44,000

The withdrawals were added back because they reduced equity

without reducing net income.

d. Net income……………………………………………….... $ ?

Plus owner investment…………….…..…………….. 35,000

Less owner withdrawals ($1,250/mo. X 12 mo.) (15,000)

2-66

Chapter 02 – Analyzing and Recording Transactions

Exercise 2-16 (15 minutes)

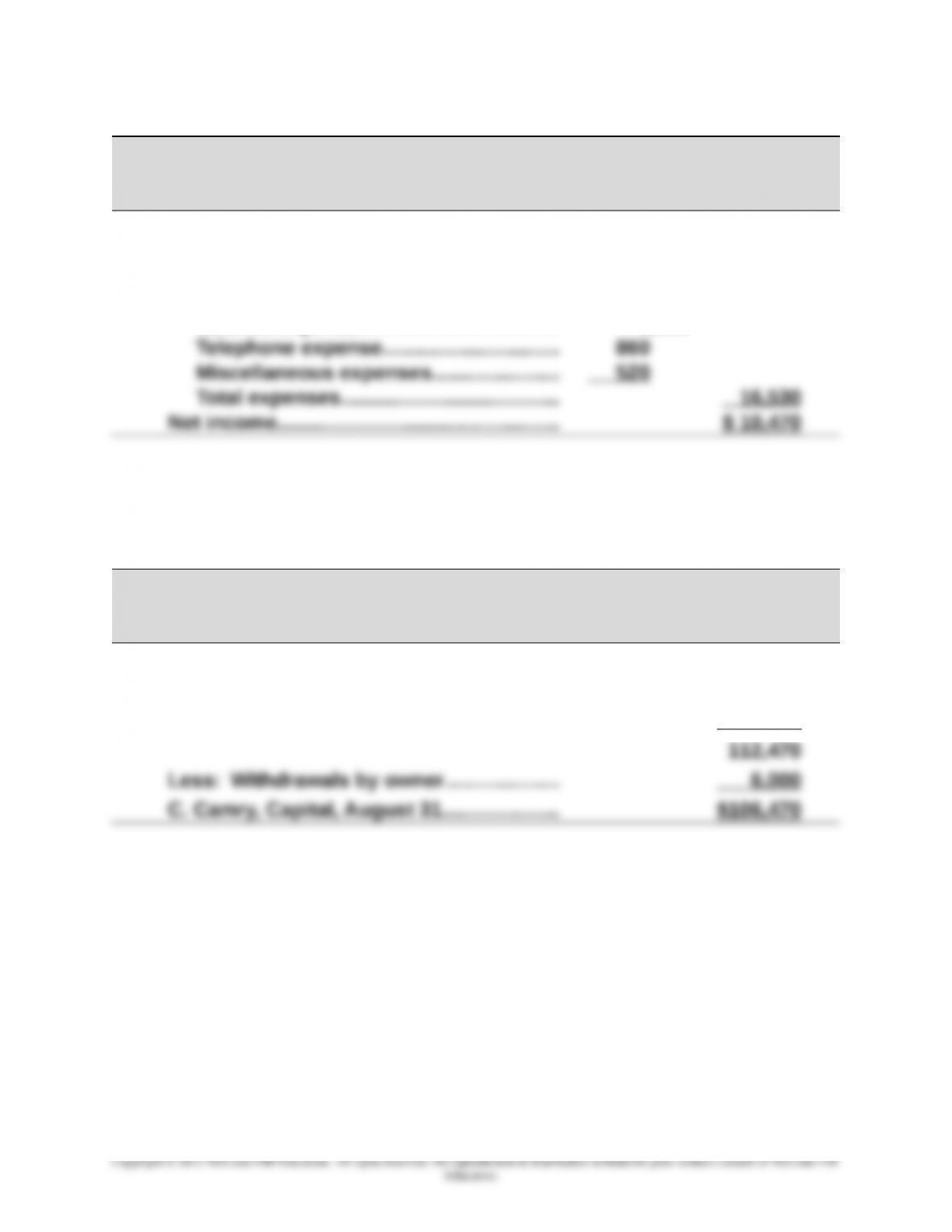

HELP TODAY

Income Statement

For Month Ended August 31

Revenues

Consulting fees earned……………………. $ 27,000

Expenses

Rent expense…………………………..……… $ 9,550

Salaries expense………..……………..……. 5,600

Exercise 2-17 (15 minutes)

HELP TODAY

Statement of Owner’s Equity

For Month Ended August 31

C. Camry, Capital, July 31…………………..… $ 0

Add: Investment by owner..…..……......... 102,000

Net income (from Exercise 2-16)...... 10 ,470

2-67

Chapter 02 – Analyzing and Recording Transactions

Exercise 2-18 (15 minutes)

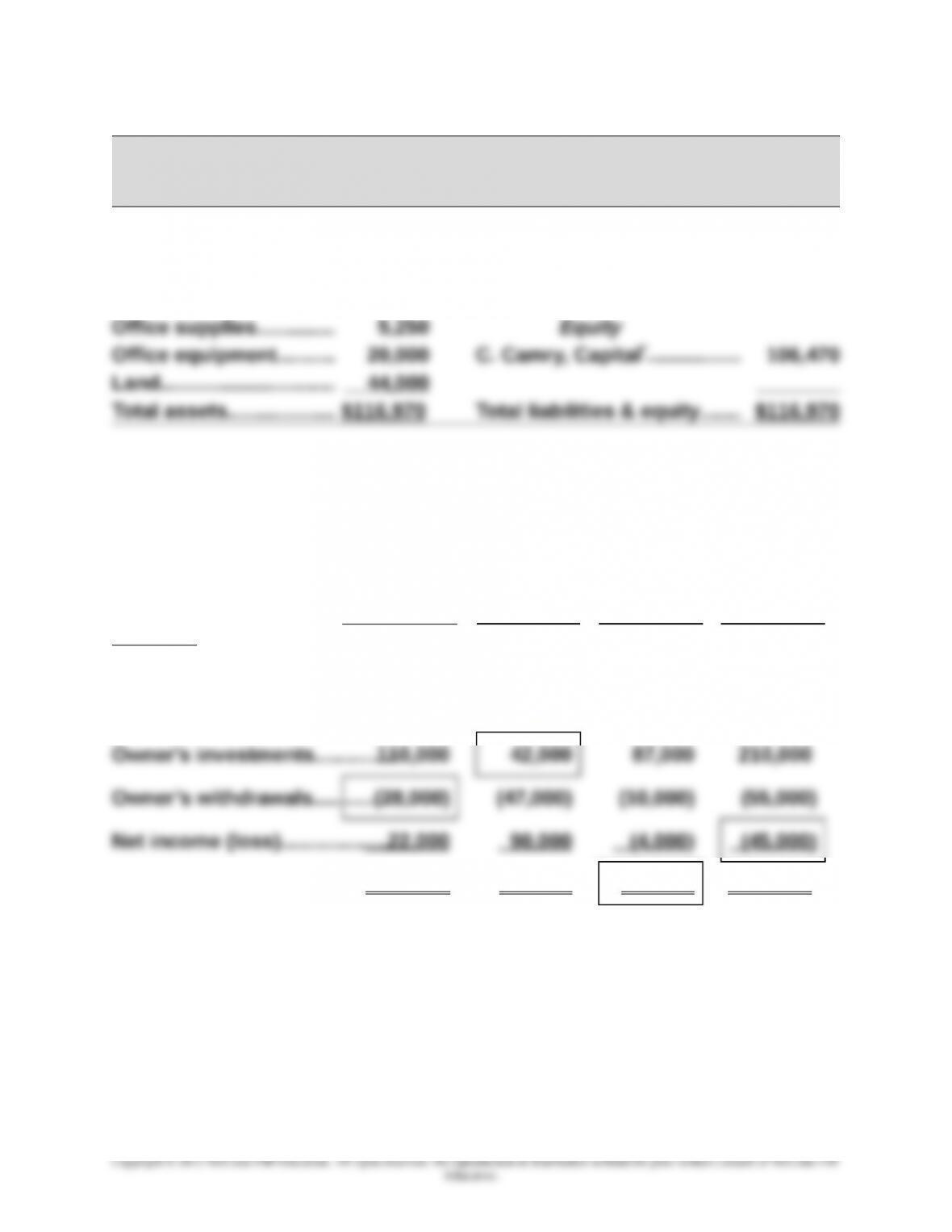

HELP TODAY

Balance Sheet

August 31

Assets Liabilities

Cash……………………….… $ 25,360 Accounts payable………....... $ 10,500

Accounts receivable.... 22,360

* Amount from Exercise 2-17.

Exercise 2-19 (15 minutes)

(a) (b) (c) (d)

Answers $(28,000) $42,000 $73,000 $(45,000)

Computations:

Equity, Dec. 31, 2014..….........$ 0 $ 0 $ 0 $ 0

Equity, Dec. 31, 2015..….........$104 ,000 $85 ,000 $73 ,000 $110,000

2-68