Chapter 02 – Analyzing and Recording Transactions

CHAPTER 2

ANALYZING AND RECORDING TRANSACTIONS

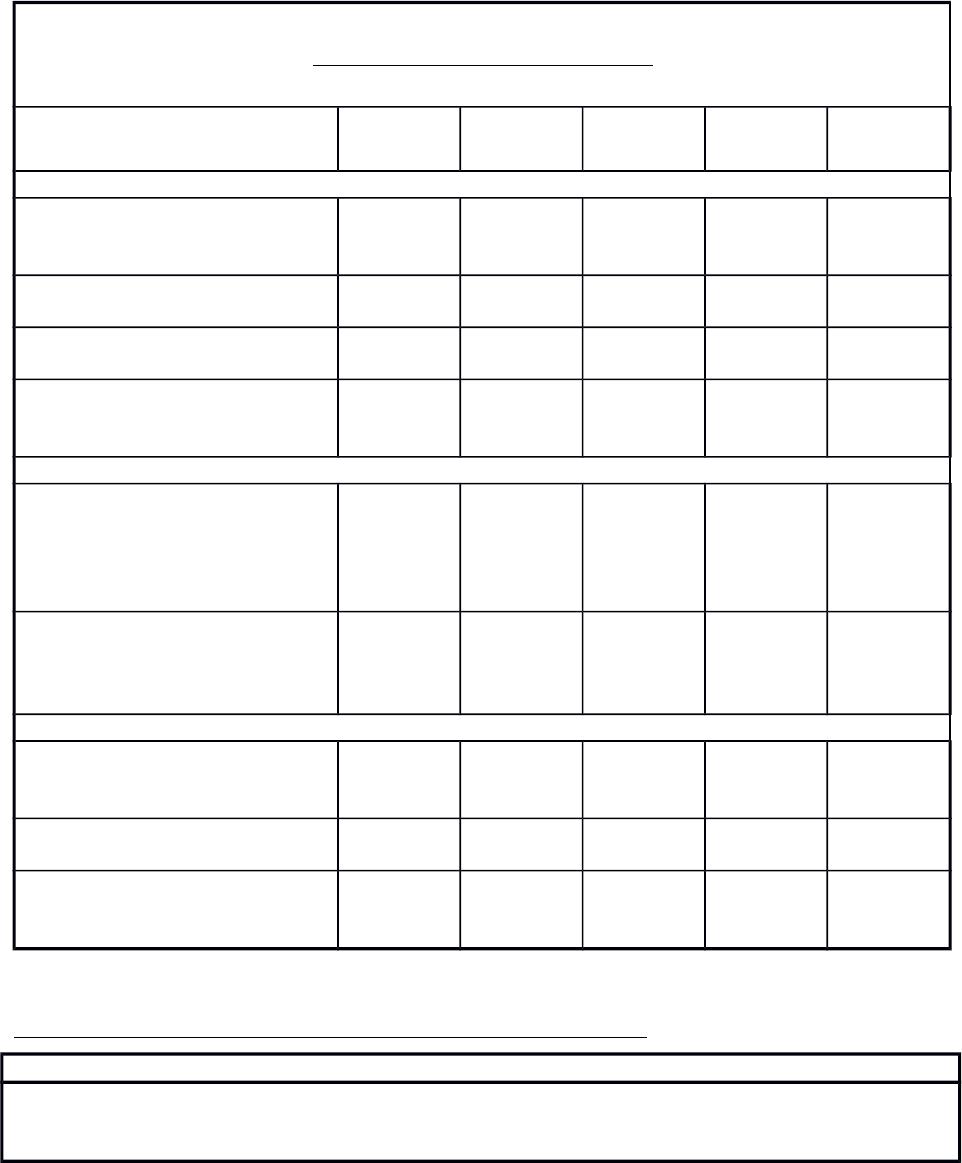

Related Assignment Materials

Student Learning Objectives Questions

Quick

Studies* Exercises* Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Explain the steps in processing

transactions and the role of

source documents.

3, 6, 9 2-1 2-1 2-6 2-3, 2-4,

2-6, 2-9

C2. Describe an account and its use

in recording transactions.

1,2, 14 2-2 2-2 2-5 2-4, 2-6

C3. Describe a ledger and a chart of

accounts.

2-3 2-3, 2-16 2-1, 2-2,

2-3, 2-4, 2-6

C4. Define debits and credits and

explain their role in

double-entry accounting.

7 2-4, 2-5,

2-10

2-4 2-1, 2-2, 2-3 2-6

Analytical objectives:

A1. Analyze the impact of

transactions on accounts and

financial statements.

.

2-7 2-5, 2-6,

2-9, 2-11,

2-12, 2-13,

2-15, 2-20,

2-21

2-1, 2-2,

2-3, 2-4,

2-5, 2-6

2-1, 2-2,

2-4, 2-5,

2-6, 2-7,

2-8

A2. Compute the debt ratio and

describe its use in analyzing

financial condition.

2-23 2-5 2-1, 2-2,

2-7, 2-8,

2-10

Procedural objectives:

P1. Record transactions in a journal

and post entries to a ledger.

3, 4,5 2-6 2-7, 2-11,

2-12, 2-14

2-19

2-1, 2-2,

2-3, 2-4

P2. Prepare and explain the use of a

trial balance.

8 2-8 2-8, 2-10,

2-20, 2-21

2-1, 2-2,

2-3, 2-4, 2-6

P3. Prepare financial statements

from business transactions.

10, 11, 12,

13,15, 16,

17, 18

2-9 2-16, 2-17,

2-18, 2-19,

2-22

2-5 2-4, 2-7,

2-8

*See additional information on next page that pertains to these quick studies, exercises and problems.

Additional Information on Related Assignment Material

The Serial Problem for Success Systems continues in this chapter.

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

2-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 02 – Analyzing and Recording Transactions

in practice, homework, or exam mode

Synopsis of Chapter Revisions

Akola Project: NEW opener with new entrepreneurial assignment

New layout showing financial statements drawn from trial balance

New preliminary coverage of classified and unclassifed balance sheets

Changed selected numbers for FastForward

Revised Piaggio’s (IFRS) balance sheet

Updated debt ratio section using Skechers

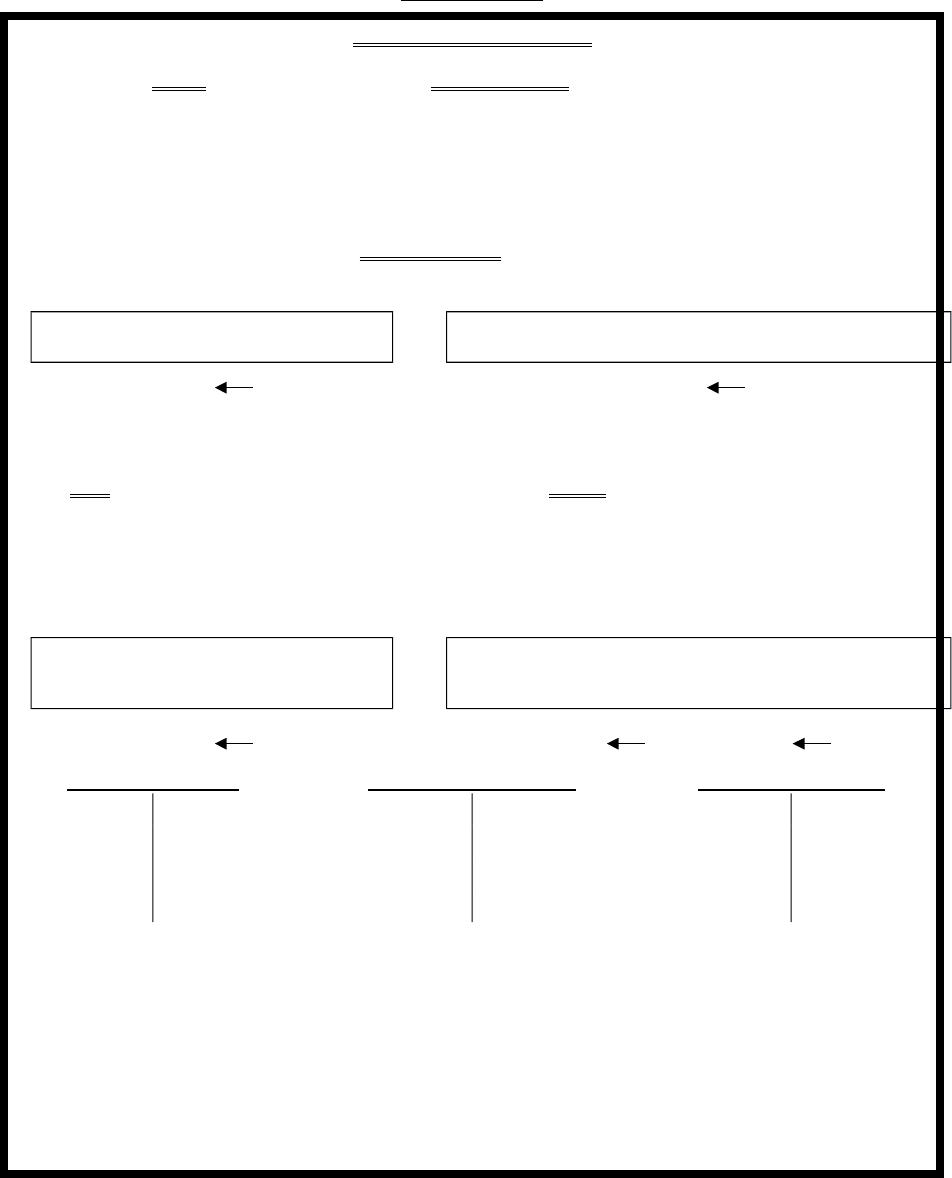

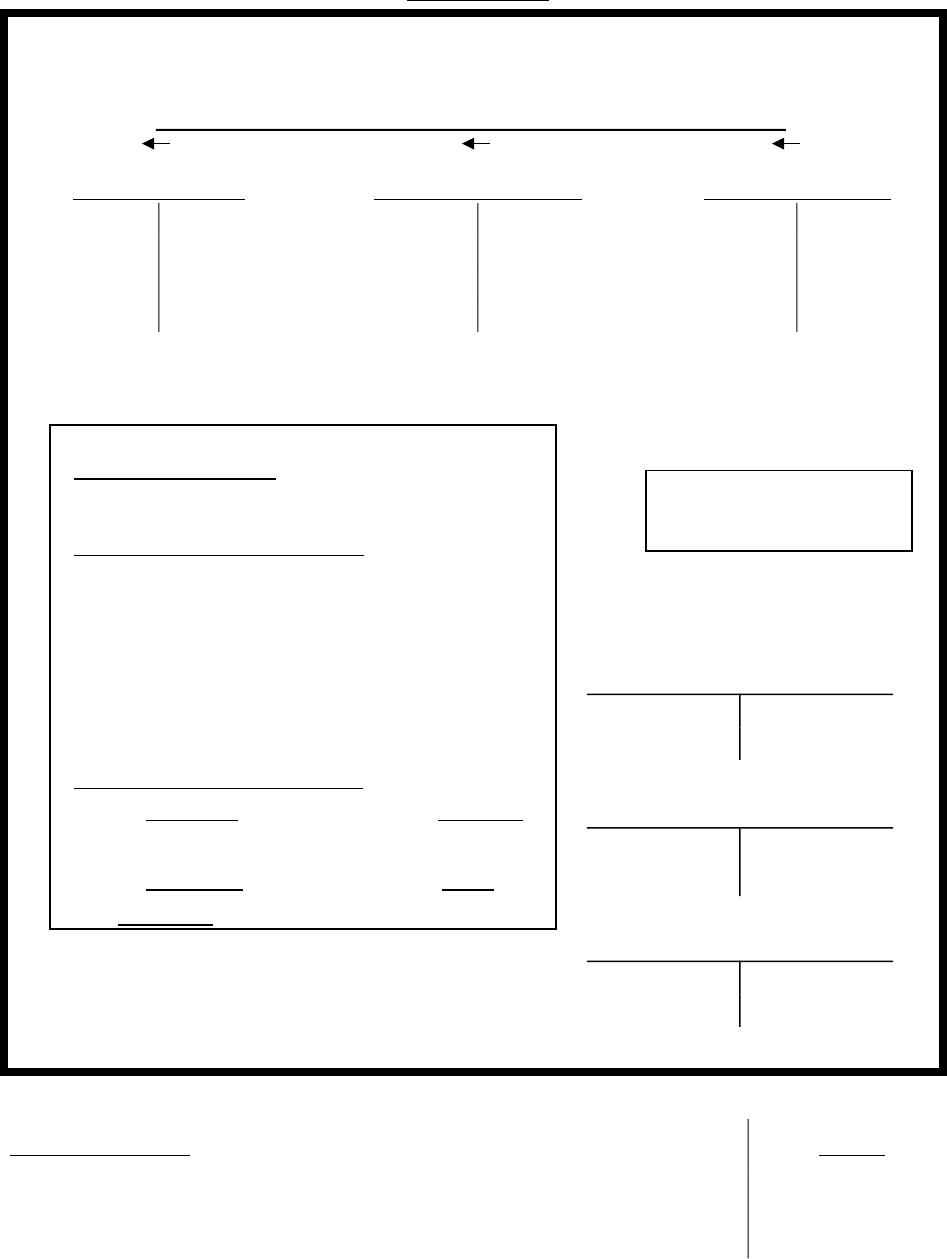

VISUAL #2-1

THREE PARTS OF AN ACCOUNT

(1) ACCOUNT TITLE

Left Side Right Side

called called

(2) DEBIT (3) CREDIT

Rules for using accounts

Accounts are assigned balance sides (Debit or Credit).

To increase any account, use the balance side.

To decrease any account, use the side opposite the balance.

Finding account balances

If total debits = total credits, the account balance is zero.

2-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 02 – Analyzing and Recording Transactions

If total debits are greater than total credits, the account has a debit

balance equal to the difference of the two totals.

If total credits are greater than total debits, the account has a

credit balance equal to the difference of the two totals.

2-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 02 – Analyzing and Recording Transactions

VISUAL #2-2

REAL ACCOUNTS

ALL ACCOUNTS ARE ASSIGNED BALANCE SIDES

BALANCE SIDES FOR ASSETS, LIABILITIES, AND

EQUITY ACCOUNTS ARE ASSIGNED BASED ON

SIDE OF EQUATION THEY ARE ON.

ASSETS =LIABILITIES + EQUITY

are on the

left side of the equation

therefore they are

are on the

right side of the equation

therefore they are

ASSIGNED LEFT SIDE

BALANCE

ASSIGNED RIGHT SIDE

BALANCE

DEBIT BALANCE CREDIT BALANCE

All Asset Accts All Liability Accts All Equity Accts

Normal Normal Normal

Debit Credit Debit Credit Debit Credit

Balance Balance Balance

+ side – side – side + side – side + side

*In a sole proprietorship, there is only one equity account, which is called

capital. For that reason, the terms equity and capital are often used

interchangeably. (When corporations are discussed in detail, you will learn

many stockholders’ equity accounts.) Equity is an account classification like

assets. Owner’s Name, Capital, is the account title.

2-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 02 – Analyzing and Recording Transactions

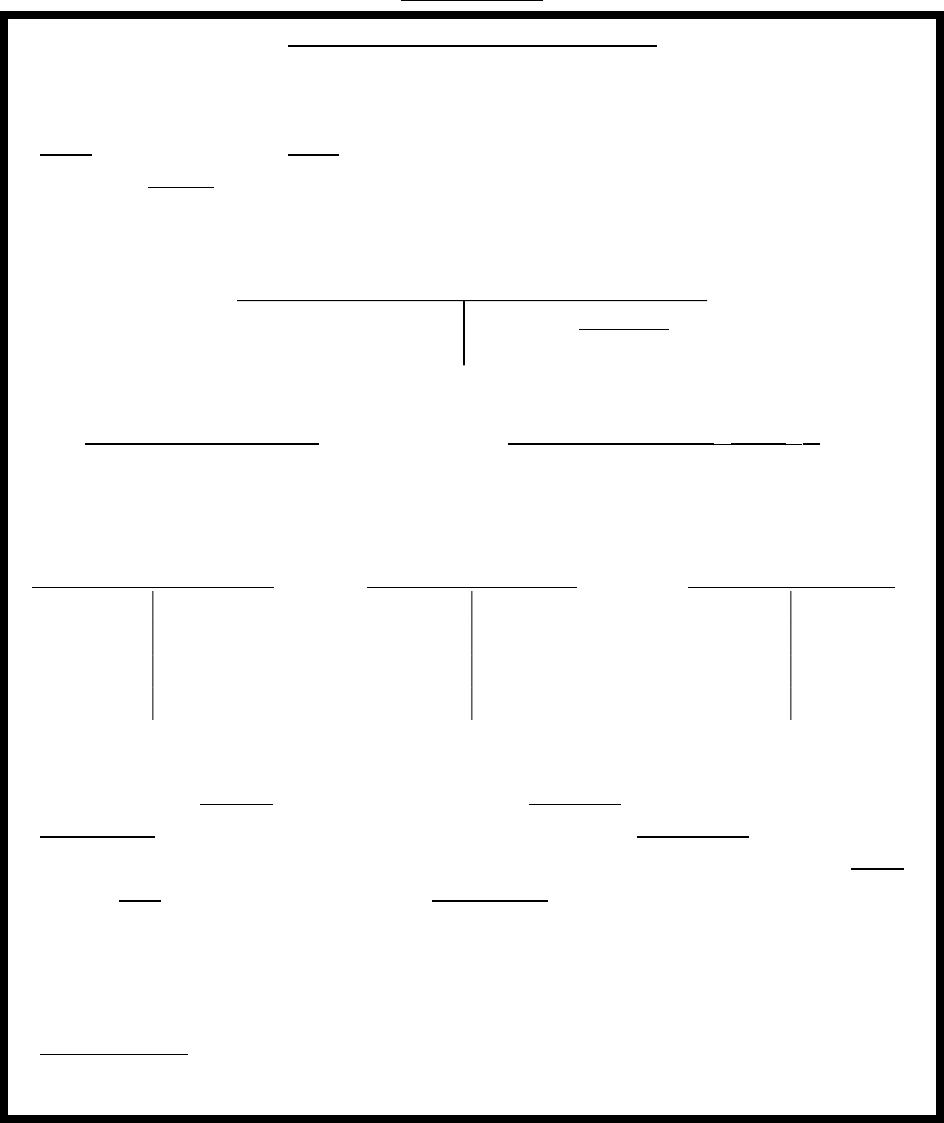

VISUAL #2-3

TEMPORARY ACCOUNTS

Temporary accounts are established to facilitate efficient accumulation of

data for statements. Temporary accounts are established for withdrawals,

each revenue, and each expense. Temporary accounts are assigned

balances based on how they affect equity.

(Equity Account)

Owner’s Name, Capital

Debit Credit Balance

– side + side

Temporary Accounts Effect on equity? E or E

Owner, Withdrawals* E = Dr

Revenues E = Cr

Expenses E = Dr

All Withdrawal Accts All Revenue Accts All Expense Accts

Normal Normal Normal

Debit Credit Debit Credit Debit Credit

Balance Balance Balance

+ side – side – side + side + side – side

Note:

Transactions during the period always increase the balances of these

temporary accounts since the transaction represent additional withdrawals,

revenues, and expenses. We will later learn how to move these amounts back

to the real account they affect CAPITAL. At the end of the accounting

period, transferring withdrawals, revenues, and expenses back to capital is

the main use for the decrease side of the temporary accounts.

*The “Owner’s Name, Withdrawals” is the account title and the

classification of account is a contra-equity.

2-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 02 – Analyzing and Recording Transactions

VISUAL #2-4

USING ACCOUNTS – SUMMARY

Real Accounts

All Asset Accts All Liability Accts All Equity Accts

Debit + Credit + Credit +

Balance Balance Balance

RULE REVIEW

Temporary Accounts

Transaction analysis rules

Each transaction affects at least 2

accounts.

Each transaction must have equal

debits and credits.

All Withdrawal Accounts

Debit +

Balance

General account use rules

To increase any account, use balance All Revenue Accounts

side. Credit +

To decrease any account, use side Balance

opposite the balance

All Expense Accounts

Debit +

Balance

Chapter Outline Notes

I. Analyzing and Recording Process—steps include:

A. Analyzing each transaction and event from source documents. Source

documents are business papers that identify and describe economic

2-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 02 – Analyzing and Recording Transactions

events and transactions. Examples: sales tickets, checks, purchase

orders, bills, and bank statements. Source documents provide

objective and reliable evidence about transactions and events.

B. Record relevant transactions and events in a journal.

C. Post journal information to ledger accounts.

D. Prepare and analyze the trial balance.

II. The Account and its Analysis

A. An account is a record of increases and decreases in a specific asset,

liability, equity, revenue, or expense item.

B. Accounts are arranged into three basic categories based on the

accounting equation. Categories are:

1. Assets—resources owned or controlled by a company that have

future economic benefit. Examples include Cash, Accounts

Receivable, Note Receivable, Prepaid Expenses, Prepaid

Insurance, Supplies, Store Supplies, Equipment, Buildings, Land.

2. Liabilities—claims (by creditors) against assets, which means

they are obligations to transfer assets or provide products or

services to others. Examples include Accounts Payable, Note

Payable, Unearned Revenues, and Accrued Liabilities.

a. Accounts Payable—verbal or implied promise to pay later

usually arising from purchase of inventory or other assets.

b. Notes Payable—formal promise to pay usually denoted by

signing a promissory note, to pay a future amount.

c. Unearned revenue—revenue collected before it is earned;

before services or goods are provided.

d. Accrued liabilities—amounts owed that are not yet paid.

3. Equity—owner’s claim on company’s assets is called equity or

owner’s equity. Examples include Owner’s Capital, Owner’s

Withdrawals (decreases in equity). Revenues (results from

providing goods or services; i.e. Sales, Fees Earned) increases

equity. Expenses (results from assets or services used in

operation; i.e. Supplies Expense) decreases equity.

III. Analyzing and Processing Transactions

A. The general ledger or ledger (referred to as the books) is a record

containing all the accounts a company uses.

B. The chart of accounts is a list of all accounts in the ledger with their

identification numbers.

C. A T-account represents a ledger account and is a tool used to

understand the effects of one or more transactions. Has shape like the

letter T with account title on top.

Chapter Outline Notes

IV. Debits and Credits

A. The left side of an account is called the debit side. A debit is an entry

on the left side of an account.

B. The right side of an account is called the credit side. A credit is an

2-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 02 – Analyzing and Recording Transactions

entry on the right side of an account.

C. Accounts are assigned balance sides based on their classification or

type.

D. To increase an account, an amount is placed on the balance side, and

to decrease an account, the amount is placed on the side opposite its

assigned balance side.

E. The account balance is the difference between the total debits and the

total credits recorded in that account. When total debits exceed total

credits the account has a debit balance. When total credits exceed

total debits the account has a credit balance. When two sides are

equal the account has a zero balance.

V. Double-Entry Accounting—requires that each transaction affect, and be

recorded in, at least two accounts. The total debits must equal total credits

for each transaction.

A. The assignment of balance sides (debit or credit) follows the

accounting equation.

1. Assets are on the left side of the equation; therefore, the left, or

debit, side is the normal balance for assets.

2. Liabilities and equities are on the right side; therefore, the right,

or credit, side is the normal balance for liabilities and equity.

3. Withdrawals, revenues, and expenses really are changes in equity,

but it is necessary to set up temporary accounts for each of these

items to accumulate data for statements. Withdrawals and

expense accounts really represent decreases in equity; therefore,

they are assigned debit balances. Revenue accounts really

represent increases in equity; therefore, they are assigned credit

balances.

B. Three important rules for recording transactions in a double-entry

accounting system are:

1. Increases to assets are debits to the asset accounts. Decreases to

assets are credits to the asset accounts.

2. Increases to liabilities are credits to the liability accounts.

Decreases to liabilities are debits to the liability accounts.

3. Increases to equity are credits to the equity accounts. Decreases

to equity are debits to the equity accounts.

Chapter Outline Notes

VI. Journalizing and Posting Transactions

A. Four steps in processing transactions are as follows:

Journalizing–The process of recording each transaction in a journal.

1. Identify transaction and source documents.

2. Analyze using the accounting equation. Apply double entry

accounting to determine account to be debited and credited.

3. Record journal entry—recorded chronologically (A journal

gives us a complete record of each transaction in one place.)

2-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 02 – Analyzing and Recording Transactions

a. A General Journal is the most flexible type of journal

because it can be used to record any type of transaction.

b. When a transaction is recorded in the General Journal, it is

called a journal entry. A journal entry that affects more

than two accounts is called a compound journal entry.

c. Each journal entry must contain equal debits and credits.

4. Post entry to ledger—transfer (or post) each entry from journal

to ledger.

a. Debits are posted as debit, and credits as credits to the

accounts identified in the journal entry.

b. Actual accounting systems use balance column accounts

rather than T-accounts in the ledger.

c. A balance column account has debit and credit columns

for recording entries and a third column for showing the

balance of the account after each entry is posted.

Note: To see an illustration of analyzing, journalizing and posting of 16

basic transactions refer to pages 64-72 of the textbook.

VII. Trial Balance

A. A trial balance is a list of accounts and their balances at a point in

time. Account balances are reported in their appropriate debit or

credit columns of the trial balance.

B. The trial balance tests for the equality of the debit and credit

account balances as required by double-entry accounting.

C. Three steps to prepare a trial balance are as follows:

1. List each account and its amount (from the ledger).

2. Compute the total debit balances and the total credit balances.

3. Verify (prove) total debit balances equal total credit balances.

D. When a trial balance does not balance (the columns are not equal),

an error has occurred in one of the following steps:

1. Preparing the journal entries.

2. Posting the journal entries to the ledger.

3. Calculating account balances.

Chapter Outline Notes

4. Copying account balances to the trial balance.

5. Totaling the trial balance columns.

(Note: Any errors must be located and corrected before preparing

the financial statements. Financial Statements prepared from the

trial balance are actually unadjusted statements. The purpose,

content and format for each statement was presented in Chapter 1.

The next chapter will address adjustments)

E. Correcting Errors

1. Approach to correcting errors depends on the kind of error and

when it is discovered.

2-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 02 – Analyzing and Recording Transactions

2. Correcting entries may be necessary.

F. Presentation Issues

1. Dollar signs are not used in journals and ledgers but do appear

in financial statements and other reports such as a trial

balance.

2. Usual practice on statements is to put dollar signs before the

first and last number in each column.

3. Commas are optional except for financial reports were they

are always used.

4. Companies commonly round in reports to the nearest dollar, or

even higher levels.

5. Double rule the final total(s) on the financial statements.

VIII. Global View—Compares U.S.GAAP to IFRS

A. Analyzing and recording transactions—all transactions in this

chapter are accounted for identically under both systems.

B. Financial Statements—both systems require the same 4 basic

statement but there are some differences in the presentation

sequence with a given statement.

C. Accounting controls and assurance—SOX strengthened U.S.

control procedures that insure proper principle application,

however global standards for control and enforcement are diverse.

This can yield different outcomes.

IX. Decision Analysis—Debt Ratio:

A. Companies finance their assets with either liabilities or equity.

B. A company that finances a relatively large portion of its assets

with liabilities has a high degree of financial leverage.(greater

risk)

C. The debt ratio describes the relationship between a company’s

liabilities and assets. It is calculated as total liabilities divided by

total assets.

D. The debt ratio tells us how much (what percentage) of the assets

are financed by creditors (non-owners), or liability financing. The

higher this ratio, the more risk a company faces, because liabilities

must be repaid and often require regular interest payments.

2-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.