Chapter 18 – Managerial Accounting Concepts and Principles

Chapter 18

Managerial Accounting Concepts and

Principles

QUESTIONS

1. The managerial accountant plays an important role in preparing the information

necessary for effective planning and control decisions. One example is the budget,

2.

Financial Accounting Managerial Accounting

(a) Users and decision

makers

Investors, creditors, and

other users external to the

organization

Managers, employees, and

decision makers internal to

the organization

3. A customer orientation has led companies to adopt the principles of the lean

business model in response to consumer demands. The essence of customer

18-1011

4. Direct labor refers to the efforts of employees who physically convert materials to

finished product. Indirect labor refers to the efforts of factory employees who do not

5. Factory overhead is limited to indirect costs that are incurred in the production

process. That is, it consists of activities that support the production process, such

6. Direct materials are raw materials that physically become part of the product and

can be clearly traced to specific units or batches of product. Indirect materials are

7. Direct labor can be either a prime cost or a conversion cost.

8. Direct costs include: costs of materials such as circuit boards, wires, television

tubes, smartphone cameras, memory chips, and processors, as well as the labor of

9. The production manager should likely not be evaluated on the basis of operating

expenses. Operating expenses are not under the influence of production managers,

and they should not be held accountable for them.

10. Management usually must be able to predict financial performance to be successful.

11. Product costs are capitalized because they represent a future value (an asset) to the

18-1012

12. A manufacturing business produces a product, whereas in a merchandising or

service business this is not the case. In making a product, the manufacturing

13. To run a successful business, management must make predictions and estimates

about what will occur in the future. Thus, managerial accountants must project how

the numbers will look under different possibilities.

14. A manufacturing firm converts raw materials into finished products. A

manufacturing company would report three types of inventories on its balance

sheet: raw materials, work in process, and finished goods. The finished goods are

15. Manufacturers’ balance sheets usually include small tools, factory buildings, factory

16. Manufacturing firms have inventories at various states of completion. Manufacturing

a product requires raw materials, which are converted to finished goods.

17. Manufacturing activities of a company are described in the Schedule of Cost of

18. The three categories of manufacturing costs are: direct materials, direct labor, and

factory overhead.

19. Examples of factory overhead costs include: indirect materials, indirect labor,

depreciation of the factory equipment and plant, amortization of patents, the cost of

20. Components of Schedule of COGM Apple Examples

Direct material……………………………………………………….....Processors, chips, covers

18-1013

Chapter 18 – Managerial Accounting Concepts and Principles

21. Google

Schedule of Cost of Goods Manufactured

For Year Ended December 31, 2015

22. The income statement describes the revenues and expenses for the year. Included in

the calculation of the cost of goods sold is a line item identified as the cost of goods

23. Raw materials inventory turnover and days’ sales in raw materials inventory can be

used to assess raw materials inventory management. Raw materials inventory

24. Yes. Apple can use the concepts and measures of cycle time and cycle efficiency to

evaluate performance on its product offerings.

25. Inventory Components ($ millions) Dell (February 1, 2013)

Production materials………………………..………................... $ 593

QUICK STUDIES

Quick Study 18-1 (5 minutes)

1. Its primary users are company managers. Managerial

2. Its information is often available only after an audit is

Quick Study 18-2 (5 minutes)

1. At her normal usage, your sister’s total cost with Plan A is $80 (fixed).

18-1014

Chapter 18 – Managerial Accounting Concepts and Principles

2. If her usage doubles, your sister’s total cost remains fixed at $80 under

Quick Study 18-3 (5 minutes)

Quick Study 18-4 (10 minutes)

1. Direct materials

Quick Study 18-5 (10 minutes)

1. Product cost

2. Period cost

Quick Study 18-6 (5 minutes)

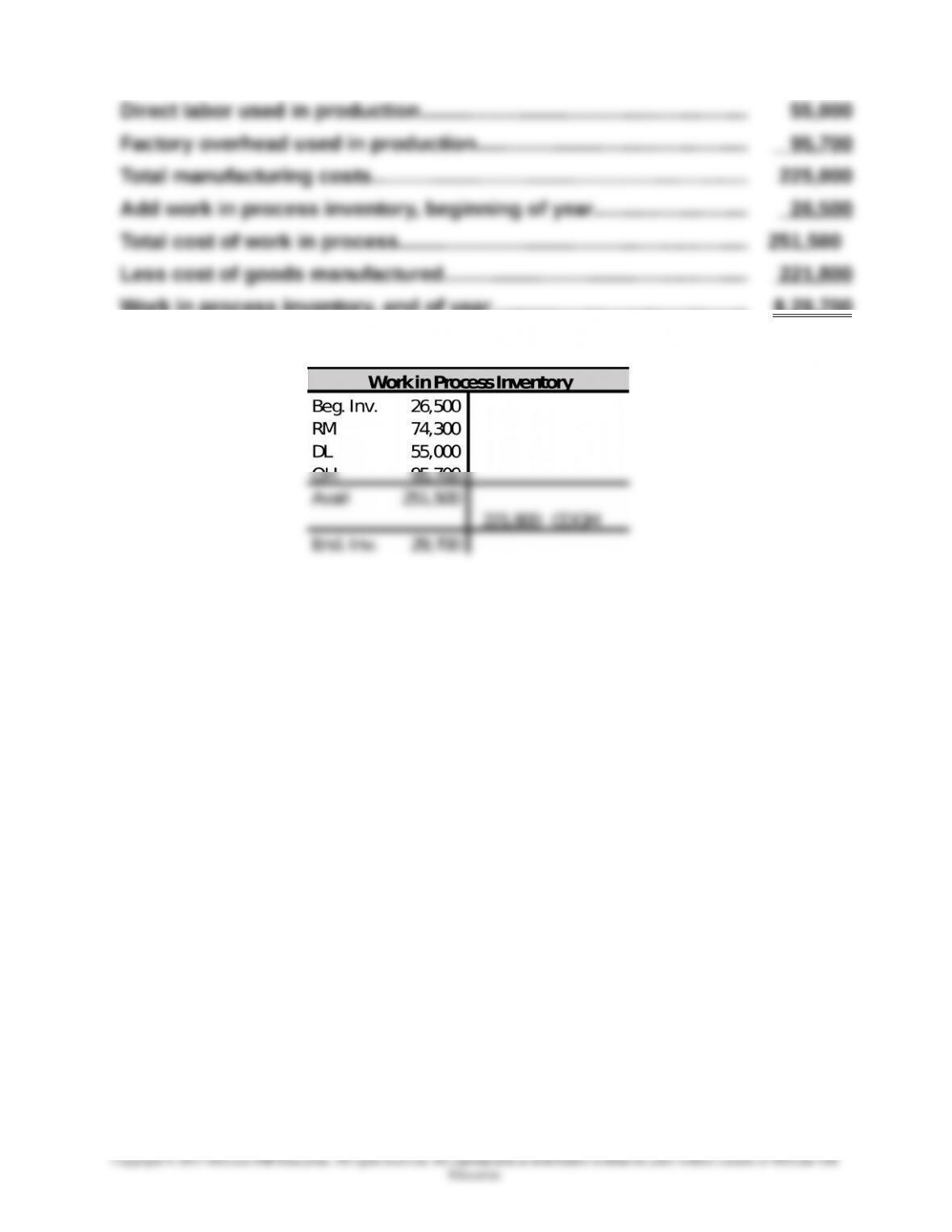

Ending work in process inventory is computed as:

Raw materials used in production………………………………..………..….. $74,300

18-1015

Chapter 18 – Managerial Accounting Concepts and Principles

Work in process inventory, end of year…………………..…………..…….. $ 29,700

18-1016

Chapter 18 – Managerial Accounting Concepts and Principles

Quick Study 18-7 (10 minutes)

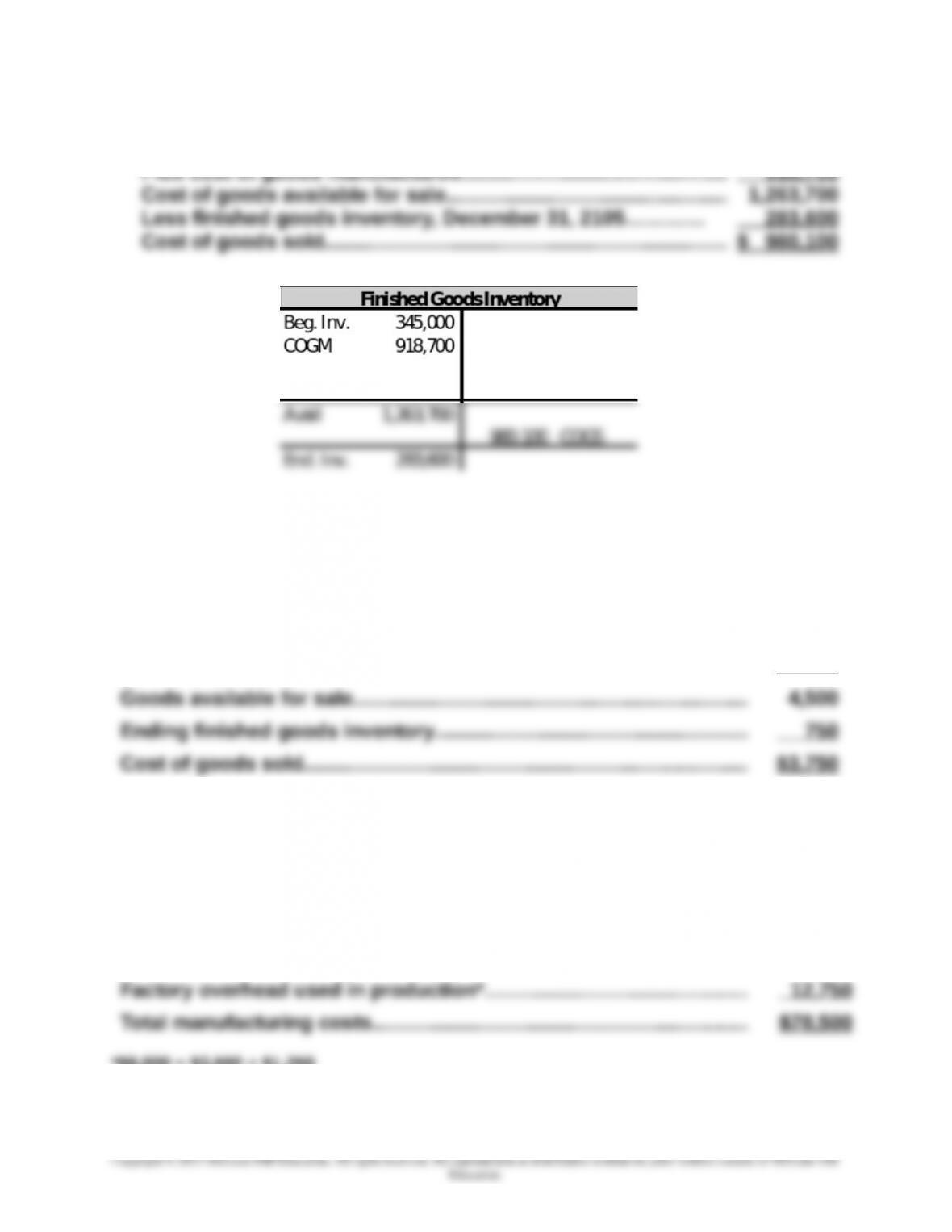

Finished goods inventory, December 31, 2014………………..…… $ 345,000

Quick Study 18-8 (10 minutes)

Cost of goods sold is computed as:

Beginning finished goods inventory………………………..…………..……. $ 500

Cost of goods manufactured……………………………………………………... 4,000

Quick Study 18-9 (5 minutes)

Total manufacturing cost is computed as:

Raw materials used in production………………………………..………..….. $53,750

Direct labor used in production…………………………….………..…………. 12,000

*$8,000 + $3,500 + $1,250

18-1017

Chapter 18 – Managerial Accounting Concepts and Principles

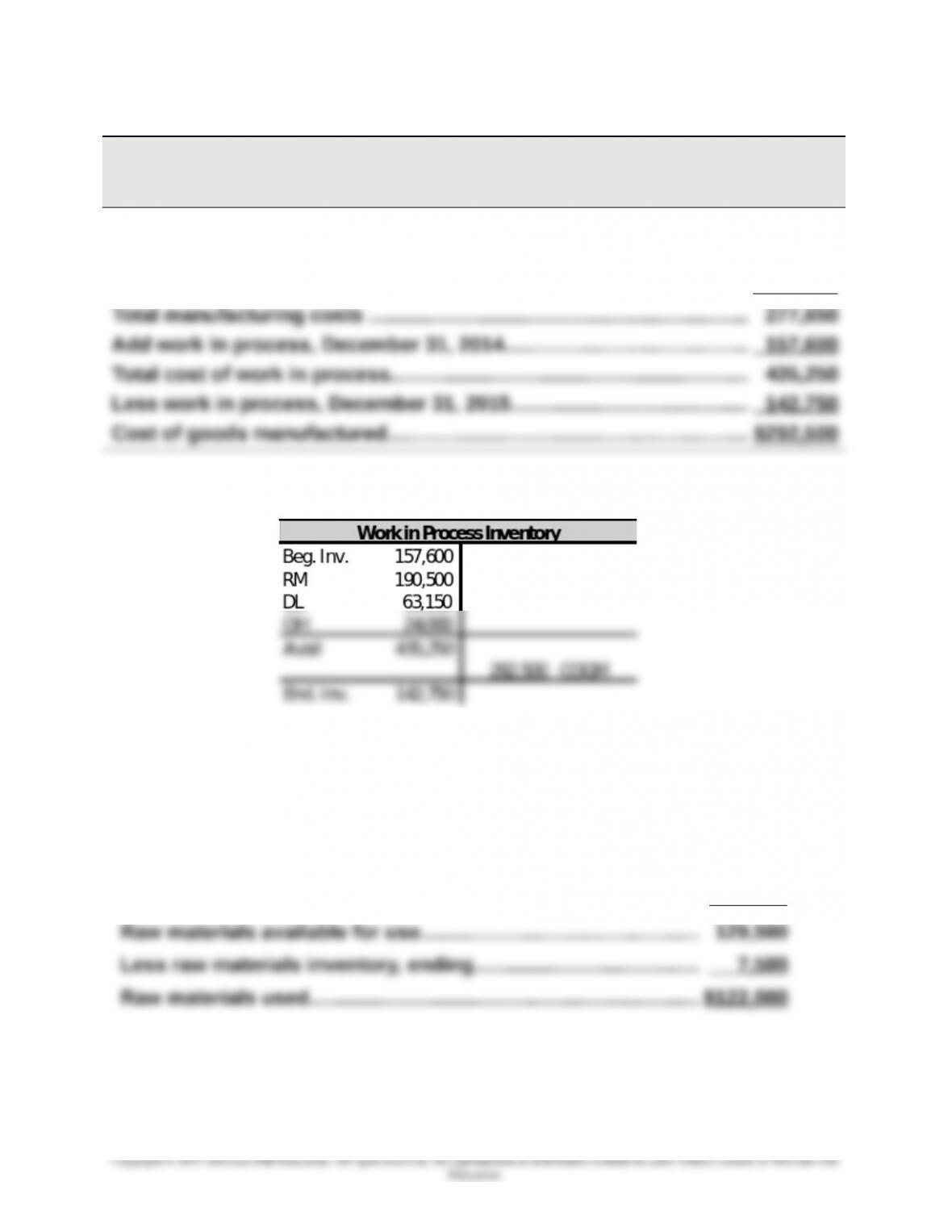

Quick Study 18-10 (15 minutes)

Barton Company

Schedule of Cost of Goods Manufactured

For Year Ended December 31, 2015

Direct materials……………………………………………………….……..………….. $190,500

Direct labor …………………………………………………………………..………..…. 63,150

Factory overhead costs…………………………………………………………....… 24,000

Quick Study 18-11 (5 minutes)

Raw materials inventory, beginning……………..…………..……….. $ 6,000

Plus raw materials purchased……………………………....…………... 123,500

Quick Study 18-12 (10 minutes)

1. D

18-1018

Chapter 18 – Managerial Accounting Concepts and Principles

Quick Study 18-13 (5 minutes)

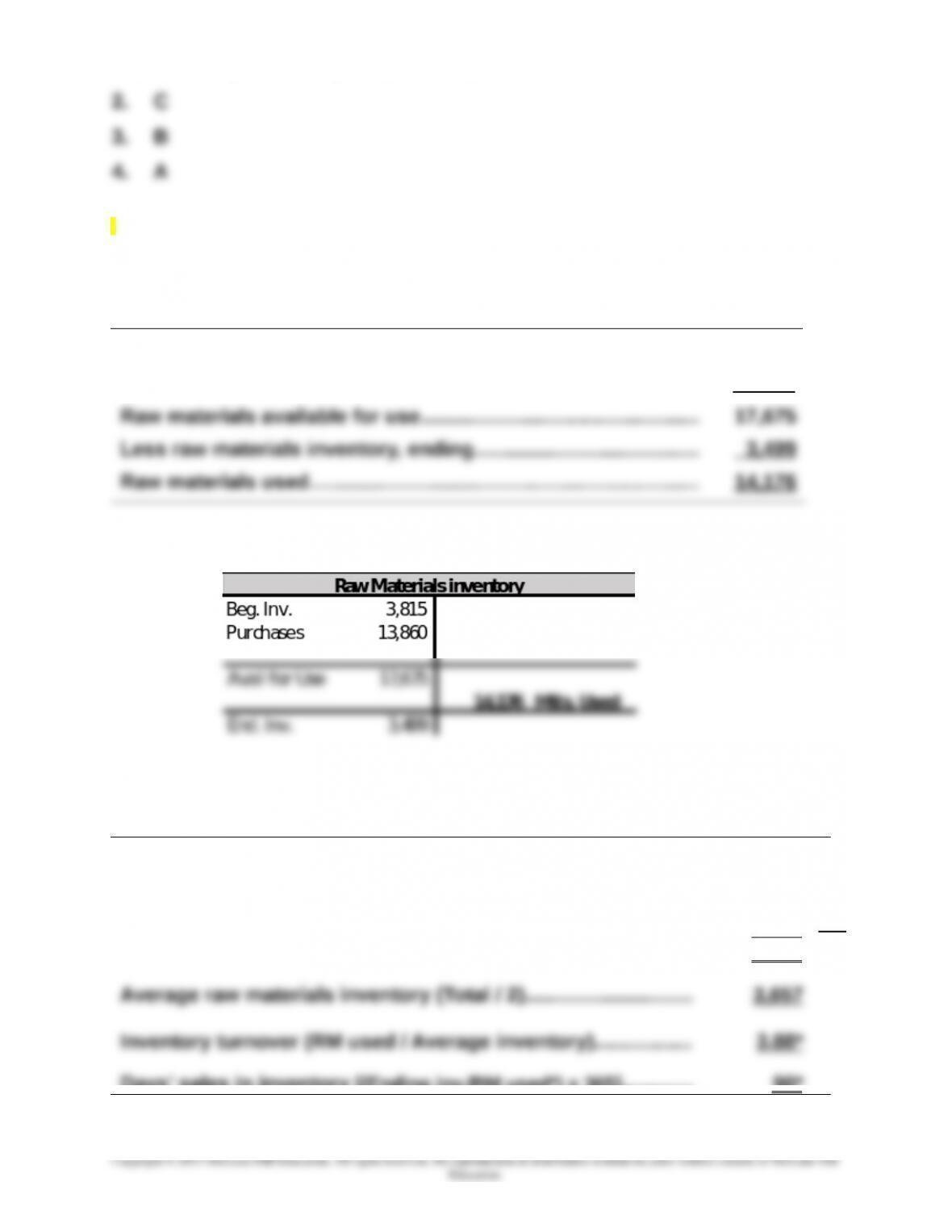

(Amounts in millions of Swiss francs)

Raw materials inventory, beginning……………..…………..……….. 3,815

Plus raw materials purchased……………………………....…………... 13,860

Quick Study 18-14 (10 minutes)

(in millions of Swiss francs)

Cost of raw materials used………………………………………..……… 14,176

Beginning raw materials inventory……………………………..…..… 3,815

Ending raw materials inventory…………………….……..………..…. 3,499

Total beginning plus ending raw materials inventory…………. 7,314

Days’ sales in inventory [(Ending inv./RM used*) x 365]............ 90*

*Rounded

18-1019

18-1020