Chapter 17 – Analysis of Financial Statements

Chapter 17

Analysis of Financial Statements

QUESTIONS

1. Financial reporting includes the entire process of preparing and issuing financial

2. With comparative statements, financial statement items for two or more successive

accounting periods are placed side by side on a single statement, with the change in

3. Total assets (or equivalently, the total of liabilities plus equity) are assigned a value of

100% on a common-size balance sheet. Net sales (revenues) are assigned a value of

100% on a common-size income statement.

4. The nature of a company’s business, the composition of its current assets, and the

5. A 2-to-1 current ratio may not be adequate if the company’s current assets consist of

6. Adequate working capital enables a company to carry sufficient inventories, meet

7. When evaluated in light of a company’s credit terms, the number of days’ sales

8. A high accounts receivable turnover implies that accounts are collected quickly,

17-963

Chapter 17 – Analysis of Financial Statements

9. Users are interested in the capital structure of a company, as measured by debt and

equity ratios, for at least two reasons. First, as a company includes more debt in its

10. Inventory turnover reflects on the efficiency of inventory management. That is, a

high inventory turnover means that a given sales volume can be supported with a

11. Since management is responsible for a company’s performance, all ratios that are

useful in evaluating a company are of some usefulness in assessing management

12. Almost all companies have some liabilities. Since total assets equals total liabilities

plus equity, total assets are almost always higher than common stockholders’ equity.

13. This gain is considered to be unusual but not infrequent. It would be included in the

14. Profit margin: Net Income / Sales ($ in millions)

15. Equity ratio: Total Equity / Total Assets ($ in millions)

2013: $87,309 / $110,920 = 78.7%

2012: $71,715 / $93,798 = 76.5%

16. Debt ratio: Total Liabilities / Total Assets ( in millions)₩

17. Return on total assets: Net Income / Average Total Assets ( in millions)₩

17-964

Chapter 17 – Analysis of Financial Statements

QUICK STUDY

Quick Study 17-1 (5 minutes)

is a. Income statement

is b. Balance sheet

Quick Study 17-2 (10 minutes)

Quick Study 17-3 (15 minutes)

2015 2014

Dollar

Change

Percent

Change

Short-term investments……..……$374,634 $234,000 $140,634 60.1%

17-965

Chapter 17 – Analysis of Financial Statements

Quick Study 17-4 (5 minutes)

Trend percents

Quick Study 17-5 (5 minutes)

Common-size percents

Quick Study 17-6 (10 minutes)

Ratio 2015 2014 Change

1. Profit Margin Ratio…………………..……… 9% 8% Favorable

2. Debt Ratio……………………..………………..47% 42% Unfavorable

17-966

Chapter 17 – Analysis of Financial Statements

Quick-Study 17-7 (30 minutes)

Parker has a greater amount of working capital. This by itself does not

indicate whether the company is more capable of meeting its current

This evidence also shows that Parker’s working capital, current ratio, and

acid-test ratio all increased dramatically over the three-year period. This

generating sales from available inventory. However, these statistics also

may suggest that Morgan is too conservative in granting credit and

investing in inventory. This could have a negative impact on sales and net

income. Parker’s ratios may be acceptable, but no definitive determination

can be made without having information on industry (or other competitors’)

standards.

Quick Study 17-8A (5 minutes)

This material error should be reported on the statement of retained

earnings (and/or the statement of stockholders’ equity) as a prior period

17-967

Chapter 17 – Analysis of Financial Statements

Quick Study 17-9 (10 minutes)

a. Although ratio analysis can eliminate currency differences, it cannot

eliminate differences in the application of GAAP under different

accounting systems. For example, if we compare the gross margin

Additional examples that are arguably even more problematic: (1)

Consider two companies, one reporting under U.S. GAAP and the other

under IFRS, which we are reviewing via the Operating Cash Flow /

Average Total Assets ratio. We can potentially see the dividends and the

interest items reported differently for these two companies under the

two different reporting regimes. That type of difference would persist

accounting systems.

b. A key advantage to using horizontal and vertical analyses when

examining companies reporting under different currencies is that the

EXERCISES

Exercise 17-1 (10 minutes)

17-968

Chapter 17 – Analysis of Financial Statements

Exercise 17-2 (5 minutes)

1. Profit Margin (f); Total Asset Turnover (e) –in either order

Return on Total Assets (d)

Exercise 17-3 (20 minutes)

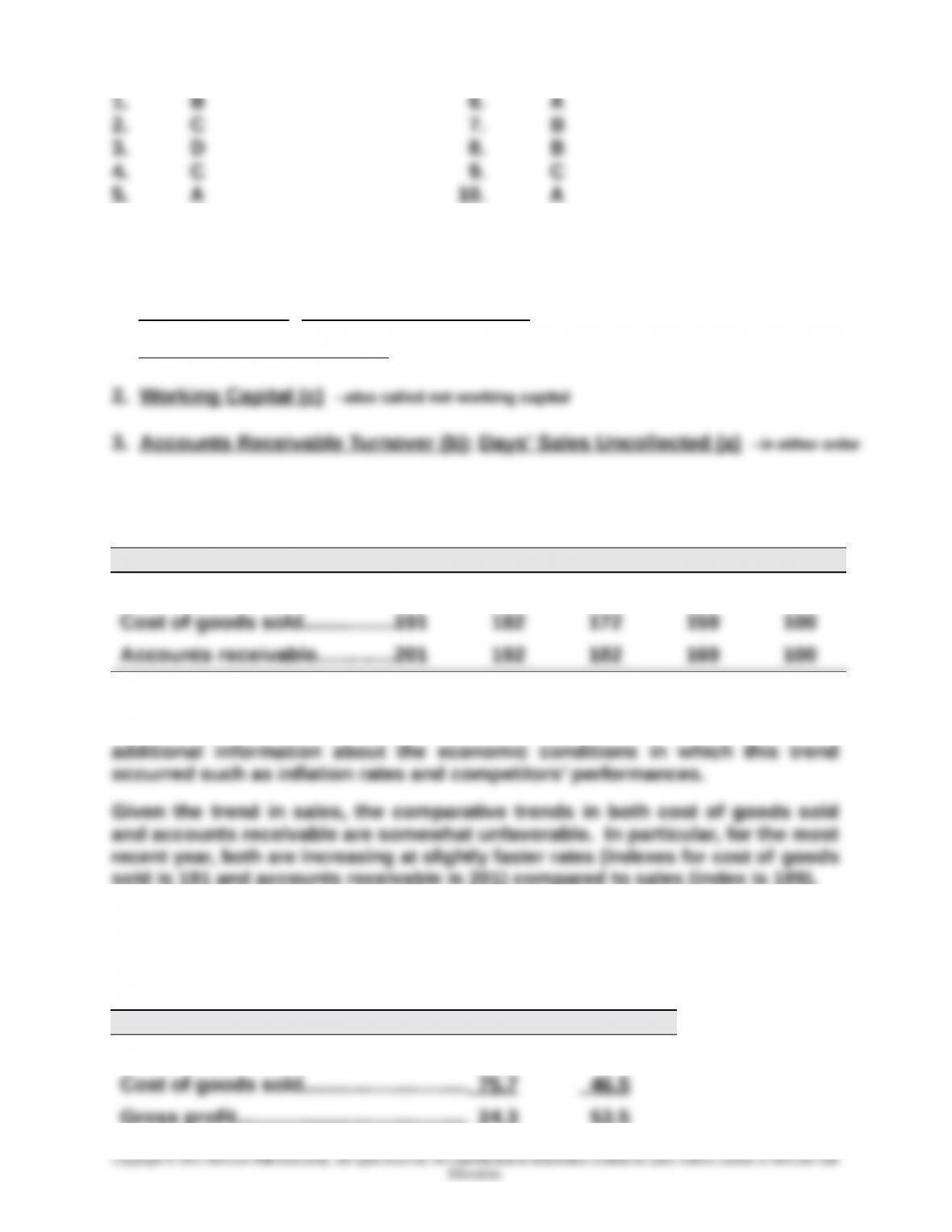

2015 2014 2013 2012 2011

Sales…………………………..…..…189 181 168 156 100

Analysis: The trend in sales is positive. While this is better than no growth,

one cannot definitively say whether the sales trend is favorable without

sold is 191 and accounts receivable is 201) compared to sales (index is 189).

Exercise 17-4 (25 minutes)

2015 2014

Sales……………………..…..………………...100.0% 100.0%

Gross profit………………….………………. 24.3 53.5

17-969

Chapter 17 – Analysis of Financial Statements

Analysis: Overall, this company’s situation has worsened. This is evident from

the substantial decline in net income as a percent of sales for 2015 (7.0%)

Exercise 17-5 (25 minutes)

Answer: Net income decreased.

Supporting calculations: When the sum of each year’s common-size cost of

goods sold and total expenses is subtracted from the common-size sales

percent, the net income percent is as follows:

Next, if 2013 sales are assumed to be $100, then sales for 2014 are $104.20 and

the sales for 2015 are $105.40. If the net income percents for the three years are

applied to these amounts, the net incomes are:

17-970

Chapter 17 – Analysis of Financial Statements

Exercise 17-6 (20 minutes)

Simon Company

Common-Size Comparative Balance Sheets

December 31, 2013-2015

At December 31 2015 2014*2013

Assets

Prepaid expenses………………………..……..……… 2.0 2.1 1.3

Plant assets, net ………………….……………..…….. 53.3 57.3 61.1

Total assets ………………………………..……………..100.0% 100.0% 100.0%

Retained earnings ……………………..……………… 25.1 23.5 21.0

Total liabilities and equity………………….…..……100.0% 100.0% 100.0%

* Column does not equal 100.0 due to rounding.

Analysis: Several observations can be made.

(1) Cash as a percent of assets has declined—this is favorable provided sufficient

cash is available for operations.

downsizing due to poor performance.

(4) Accounts payable have markedly increased as a percent of assets—this could

reveal liquidity constraints.

17-971