Chapter 16 – Reporting the Statement of Cash Flows

Quick Study 16-19 (Concluded)

Part 2

The company’s operating cash flows are negative, $(1,750). This is not a good

omen. However, much of this is attributed to a huge increase in inventory.

Quick Study 16-20 (15 minutes)

1. Under IFRS (as with U.S. GAAP), both the indirect method and direct

method of reporting operating cash flows are acceptable.

2. IFRS and US GAAP differ on the classification of the following cash flows

as operating, investing or financing:

Cash flow source U.S. GAAP IFRS _

16-903

Education.

Chapter 16 – Reporting the Statement of Cash Flows

EXERCISES

Exercise 16-1 (25 minutes)

Statement of Cash Flows Noncash

Operating

Activities

Investing

Activities

Financing

Activities

Investing &

Financing

Activities

Not Reported

on Statement

or in Notes

a. Declared and paid a

cash dividend X

increased in the year X

e. Accounts receivable

decreased in the year X

f. Purchased land by

issuing common stock X

decreased in the year X

j. Income taxes payable

increased in the year X

16-904

Chapter 16 – Reporting the Statement of Cash Flows

Exercise 16-2 (20 minutes)

Cash flows from operating activities—indirect method

Net income………………………………………………………………………..………..…...$ 24,000

Adjustments to reconcile net income to net cash provided by

operating activities

Income statement items not affecting cash

Exercise 16-3 (30 minutes)

1. Cash flows from operating activities—indirect method

Net income (loss)…………………………………………………..…..…..…..…..……….$ (16,000)

Adjustments to reconcile net income to net cash provided by

operating activities

Income statement items not affecting cash

Depreciation expense……………………………………………………………….…..14,600

Changes in current operating assets and liabilities

2. One reason for the net loss was depreciation expense. Depreciation

expense is added to net income to adjust for the effects of a noncash

3. Differences between cash flow from operations and net income can be

caused by various items. The most important causes for investors are

16-905

Chapter 16 – Reporting the Statement of Cash Flows

Exercise 16-4 (30 minutes)

Cash flows from operating activities

Net income…………………………………………………………………… $ 481,540

Adjustments to reconcile net income to net cash

provided by operating activities

Income statement items not affecting cash

Depreciation expense………………………………………………. 44,200

Amortization expense—Patents……………………….…..….. 4,200

Gain on sale of equipment…………………………….……….... (6,200)

Changes in current operating assets and liabilities

Increase in accounts receivable……………………………..… (30,500)

Increase in inventory…………………………………….………... (25,000)

Decrease in accounts payable……..…..…..…..…..…..….... (12,500)

Decrease in salaries payable………………………………..….. (3,500)

Net cash provided by operating activities…………..………..…. $ 452,240

Exercise 16-5 (20 minutes)

Cash flows from operating activities

Net income…………………………………………………………………… $374,000

Adjustments to reconcile net income to net cash

Changes in current operating assets and liabilities

Decrease in accounts receivable………..………..…..…..…. 17,100

Decrease in inventory……………….…..…..………..…..…..… 42,000

Increase in prepaid expenses…………………………………… (4,700)

16-906

Chapter 16 – Reporting the Statement of Cash Flows

Exercise 16-6 (10 minutes)

Gain on sale of machinery………………………………….…..…..(20,000)

Changes in current operating assets and liabilities

Accounts receivable increase……………………….…..…..…...(40,000)

Prepaid expense decrease…………………..…..…..………..…..12,000

Exercise 16-7 (10 minutes)

Cash flows from investing activities

Cash received from the sale of equipment*……….………..…..…..…. $ 51,300

Cash paid for new truck……………………………………..………..…..….... (89,000)

Exercise 16-8 (10 minutes)

Cash flows from financing activities

Sale of common stock…………………………………………………..…..…..…..….... $ 64,000

Paid cash dividend…………………………………………………………………..…..…..(14,600)

Exercise 16-9 (20 minutes)

PEUGEOT S.A.

Statement of Cash Flows (Indirect Method)

For Year Ended December 31, 2011

16-907

Chapter 16 – Reporting the Statement of Cash Flows

Cash flows from operating activities

Net income……………………………………………………….…….. € 784

Adjustments to reconcile net income to net cash

provided by operating activities

Income statement items not affecting cash

Cash flows from investing activities

Cash from disposal of plant assets & intangibles.….… 189

Cash paid for plant assets and intangibles……….…..…. (3,921)

Net cash used in investing activities……..………..…..….. (3,732)

Cash flows from financing activities

Cash from purchases of treasury stock.…..………..….... (199)

Cash paid for dividends………………….…..…..…..……….... (290)

Exercise 16-10 (15 minutes)

Interpretation: Both years’ ratios are good in that they are positive and at

16-908

Chapter 16 – Reporting the Statement of Cash Flows

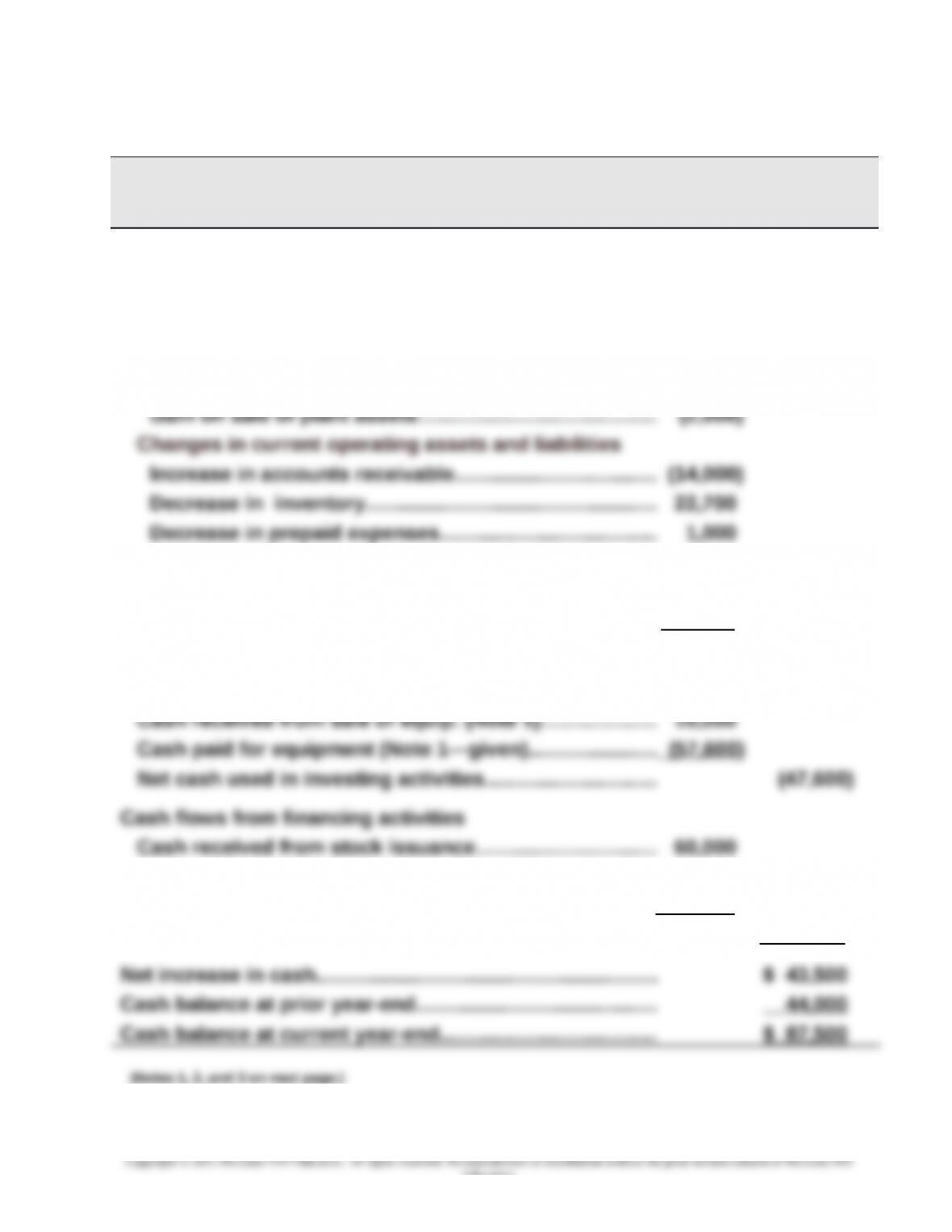

Exercise 16-11 (40 minutes)

Part 1

IKIBAN, INC.

Statement of Cash Flows (Indirect Method)

For Year Ended June 30, 2015

Cash flows from operating activities

Net income………………………………………………..………..…...$ 99,510

Adjustments to reconcile net income to net cash

provided by operating activities

Income statement items not affecting cash

Depreciation expense………………………………….…..…..… 58,600

Decrease in accounts payable……………………………..…. (5,000)

Decrease in wages payable……….…..…..…..…..…..…..… (9,000)

Decrease in income taxes payables………………………… (400)

Net cash provided by operating activities..…..………..…. $151,410

Cash flows from investing activities

Cash paid to retire notes (Note 2—given)………………….. (30,000)

Cash paid for dividends (Note 3)…………….…..…..…..…... (90,310)

Net cash used in financing activities..…..………..…..….... (60,310)

16-909

Education.

Chapter 16 – Reporting the Statement of Cash Flows

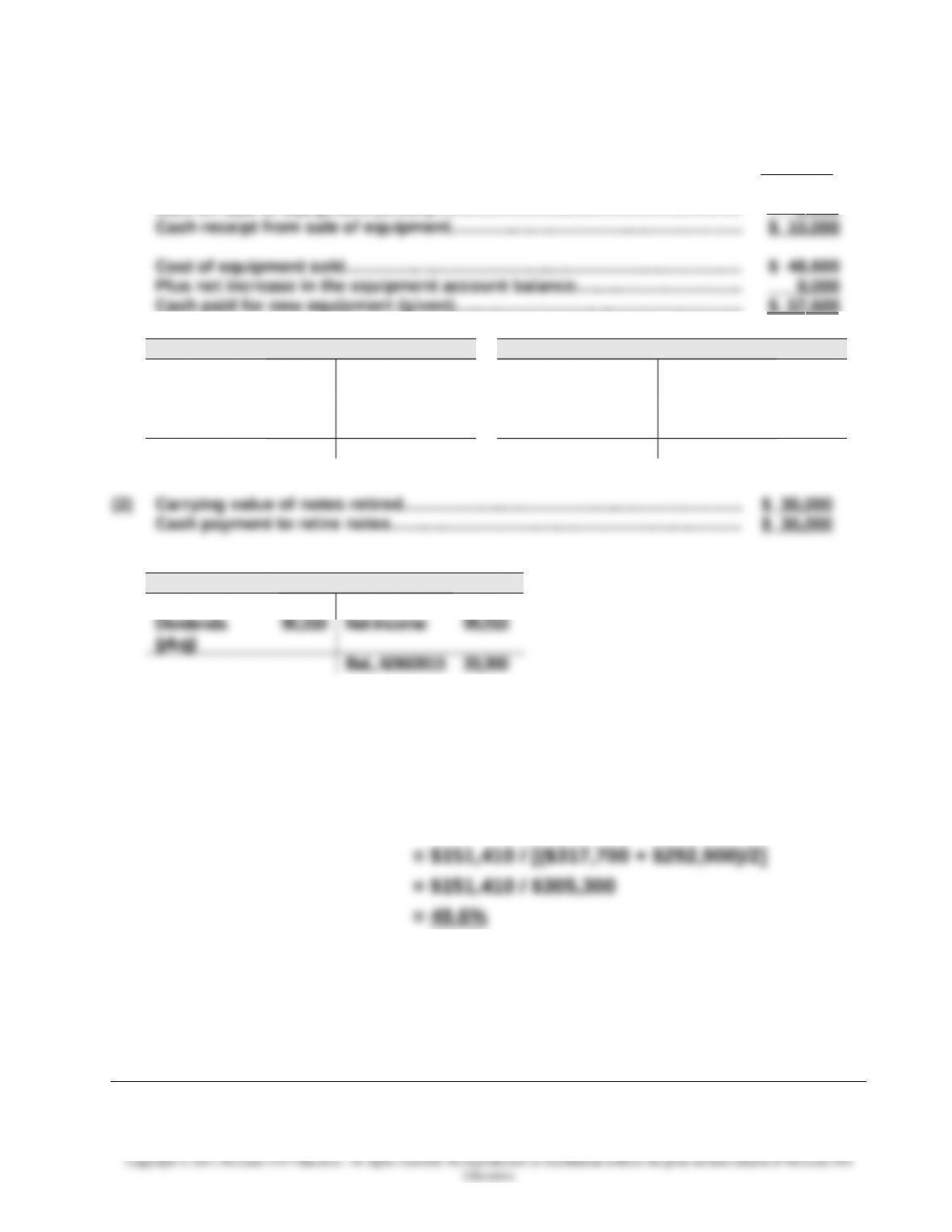

Exercise 16-11 (Part 1 continued)

(1) Cost of equipment sold (Given)……………………………………………………….….. $ 48,600

Accumulated depreciation of equipment sold*………….………..………….……. (40 ,600)

Book value of equipment sold…………………………………………………..…..….… 8,000

Gain on sale of equipment (Given)……………………………………………….…..…. 2 ,000

Equipment Accumulated Depreciation, Equipment

Bal.,

6/30/2014

115,000 Bal., 6/30/2014 9,000

Purchase 57,600 Sale 48,600 Sale (plug)

*40,600

Depr. Expense 58,600

Bal., 6/30/2015 124,000 Bal., 6/30/2015 27,000

(3)

Retained Earnings

Bal., 6/30/2014 24,100

Part 2

Cash flow on total assets ratio = Operating cash flows / Average total assets

Interpretation: A 49.6% result on the cash flow on total assets ratio is

indicative of very good performance. Also, this favorably compares to its

return on assets figure of 32.6% (high-quality earnings).

16-910