Chapter 16 – Reporting the Statement of Cash Flows

Chapter 16

Reporting the Statement of Cash Flows

QUESTIONS

1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and

cash payments (outflows) during a period. It helps users to answer questions such as:

2. On a statement of cash flows, investing activities include cash outflows from purchases

of long-term investments such as stocks and bonds, from purchases of plant assets

3. On a statement of cash flows, financing activities include cash inflows such as those

that result from issuing preferred or common stock, and from borrowing by issuing

4. The direct method of reporting cash flows from operating activities itemizes the major

5. On a statement of cash flows prepared according to the direct method, operating

activities generally include cash receipts from the sale of goods and services, cash

6. The indirect method of reporting cash flows from operating activities begins with net

7. Payments of cash dividends should be reported on the statement of cash flows as

financing activities.

8. The amount of the land purchase that was paid for in cash ($400,000) should be reported

on the statement of cash flows as an investing activity. Also, a schedule of noncash

16-903

Chapter 16 – Reporting the Statement of Cash Flows

9. Since this cash inflow results from borrowing money, it is reported on the statement of

cash flows as a financing activity.

10. Yes; even though a company reports positive net income for the year, it may still show a

net cash outflow from operating activities. When net income is reconciled to the net

11. Depreciation is not a source or a use of cash, even though it must be added to net

12. (a) Indirect method. (b) The increase in accounts (trade) receivable represents an

amount by which the company had cash tied up in accounts (trade) receivable versus

13. Google’s statement of cash flows shows several major financing activities for the year

ended December 31, 2013 ($ millions):

14. Samsung’s net cash (all is KRW millions) from operating activities is 46,707,440; its₩

15. Samsung’s investing activities yielding cash outflows and inflows for the year ended

December 31, 2013, follow. Its cash outflows are listed in parentheses ( in millions):₩

Net decrease (increase) in short-term financial instruments……………..……………. (19,391,643)₩

Net decrease (increase) in short-term available-for-sale financial assets………... 33,663

16-904

Chapter 16 – Reporting the Statement of Cash Flows

QUICK STUDIES

Quick Study 16-1 (10 minutes)

* For the “indirect” method, the loss is reported as an adjustment (add-

back) to net income in the operating section.

Quick Study 16-2 (20 minutes)

Statement of cash flow items in sequential order 1 through 13 on left OR

textbook order on right:

Quick Study 16-3 (20 minutes)

Cash Flows from Operations (Indirect) Case X Case Y Case Z

Net Income…………………………………….…………..… $ 4,000 $100,000 $72,000

Adjustments to reconcile net income to net

cash provided by operations

16-905

Chapter 16 – Reporting the Statement of Cash Flows

Quick Study 16-4 (10 minutes)

Cash flows from operating activities

Net income……………………………………………………………………….. $18,200

Adjustments to reconcile net income to operating cash flow

Income statement items not affecting cash

Quick Study 16-5 (10 minutes)

a. Reconstructed journal entry for equipment sale:

Cash………………………………………….……..…………..…….. 37,000

To record sale of equipment.

Company received $37,000 cash from sale.

b. We reconstruct the T-account for Accumulated Depreciation—Equipment

to determine its Depreciation Expense of $60,000.

Accumulated Depreciation—Equipment

Bal., 2014 210,000

Sale 170,000

c. We reconstruct the T-account for Equipment to determine its purchases of

equipment of $120,000.

Equipment

Bal., 2014 270,000

Sale 210,000

16-906

16-907

Chapter 16 – Reporting the Statement of Cash Flows

Quick Study 16-6 (10 minutes)

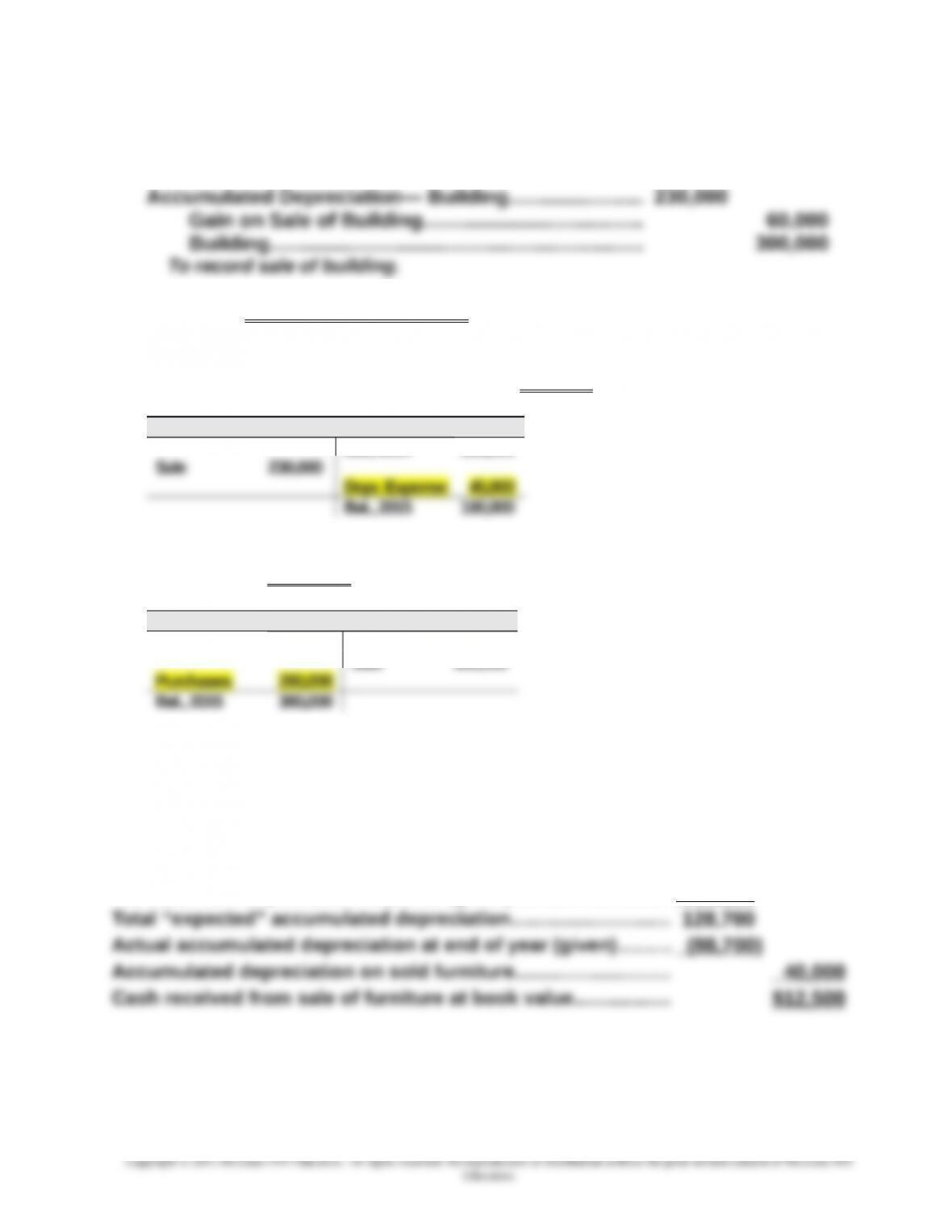

a. Reconstructed journal entry for building sale:

Cash………………………………………….……..…………..…….. 130,000

Company received $130,000 cash from sale.

b. We reconstruct the T-account for Accumulated Depreciation—Building to

determine its Depreciation Expense of $45,000.

Accumulated Depreciation—Building

Bal., 2014 285,000

c. We reconstruct the T-account for Building to determine its purchases of

buildings of $280,000.

Building

Bal., 2014 400,000

Sale 300,000

Quick Study 16-7 (10 minutes)

Computation of cash inflow from sale of furniture

Cost of furniture sold (given)….……….……….............................. $52,500

Accumulated depreciation at beginning of year (given)..........$110,700

Increase from depreciation expense (given)…….……….…......... 18,000

16-908

Chapter 16 – Reporting the Statement of Cash Flows

Quick Study 16-8 (15 minutes)

Investing Activities

Purchase of used equipment……………………………………………………..……..$(5,000)

Quick Study 16-9 (10 minutes)

Part 1

Computation of cash received from the sale of common stock

Increase in Common stock ($105,000 – $100,000)………………………………….$ 5,000

Part 2

Computation of cash paid for dividends

Beginning retained earnings……………………………………………………..………$287,500

Net income………………………………………………………………………..…………..… 48,000

Quick Study 16-10 (15 minutes)

Financing Activities

Quick Study 16-11 (10 minutes)

Cash flows from operating activities

Net income……………………………………………………………………….. $30,000

Adjustments to reconcile net income to operating cash flow

16-909

Education.

Chapter 16 – Reporting the Statement of Cash Flows

Inventory decrease……………………………………..………..………10,000

Prepaid expense increase………………………………………….…. (1,200)

Accounts payable decrease……………..………..…………..……. (6,000)

Quick Study 16-12 (15 minutes)

Computation of cash inflow from sale of furniture

Cost of furniture sold (given)……………………………..……..……. $55,000

Accumulated depreciation at beginning of year (given).......... $ 9,000

Quick Study 16-13 (15 minutes)

1. Computation of cash paid for dividends

Beginning retained earnings……..…………..………..……….. $ 8,400

2. Computation of cash payments for notes

Beginning notes payable…………………………………………… $69,000

16-910

Chapter 16 – Reporting the Statement of Cash Flows

Quick Study 16-14B (10 minutes)

1. Cash received from customers = Sales + Accounts receivable decrease

= $498,000

2. Net increase in cash = $94,800 – $24,000 = $70,800

Quick Study 16-15B (10 minutes)

1. Cash paid for inventory

2. Cash paid for operating expenses

= Operating expenses (excluding depreciation)

+ Prepaid expenses increase – Wages payable increase

Quick Study 16-16B (10 minutes)

Cash flows from operating activities

Receipts from sales to customersa………………..……..………. $ 498,000

Payments for inventoryb…………………………………………….... (310,000)

a From QS 16-14B

b From QS 16-15B

c From QS 16-15B

d $17,300 (income tax expense) + $1,200 (decrease in income taxes payable)

Quick Study 16-17 (10 minutes)

16-911

Chapter 16 – Reporting the Statement of Cash Flows

1. Moore is probably in the strongest position of the three competing companies

on the basis of the statement of cash flows. Moore’s cash flows from

2. Sykes’s cash flow on total assets ratio is slightly stronger than that for Moore.

($70,000/$790,000).

Quick Study 16-18A (10 minutes)

The balance sheet equation can be arranged so that the algebraic total of all

noncash items is equal to cash (see Exhibit 16.9). It follows that when all

Quick Study 16-19 (25 minutes)

Part 1

MONTGOMERY, INC.

Statement of Cash Flows (Indirect Method)

For Year Ended December 31, 2016

Cash flows from operating activities

Net income………………………………………………….…………..………… $ 10,500

Adjustments to reconcile net income to net cash

provided by operating activities

Income statement items not affecting cash

16-912

Chapter 16 – Reporting the Statement of Cash Flows

Cash paid for equipment (Note 1)………………………….………..….. (8,400)

Net cash used in investing activities…………………………….…….. (8,400)

Cash flows from financing activities

Note 1

Equipment

Bal., 12/31/2015 41,500

Purchase “plug” Sale 0 plug = $8,400

Bal., 12/31/2016 49,900

16-913