Chapter 15 – Investments and International Operations

Problem 15-2B (Concluded)

Part 2

Comparison of Cost and Fair Values of AFS Portfolio

Unrealized

Cost Fair Value Gain (Loss)

Nokia (2,550 x $41.25) + $2,250a………. $107,437

$340,232 $298,738 $41,494

a Brokerage fee attached to remaining 2,550 shares: $3,000 x (3,400 sh.– 850 sh.)/ 3,400 sh. = $2,250.

b Brokerage fee attached to remaining 1,200 shares: Entire $1,255 (none sold).

c Brokerage fee attached to remaining 2,500 shares: Entire $2,890 (none sold).

Part 3

Dec. 31 Unrealized Loss—Equity…………………………….……….. 41,494

Fair Value Adjustment—AFS (ST).….…......….. 41,494

To reflect an unrealized loss in fair values of

available-for-sale securities.

Part 4

The balance sheet would report the cost of these short-term investments in

available-for-sale securities at $340,232 and show a subtraction of $41,494

Part 5

(a) Income statement

(i) Interest Revenue, $600

(b) Equity section of Balance sheet

15-1

Chapter 15 – Investments and International Operations

Part 1

2015

Mar. 10 Long-Term Investments—AFS (Apple)………………………………31,400

Cash……………………………………………………………………….… 31,400

Purchased Apple shares

[(1,200 x $25.50) + $800].

Apple: 1,200 x $27.50 = $33,000

Ford: 2,500 x $21.00 = 52,500

Polaroid: 600 x $49.00 = 29,400

$117,773 – $114,900 = $2,873

Problem 15-3B (Continued)

2016

Apr. 26 Cash……………………………………………………………………………….50,043

Loss on Sale of Investments……………………………………..….…7,240

15-2

Chapter 15 – Investments and International Operations

June 2 Long-Term Investments—AFS (Duracell)……………………………35,700

Cash……………………………………………………………………….… 35,700

[(1,200 x $21.00) + $280].

Nov. 27 Cash ………………………………………………………………………………29,755

Gain on Sale of Investments…………………..….….….…..….. 665

Long-Term Investments—AFS (Polaroid)…………….….….…. 29,090

Sold Polaroid shares

* Cost _ Fair Value

Apple…........ $31,400 $34,800

Duracell….... 35,700 32,400

Sears........... 25,480 27,600

Total….……… $92,580 $94,800

Required balance ….. $2,220 Dr.

Unadjusted balance.. 2,873 Cr.

Required change …… $5,093 Dr.

Problem 15-3B (Continued)

2017

Jan. 28 Long-Term Investments—AFS (Coca-Cola)..………………………41,480

Cash ………………………………………………………………………… 41,480

15-3

Education.

Chapter 15 – Investments and International Operations

Long-Term Investments—AFS (Apple)……………………..…. 31,400

Sold Apple shares [(1,200 x $21.50) – $1,850].

Gain on Sale of Investments ………………….….….….….…... 2,721

Long-Term Investments—AFS (Sears)……………………….… 25,480

Sold Sears shares [(1,200 x $24.00) – $599].

Oct. 31 Cash ………………………………………………………………………….…..26,102

Loss on Sale of Investments …………………………………….….…9,598

Long-Term Investments—AFS (Duracell)……………………… 35,700

Sold Duracell shares [(1,800 x $15.00) – $898].

* Cost _ Fair Value

Coca-Cola……..…………….. $ 41,480 $ 48,000

Motorola……….……………… 84,780 72,000

Total…………..………………… $126,260 $120,000

Unadjusted balance. . 2,220 Dr.

Required change..….. $8,480 Cr.

Problem 15-3B (Concluded)

Part 2

12/31/2015 12/31/2016 12/31/2017

Long-Term AFS Securities (cost)……………. $117,773 $92,580 $126,260

15-4

Chapter 15 – Investments and International Operations

Part 3

2015 2016 2017

Realized gains (losses)

Sale of Ford shares..….…..….….….…..... $(7,240)

Sale of Polaroid shares……….….….….… 665

Sale of Duracell shares…….….….….…... $ (9,598)

Sale of Apple shares………………………... (7,450)

Problem 15-4B (50 minutes)

Part 1

1. Journal entries (assuming significant influence)

2015

Jan. 5 Long-Term Investments—Bloch…………………….….….….….….200,500

Cash……………………………………………………………………….…200,500

Purchased Bloch shares.

2016

Aug. 1 Cash…………………………………………………………………………..…..27,000

15-5

Chapter 15 – Investments and International Operations

Long-Term Investments—Bloch……………........................

27,000

Record cash dividend (20,000 x $1.35).

2017

Jan. 8 Cash……………………………………………………………………………….375,000

Long-Term Investments—Bloch*………………………..….…..192,500

Gain on Sale of Investments…………………..….….….…..…..182,500

Sold Bloch shares.

*Investment carrying value at Jan. 7, 2017

Original cost………….………..……………….$200,500

Less 2015 dividends…………..……………. (21,000)

Problem 15-4B (Continued)

2. Carrying value per share (see computations in part 1)

3. Change in Brinkley’s equity

Earnings from Bloch (for 2015)………………..….…$ 20,500

Chapter 15 – Investments and International Operations

Jan. 5 Long-Term Investments—AFS (Bloch)……………………………..200,500

Cash……………………………………………………………………….…200,500

Purchased Bloch shares.

*20,000 x $11.90 = $238,000

$238,000 – $200,500 = $37,500

Problem 15-4B (Concluded)

2016

Aug. 1 Cash…………………………………………………………………………..…..27,000

Dividend Revenue…………………………………….….….….….… 27,000

Received cash dividends (20,000 x $1.35).

2017

Jan. 8 Cash……………………………………………………………………………….375,000

Long-Term Investments—AFS (Bloch)………………………..200,500

Gain on Sale of Investments…………………..….….….…..…..174,500

Sold Bloch shares.

related accounts.

15-7

Chapter 15 – Investments and International Operations

2. Investment cost per share, January 7, 2017

$200,500 / 20,000 shares = $10.03*

*rounded to the nearest cent

3. Change in Brinkley’s equity

Dividend Revenue (for 2015)…………………….…...$ 21,000

Problem 15-5B (40 minutes)

Part 1

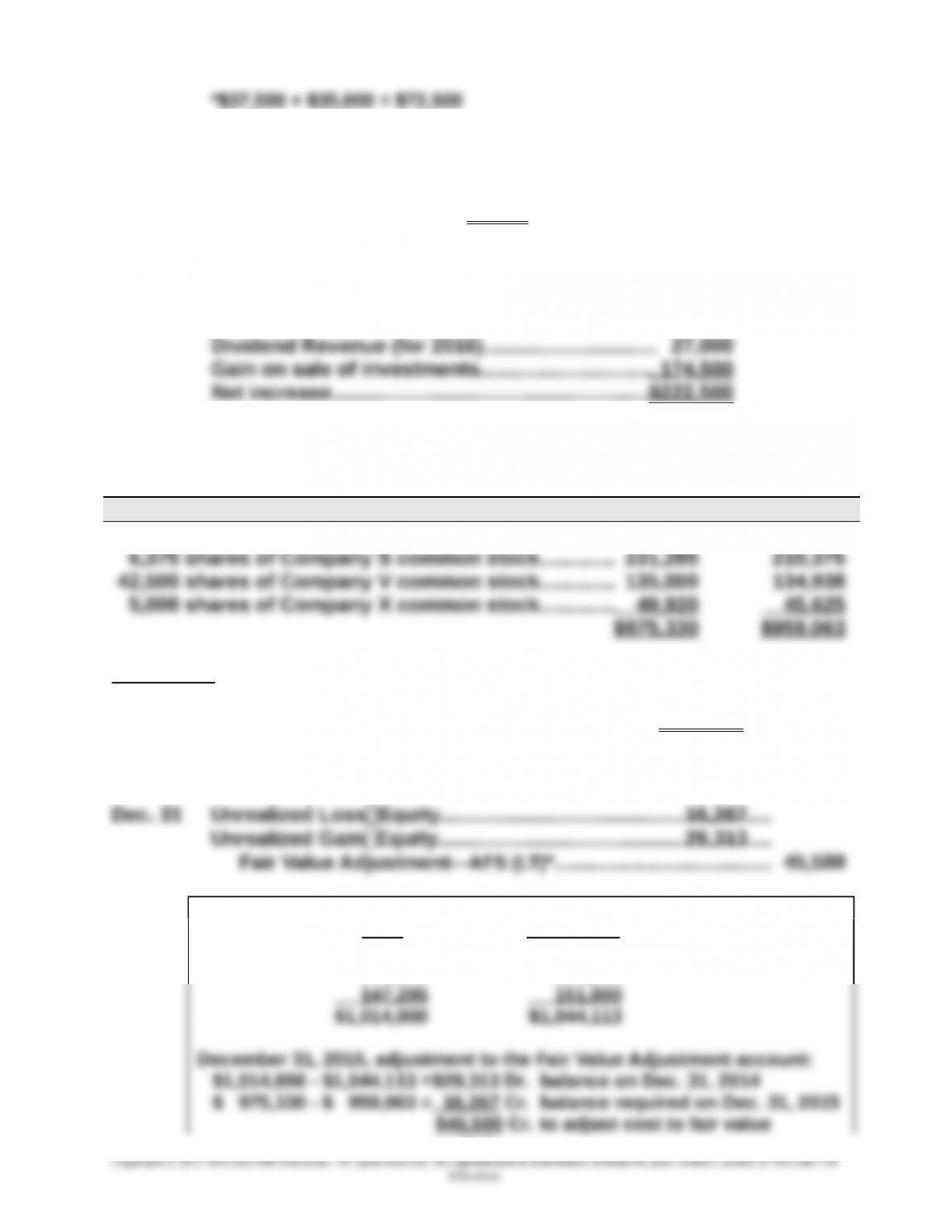

Available-for-sale securities on December 31, 2015

Security Cost Fair Value

27,500 shares of Company R common stock.….….….$559,125 $568,125

Disclosure

The portfolio of available-for-sale securities would be reported on the

December 31, 2015, balance sheet at its fair fair value of $959,063.

Part 2

*December 31, 2014, available-for-sale securities:

Cost Fair Value

$ 559,125 $ 599,063

308,380 293,250

15-8

Chapter 15 – Investments and International Operations

Part 3

Only gains or losses realized on the sale of available-for-sale securities

appear on the 2015 income statement. Unrealized gains or losses appear

in the equity section of the balance sheet.

Year 2015 realized gain (loss)

Stock Sold Cost Sale Gain (Loss)

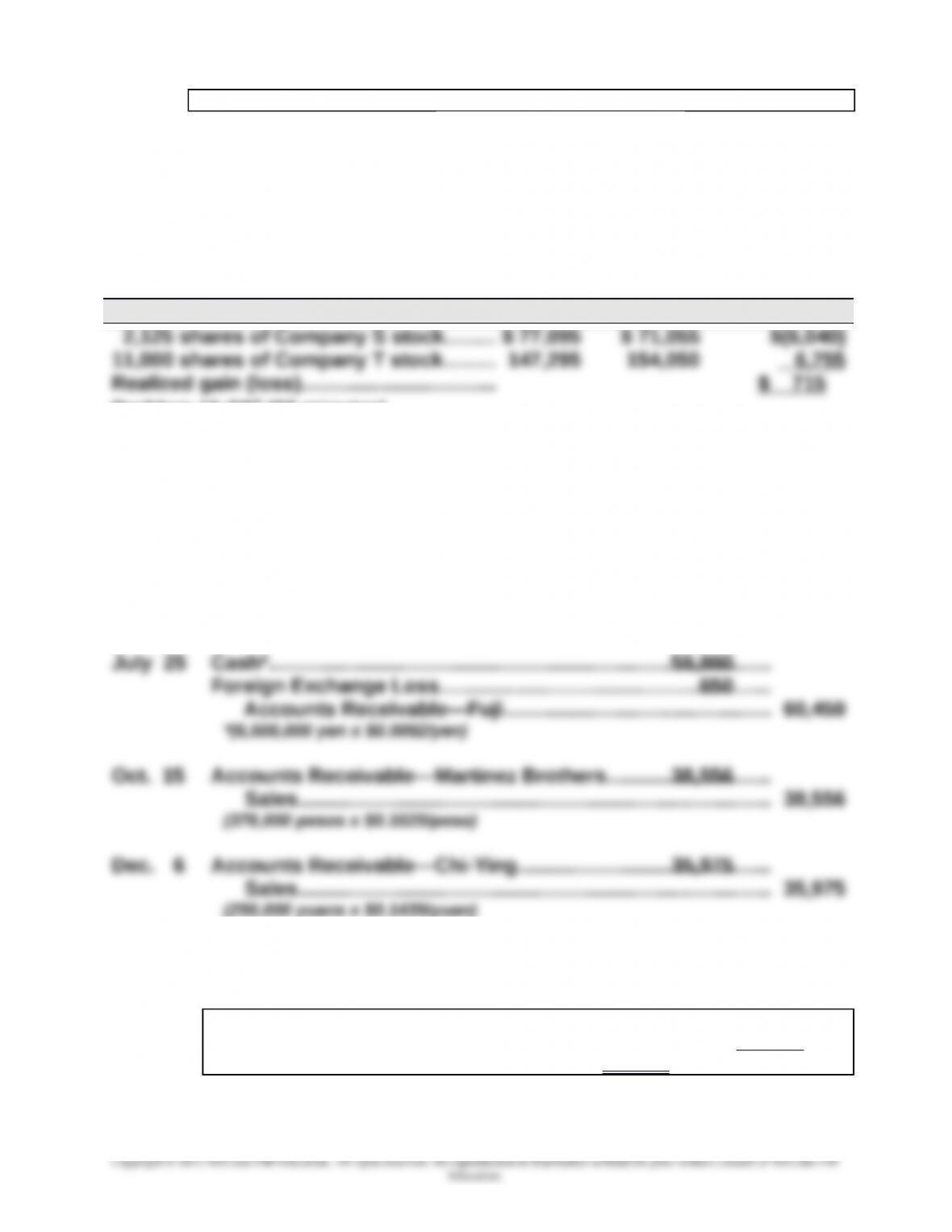

Problem 15-6BA (60 minutes)

Part 1

2015

May 26 Accounts Receivable—Fuji…………………………….….….….….…60,450

Sales………………………………………………………….….….….….. 60,450

(6,500,000 yen x $0.0093/yen)

June 1 Cash…………………………………………………………………………….…64,800

Sales………………………………………………………….….….….….. 64,800

Dec. 31 Accounts Receivable–Martinez Brothers……….….….….….….1,512

Foreign Exchange Gain*……………………………………..….…. 1,512

*Original measure = (378,000 pesos x $0.1020/peso) = $38,556

Year-end measure = (378,000 pesos x $0.1060/peso) = 40,068

Gain for the period …………………………. = $ 1,512

Dec. 31 Accounts Receivable—Chi-Ying……………………………..….…...275

15-9

Chapter 15 – Investments and International Operations

2016

Jan. 5 Cash*……………………………………………………….….….….….….…..39,500

Accounts Receivable—Chi-Ying**…………..….….….….…... 36,250

Foreign Exchange Gain………………………….….….….….…... 3,250

*(250,000 yuans x $0.1580/yuan) **($35,975 + $275)

Part 3

To reduce the risk of foreign exchange gain or loss, Datamix could attempt

to negotiate foreign customer sales that are denominated in U.S. dollars.

To accomplish this, Datamix may be willing to offer favorable terms, such

15-10

15-11