Problem 15-2B (40 minutes)

Part 1

Feb. 6 Short-Term Investments—AFS (Nokia)………… 143,250

15 Short-Term Investments—AFS (T-bills)……….. 20,000

Apr. 7 Short-Term Investments—AFS (Dell)…………… 48,655

June 2 Short-Term Investments—AFS (Merck)……….. 184,140

30 Cash………………………………………………………… 646

Aug. 11 Cash*……………………………………………………… 38,050

16 Cash……………………………………………………….. 20,600

24 Cash……………………………………………………….. 120

Nov. 9 Cash………………………………………………………… 510

Dec. 18 Cash………………………………………………………… 180

Problem 15-2B (Concluded)

Part 2

Comparison of Cost and Fair Values of AFS Portfolio

Unrealized

Cost Fair Value Gain (Loss)

Nokia (2,550 x $41.25) + $2,250a……… $107,437

a Brokerage fee attached to remaining 2,550 shares: $3,000 x (3,400 sh.– 850 sh.)/ 3,400 sh. = $2,250.

Part 3

Dec. 31 Unrealized Loss—Equity…………………………………….. 41,494

Part 4

The balance sheet would report the cost of these short-term investments in

available-for-sale securities at $340,232 and show a subtraction of $41,494

for the fair value adjustment. This yields $298,738 as the net fair value for

these securities reported in the current assets section. An alternative

presentation is to list these securities at the fair value of $298,738 with a

note disclosure of the cost.

Part 5

(a) Income statement

(i) Interest Revenue, $600

(b) Equity section of Balance sheet

Problem 15-3B (60 minutes)

Part 1

2015

Mar. 10 Long-Term Investments—AFS (Apple)……………………………..31,400

Cash………………………………………………………………………. 31,400

April 7 Long-Term Investments—AFS (Ford)……………………………….57,283

Cash………………………………………………………………………. 57,283

Purchased Ford shares

Sept. 1 Long-Term Investments—AFS (Polaroid)………………………….29,090

Dec. 31 Unrealized Loss—Equity………………………………………………..2,873

Fair Value Adjustment—AFS (LT)*………………………………………. 2,873

Annual adjustment to fair values.

* Cost _ Fair Value

Apple…………………$ 31,400 $ 33,000

Problem 15-3B (Continued)

2016

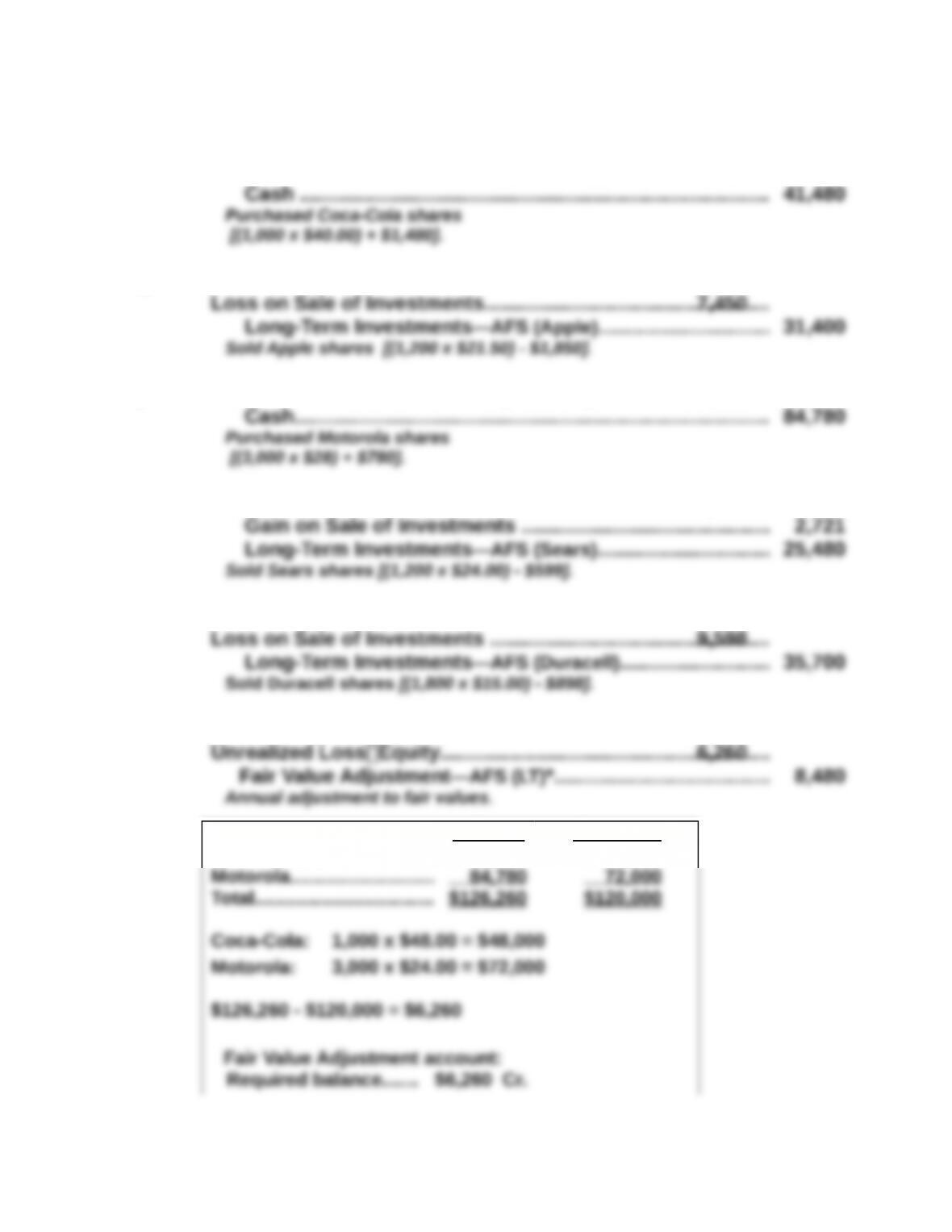

Apr. 26 Cash…………………………………………………………………………….50,043

Loss on Sale of Investments………………………………………….7,240

June 2 Long-Term Investments—AFS (Duracell)…………………………..35,700

Cash………………………………………………………………………. 35,700

Purchased Duracell shares

June 14 Long-Term Investments—AFS (Sears)………………………………25,480

Nov. 27 Cash ……………………………………………………………………………29,755

Gain on Sale of Investments…………………………………….. 665

Dec. 31 Fair Value Adjustment—AFS (LT)*…………………………………………………

5,093

* Cost _ Fair Value

Apple……….. $31,400 $34,800

Apple: 1,200 x $29.00 = $34,800

Fair Value Adjustment account:

Problem 15-3B (Continued)

2017

Jan. 28 Long-Term Investments—AFS (Coca-Cola)……………………….41,480

Aug. 22 Cash ……………………………………………………………………………23,950

Sept. 3 Long-Term Investments—AFS (Motorola)………………………….84,780

Oct. 9 Cash ……………………………………………………………………………28,201

Oct. 31 Cash ……………………………………………………………………………26,102

Dec. 31 Unrealized GainEquity…………………………………………………2,220

* Cost _ Fair Value

Coca-Cola…………………… $ 41,480 $ 48,000

Problem 15-3B (Concluded)

Part 2

12/31/2015 12/31/2016 12/31/2017

Long-Term AFS Securities (cost)…………… $117,773 $92,580 $126,260

Part 3

2015 2016 2017

Realized gains (losses)

Sale of Ford shares…………………………. $(7,240)

Sale of Polaroid shares…………………… 665

Problem 15-4B (50 minutes)

Part 1

1. Journal entries (assuming significant influence)

2015

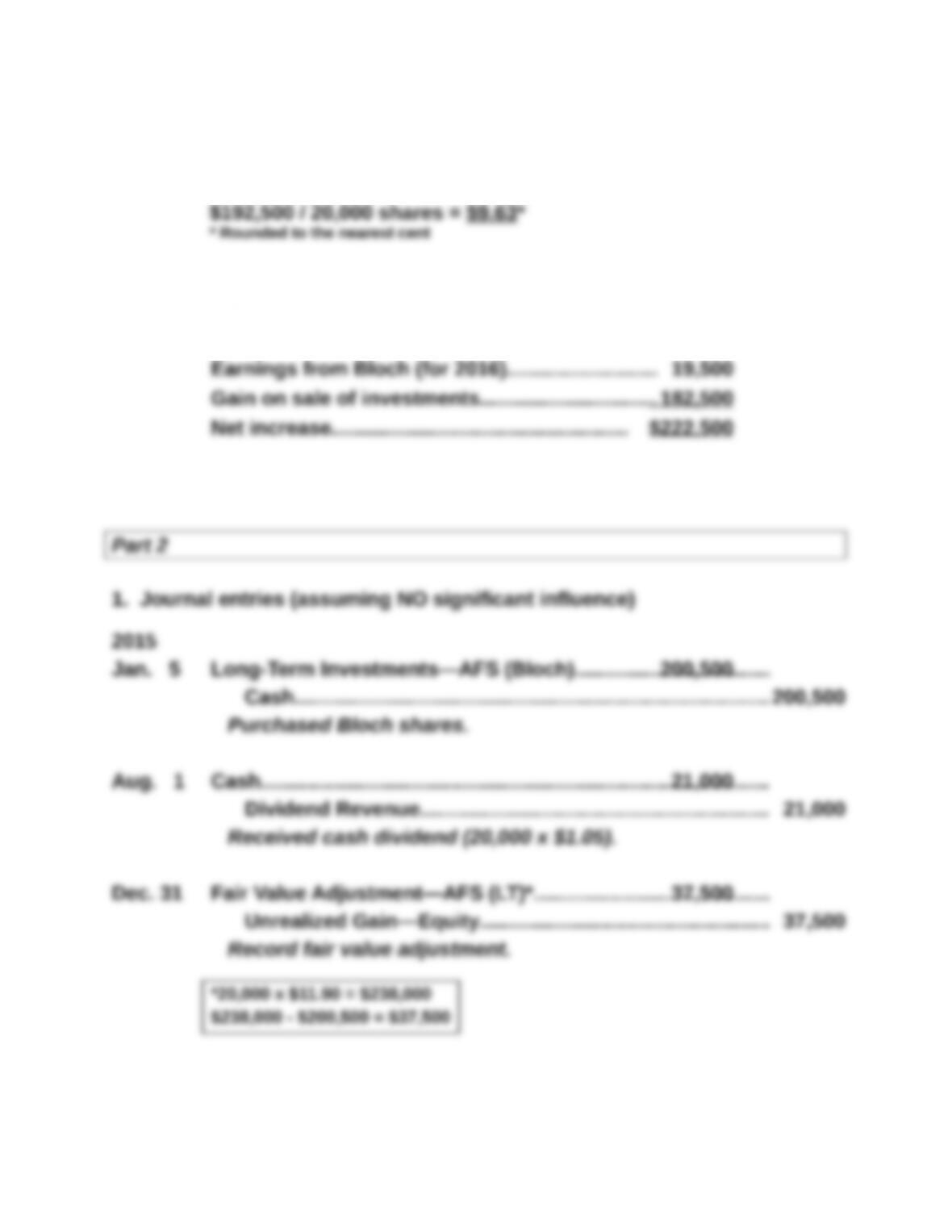

Jan. 5 Long-Term Investments—Bloch……………………………………..200,500

Aug. 1 Cash…………………………………………………………………………….21,000

Dec. 31 Long-Term Investments—Bloch……………………………………..20,500

2016

Aug. 1 Cash…………………………………………………………………………….27,000

Long-Term Investments—Bloch………………………………..

27,000

Record cash dividend (20,000 x $1.35).

Dec. 31 Long-Term Investments (Bloch)……………………………………..19,500

2017

Jan. 8 Cash…………………………………………………………………………….375,000

Sold Bloch shares.

*Investment carrying value at Jan. 7, 2017

Original cost…………………………………..$200,500

Less 2015 dividends……………………….. (21,000)

Problem 15-4B (Continued)

2. Carrying value per share (see computations in part 1)

3. Change in Brinkley’s equity

Earnings from Bloch (for 2015)……………………..$ 20,500

Problem 15-4B (Concluded)

2016

Aug. 1 Cash…………………………………………………………………………….27,000

Dec. 31 Fair Value Adjustment—AFS (LT)*…………………………………..35,000

*20,000 x $13.65 = $273,000

2017

Jan. 8 Cash…………………………………………………………………………….375,000

Jan. 8 Unrealized Gain—Equity………………………………………………..72,500

2. Investment cost per share, January 7, 2017

3. Change in Brinkley’s equity

Dividend Revenue (for 2015)…………………………$ 21,000

Problem 15-5B (40 minutes)

Part 1

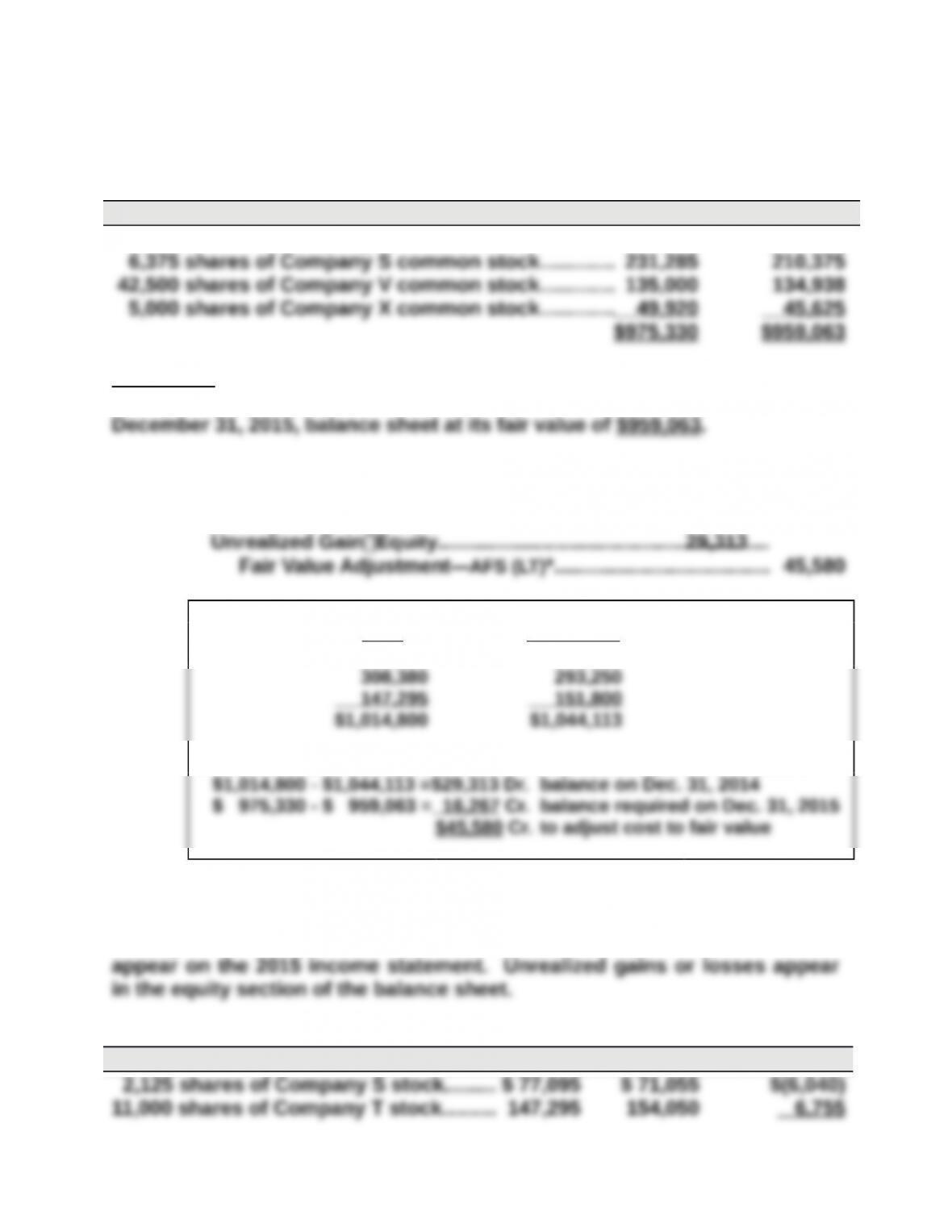

Available-for-sale securities on December 31, 2015

Security Cost Fair Value

27,500 shares of Company R common stock…………$559,125 $568,125

Disclosure

The portfolio of available-for-sale securities would be reported on the

Part 2

Dec. 31 Unrealized LossEquity…………………………………………………16,267

*December 31, 2014, available-for-sale securities:

Cost Fair Value

$ 559,125 $ 599,063

December 31, 2015, adjustment to the Fair Value Adjustment account:

Part 3

Only gains or losses realized on the sale of available-for-sale securities

Year 2015 realized gain (loss)

Stock Sold Cost Sale Gain (Loss)

Problem 15-6BA (60 minutes)

Part 1

2015

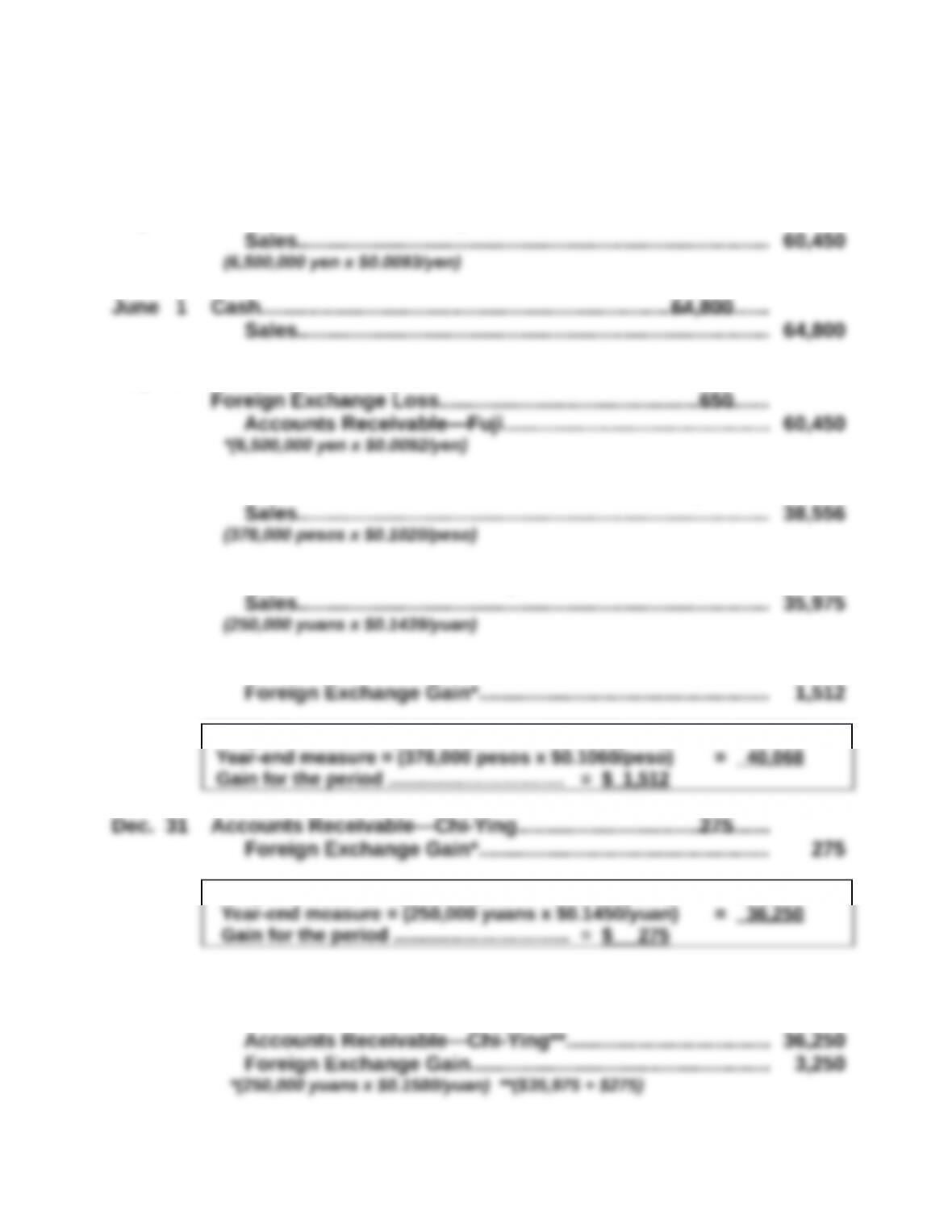

May 26 Accounts Receivable—Fuji…………………………………………….60,450

July 25 Cash*……………………………………………………………………………59,800

Oct. 15 Accounts Receivable—Martinez Brothers……………………….38,556

Dec. 6 Accounts Receivable—Chi-Ying…………………………………….. 35,975

Dec. 31 Accounts Receivable–Martinez Brothers………………………..1,512

*Original measure = (378,000 pesos x $0.1020/peso) = $38,556

*Original measure = (250,000 yuans x $0.1439/yuan) = $35,975

2016

Jan. 5 Cash*……………………………………………………………………………39,500

Jan. 13 Cash*……………………………………………………………………………39,274

Problem 15-6BA (Concluded)

Part 2

Foreign exchange gain reported on 2015 income statement

July 25………………………………………….. $ (650)

Part 3

To reduce the risk of foreign exchange gain or loss, Datamix could attempt

to negotiate foreign customer sales that are denominated in U.S. dollars.

NOTE: A few students may also understand the company’s opportunity for

hedging. This involves selling foreign currency futures to be delivered at the time

the receivables from foreign customers will be collected.