SERIAL PROBLEM — SP 14

Serial Problem — SP 14, Business Solutions (75 minutes)

Part 1

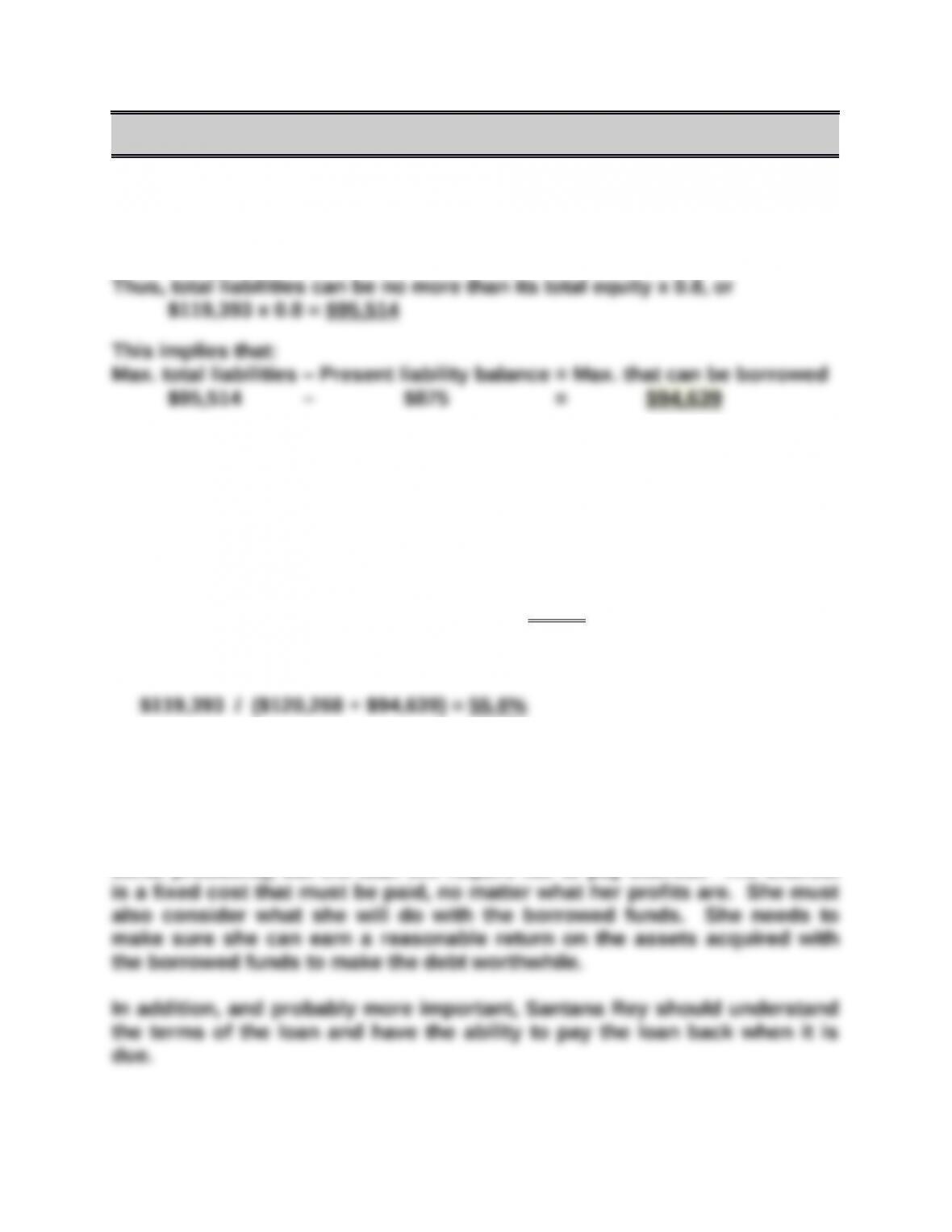

Total equity = $119,393

Part 2

Assume the secured loan is taken, then the percent of assets financed by:

a. Debt

($875 + $94,639) / ($120,268 + $94,639) = 44.4 %

b. Equity

Part 3

Santana Rey should understand the risks she is taking by borrowing funds

from the bank. She currently has no interest-bearing debt (per prior chapter

serial problems), but the loan will require her to pay interest. The interest

Reporting in Action — BTN 14-1

1. Apple reported long-term debt of $16,960 million as of September 28,

2013.

3. Assuming that Apple had $100 million carrying value of convertible

bonds that convert into 20,000 shares of stock, the following entry

would be recorded upon conversion:

4. Answer depends on the financial statement information obtained.

Comparative Analysis — BTN 14-2

1. Apple’s current year debt-to-equity ratio = $83,451 / $123,549 = 0.68

2. For both years, Apple’s debt-to-equity ratio is above that of the industry

average of 0.44. This implies that its debt levels are more risky than that

of its competitors. Conversely, for both years, Google’s debt-to-equity

Ethics Challenge — BTN 14-3

1. The ethics of the Traverse County officials are questionable. The

financial impact of the leasing arrangement is the same as bond

In reality, the taxpayers of Traverse County reacted very negatively to

the actions of the county officials when they learned of the leasing

arrangement. The taxpayers felt that their voice was taken out of the

2. Because the lease requires payments of a non-binding nature, investors

Communicating in Practice — BTN 14-4

MEMORANDUM

TO:

FROM:

SUBJECT:

The body of the memorandum should make the following points:

interest. This means that selling/buying at a premium incurs/yields an

effective rate of interest equivalent to the market rate for the risk assessed

for that bond at the time of issuance. In addition, this market rate of

interest is lower than the contract rate of interest for premium bonds.

A cordial closing that indicates willingness to discuss the issue further

would be appropriate.

Taking It to the Net — BTN 14-5

1. Home Depot’s long-term liabilities as of February 2, 2014, follow:

Long-term debt, excluding current installments............. $14,691

million

2 a. These Home Depot notes offer a 5.875% interest rate. If the interest

rate for similar notes from companies with similar risk was 5.875%,

b. Cash interest that must be paid:

$3,000,000,000 x 0.05875 x ½ year = $88,125,000

Teamwork in Action — BTN 14-6

Parts 1 and 2

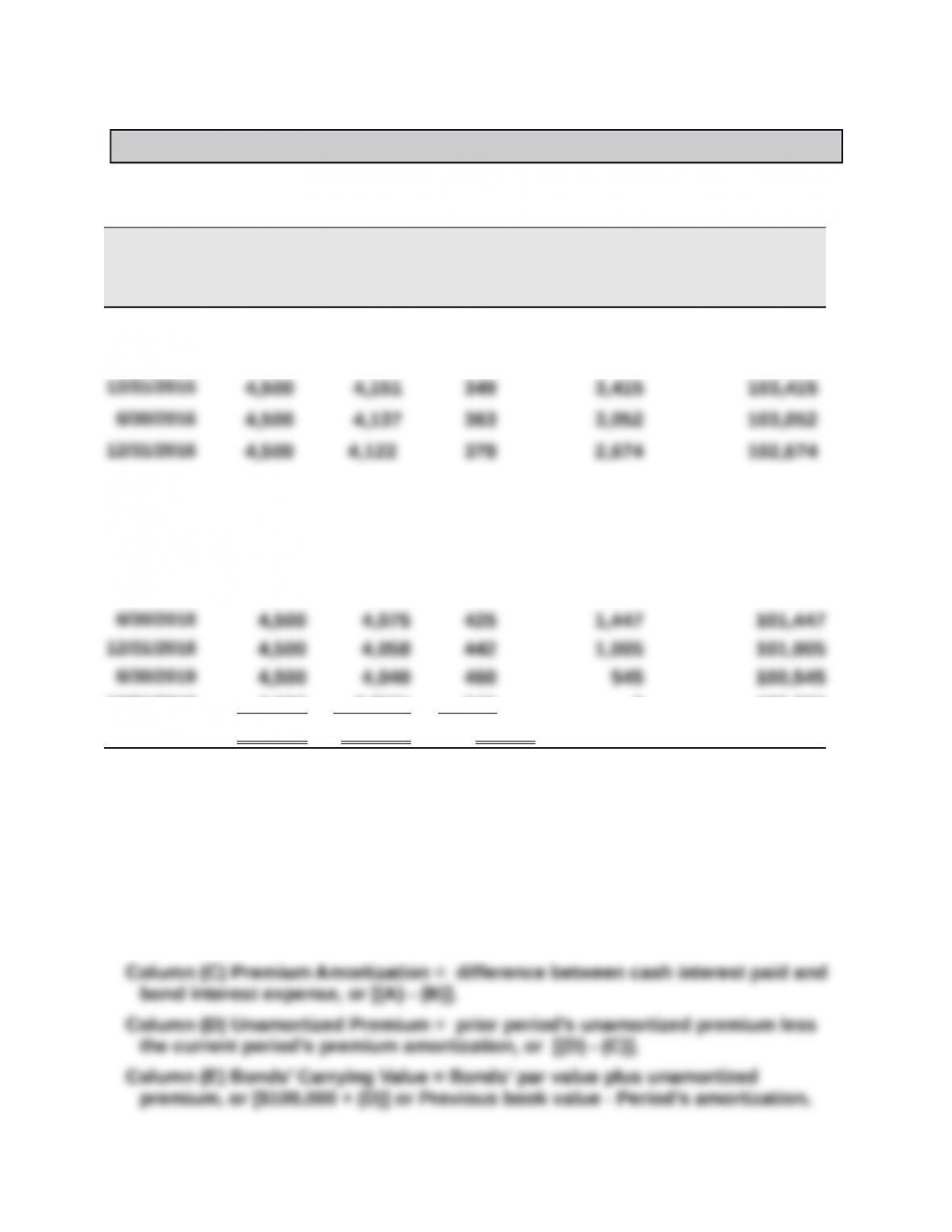

Effective Interest Amortization of Bond Premium

Semi-

annual

Period-end

(A)

Cash

Interest

Paid

(B)

Bond

Interest

Expense

(C)

Premium

Amortization

(D)

Unamortized

Premium

(E)

Carrying

Value

1/01/2015 $ 4,100 $ 104,100

6/30/2015 $ 4,500 $ 4,164 $ 336 3,764 103,764

6/30/2017 4,500 4,107 393 2,281 102,281

Since teams generally have 4 or 5 members, the team solution will likely end about

here. The remainder of the table is shown for help in answering part 3.

12/31/2017 4,500 4,091 409 1,872 101,872

12/31/2019 4 ,500 3 ,955* 545 0 100,000

$45 ,000 $40 ,900 $4 ,100

*Discrepancy due to rounding.

The following computations should be articulated by team members as

each line is explained and prepared:

Column (A) Cash Interest Paid = Bonds’ par value ($100,000) x Semiannual

contract rate (4.5%).

Column (B) Bond interest expense = Bonds’ prior period carrying value x

Semiannual market rate (4%).

Teamwork in Action (Concluded)

Part 3

Without completing the table, team members should be able to project the

final number in the first column and for each of the columns (A), (D), and

(E). Specifically:

(Col. 1) Last interest period date is 12/31/2019 because this is a five-year

bond, issued 1/1/2015, with semiannual interest payments made

on 6/30 and 12/31 of each year.

Part 4

Total Bond interest expense = Interest Paid – Premium

= ($4,500 x 10 periods) – $4,100

= $45,000 – $4,100 = $40,900

Part 5 List likely includes:

Similarities Differences

a. Table column headings

for the period and for

columns (A), (B), and (E).

a. Column (C) will be Discount Amortization and

Column (D) will be Unamortized Discount.

b. Dates in the period

column and interest paid in

column (A).

b. Bond interest expense is higher (lower) than the

interest paid and will increase (decrease) as we

amortize a discount (premium).

in both cases.

f. Unamortized discount

f. Computation of Column (E) will be previous Column

(E) plus discount amortization whereas with a

each period

Entrepreneurial Decision — BTN 14-7

Part 1

The table below reveals how the five alternative interest-bearing notes

would affect this company’s interest expense, net income, equity, and

return on equity (net income/equity):

Alternative Notes for Expansion

Current 10% Note 15% Note 16% Note 17% Note 20% Note

Income before

interest………….. $ 40,000 $ 56,000 $ 56,000 $ 56,000 $ 56,000 $ 56,000

Return on equity. . . 12% 14.4% 12.4% 12% 11.6% 10.4%

Part 2

The analysis in Part 1 illustrates the general rule (called “financial

leverage” or “trading on the equity”): When a company earns a higher

return with borrowed funds than it is paying in interest, it increases its

less than 16%.

The table in Part 1 reveals this result, where those notes with interest

expense below 16% are profitable (that is, yield a return greater than the

Hitting the Road — BTN 14-8

Global Decision — BTN 14-9

1. Samsung’s current year debt-to-equity ratio (in KRW millions):

Samsung’s prior year debt-to-equity ratio (in KRW millions):

2. Samsung’s debt-to-equity ratio decreased slightly from the prior year to

the current year. For the current year, Samsung’s debt-to-equity ratio is