Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 14-8BB (60 minutes)

Part 1

2015

Jan. 1 Cash.................................................................................198,494

Part 2

Thirty payments of $7,200*........................ $ 216,000

Par value at maturity.................................. 240,000

or:

Thirty payments of $7,200......................... $ 216,000

Plus discount............................................. 41,506

Total bond interest expense..................... $ 257,506

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[3% x $240,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Discount

Amortization

[(B) - (A)]

(D)

Unamortized

Discount

[Prior (D) - (C)]

(E)

Carrying

Value

[$240,000 - (D)]

1/01/2015 $41,506 $198,494

6/30/2015 $7,200 $7,940 $740 40,766 199,234

Problem 14-8BB (Concluded)

Part 4

2015

June 30 Bond Interest Expense..................................................7,940

2015

Dec. 31 Bond Interest Expense..................................................7,969

Problem 14-9BB (45 minutes)

Part 1

Ten payments of $14,400........................... $144,000

Par value at maturity.................................. 320 ,000

Total repaid................................................. 464,000

Part 2

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[4.5% x $320,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Premium

Amortization

[(A) - (B)]

(D)

Unamortized

Premium

[Prior (D) - (C)]

(E)

Carrying

Value

[$320,000 + (D)]

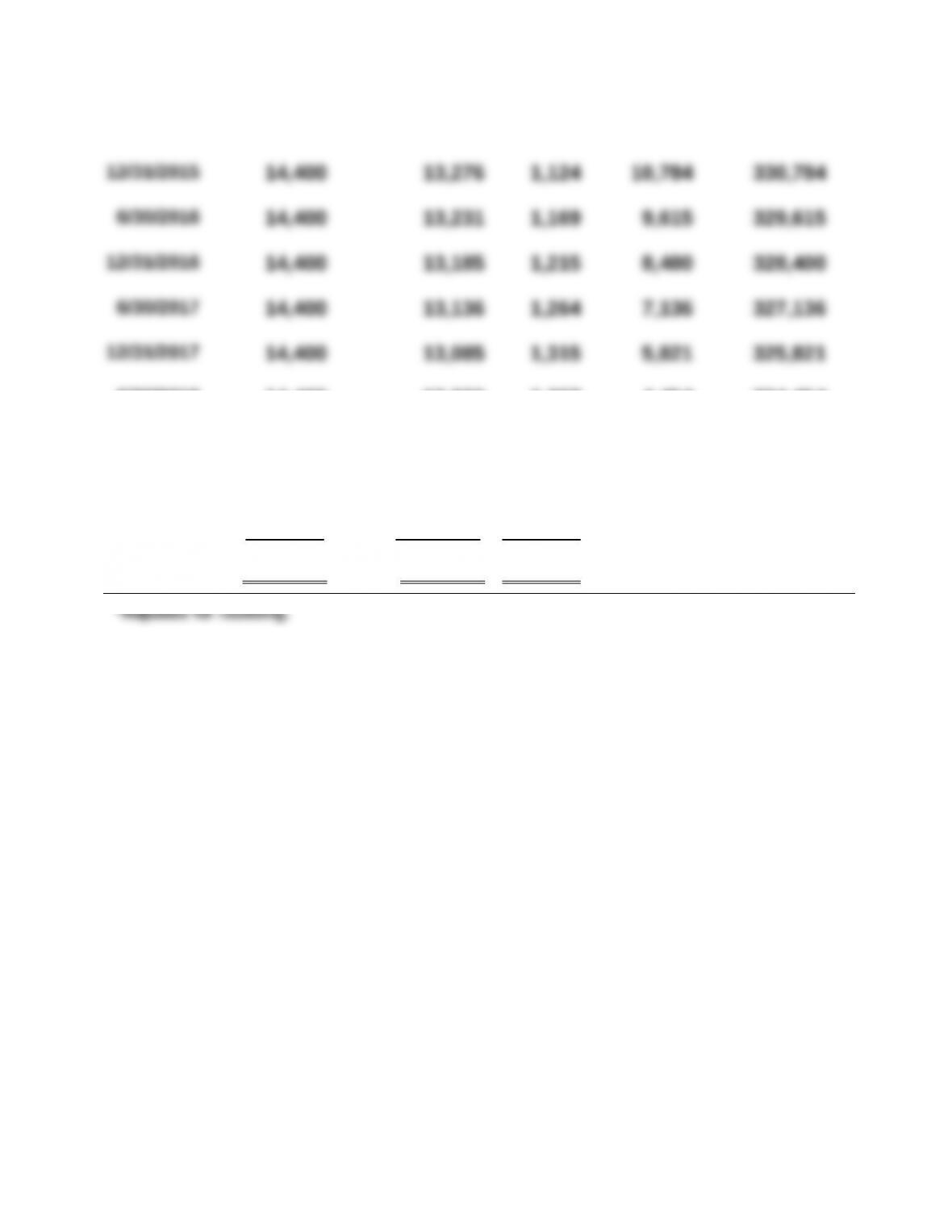

1/01/2015 $12,988 $332,988

6/30/2015 $ 14,400 $ 13,320 $ 1,080 11,908 331,908

6/30/2018 14,400 13,033 1,367 4,454 324,454

12/31/2018 14,400 12,978 1,422 3,032 323,032

6/30/2019 14,400 12,921 1,479 1,553 321,553

12/31/2019 14,400 12 ,847* 1,553 0 320,000

$144,000 $131 ,012 $ 12,988

Problem 14-9BB (Concluded)

Part 3

2015

June 30 Bond Interest Expense..................................................13,320

Premium on Bonds Payable..........................................1,080

Cash........................................................................... 14,400

To record six months’ interest and

premium amortization.

2015

Dec. 31 Bond Interest Expense..................................................13,276

Part 4

As of December 31, 2017

Cash Flow Table Table Value* Amount Present Value

* Table values are based on a discount rate of 4% (half the annual original market

rate) and 4 periods (semiannual payments).

Comparison to Part 2 Table

Except for a small rounding difference, this present value ($325,807) equals

the market rate at the time of issuance.

Problem 14-10BB (70 minutes)

Part 1

2015

Jan. 1 Cash.................................................................................493,608

Part 2

Eight payments of $29,250*...................... $ 234,000

Par value at maturity.................................. 450 ,000

Total repaid................................................. 684,000

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[6.5% x $450,000]

(B)

Bond Interest

Expense

[5% x Prior (E)]

(C)

Premium

Amortization

[(A) - (B)]

(D)

Unamortized

Premium

[Prior (D) - (C)]

(E)

Carrying

Value

[$450,000 + (D)]

1/01/2015 $43,608 $493,608

6/30/2015 $29,250 $24,680 $4,570 39,038 489,038

Problem 14-10BB (Concluded)

Part 4

2015

June 30 Bond Interest Expense..................................................24,680

2015

Dec. 31 Bond Interest Expense..................................................24,452

Part 5

2017

Jan. 1 Bonds Payable ...............................................................450,000

Part 6

If the market rate on the issue date had been 14% instead of 10%, the bonds

would have sold at a discount because the contract rate of 13% would have been

lower than the market rate.

This change would affect the balance sheet because the bond liability would be

smaller (par value minus a discount instead of par value plus a premium). As the

The statement of cash flows would show a smaller amount of cash received from

borrowing. However, the cash flow statements presented over the life of the

Problem 14-11BD (35 minutes)

Part 1

Present Value of the Lease Payments

Part 2

Part 3

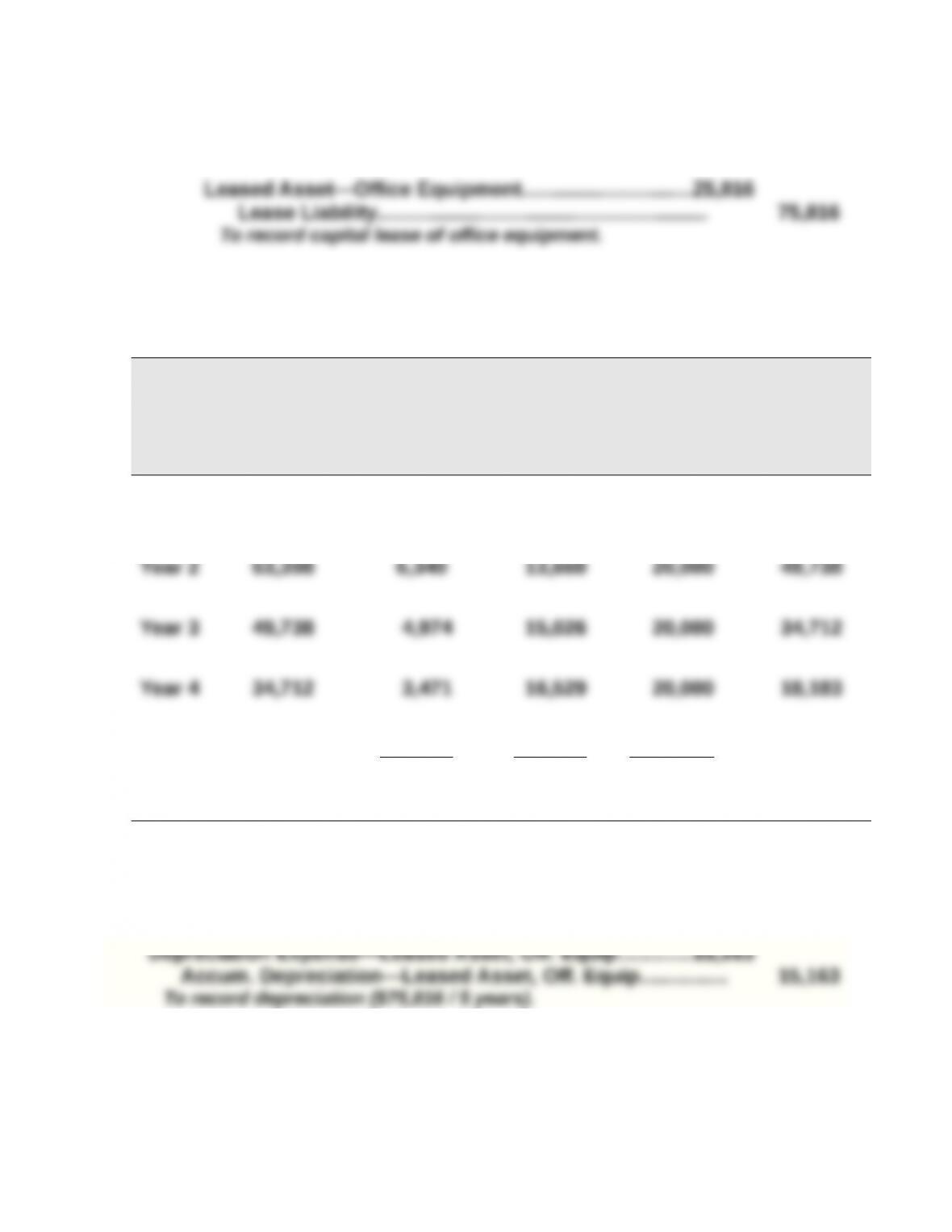

Capital Lease Liability Payment (Amortization) Schedule

Period

Endin

g

Date

Beginning

Balance of

Lease

Liability

Interest on

Lease

Liability

(10%)

Reduction

of Lease

Liability

Cash

Lease

Payment

Ending

Balance of

Lease

Liability

Year 1 $75,816 $ 7,582* $12,418 $ 20,000 $63,398

Year 5 18,183 1,817** 18,183 20,000 0

$24,184 $75,816 $100,000

* Rounded to nearest dollar.

** Adjusted for prior period rounding errors.

Part 4