Problem 14-9BB (45 minutes)

Part 1

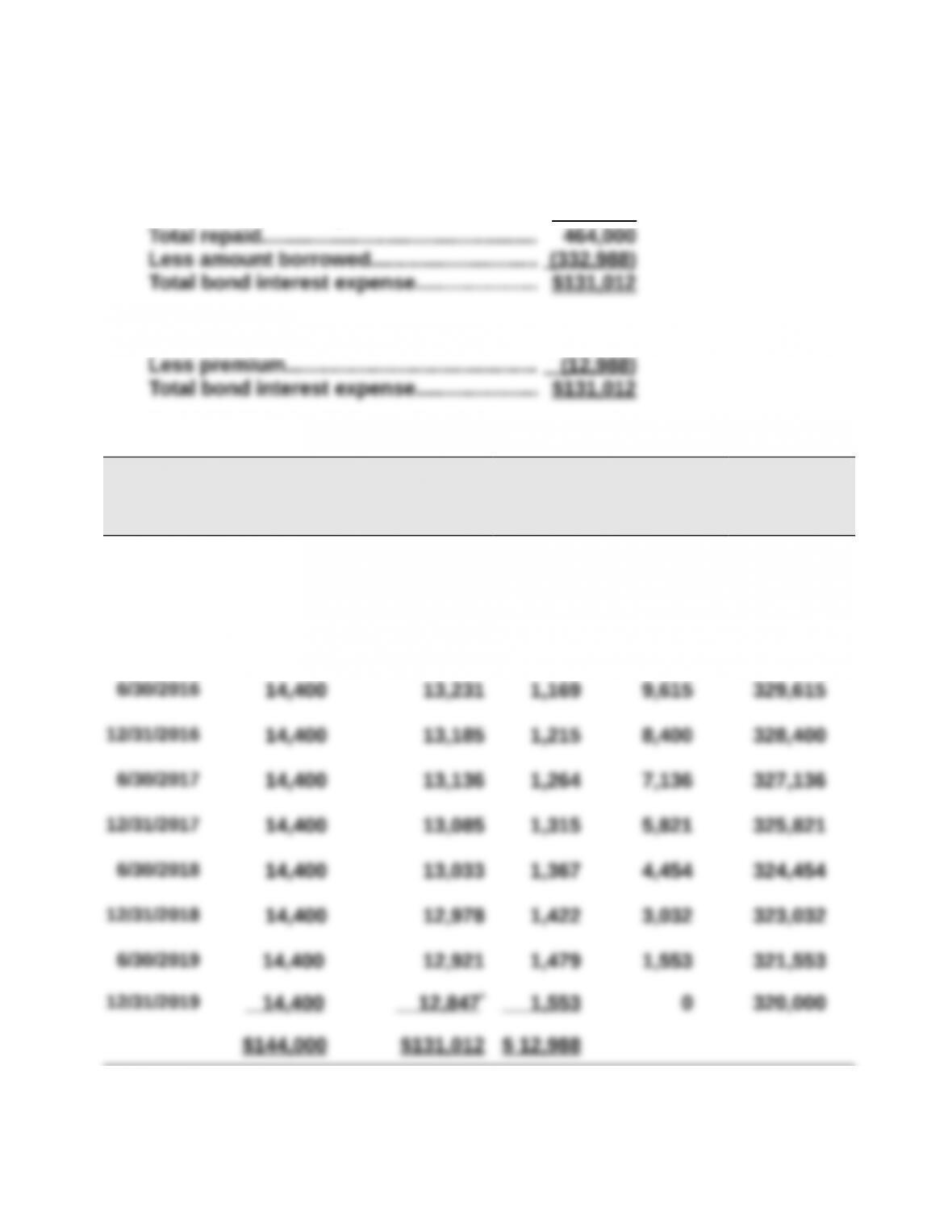

Ten payments of $14,400…………………….. $144,000

Par value at maturity…………………………… 320 ,000

or:

Ten payments of $14,400…………………….. $144,000

Part 2

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[4.5% x $320,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$320,000 + (D)]

1/01/2015 $12,988 $332,988

6/30/2015 $ 14,400 $ 13,320 $ 1,080 11,908 331,908

12/31/2015 14,400 13,276 1,124 10,784 330,784

*Adjusted for rounding.

Problem 14-9BB (Concluded)

Part 3

2015

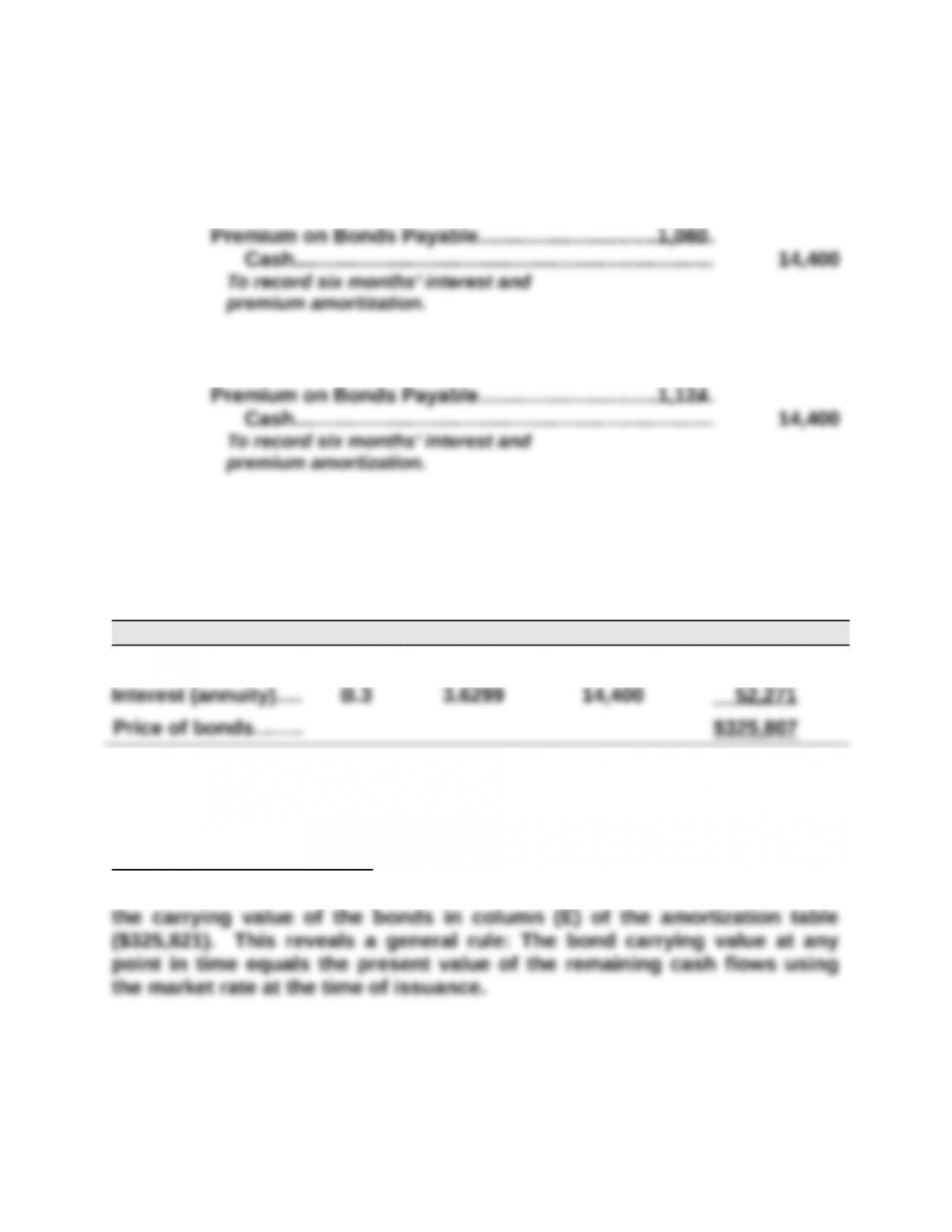

June 30 Bond Interest Expense………………………………………….13,320

2015

Dec. 31 Bond Interest Expense………………………………………….13,276

Part 4

As of December 31, 2017

Cash Flow Table Table Value* Amount Present Value

Par value…………….. B.1 0.8548 $320,000 $273,536

* Table values are based on a discount rate of 4% (half the annual original market

rate) and 4 periods (semiannual payments).

Comparison to Part 2 Table

Except for a small rounding difference, this present value ($325,807) equals

Problem 14-10BB (70 minutes)

Part 1

2015

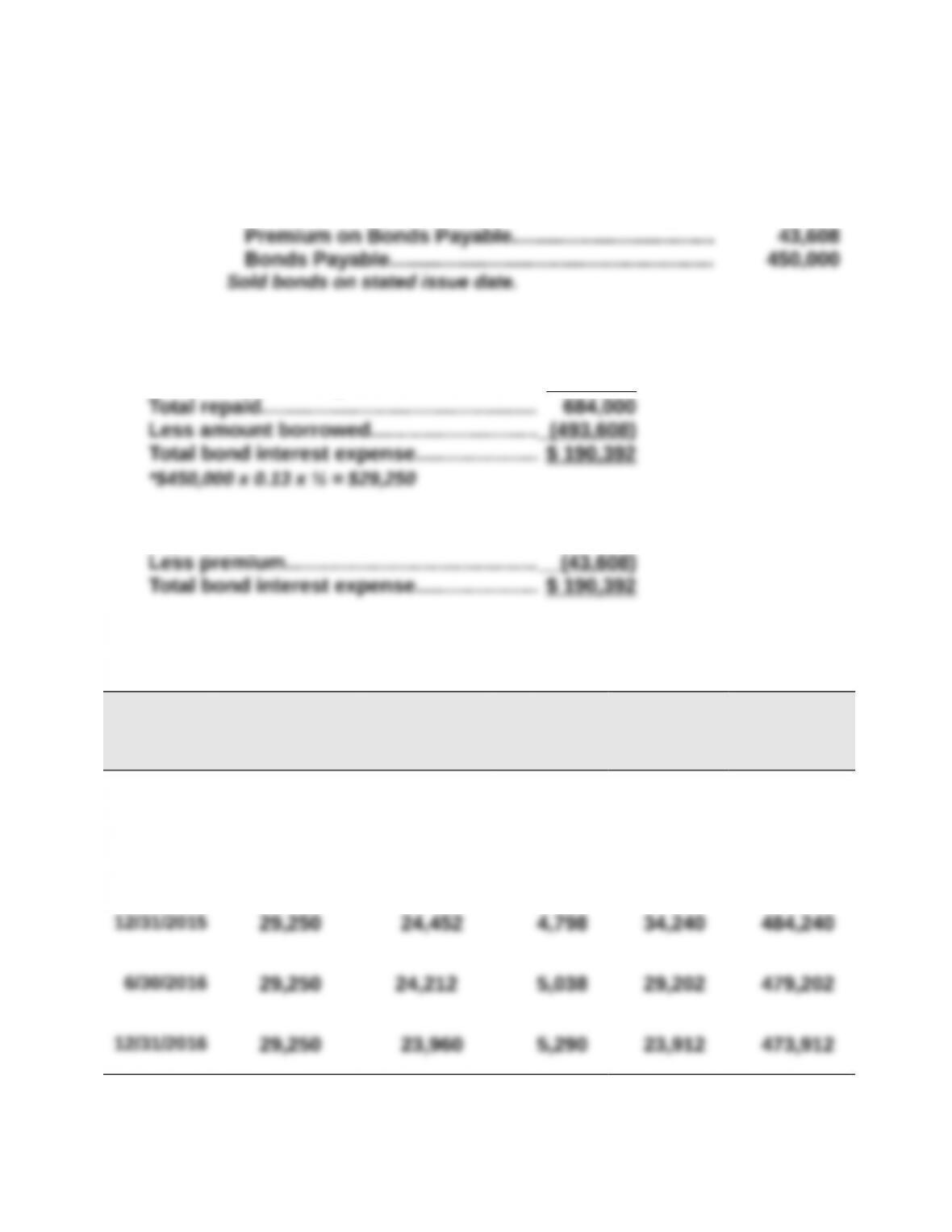

Jan. 1 Cash……………………………………………………………………493,608

Part 2

Eight payments of $29,250*…………………. $ 234,000

Par value at maturity…………………………… 450 ,000

or:

Eight payments of $29,250………………….. $ 234,000

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[6.5% x $450,000]

(B)

Bond Interest

Expense

[5% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$450,000 + (D)]

1/01/2015 $43,608 $493,608

6/30/2015 $29,250 $24,680 $4,570 39,038 489,038

Problem 14-10BB (Concluded)

Part 4

2015

June 30 Bond Interest Expense………………………………………….24,680

2015

Dec. 31 Bond Interest Expense………………………………………….24,452

Part 5

2017

Jan. 1 Bonds Payable …………………………………………………….450,000

Part 6

If the market rate on the issue date had been 14% instead of 10%, the bonds

This change would affect the balance sheet because the bond liability would be

The income statement would show larger amounts of bond interest expense over

The statement of cash flows would show a smaller amount of cash received from

Problem 14-11BD (35 minutes)

Part 1

Present Value of the Lease Payments

Part 2

Leased Asset—Office Equipment…………………………..75,816

Part 3

Capital Lease Liability Payment (Amortization) Schedule

Period

Endin

g

Date

Beginning

Balance of

Lease

Liability

Interest on

Lease

Liability

(10%)

Reduction

of Lease

Liability

Cash

Lease

Payment

Ending

Balance of

Lease

Liability

Year 1 $75,816 $ 7,582* $12,418 $ 20,000 $63,398

Year 2 63,398 6,340 13,660 20,000 49,738

* Rounded to nearest dollar.

** Adjusted for prior period rounding errors.

Part 4

To record depreciation ($75,816 / 5 years).

SERIAL PROBLEM — SP 14

Serial Problem — SP 14, Business Solutions (75 minutes)

Part 1

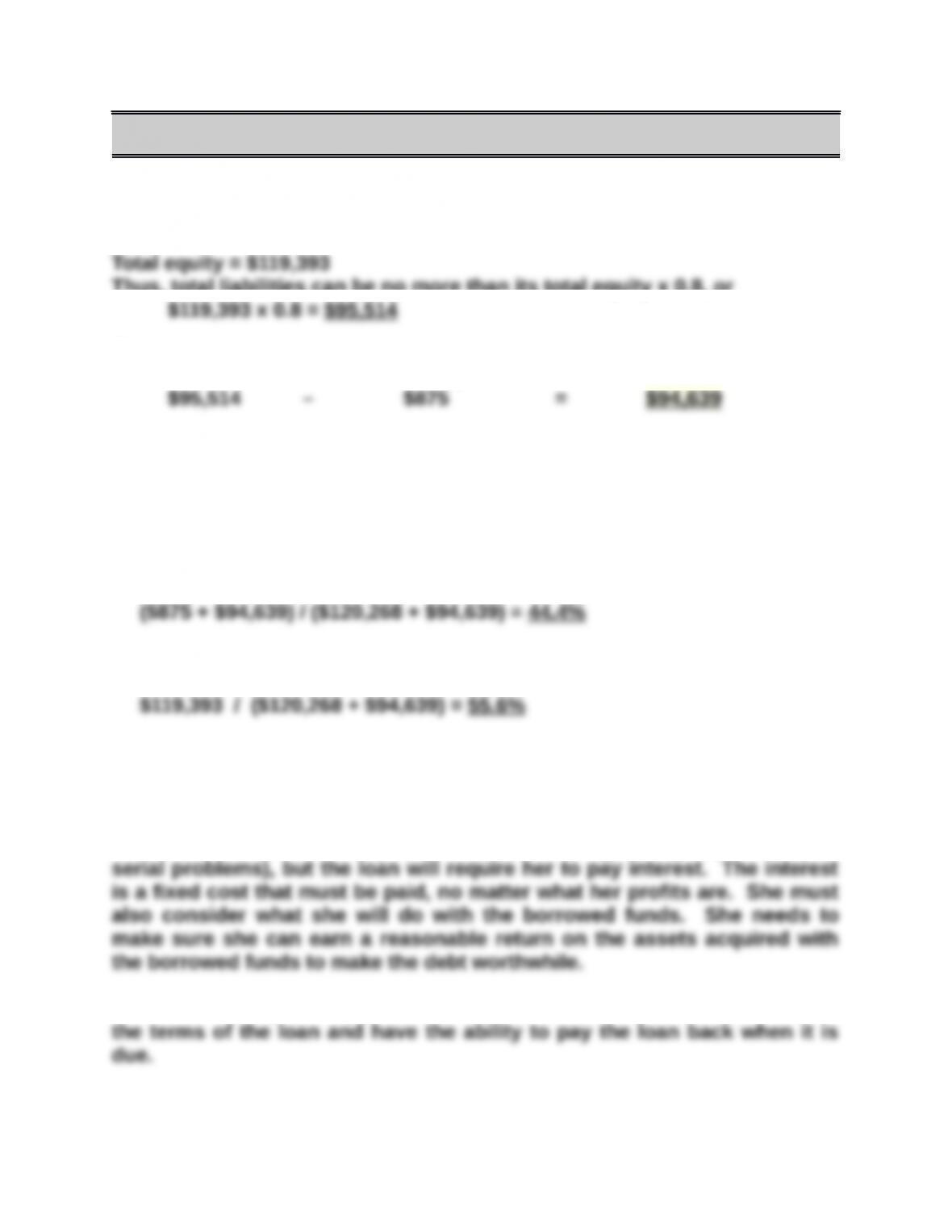

Thus, total liabilities can be no more than its total equity x 0.8, or

This implies that:

Max. total liabilities – Present liability balance = Max. that can be borrowed

Part 2

Assume the secured loan is taken, then the percent of assets financed by:

a. Debt

b. Equity

Part 3

Santana Rey should understand the risks she is taking by borrowing funds

from the bank. She currently has no interest-bearing debt (per prior chapter

In addition, and probably more important, Santana Rey should understand

Reporting in Action — BTN 14-1

1. Apple reported long-term debt of $16,960 million as of September 28,

2013.

2. The interest that Apple must pay on $100 million of 4.25% convertible

3. Assuming that Apple had $100 million carrying value of convertible

Instructor note: Apple’s stock is no par stock and therefore there is no

entry required to credit Paid-in-Capital in Excess of Par Value upon

conversion.

4. Answer depends on the financial statement information obtained.

Comparative Analysis — BTN 14-2

1. Apple’s current year debt-to-equity ratio = $83,451 / $123,549 = 0.68

2. For both years, Apple’s debt-to-equity ratio is above that of the industry

average of 0.44. This implies that its debt levels are more risky than that