Problem 14-3B (40 minutes)

Part 1

2015

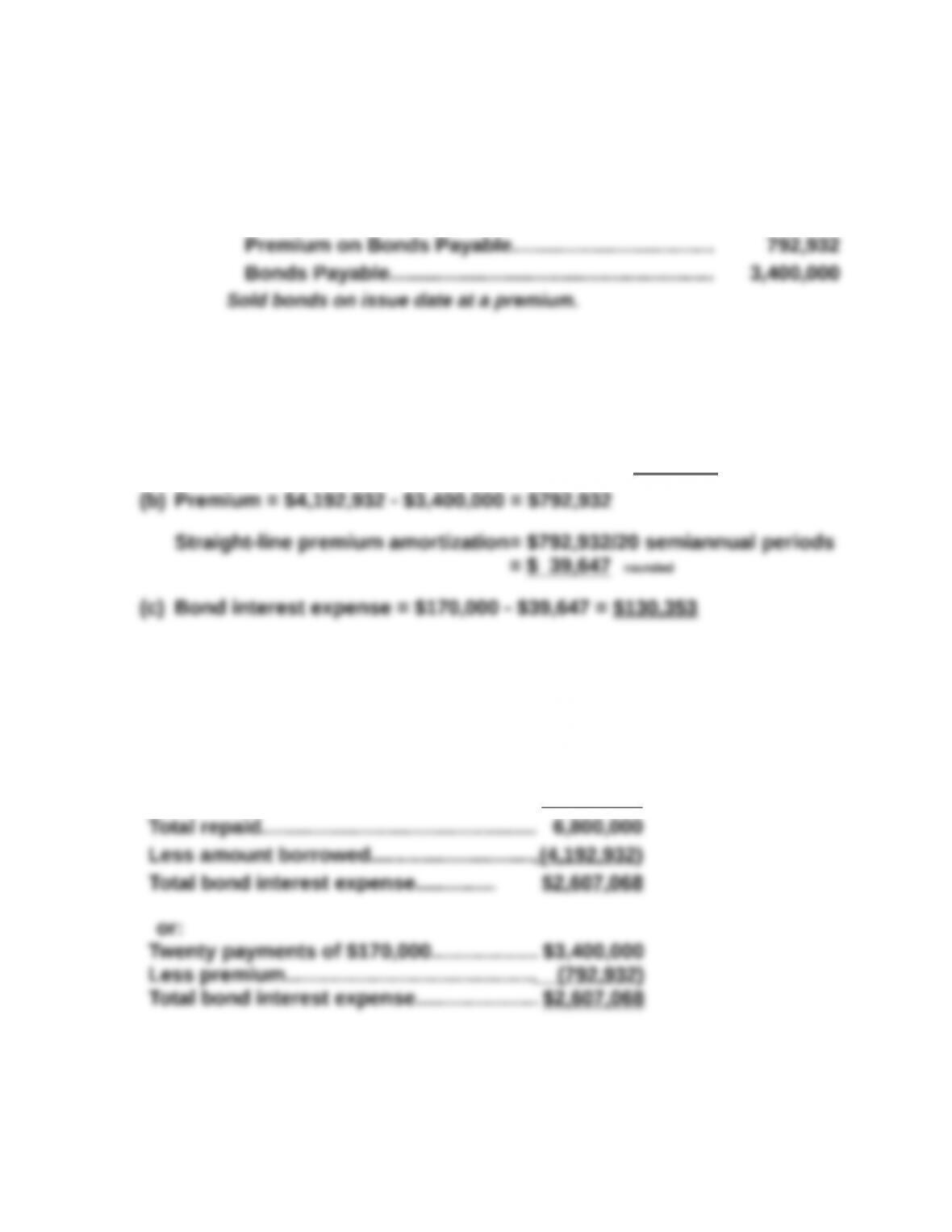

Jan. 1 Cash……………………………………………………………………4,192,932

Part 2

(a) Cash Payment = $3,400,000 x 10% x 6/12 year = $170,000

Part 3

Twenty payments of $170,000……………… $3,400,000

Par value at maturity…………………………… 3,400,000

Problem 14-3B (Concluded)

Part 4

Semiannual

Period-End

Unamortized

Premium

Carrying

Value

1/01/2015………………… $792,932 $4,192,932

Part 5

2015

June 30 Bond Interest Expense………………………………………….130,353

2015

Dec. 31 Bond Interest Expense………………………………………….130,353

Problem 14-4B (45 minutes)

Part 1

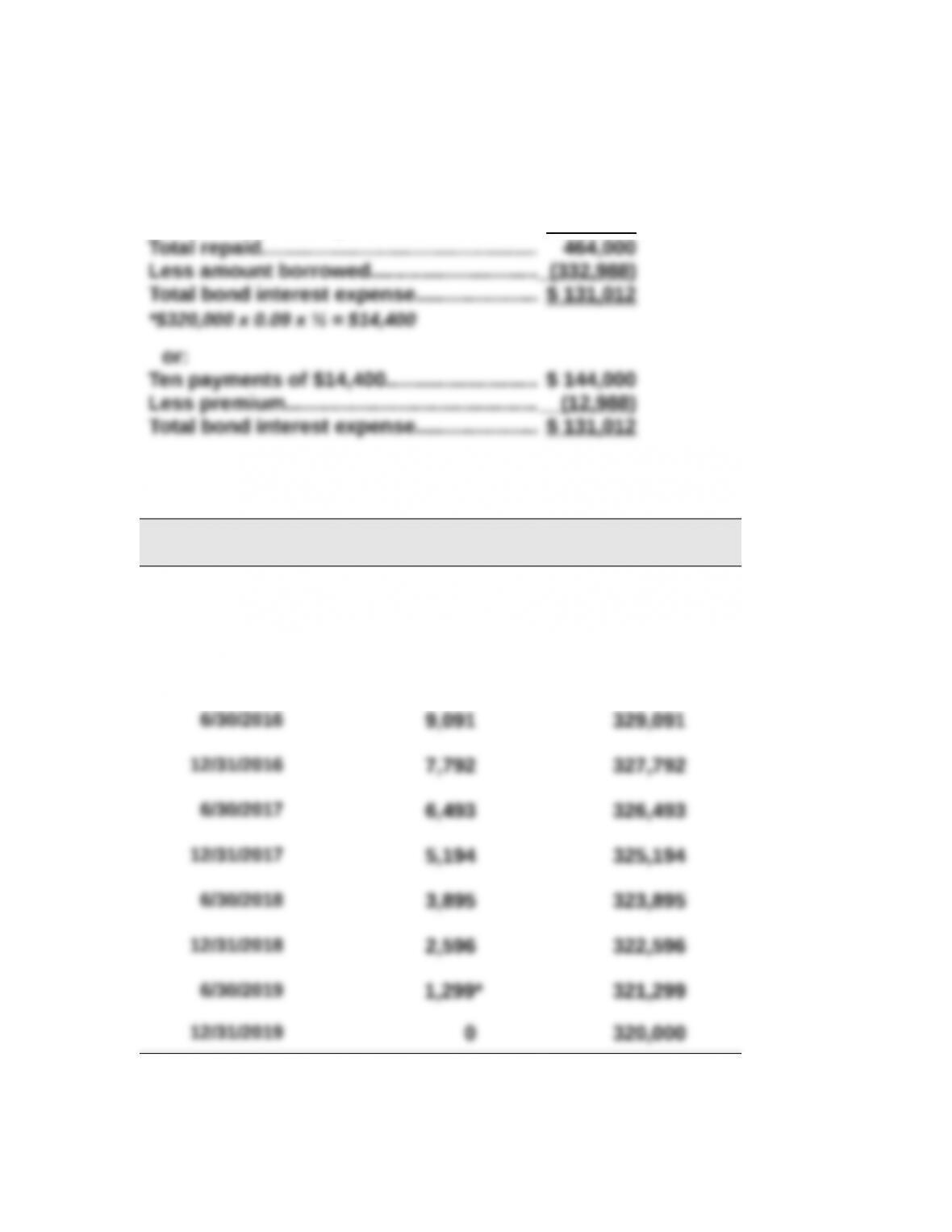

Ten payments of $14,400*……………………. $ 144,000

Par value at maturity…………………………… 320 ,000

Part 2

Straight-line amortization table ($12,988/10 = $1,299**)

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2015 $12,988 $332,988

6/30/2015 11,689 331,689

12/31/2015 10,390 330,390

* Adjusted for rounding.

**Rounded to nearest dollar.

Problem 14-4B (Concluded)

Part 3

2015

June 30 Bond Interest Expense………………………………………….13,101

2015

Dec. 31 Bond Interest Expense………………………………………….13,101

Problem 14-5B (60 minutes)

Part 1

2015

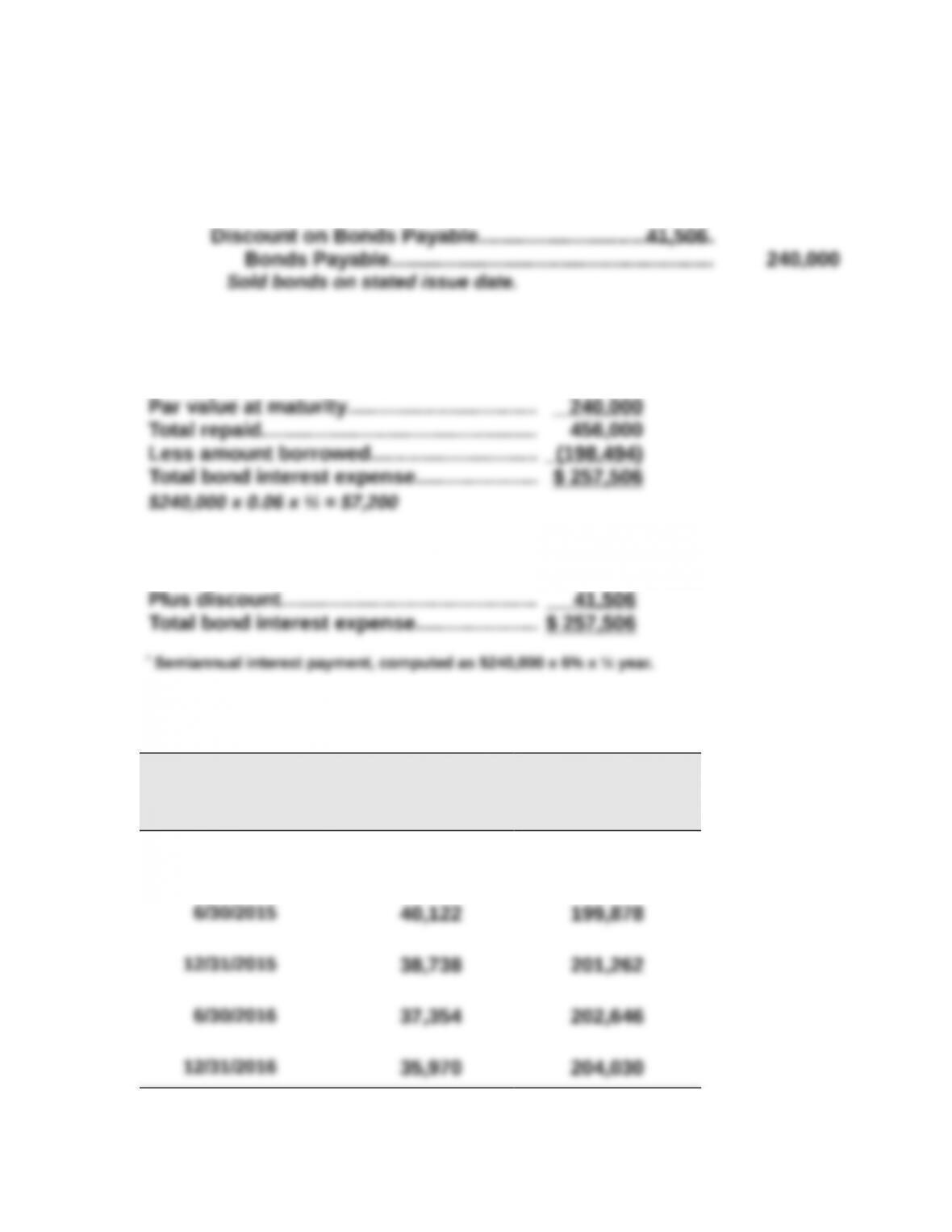

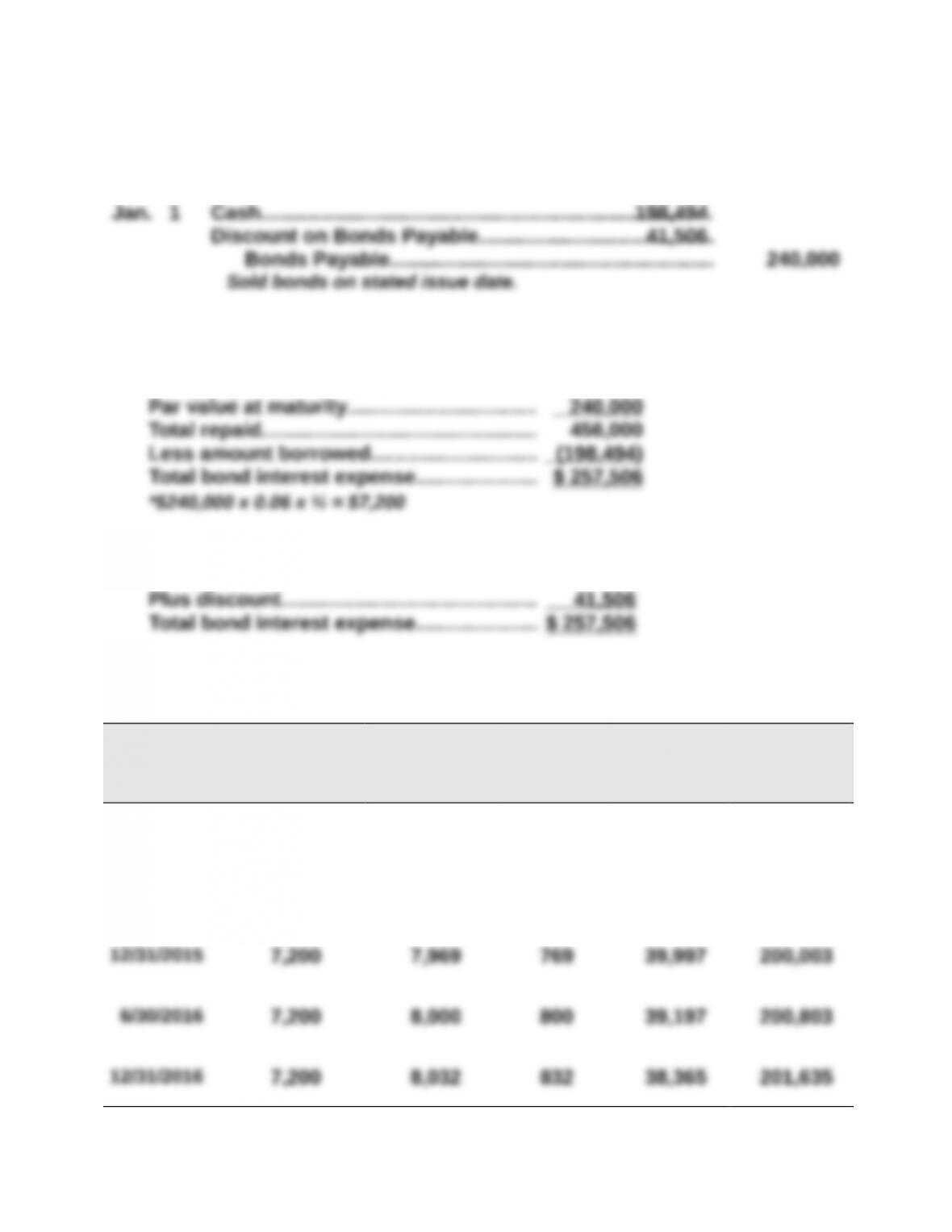

Jan. 1 Cash……………………………………………………………………198,494

Part 2

Thirty payments of $7,200*………………….. $ 216,000

or:

Thirty payments of $7,200*………………….. $ 216,000

Part 3 Straight-line amortization table ($41,506/30= $1,384)

Semiannual

Interest Period-End

Unamortized

Discount

Carrying

Value

1/01/2015 $41,506 $ 198,494

Problem 14-5B (Concluded)

Part 4

2015

June 30 Bond Interest Expense………………………………………….8,584

2015

Dec. 31 Bond Interest Expense………………………………………….8,584

Problem 14-6B (45 minutes)

Part 1 Amount of Payment

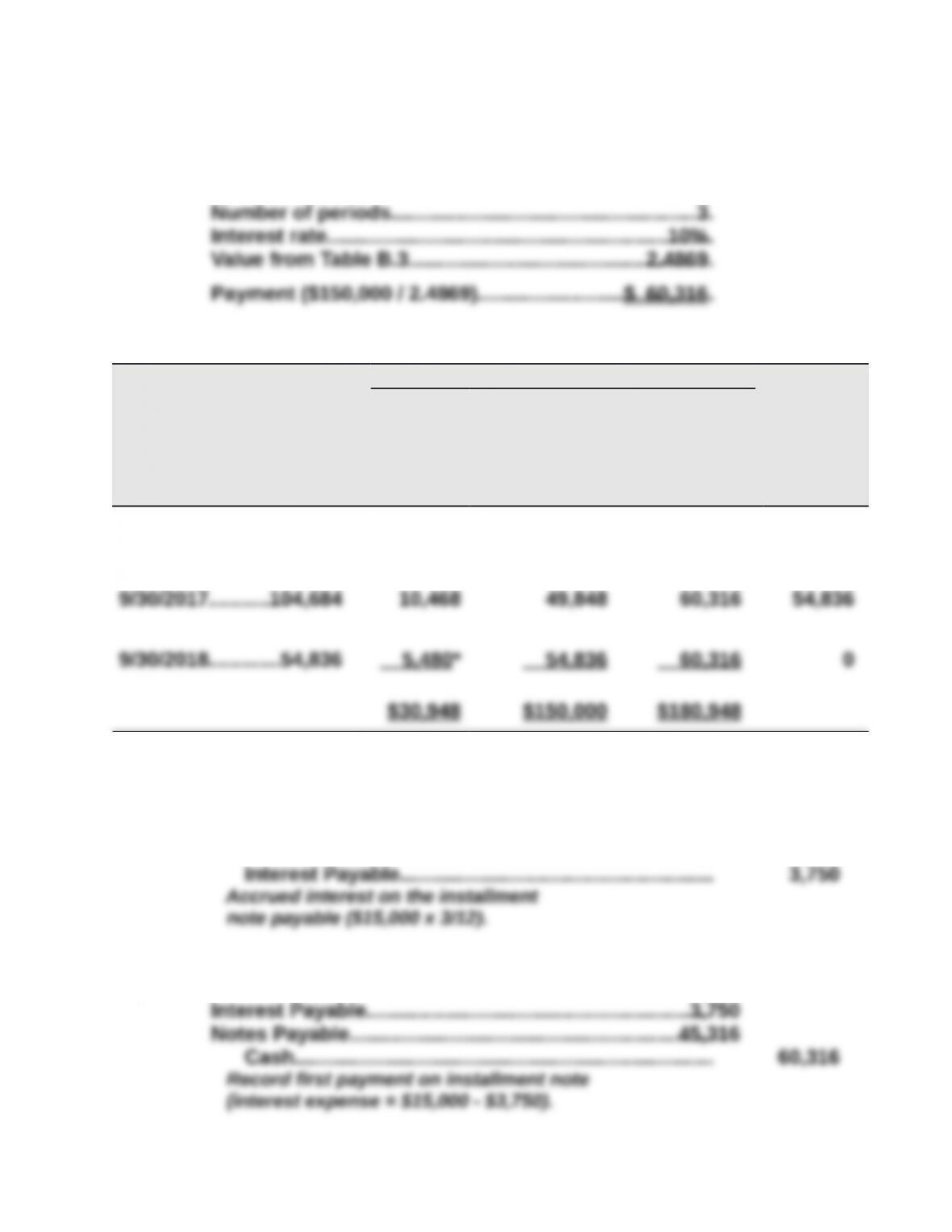

Note balance………………………………………………………..$150,000

Part 2

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[10% x (A)]

+

(C)

Debit

Notes

Payable

[(D) – (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

9/30/2016………….$150,000 $15,000 $ 45,316 $ 60,316 $104,684

*Adjusted for rounding.

Part 3

2015

Dec. 31 Interest Expense…………………………………………………..3,750

2016

Sept. 30 Interest Expense…………………………………………………..11,250

Problem 14-7B (30 minutes)

Part 1

Atlas Company

Bryan Company

Part 2

Bryan’s debt-to-equity ratio is much higher than that for Atlas. This implies

Problem 14-8BB (60 minutes)

Part 1

2015

Part 2

Thirty payments of $7,200*………………….. $ 216,000

or:

Thirty payments of $7,200…………………… $ 216,000

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[3% x $240,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Discount

Amortization

[(B) – (A)]

(D)

Unamortized

Discount

[Prior (D) – (C)]

(E)

Carrying

Value

[$240,000 – (D)]

1/01/2015 $41,506 $198,494

6/30/2015 $7,200 $7,940 $740 40,766 199,234

Problem 14-8BB (Concluded)

Part 4

2015

June 30 Bond Interest Expense………………………………………….7,940

2015

Dec. 31 Bond Interest Expense………………………………………….7,969