Problem 14-8AB (Concluded)

Part 4

2015

June 30 Bond Interest Expense………………………………………….11,687

2015

Dec. 31 Bond Interest Expense………………………………………….11,830

Problem 14-9AB (45 minutes)

Part 1

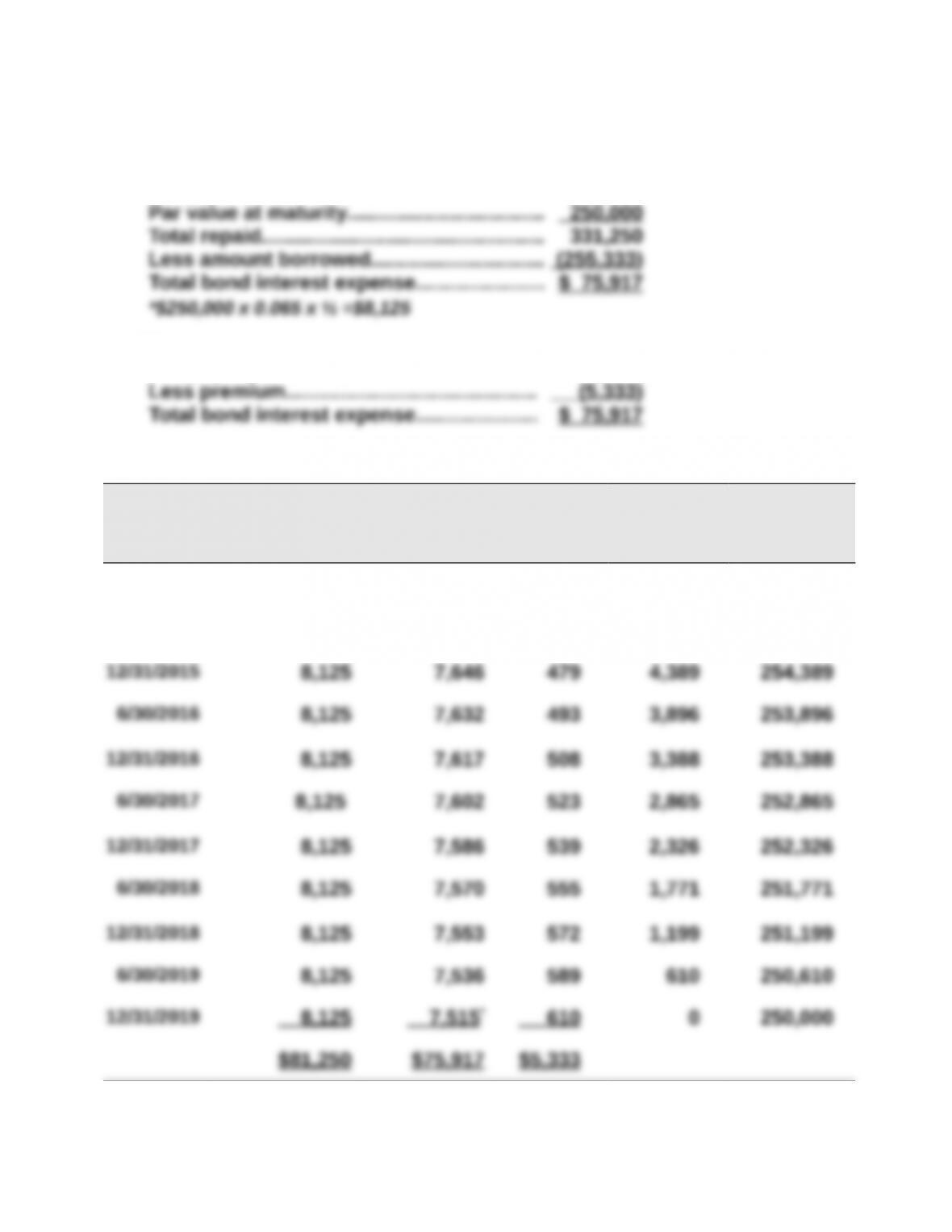

Ten payments of $8,125* ……………………… $ 81,250

or:

Ten payments of $8,125………………………. $ 81,250

Part 2

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[3.25% x $250,000]

(B)

Bond Interest

Expense

[3% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$250,000 + (D)]

1/01/2015 $5,333 $255,333

6/30/2015 $ 8,125 $ 7,660 $ 465 4,868 254,868

*Adjusted for rounding.

Problem 14-9AB (Concluded)

Part 3

2015

June 30 Bond Interest Expense………………………………………….7,660

2015

Dec. 31 Bond Interest Expense………………………………………….7,646

Part 4

As of December 31, 2017

Cash Flow Table Table Value* Amount Present Value

Par value…………………. B.1 0.8885 $250,000 $222,125

* Table values are based on a discount rate of 3% (half the annual original market

rate) and 4 periods (semiannual payments).

Comparison to Part 2 Table

This present value ($252,326) equals the carrying value of the bonds in

Problem 14-10AB (60 minutes)

Part 1

2015

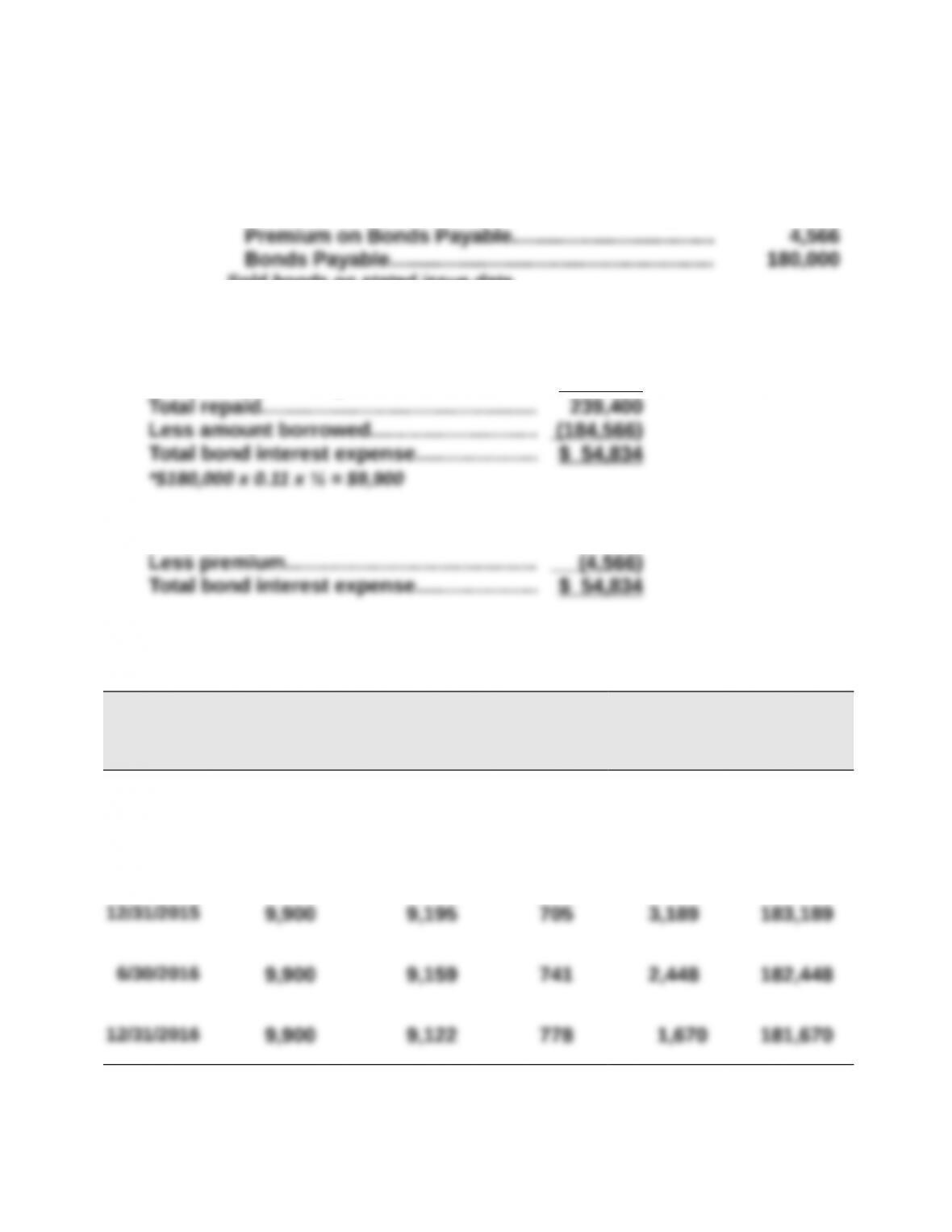

Jan. 1 Cash……………………………………………………………………184,566

Sold bonds on stated issue date.

Part 2

Six payments of $9,900 ………………………. $ 59,400

Par value at maturity…………………………… 180,000

or:

Six payments of $9,900……………………….. $ 59,400

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[5.5% x $180,000]

(B)

Bond Interest

Expense

[5% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$180,000 + (D)]

1/01/2015 $4,566 $184,566

6/30/2015 $9,900 $9,228 $672 3,894 183,894

Problem 14-10AB (Concluded)

Part 4

2015

June 30 Bond Interest Expense………………………………………….9,228

2015

Dec. 31 Bond Interest Expense………………………………………….9,195

Part 5

2017

Jan. 1 Bonds Payable …………………………………………………….180,000

Part 6

If the market rate on the issue date had been 12% instead of 10%, the bonds

This change would affect the balance sheet because the bond liability would be

The income statement would show larger amounts of bond interest expense over

The statement of cash flows would show a smaller amount of cash received from

borrowing. However, the cash flow statements presented over the life of the

Problem 14-11AD (35 minutes)

Part 1

Present Value of the Lease Payments

Part 2

Part 3

Capital Lease Liability Payment (Amortization) Schedule

Period

Endin

g

Date

Beginning

Balance of

Lease

Liability

Interest on

Lease

Liability

(8%)

Reduction

of Lease

Liability

Cash

Lease

Payment

Ending

Balance of

Lease

Liability

Year 1 $39,927 $ 3,194* $ 6,806 $ 10,000 $33,121

* Rounded to nearest dollar.

** Difference due to rounding.

Part 4

Depreciation Expense—Leased Asset, Off. Equip……………….7,985

PROBLEM SET B

Problem 14-1B (50 minutes)

Part 1

a.

Cash Flow Table Table Value* Amount Present Value

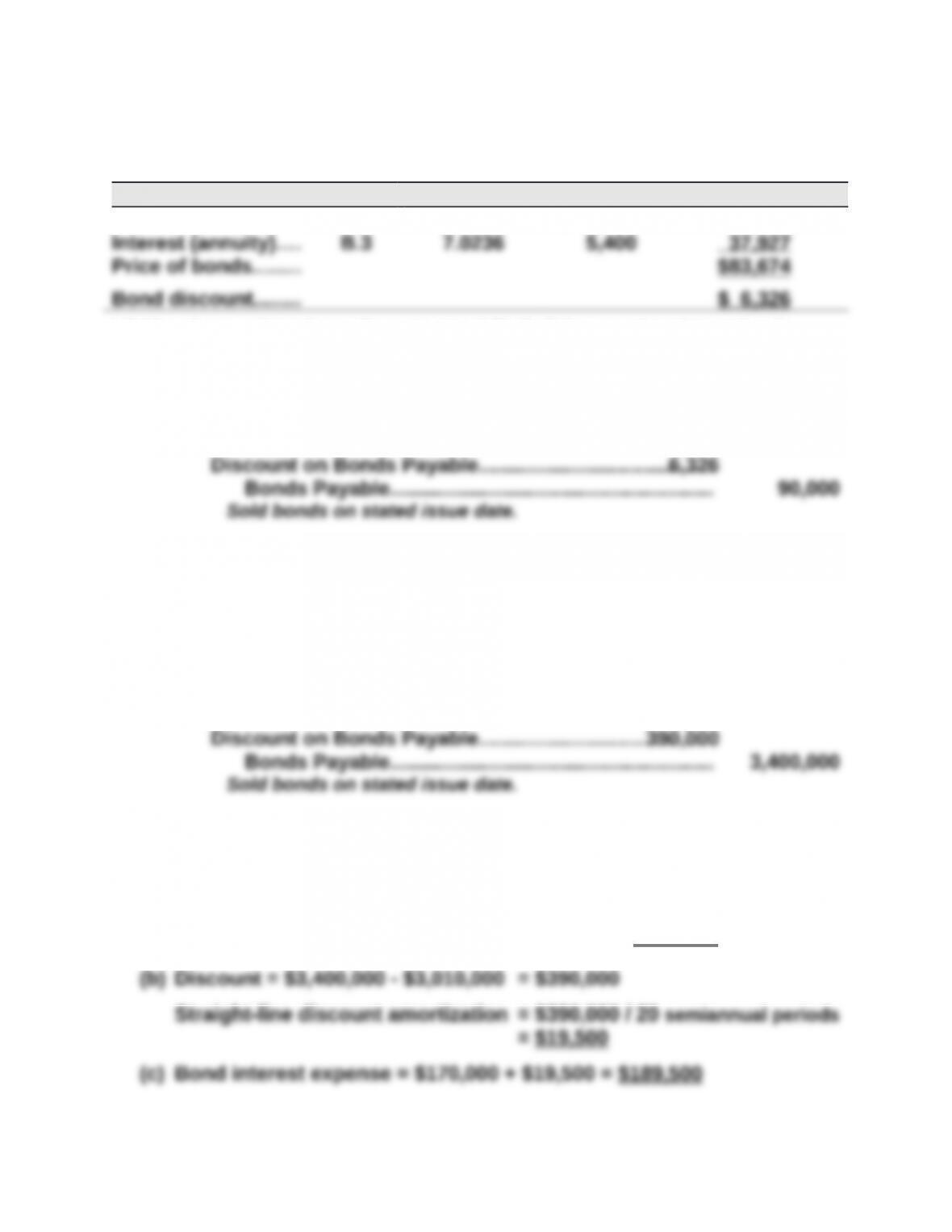

Par value…………….. B.1 0.6139 $90,000 $55,251

* Table values are based on a discount rate of 5% (half the annual market rate) and 10

periods (semiannual payments).

b.

2015

Jan. 1 Cash……………………………………………………………………96,948

Part 2

a.

Cash Flow Table Table Value* Amount Present Value

Par value…………….. B.1 0.5584 $90,000 $50,256

* Table values are based on a discount rate of 6% (half the annual market rate) and

10 periods (semiannual payments). (Note: When the contract rate and market

rate are the same, the bonds sell at par and there is no discount or premium.)

**Difference due to rounding

b.

2015

Jan. 1 Cash……………………………………………………………………90,000

* Table values are based on a discount rate of 7% (half the annual market rate) and

10 periods (semiannual payments).

b.

2015

Jan. 1 Cash……………………………………………………………………83,674

Problem 14-2B (40 minutes)

Part 1

2015

Jan. 1 Cash……………………………………………………………………3,010,000

Part 2

[Note: The semiannual amounts for (a), (b), and (c) below are the same throughout

the bonds’ life because the company uses straight-line amortization.]

(a) Cash Payment = $3,400,000 x 10% x 6/12 year = $170,000

Problem 14-2B (Concluded)

Part 3

Twenty payments of $170,000……………… $3,400,000

Par value at maturity…………………………… 3,400,000

or:

Part 4 (Semiannual amortization: $390,000/20 = $19,500)

Semiannual

Period-End

Unamortized

Discount

Carrying

Value

1/01/2015………………… $390,000 $3,010,000

Part 5

2015

June 30 Bond Interest Expense………………………………………….189,500

2015

Dec. 31 Bond Interest Expense………………………………………….189,500

discount amortization.