Problem 14-2A (40 minutes)

Part 1

2015

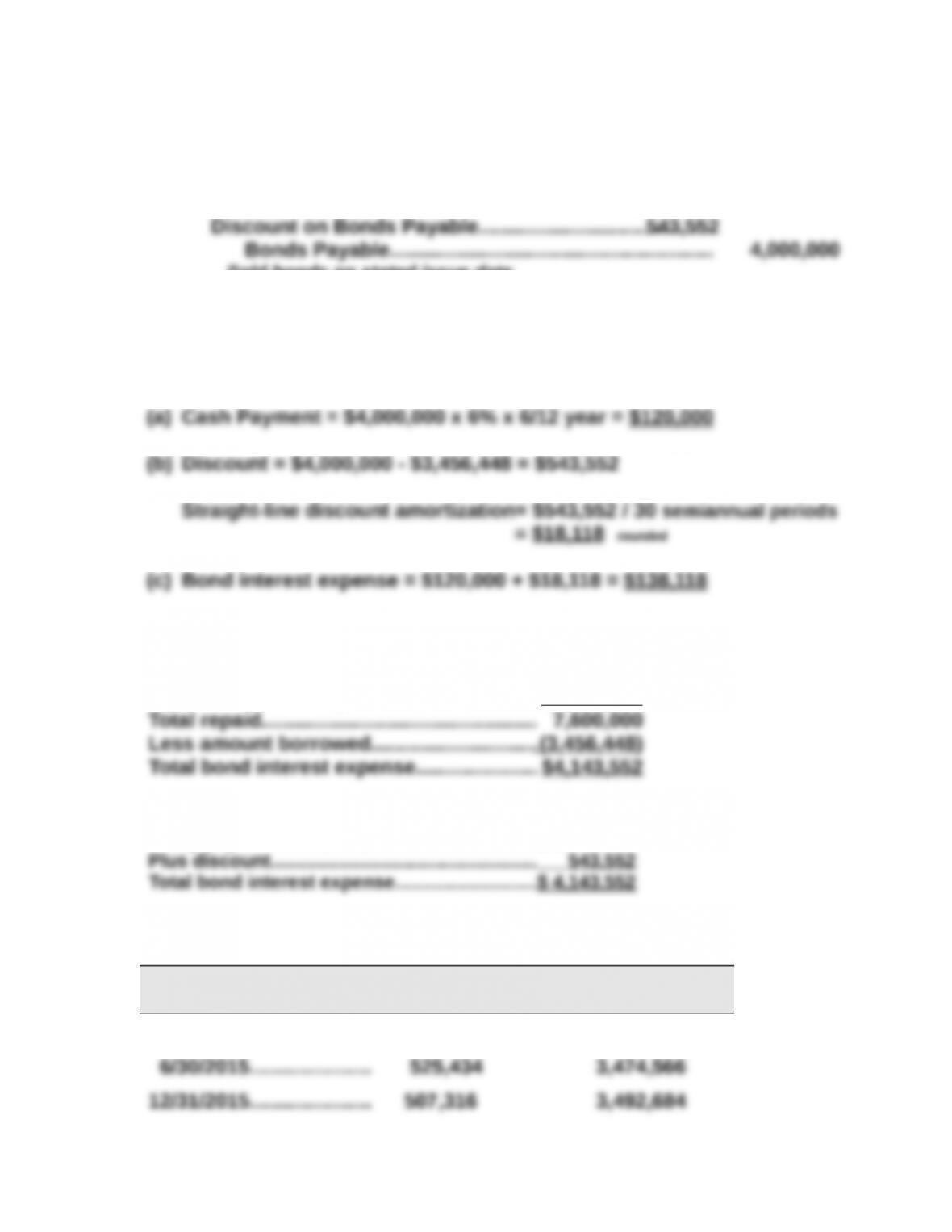

Jan. 1 Cash……………………………………………………………………3,456,448

Sold bonds on stated issue date.

Part 2

[Note: The semiannual amounts for (a), (b), and (c) below are the same throughout the bonds’

life because this company uses straight-line amortization.]

Part 3

Thirty payments of $120,000 ………………. $3,600,000

Par value at maturity…………………………… 4,000,000

or:

Thirty payments of $120,000……………………..$ 3,600,000

Part 4 (Semiannual amortization: $543,552/30 = $18,118.4)

Semiannual

Period-End

Unamortized

Discount

Carrying

Value

1/01/2015………………… $543,552 $3,456,448

Problem 14-2A (Concluded)

Part 5

2015

June 30 Bond Interest Expense………………………………………….138,118

2015

Dec. 31 Bond Interest Expense………………………………………….138,118

Problem 14-3A (40 minutes)

Part 1

2015

Jan. 1 Cash……………………………………………………………………4,895,980

Part 2

(a) Cash Payment = $4,000,000 x 6% x 6/12 = $120,000

Part 3

Thirty payments of $120,000 ………………. $3,600,000

or:

Problem 14-3A (Concluded)

Part 4

Semiannual

Period-End

Unamortized

Premium

Carrying

Value

1/01/2015………………… $895,980 $4,895,980

6/30/2015………………… 866,114 4,866,114

Part 5

2015

June 30 Bond Interest Expense………………………………………….90,134

2015

Dec. 31 Bond Interest Expense………………………………………….90,134

Premium on Bonds Payable…………………………………..29,866

Problem 14-4A (45 minutes)

Part 1

Ten payments of $8,125* …………………….. $ 81,250

Par value at maturity…………………………… 250,000

or:

Ten payments of $8,125………………………. $ 81,250

Part 2

Straight-line amortization table ($5,333/10 = $533*)

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2015 $5,333 $255,333

6/30/2015 4,800 254,800

* Rounded to nearest dollar. ** Adjusted for rounding.

Problem 14-4A (Concluded)

Part 3

2015

June 30 Bond Interest Expense………………………………………….7,592

2015

Dec. 31 Bond Interest Expense………………………………………….7,592

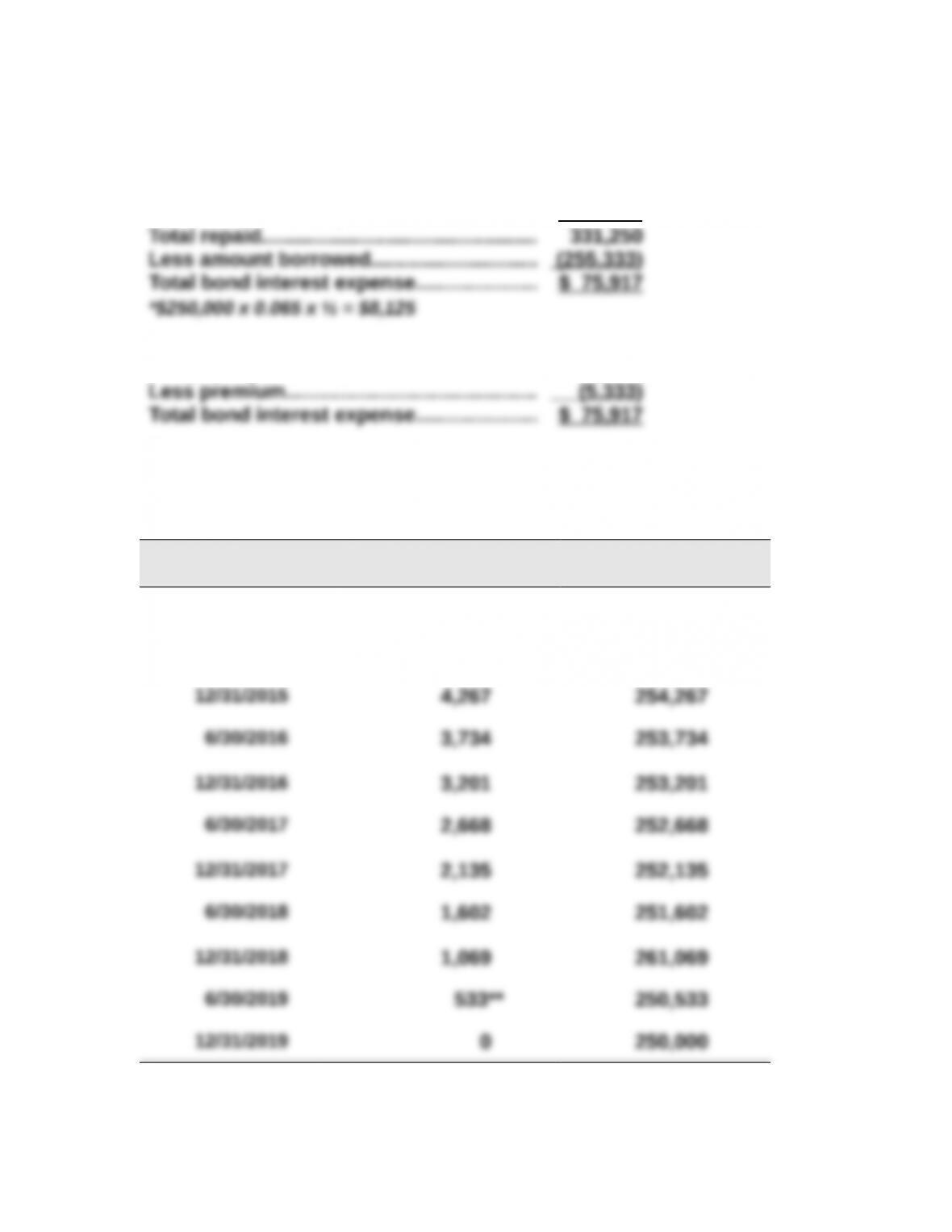

Problem 14-5A (60 minutes)

Part 1

2015

Jan. 1 Cash……………………………………………………………………292,181

Part 2

Eight payments of $8,125* ……………… $ 65,000

Par value at maturity………………………. 325,000

or:

Eight payments of $8,125……………….. $ 65,000

Semiannual

Interest Period-End

Unamortized

Discount

Carrying

Value

1/01/2015 $32,819 $292,181

6/30/2015 28,717 296,283

*(rounded to nearest dollar)

Problem 14-5A (Concluded)

Part 4

2015

June 30 Bond Interest Expense………………………………………….12,227

2015

Dec. 31 Bond Interest Expense………………………………………….12,227

Part 5

If the market interest rate on the issue date had been 4% instead of 8%, the

This change would affect the balance sheet because the bond liability

would be larger (par value plus a premium instead of par value minus a

The income statement would show smaller amounts of bond interest

expense over the life of the bonds discount.

The statement of cash flows would show a larger amount of cash received

Problem 14-6A (45 minutes)

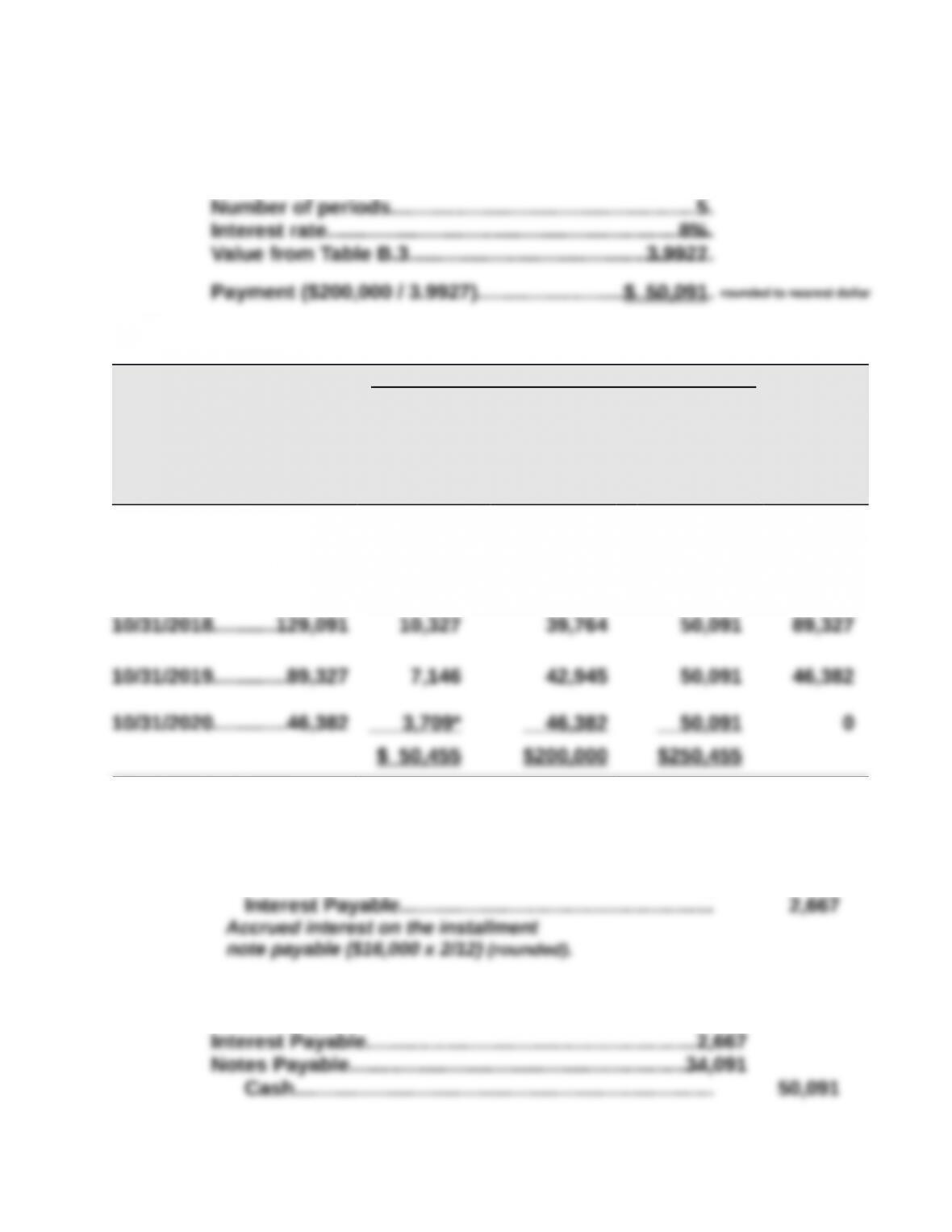

Part 1 Amount of Payment

Note balance………………………………………………………..$200,000

Part 2

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[8% x (A)]

+

(C)

Debit

Notes

Payable

[(D) – (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

10/31/2016………….$200,000 $ 16,000 $ 34,091 $ 50,091 $165,909

10/31/2017………….165,909 13,273 36,818 50,091 129,091

* Adjusted for rounding

Part 3

2015

Dec. 31 Interest Expense…………………………………………………..2,667

2016

Oct. 31 Interest Expense…………………………………………………..13,333

Record first payment on installment note

Problem 14-7A (20 minutes)

Part 1

Part 2

Scott’s debt-to-equity ratio is higher than Pulaski’s. This implies that Scott

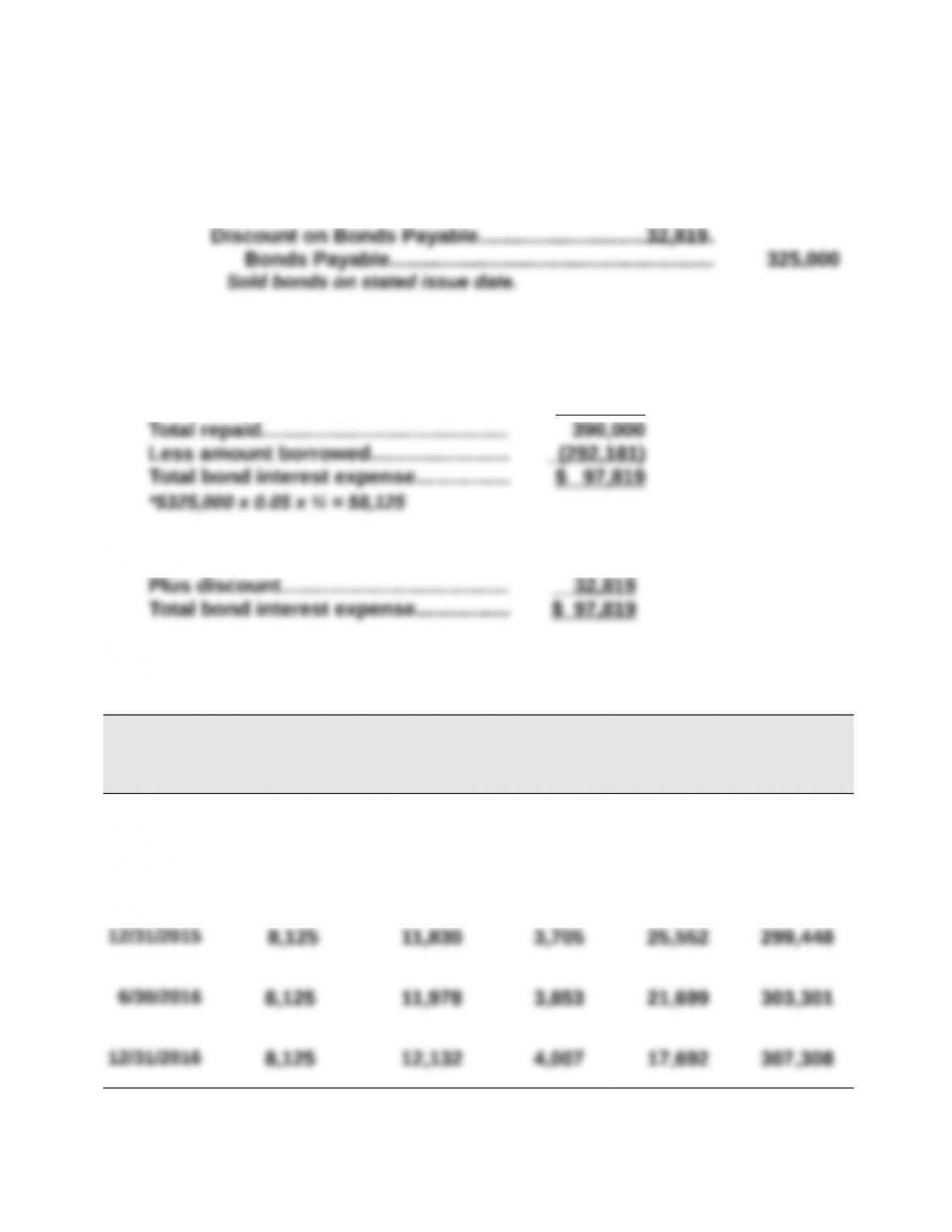

Problem 14-8AB (60 minutes)

Part 1

2015

Jan. 1 Cash……………………………………………………………………292,181

Part 2

Eight payments of $8,125* ……………… $ 65,000

Par value at maturity………………………. 325,000

or:

Eight payments of $8,125……………….. $ 65,000

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[2.5% x $325,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Discount

Amortization

[(B) – (A)]

(D)

Unamortized

Discount

[Prior (D) – (C)]

(E)

Carrying

Value

[$325,000 – (D)]

1/01/2015 $32,819 $292,181

6/30/2015 $8,125 $11,687 $3,562 29,257 295,743