Exercise 14-11 (20 minutes)

2015

Jan. 1 Cash……………………………………………………………………100,000

2015

Dec. 31 Interest Expense…………………………………………………..7,000

2016

Dec. 31 Interest Expense…………………………………………………..5,423

2017

Dec. 31 Interest Expense…………………………………………………..3,736

2018

Dec. 31 Interest Expense…………………………………………………..1,933

Exercise 14-12 (15 minutes)

2. Montclair’s risk will increase because it will have more debt. That debt

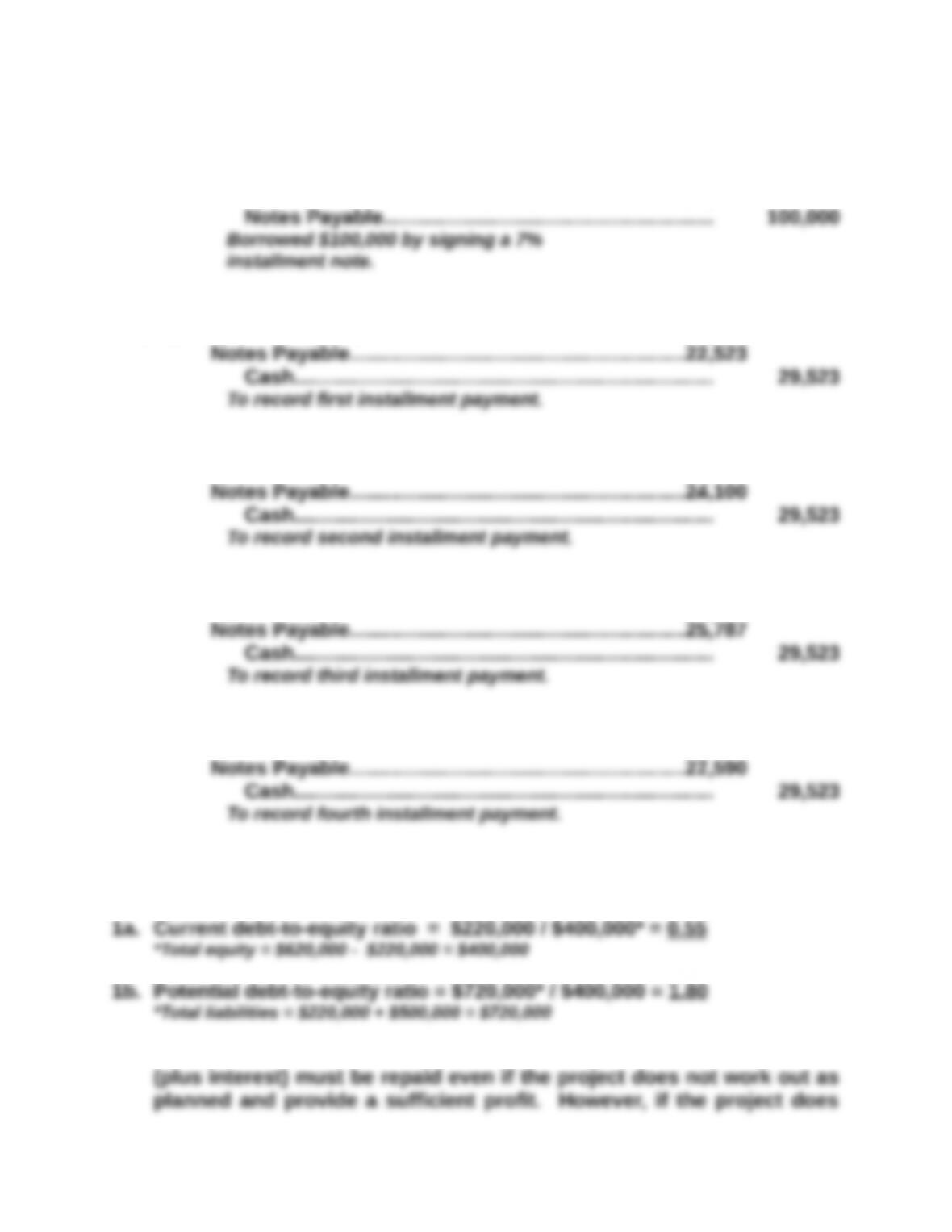

Exercise 14-13B (30 minutes)

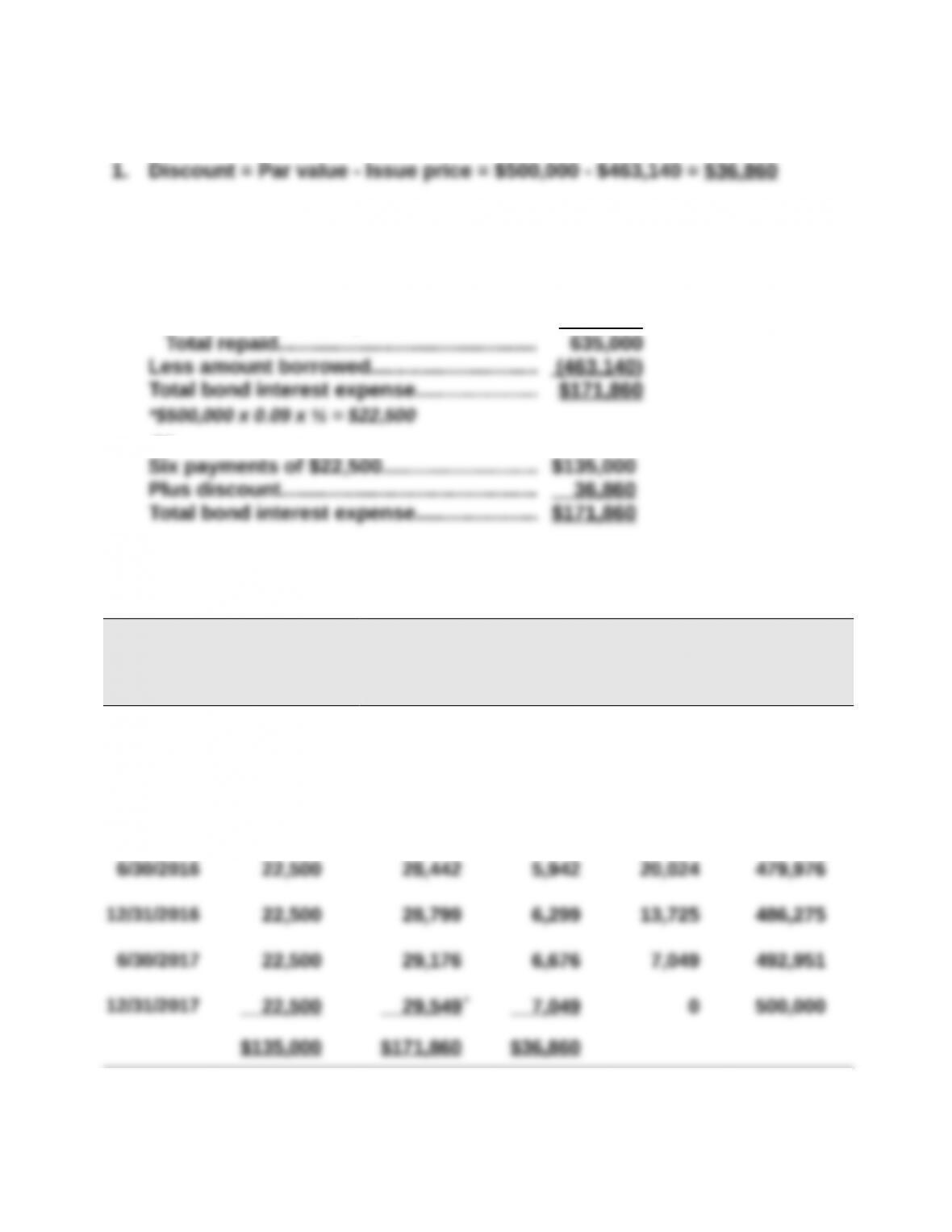

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $22,500*…………………. $135,000

Par value at maturity………………………… 500,000

or

3. Effective interest amortization table

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[4.5% x $500,000]

(B)

Bond Interest

Expense

[6% x Prior (E)]

(C)

Discount

Amortization

[(B) – (A)]

(D)

Unamortized

Discount

[Prior (D) – (C)]

(E)

Carrying

Value

[$500,000 – (D)]

1/01/2015 $36,860 $463,140

6/30/2015 $ 22,500 $ 27,788 $ 5,288 31,572 468,428

12/31/2015 22,500 28,106 5,606 25,966 474,034

*Adjusted for rounding.

Exercise 14-14B (30 minutes)

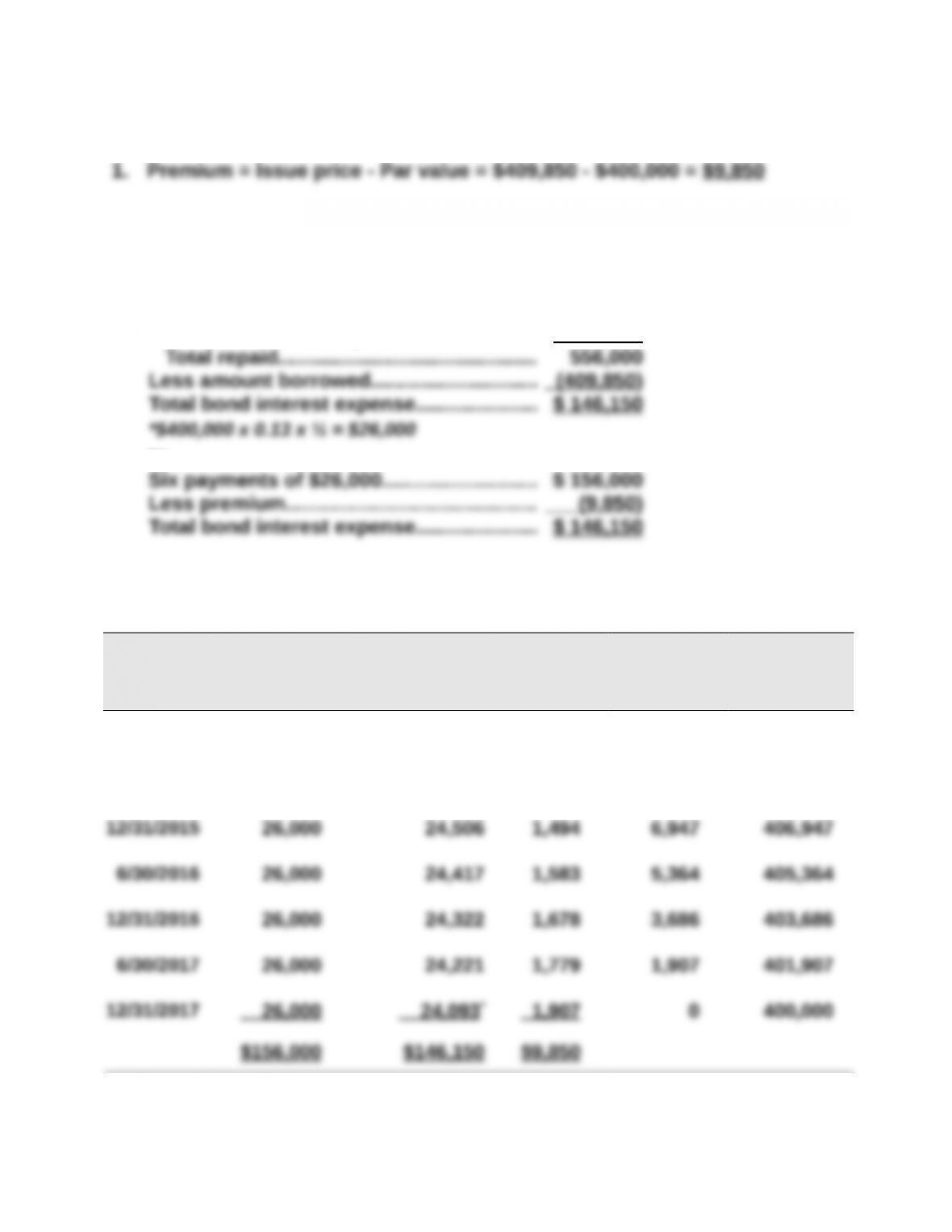

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $26,000*…………………. $ 156,000

Par value at maturity………………………… 400,000

or

3. Effective interest amortization table

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[6.5% x $400,000]

(B)

Bond Interest

Expense

[6% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[400,000 + (D)]

1/01/2015 $9,850 $409,850

6/30/2015 $ 26,000 $ 24,591 $1,409 8,441 408,441

*Adjusted for rounding.

Exercise 14-15 (40 minutes)

1. Straight-line amortization table (($100,000-$95,948)/8 = $506.5)

Semiannual

Period-End

Unamortized

Discount †

Carrying

Value

6/01/2015………………… $4,052 $95,948

11/30/2015………………… 3,546 96,454

* Adjusted for rounding difference.

† Supporting computations

Eight payments of $3,500**………………… $ 28,000

Par value at maturity………………………….. 100,000

or

Exercise 14-15 (Concluded)

2.

2015

Nov. 30 Bond Interest Expense………………………………………….4,006

Dec. 31 Bond Interest Expense…………………………………………. 668

2016

May 31 Interest Payable…………………………………………………… 584

Exercise 14-16C (20 minutes)

2. Journal entries

2015

May 1 Cash……………………………………………………………………3,502,000

June 30 Interest Payable……………………………………………………102,000

Dec. 31 Bond Interest Expense………………………………………….153,000

Exercise 14-17D (10 minutes)

1. Operating 2. Capital 3. Capital

Exercise 14-18D (20 minutes)

1. Leased Asset—Office Equipment………………………………………41,000

2. Depreciation Expense—Leased Asset, Office Equip……………8,200

Exercise 14-19D (15 minutes)

Analysis: Option 2 has the lowest present value at $38,035 and, thus, is the

best lease deal for the customer.

Exercise 14-20 (20 minutes)

(amounts in euros millions)

1. Cash…………………………………………………………………… 1,663

2. Loans and Borrowings…………………………………………. 2,400

3. Heineken’s Loans and Borrowings carried a premium of €112 as of

4. The contract rate was higher than the market rate at issuance. This is

PROBLEM SET A

Problem 14-1A (50 minutes)

Part 1

a.

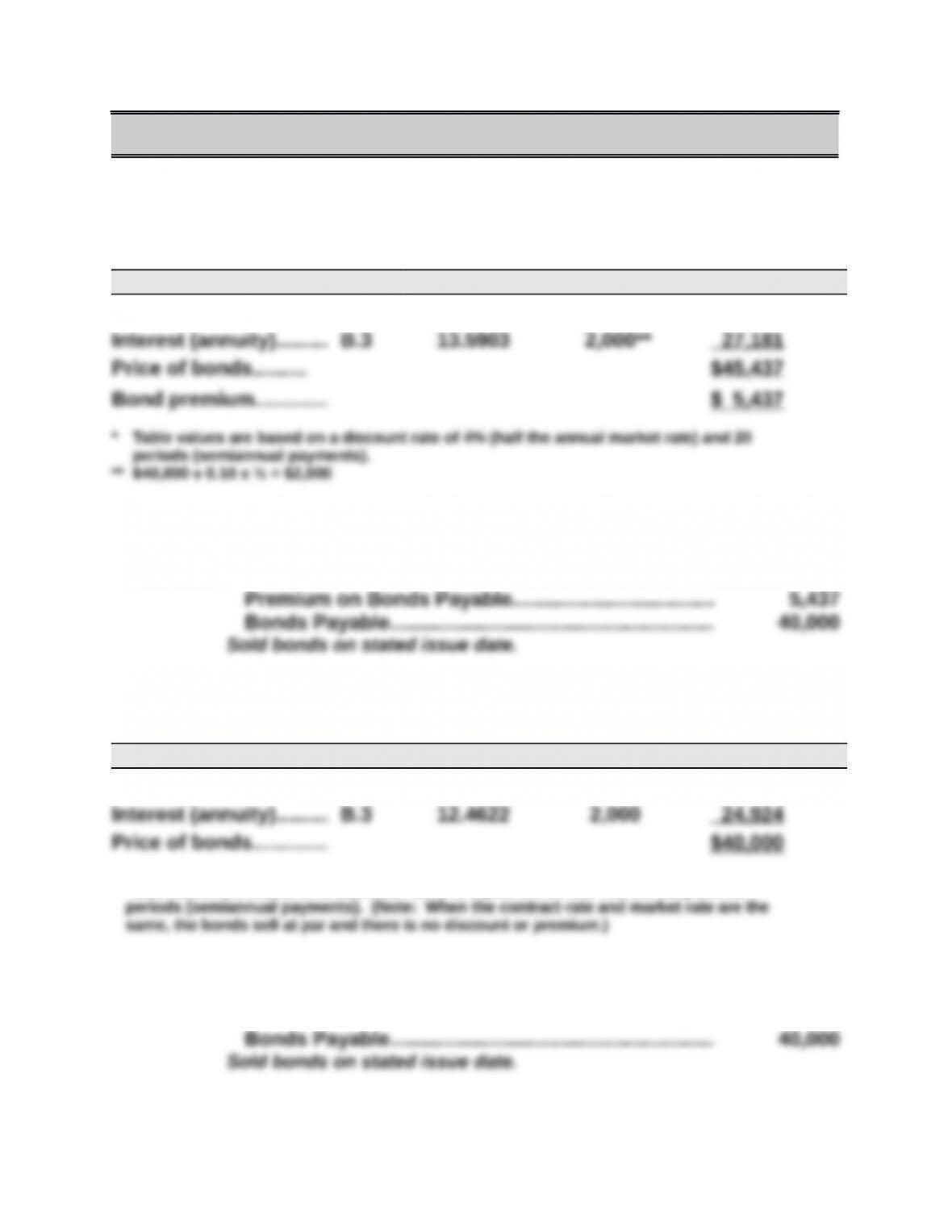

Cash Flow Table Table Value* Amount Present Value

Par value…………………. B.1 0.4564 $40,000 $18,256

b.

2015

Jan. 1 Cash……………………………………………………………………45,437

Part 2

a.

Cash Flow Table Table Value* Amount Present Value

Par value…………………. B.1 0.3769 $40,000 $15,076

* Table values are based on a discount rate of 5% (half the annual market rate) and 20

b.

2015

Jan. 1 Cash……………………………………………………………………40,000

Problem 14-1A (Concluded)

Part 3

a.

Cash Flow Table Table Value* Amount Present Value

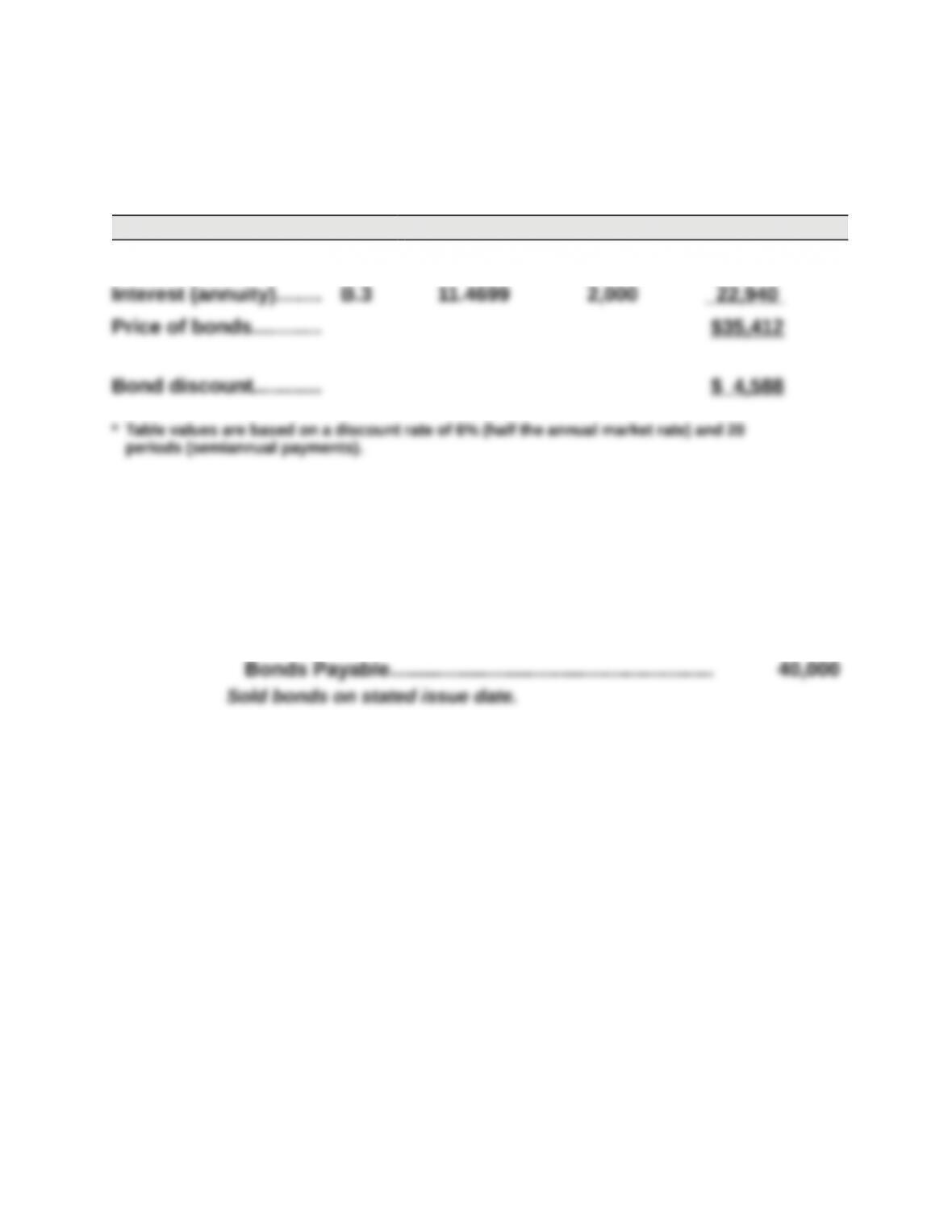

Par value……………….. B.1 0.3118 $40,000 $12,472

b.

2015

Jan. 1 Cash……………………………………………………………………35,412

Discount on Bonds Payable…………………………………..4,588