Chapter 14 – Long-Term Liabilities

Exercise 14-2 (30 minutes)

1. Discount = Par value – Issue price = $180,000 – $170,862 = $9,138

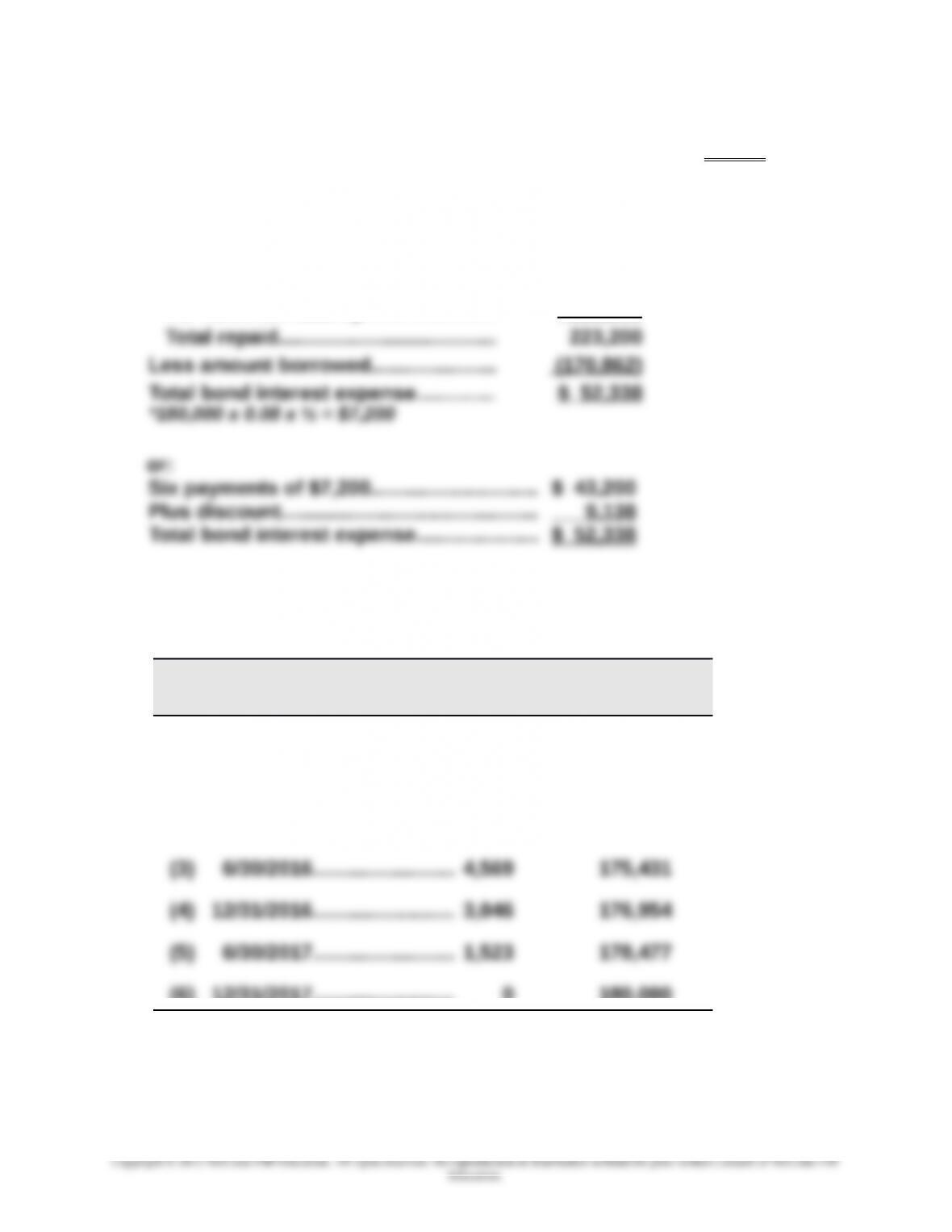

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $7,200*……………... $ 43,200

Par value at maturity………………..... 180,000

3. Straight-line amortization table ($9,138/6 = $1,523)

Semiannual

Period-End

Unamortized

Discount

Carrying

Value

(0) 1/01/2015………..…………..$9,138 $170,862

(1) 6/30/2015………..………….. 7,615 172,385

(2) 12/31/2015………….………… 6,092 173,908

(6) 12/31/2017………….………… 0 180,000

14-769

Chapter 14 – Long-Term Liabilities

Exercise 14-3 (25 minutes)

1. Semiannual cash interest payment = $800,000 x 6% x ½ year = $24,000

bonds are issued at a discount.

4. Estimation of the market price at the issue date

Cash Flow Table Table Value* Amount Present Value

* Table values are based on a discount rate of 4% (half the annual market rate) and

20 periods (semiannual payments).

5. Cash………………………………………………………………………691,287

Discount on Bonds Payable……………………………………108,713

2015

(a)

Dec. 31 Cash………………………………………………………………………186,534

2016

(b)

June 30 Bond Interest Expense…………………………………………..7,684

Discount on Bonds Payable**……………….………….. 1,684

14-770

14-771

Chapter 14 – Long-Term Liabilities

Exercise 14-5 (35 minutes)

2015

(a)

Dec. 31 Cash………………………………………………………………………188,000

2016

June 30 Bond Interest Expense…………………………………………..8,000

Discount on Bonds Payable*…..……………………….. 3,000

Cash**……………………………………………………..………. 5,000

Paid semiannual interest and record

amor-tization. *$12,000-$9,000 **$200,000x

5% x ½

Dec. 31 Bond Interest Expense………………….……………………….8,000

5% x ½

2017

June 30 Bond Interest Expense…………………………………………..8,000

Discount on Bonds Payable*…..……………………….. 3,000

Cash**……………………………………………………..………. 5,000

Paid semiannual interest and record

amor-tization. *$6,000-$3,000 **$200,000 x

5% x ½

Dec. 31 Bond Interest Expense………………….……………………….8,000

14-772

14-773

Chapter 14 – Long-Term Liabilities

Exercise 14-6 (20 minutes)

2014

(a)

Dec. 31 Cash………………………………………………………………………216,222

2015

(b)

June 30 Bond Interest Expense…………………………………………..8,378

Premium on Bonds Payable*………..………………………..1,622

Cash**……………………………………………………..………. 10,000

1. Premium = Issue price – Par value = $409,850 – $400,000 = $9,850

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $26,000*……………. $156,000

Par value at maturity………………..... 400,000

Total repaid………………………………… 556,000

3. Straight-line amortization table ($9,850/6 = $1,642)

14-774

Chapter 14 – Long-Term Liabilities

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2015 $9,850 $409,850

6/30/2015 8,208 408,208

12/31/2017 0 400,000

*Adjusted for rounding.

14-775

Chapter 14 – Long-Term Liabilities

Exercise 14-8 (25 minutes)

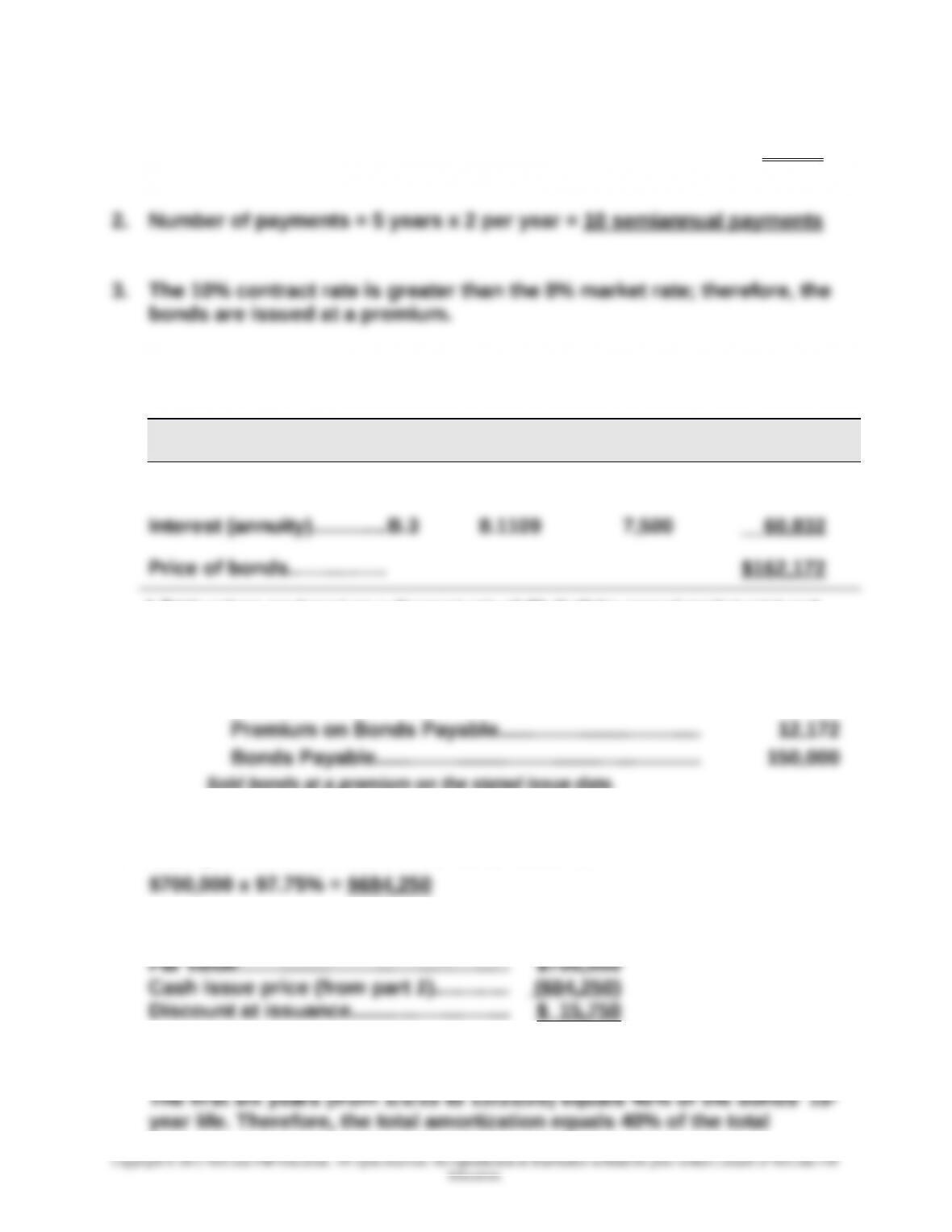

1. Semiannual cash interest payment = $150,000 x 10% x ½ year = $7,500

4. Estimation of the market price at the issue date

Cash Flow Table Table Value* Amount Present Value

Par (maturity) value........B.1 0.6756 $150,000 $101,340

* Table values are based on a discount rate of 4% (half the annual market rate) and

10 periods (semiannual payments).

5. Cash………………………………………………………………………162,172

Sold bonds at a premium on the stated issue date.

Exercise 14-9 (20 minutes)

1. Cash proceeds from sale of bonds at issuance

2. Discount at issuance

3. Total amortization for first 6 years

14-776

4. Carrying value of the bonds at 12/31/2020

Discount at issuance (from part 2)……

$ 15,750

Less amortization (from part 3)...........

Entire Group

Retired 20%

Par value.…………………………………………

$700,000

$140,000

5. Cash purchase price

($700,000 x 20%) x 104.5% = $146,300

6. Loss on retirement

7. Journal entry at retirement for 20% of bonds

2021

Jan. 1 Bonds Payable……………………………………………………….140,000

14-777

Chapter 14 – Long-Term Liabilities

Exercise 14-10 (20 minutes)

1. Amount of each payment = Initial note balance / Table B.3 value

2. Amortization table for the loan

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[7% x (A)]

+

(C)

Debit

Notes

Payable

[(D) – (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

2015....... $100,000 $ 7,000 $ 22,523 $ 29,523 $77,477

2016....... 77,477 5,423 24,100 29,523 53,377

*Adjusted for rounding.

14-778